Finding the Best Small Business Insurance in Utah

Running a small business in Utah means protecting what you’ve built. The right small business insurance Utah coverage shields your company from lawsuits, property damage, and employee-related claims that could otherwise drain your finances.

We at Archibald Insurance Agency help Utah business owners navigate their insurance options without the confusion. This guide walks you through the coverage types you need, how to pick the right provider, and the costly mistakes to avoid.

What Coverage Do Utah Small Businesses Actually Need

General liability insurance sits at the foundation of any Utah small business insurance program. This coverage protects you when a customer or third party claims you caused bodily injury or property damage. A contractor damages a client’s fence. A restaurant customer slips and sues. These situations happen regularly, and general liability absorbs the legal costs and settlement expenses. General liability serves as the baseline coverage for nearly all Utah businesses. Most lenders and landlords require it before you can operate. The typical monthly cost for general liability in Utah runs around $86, though this varies significantly based on your industry and location.

Property Insurance Shields Your Physical Assets

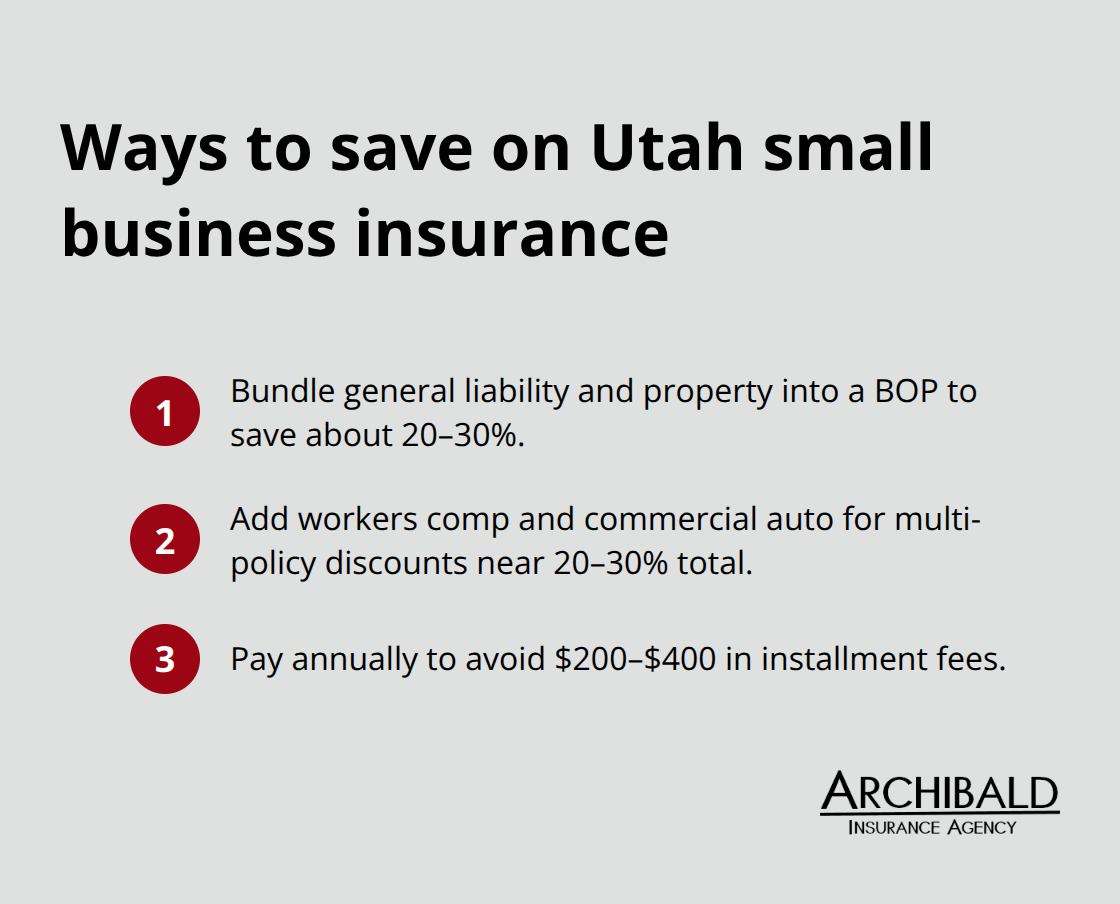

Property insurance covers your building, equipment, inventory, and fixtures if fire, theft, weather, or other covered events damage them. Utah experiences flooding in portions of the state annually, making flood assessment critical for your location. If you lease commercial space, your landlord’s insurance won’t cover your equipment or inventory. If you own the building, you absolutely need this coverage. A manufacturing business loses $50,000 in equipment to a fire. A retail shop’s inventory gets destroyed by water damage. Property insurance handles these losses. For Utah small businesses, bundling property with general liability into a Business Owner’s Policy reduces your total cost by approximately 20 to 30 percent compared to buying separately.

Workers Compensation Is Legally Non-Negotiable

Utah law requires workers compensation insurance from your first employee-there’s no getting around this requirement. In 2022, Utah reported 31,700 non-fatal workplace injuries according to the Bureau of Labor Statistics, with about 87 percent occurring in private sector businesses. Workers compensation covers medical expenses and lost wages if an employee gets injured on the job. It also protects you from lawsuits because employees typically can’t sue their employer when they have workers comp coverage. The average monthly cost in Utah runs approximately $66 for workers compensation. Skipping this coverage exposes your business to massive liability and legal penalties. If you’re a sole proprietor with no employees, you may not need this coverage, but verify your specific situation with a licensed agent since rules vary by business structure.

Location and Industry Shape Your Coverage Needs

Your Utah location and industry type determine which additional coverages matter most. Earthquake coverage becomes important if your business sits near the Wasatch Front fault lines (virtually certain to experience an earthquake in the next 50 years according to the Utah Insurance Department). Flood insurance may be required by lenders for federally backed mortgages. Contractors need general liability of $100,000/$300,000 to maintain Department of Professional Licensing licenses. Service-based businesses benefit from professional liability coverage to protect against negligence claims. Cyber liability protects your company if you hold customer data and face a breach or attack. These additions stack on top of your core coverage, so understanding your specific risks prevents costly gaps later.

Picking the Right Insurance Partner in Utah

Choosing between insurance providers matters far more than most Utah business owners realize. The cheapest quote rarely delivers the best protection, and the flashiest website doesn’t guarantee claims will get paid quickly when disaster strikes. Compare quotes from at least three carriers before deciding, but the comparison must go deeper than price alone.

Compare Coverage Details Across Carriers

Look at what each carrier actually covers. The Hartford offers general liability around $86 monthly with equipment breakdown coverage included, while Simply Business provides broader options like pollution liability and product liability for contractors at about $93 monthly, according to MoneyGeek’s Utah small business insurance study. ERGO NEXT charges roughly $86 monthly and delivers same-day certificates of insurance plus tools and equipment protection up to $50,000 for contractors. These differences matter when you operate in Utah’s diverse business landscape.

Request quotes that show your specific coverage limits, deductibles, and any exclusions that might leave gaps in protection. Ask each carrier whether they cover earthquake damage (critical given the Wasatch Front fault line risk) and flood exposure based on your location. Demand specifics about what’s included and what isn’t rather than accepting vague answers.

Evaluate Claims Support and Speed

Claims support separates reliable insurers from mediocre ones, yet most business owners never test this until they need it. ERGO NEXT processes claims with a 3.9 out of 5 rating while Simply Business scores around 8th nationally for claims speed despite strong digital capabilities. The Hartford maintains faster claims processing, making it the stronger choice if speed matters to your operation.

Ask each carrier their average claims resolution time in writing, and verify they offer 24/7 support for emergencies. Local independent agencies often translate relationships into faster problem-solving than national carriers handling thousands of claims remotely.

Maximize Savings Through Bundling and Payment Options

Bundling coverages cuts your total cost significantly. Combining general liability with property through a Business Owner’s Policy saves roughly 20 to 30 percent compared to purchasing separately. Adding workers compensation and commercial auto to that bundle yields additional multi-policy discounts that can approach 20 to 30 percent total savings.

Paying annually instead of monthly saves approximately $200 to $400 in installment fees. Look for claim-free discounts and safety program credits that reward businesses maintaining good loss history. Independent agencies represent multiple carriers and can access these bundled options across different insurers, whereas captive agents lock you into one company’s pricing and options.

Why Independent Agencies Outperform Captive Agents

An independent agency represents numerous insurance carriers, which means you gain access to competitive quotes and personalized solutions tailored to your specific needs and budget. Captive agents work for a single insurer and cannot shop your coverage across multiple companies. This fundamental difference shapes what you pay and how well your policy actually fits your business. The next section covers the mistakes that cost Utah business owners thousands of dollars annually-and how to avoid them.

What Costs Utah Business Owners the Most When Buying Insurance

Underestimating Coverage Limits Based on Guesses

Most Utah business owners make their first major insurance mistake before they even purchase a policy-they guess at coverage limits instead of calculating actual needs. You look at a general liability quote for $86 monthly with $1 million in coverage and assume that sounds reasonable without analyzing whether your specific operations justify higher or lower limits. A contractor working on residential homes faces different exposure than a consultant working from a home office, yet many business owners purchase identical coverage. This passive approach creates dangerous gaps. A manufacturing business might carry $1 million in property coverage when their equipment and inventory total $2.5 million-leaving them responsible for $1.5 million in losses. A service business might over-insure by purchasing $2 million in coverage when their actual assets total $300,000, wasting thousands annually on unnecessary premiums. Calculate your actual asset values, your potential liability exposure based on your specific operations, and your revenue at risk if business operations stop. Then match coverage limits to those real numbers, not industry guesses.

Skipping Annual Policy Reviews and Updates

The second expensive mistake happens when Utah business owners treat insurance as a set-it-and-forget-it expense rather than a strategic business tool that changes annually. Your business grows, you add employees, you relocate, you purchase new equipment-yet your insurance stays frozen in time. Simply Business offers broader coverage options including pollution liability and product liability for Utah contractors, but you’ll never access these if you never ask about them during annual reviews. ERGO NEXT provides tools and equipment protection for contractors, yet most business owners never discover this option exists. The Hartford includes equipment breakdown coverage with general liability policies, again something most owners miss without deliberate annual conversations with their agent. Your policy purchased three years ago does not account for your current operation, your current revenue, or your current risks. Review your coverage with a licensed agent annually, specifically discussing how your business has changed and what new exposures you’ve created.

Prioritizing Price Over Quality and Claims Performance

Choosing the lowest price without evaluating quality and reliability creates the costliest mistake of all. A $40 monthly general liability policy from an insurer with claims processing rated 8th nationally means you’ll wait months for claims resolution when disaster strikes. The Hartford’s faster claims processing and ERGO NEXT’s same-day certificates of insurance cost slightly more monthly but deliver real value when you need your insurance to actually work. Businesses that choose price-only quotes often face claims denials or glacial processing speeds when they needed protection most. AM Best ratings of A- or higher indicate financial strength and reliable claims support-verify this rating before committing to any carrier. Bundling coverages across multiple carriers saves 20 to 30 percent compared to purchasing separately, making quality coverage more affordable than many business owners assume. An independent agency represents numerous insurance carriers, which means you gain access to competitive quotes and personalized solutions tailored to your specific needs and budget (whereas captive agents work for a single insurer and cannot shop your coverage across multiple companies). This fundamental difference shapes what you pay and how well your policy actually fits your business.

Final Thoughts

Finding the right small business insurance in Utah requires moving beyond price comparisons and understanding what actually protects your operation. General liability, property coverage, and workers compensation form your foundation, but your specific location and industry determine what additional protections matter most. The earthquake risk near the Wasatch Front, annual flooding in portions of Utah, and industry-specific exposures like contractor licensing requirements all shape what you genuinely need. Bundling coverages saves 20 to 30 percent compared to purchasing separately, and paying annually instead of monthly cuts another $200 to $400 from your costs.

Working with a local independent agency transforms how you approach small business insurance Utah coverage. Independent agents represent numerous insurance carriers, which means you access competitive quotes and personalized solutions tailored to your specific needs and budget rather than cookie-cutter policies from a single insurer. Local agents understand Utah’s unique risks, know which carriers perform best in your region, and build relationships that translate into faster problem-solving when you need claims support.

We at Archibald Insurance Agency help Utah business owners navigate their insurance options without confusion. Request quotes from multiple carriers, then schedule a consultation with a licensed agent who understands your operation. Protect what you’ve built by getting coverage that actually matches your business, not generic policies that leave gaps when you need protection most.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation