Salt Lake Auto Quote: What to Expect in 2026

Getting a Salt Lake auto quote in 2026 looks different than it did even a year ago. Repair costs are climbing, electric vehicles are changing the insurance landscape, and new technology is making personalized rates possible.

We at Archibald Insurance Agency want you to understand what’s driving these changes and how they affect your wallet. This guide walks you through the trends shaping quotes right now and shows you how to find coverage that actually fits your needs.

What’s Driving Salt Lake Auto Quotes Higher in 2026

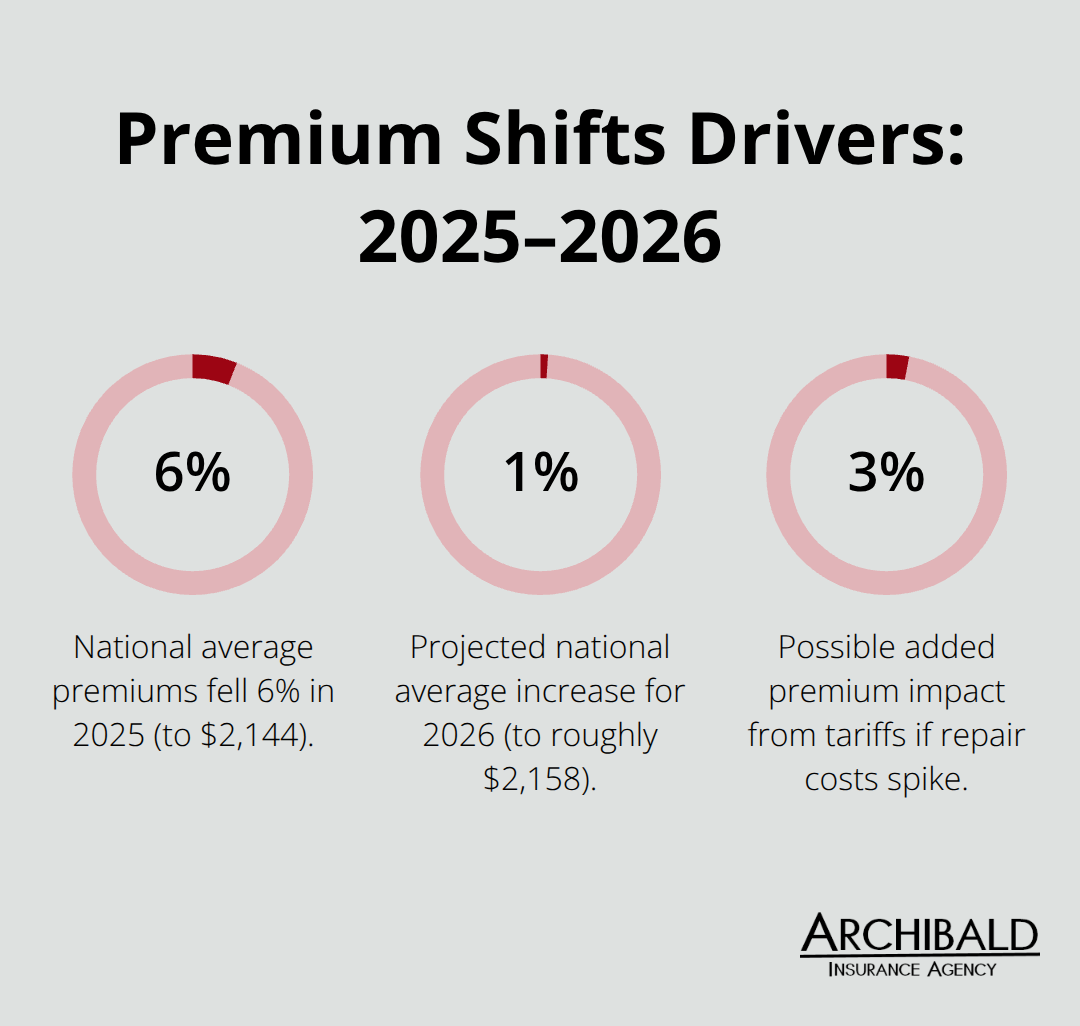

Repair costs stand as the primary reason premiums are climbing across Utah. Construction and repair expenses run significantly higher in densely populated areas like Salt Lake City, and limited supply chains make parts harder to source-this directly inflates what insurers expect to pay for claims. Insurers set premiums based on the expected cost of future claims, so when fixing a vehicle costs more, your quote rises. The national average full-coverage premium fell 6% in 2025 to $2,144 according to Insurify, but 2026 projections show a modest 1% increase to roughly $2,158. Tariffs on auto repair costs could add up to 3 percentage points to premiums if those costs spike, potentially pushing the national forecast from a 1% increase to 4%. For Salt Lake City specifically, full-coverage averages about $1,766 per year, and your ZIP code matters-84108 averages $1,666 annually while 84111 reaches $1,773.

Electric Vehicles Reshape the Rate Picture

Electric vehicles remain more expensive to insure than traditional gas-powered cars, and Tesla models buck broader pricing trends. While 48 of the 50 most-quoted vehicle models saw rate declines in 2025, the Tesla Model S increased 9% and the Model X rose 7%, reflecting higher repair costs and parts availability challenges specific to EVs. If you’re considering an electric vehicle, factor this into your quote expectations. Vehicle type and value significantly impact your rate-a 2012 Ford Focus averages $206.18 monthly while a 2017 RAM 1500 ST reaches $435.70. Safety features provide some relief; newer vehicles with advanced safety systems qualify for discounts that partially offset higher premiums from increased replacement value.

Telematics Technology Unlocks Lower Rates

Usage-based insurance programs track your actual driving patterns through telematics devices, monitoring speeding, hard braking, rapid acceleration, and sharp turns. This data collection can reduce your premium by up to 30%, making it one of the most tangible ways to lower what you pay in 2026. Poor driving habits will increase your rate, so this approach only works if you drive safely. Ask your agent whether telematics could reduce your premium before committing to a policy. This technology personalizes rates in ways that traditional underwriting cannot, rewarding safe drivers with concrete savings rather than generic discounts.

Understanding these three forces-repair costs, vehicle type, and driving behavior-positions you to make informed decisions when shopping for coverage. The next section shows you exactly which factors affect your individual quote and how your specific situation in the Salt Lake area influences what you’ll pay.

What Shapes Your Salt Lake Quote

Your Salt Lake auto quote reflects a precise calculation of your risk profile, and three factors dominate that calculation in 2026. The vehicle you drive, your history behind the wheel, and where you live create a financial blueprint that insurers use to price your coverage. Understanding these factors gives you concrete control over what you pay.

Vehicle Type and Replacement Cost

The car itself matters enormously. A 2012 Ford Focus averages $206.18 monthly while a 2017 RAM 1500 ST reaches $435.70, a stark difference driven by replacement cost and repair expenses. Car models with lower safety ratings, high repair costs, and more insurance claims may have a higher insurance rate, making a safety-equipped 2023 model potentially cheaper to insure than an older car without such systems.

Location and ZIP Code Impact

In Salt Lake City, your ZIP code determines a significant portion of your rate. ZIP code 84108 averages $1,666 annually for full coverage while 84111 reaches $1,773-a $107 difference based purely on location. High-crime areas and densely populated neighborhoods carry higher risk assessments. Garage storage matters here; storing your vehicle in a secure structure rather than on the street can lower premiums because theft risk drops measurably.

Driving Record and Claims History

Your driving record and claims history operate as the second major lever on your quote. A speeding ticket typically raises car insurance rates by about 25%. A DUI carries far steeper penalties and can stay on your record longer depending on the state. Claims history works similarly-insurers expect future claims based on past behavior, so two accidents in three years will push your quote higher than a clean record.

Telematics and Driving Behavior

Telematics devices offer a direct path to lower rates by proving your actual driving patterns. Safe drivers who avoid hard braking, speeding, and rapid acceleration can reduce premiums by up to 30%, making this technology a practical tool rather than a theoretical discount. Ask your agent whether telematics could reduce your premium before committing to a policy.

Credit Score and Annual Mileage

Your insurance score, driven by credit-based factors, influences premiums as well. Drivers with poor credit pay substantially more; GEICO quotes bad-credit drivers at $1,872 annually versus $1,042 for standard drivers, an $830 annual difference. Annual mileage compounds these factors-drivers who commute long distances face higher premiums than those who drive occasionally. These elements interact, so a young driver with a clean record in a high-crime ZIP code pays differently than an older driver with a ticket in a suburban area. When you compare auto insurance quotes across multiple carriers, you’ll discover wide price variation for identical coverage. The next section shows you how to navigate this complexity and find the coverage that matches both your needs and your budget.

Finding the Right Quote for Your Situation

Compare Quotes Across Multiple Carriers

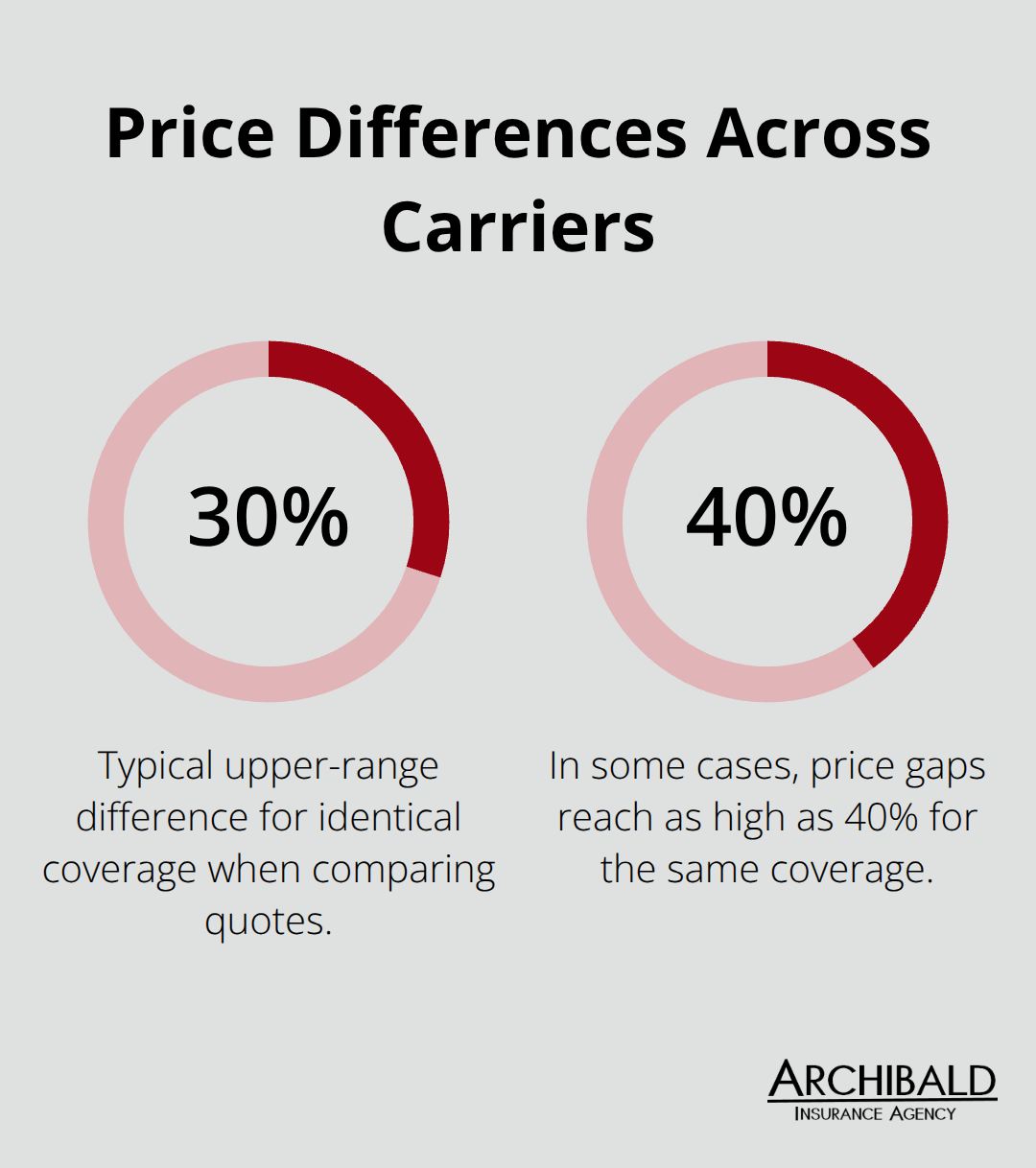

Shopping for auto insurance quotes in Salt Lake City means comparing not just price tags but actual coverage structures across carriers that price risk differently. GEICO offers the cheapest liability coverage in Salt Lake City, with an average rate of $1,248 per year according to NerdWallet’s July 2026 analysis, reflecting how each carrier weights factors like your ZIP code, vehicle type, and driving history. Request quotes from at least three carriers to reveal these gaps immediately. When you request quotes, provide identical coverage limits across all carriers so you compare apples to apples, not mixing $250 deductibles with $1,000 deductibles.

Your specific situation matters enormously here, so a 40-year-old with a clean record and a 2015 sedan will see entirely different pricing than a 25-year-old with a speeding ticket driving a 2023 truck. Online quote systems often miss discounts that phone conversations uncover. Call carriers directly to discuss household bundling, safety features on your vehicle, or professional affiliations that trigger lower rates.

Leverage Bundling and Standard Discounts

Discounts operate as your second lever for reducing what you pay. Bundling auto insurance with homeowners or rental coverage typically saves 15 to 25 percent on your auto premium, making this the single most effective discount available. Ask carriers about defensive driving course discounts, claims-free discounts for going several years without filing a claim, and discounts for vehicles equipped with advanced safety features like automatic emergency braking. Credit union memberships qualify for member-exclusive rates at many carriers.

Mileage discounts deserve attention as well, particularly if you work from home or drive infrequently. If you drive under 7,500 miles annually, mention this explicitly because some carriers offer meaningful savings for low-mileage drivers. These discounts stack, so a driver who bundles policies, maintains a clean record, and drives infrequently can reduce premiums substantially.

Unlock Savings Through Telematics Programs

Telematics programs deserve special attention because they operate differently than traditional discounts. These programs reduce rates through demonstrated safe driving rather than static discounts, with safe drivers saving up to 30 percent based on how you drive. Telematics devices track your actual behavior and reward safe habits with concrete savings. Many drivers overlook this option entirely, missing one of the most powerful rate-reduction tools available in 2026.

Work with an Independent Agent

An independent agent in Salt Lake City can access multiple carriers simultaneously and knows which ones offer which discounts, saving you hours of phone calls while identifying combinations you might miss calling carriers individually. Independent agents represent numerous insurance carriers, which means they can compare options across the market rather than pushing a single company’s products. This approach typically uncovers better pricing and more comprehensive coverage options than shopping alone.

Final Thoughts

Repair costs keep climbing, your vehicle type and driving behavior directly shape what you pay, and multiple carriers price risk differently for your Salt Lake auto quote. The national average full-coverage premium will rise about 1% to roughly $2,158 in 2026, but Salt Lake City drivers have concrete tools to manage costs through telematics programs that reward safe driving with savings up to 30%, bundling discounts that stack meaningfully, and comparing quotes across carriers to reveal price gaps exceeding $1,000 annually for identical coverage. Professional guidance matters because independent agents access multiple carriers simultaneously and know which discounts apply to your specific situation.

We at Archibald Insurance Agency represent numerous insurance carriers, which means we compare options across the market rather than steering you toward a single company’s products. Your ZIP code, vehicle type, driving record, and annual mileage create a unique financial profile that requires personalized analysis, not generic online quotes. This approach typically uncovers better pricing and more comprehensive coverage than shopping alone.

Contact Archibald Insurance Agency to discuss your coverage needs and receive quotes tailored to your situation. Our team identifies which discounts apply to you, explains how telematics could lower your rate, and shows you exactly what full coverage costs in your specific ZIP code. We build lasting relationships based on trust and reliability, which means we invest in finding you coverage that actually protects your needs without overpaying.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation

For those of us who have a passion for collecting classic cars, it’s important to have an insurance policy that aligns with our specific use and ensures the appropriate value coverage for these valuable assets. Insuring a classic car is different from insuring your everyday vehicle. Classic car insurance policies are typically more affordable and are based on an agreed value. These policies can be tailored to suit your specific vehicle, restoration stage, or usage. Here are some examples of how you can customize your classic car insurance policy:

For those of us who have a passion for collecting classic cars, it’s important to have an insurance policy that aligns with our specific use and ensures the appropriate value coverage for these valuable assets. Insuring a classic car is different from insuring your everyday vehicle. Classic car insurance policies are typically more affordable and are based on an agreed value. These policies can be tailored to suit your specific vehicle, restoration stage, or usage. Here are some examples of how you can customize your classic car insurance policy: