Utah Car Insurance Quotes: Compare Top Rates Fast

Utah car insurance rates vary significantly based on your driving history, vehicle type, and coverage choices. We at Archibald Insurance Agency help drivers cut through the confusion by showing you how to find the best Utah car insurance quotes for your situation.

Getting multiple quotes takes just minutes and can save you hundreds annually. This guide walks you through the factors that impact your premiums and the smart strategies to lower them.

What Impacts Your Utah Car Insurance Premium

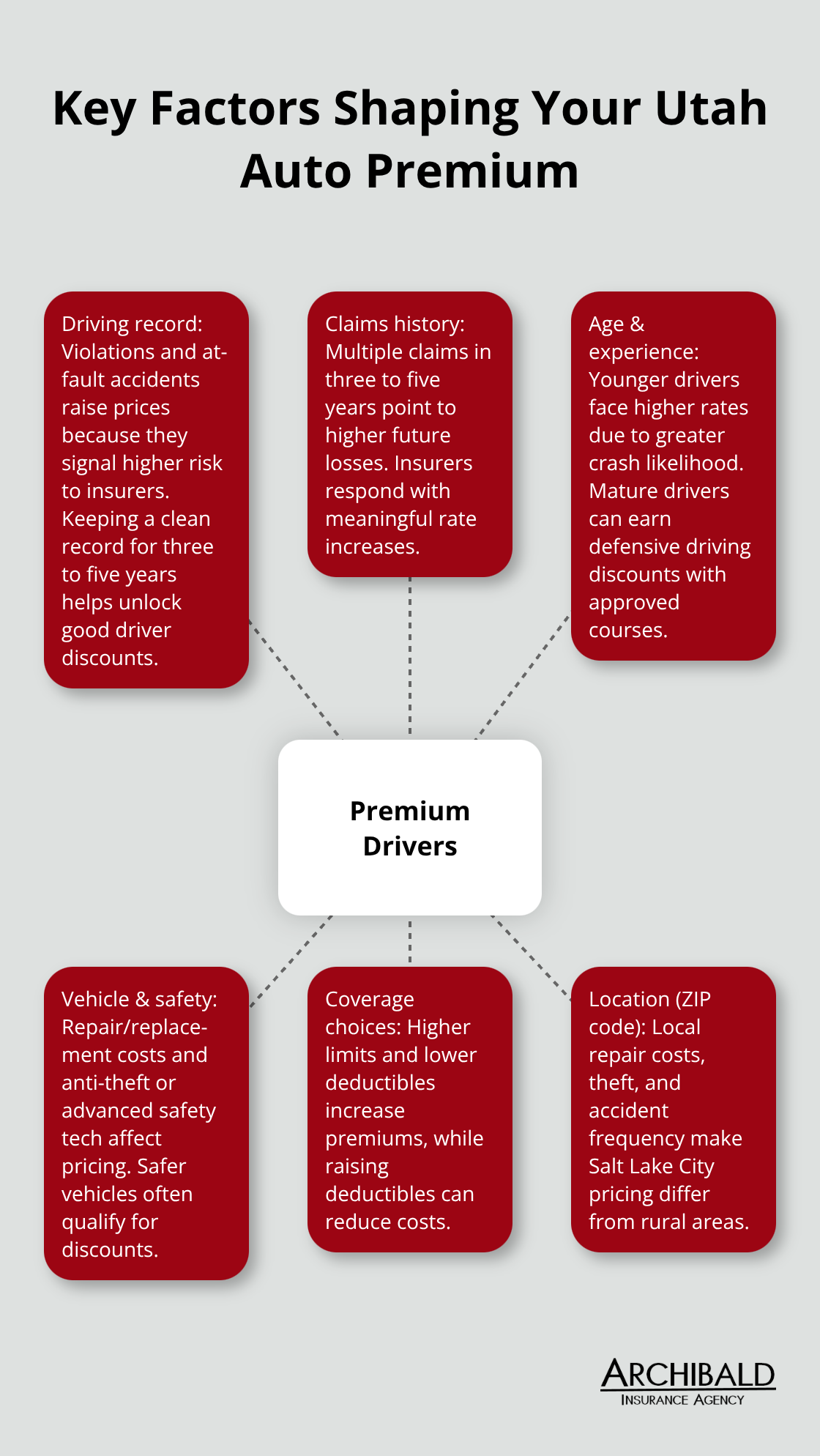

Your Utah car insurance premium isn’t random-insurers calculate it based on measurable risk factors tied directly to you, your vehicle, and your coverage choices. Understanding these factors helps you see why quotes differ and where you can make adjustments.

How Your Driving Record Sets Your Rate

Your driving record carries substantial weight in premium calculations. A single traffic violation increases your premium by 10–15%, while at-fault accidents typically push rates up 25–40% depending on severity. Utah law requires proof of insurance, and the state’s Insure-Rite system cross-checks registered vehicles against insurer records-uninsured operation convictions start at $400 for first offenses and escalate quickly, which directly influences how insurers price risk in the state.

Your claims history matters as much as violations. Multiple claims within three to five years signal higher risk, and insurers respond with meaningful rate increases. A clean driving record for the past three to five years qualifies you for good driver discounts that can reduce premiums substantially.

Age and Driving Experience

Age and driving experience factor in significantly. Drivers under 25 face higher premiums across the board because they are new to the road and more likely to be involved in crashes. Conversely, drivers aged 55 and older who complete an eligible Utah accident prevention course within the last three years qualify for defensive driving discounts that last for three years, making recertification a smart move before renewal.

Vehicle Type and Coverage Shape Your Cost

The vehicle you drive directly affects repair and replacement costs, which insurers account for in premiums. Older vehicles with lower market values may justify dropping comprehensive or collision coverage if you can absorb repair costs yourself-this single decision can lower your annual premium by several hundred dollars.

Safety features matter too. Vehicles with robust anti-theft systems and advanced safety technology may qualify for vehicle safety discounts based on the vehicle’s claims record from the prior seven model years. Your coverage limits and deductible choices create a direct relationship with your premium. Increasing your deductible from $500 to $1,000 typically lowers your premium 10–15%, and choosing lower liability limits reduces your cost immediately (though this approach carries real financial risk if you cause significant damage or injury).

These rate factors explain why your neighbor’s quote differs from yours. The next section shows you how to offset these costs through strategic discounts and smart policy choices.

How to Cut Your Utah Car Insurance Cost

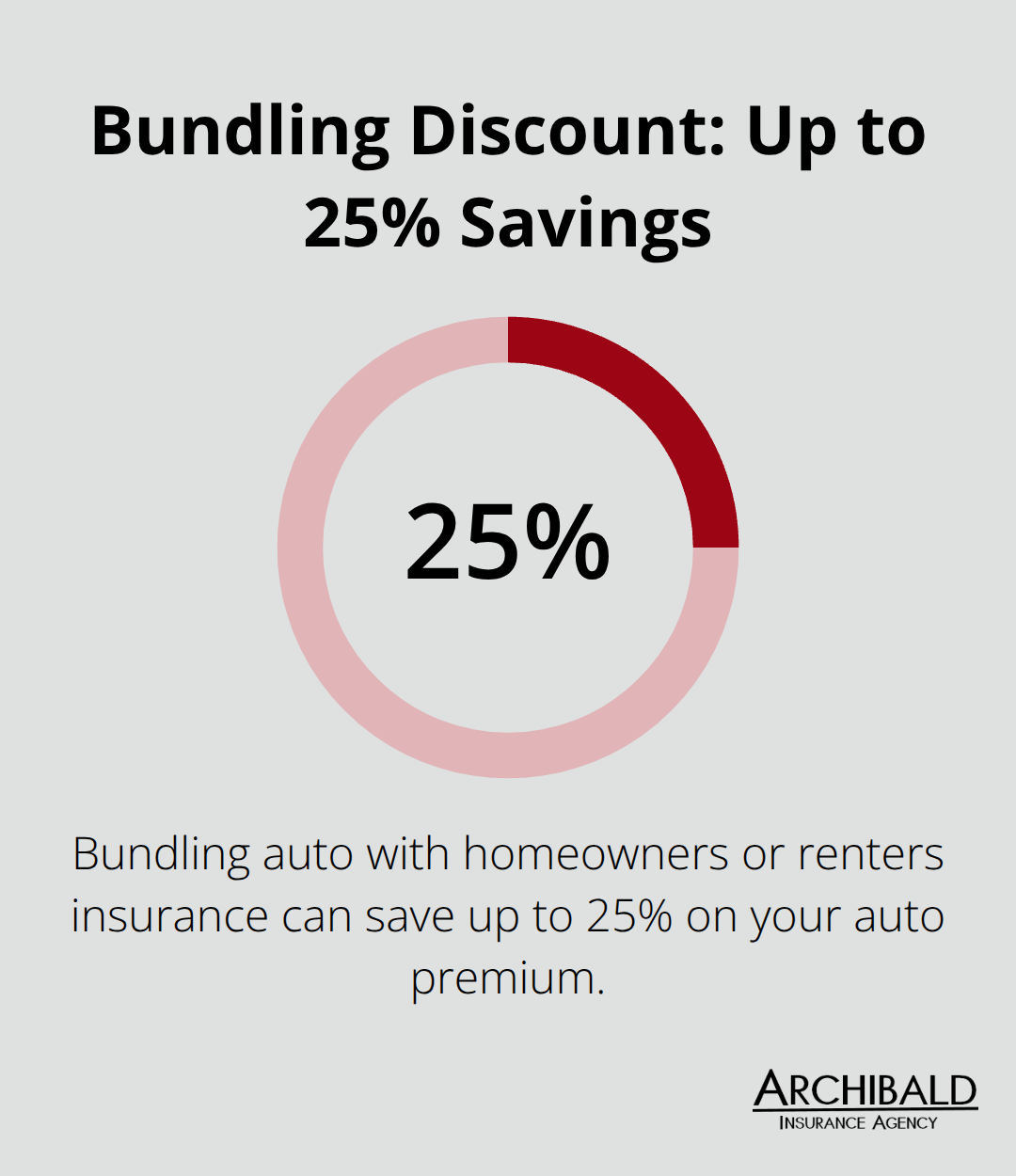

Lowering your Utah car insurance premium requires concrete action, not waiting for rate decreases or switching insurers repeatedly. Actions you take today directly reduce what you pay. Bundling your auto policy with homeowners or renters insurance cuts premiums across both policies, typically saving up to 25% on your auto coverage alone. If you own a home or rent, this single action often delivers the fastest savings.

Build Savings Through Your Driving Record

A clean driving record over the past three to five years qualifies you for good driver discounts that reward your safety. If you’ve had violations, focus on maintaining clean driving going forward-insurers reset their risk assessment gradually, and staying violation-free for three years positions you for meaningful rate reductions at renewal. Utah drivers under 25 who complete the Steer Clear Safe Driver Program can access premium reductions. Drivers 55 and older who finish an eligible accident prevention course within three years lock in defensive driving discounts lasting three years before recertification becomes necessary.

Install Protective Technology and Safety Features

Installing anti-theft devices and safety features like GPS tracking, alarm systems, or advanced collision avoidance technology directly lowers your premium. Insurers recognize these reduce claim frequency and severity, translating to discounts. Some vehicles qualify for vehicle safety discounts based on their claims history, so newer vehicles with strong safety records may carry lower premiums than older models with higher damage histories.

Optimize Your Coverage and Payment Strategy

The vehicle you drive directly affects repair and replacement costs. Older vehicles with lower market values may justify dropping comprehensive or collision coverage if you can absorb repair costs yourself-this single decision can lower your annual premium by several hundred dollars. Paying your annual premium upfront instead of monthly installments eliminates financing fees and sometimes qualifies you for an additional discount (typically 3–5% savings for advance payment).

Progressive’s Snapshot program reports average savings of $322 annually for enrolled customers who demonstrate safe driving habits through telematics monitoring. Your zip code matters significantly in Utah-rates vary sharply between Salt Lake City and rural areas due to repair costs, theft rates, and accident frequency. Shopping quotes every 6 to 12 months captures rate changes and new discounts you may qualify for.

Compare Quotes to Unlock Your Best Rate

The combination of bundling, maintaining safety, installing protective devices, and paying upfront typically reduces your total annual cost by 30–40% compared to a baseline policy with no discounts and monthly payments. However, these savings only materialize when you compare quotes across multiple carriers with identical coverage limits and deductibles-a step that reveals which insurers offer the best value for your specific situation.

Comparing Quotes Across Multiple Carriers

Shopping quotes from just one or two insurers leaves money on the table. Rates for identical coverage vary dramatically across carriers in Utah-some drivers save $461 annually simply by switching to a competitor offering the same protection. State Farm, Progressive, GEICO, Allstate, Bear River, Farm Bureau, and Auto-Owners all operate in Utah, yet their pricing models differ significantly based on how they assess risk and apply discounts. A driver with a clean record and bundled policies might find State Farm cheaper, while another with a young driver household could see lower Progressive quotes. The only way to know which insurer values your profile most favorably is to request quotes from at least three to five carriers. This takes roughly 15–20 minutes per quote and often reveals $300+ annual savings compared to your current policy.

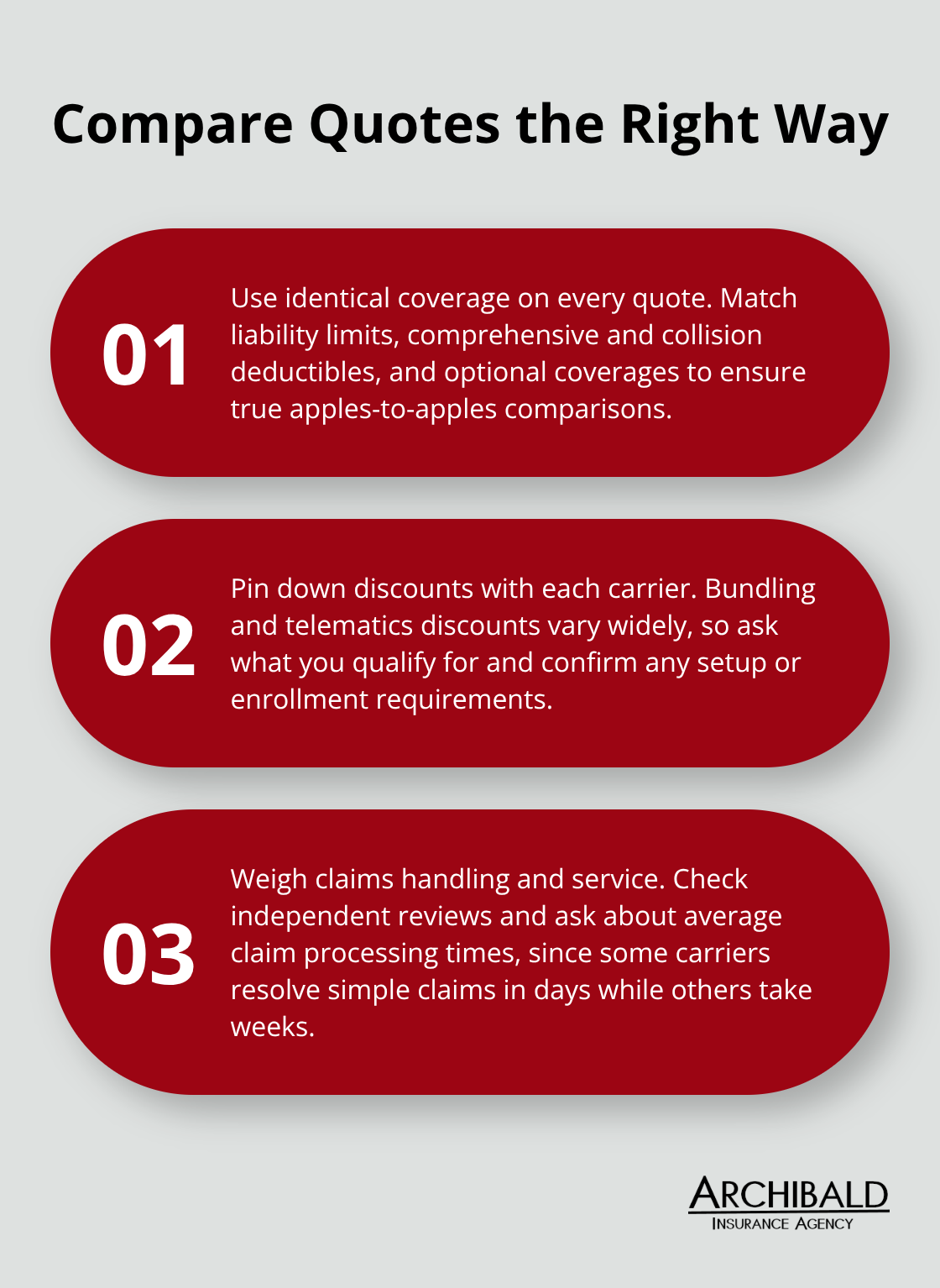

Lock in Identical Coverage Across All Quotes

When you gather quotes, use identical coverage limits and deductibles across every single request. If you compare a $250 deductible with one insurer against a $1,000 deductible with another, you’re not actually comparing rates-you’re comparing different products. Utah requires minimum liability coverage including No-Fault, Bodily Injury, and Property Damage, but your optimal limits depend on your assets and risk tolerance. Request quotes with the same liability limits (many Utah drivers choose $100,000/$300,000/$100,000), the same collision and comprehensive deductibles, and the same optional coverages like rental reimbursement or uninsured motorist protection. This apples-to-apples approach reveals which insurer truly offers the best rate for your situation.

Identify Discounts That Apply to Your Profile

Discounts vary dramatically between carriers-one insurer might offer a 15% bundling discount while another offers 25%, and a telematics program discount could range from 10–30% depending on the carrier. Ask each insurer specifically what discounts you qualify for based on your profile. Some carriers require enrollment or setup before discounts apply, so confirm timing and requirements with each company.

Evaluate Claims Handling and Service Quality

Customer service quality matters when claims arise. Farm Bureau and Auto-Owners receive positive feedback from collision shop professionals regarding repair authorization speed and claims handling, while experiences with larger national carriers vary widely. Check online reviews on independent platforms and ask potential insurers about their average claims processing time-some handle simple claims in days, others in weeks.

Account for Your Utah Location in Rate Quotes

Your zip code in Utah dramatically affects pricing due to local repair costs, theft rates, and accident frequency. Salt Lake City quotes differ sharply from rural areas, so obtain quotes specific to your actual location where you garage your vehicle. Independent insurance agents representing multiple carriers can handle quote requests across several companies simultaneously, saving you time and often delivering more competitive rates than direct online quotes because they can access both stock and mutual insurers.

Final Thoughts

Finding affordable Utah car insurance quotes requires comparing multiple carriers with identical coverage limits, understanding which rate factors you can control, and taking action on discounts that apply to your situation. The strategies in this guide-bundling policies, maintaining a clean driving record, installing safety devices, and requesting quotes from at least three to five insurers-typically reduce your annual premium by 30–40% compared to a baseline policy. Your zip code in Utah matters significantly, repair costs vary by location, and carrier pricing models differ substantially, which means the cheapest option for your neighbor may not be the cheapest for you.

Independent insurance agencies remove the guesswork from this process because they represent multiple carriers and access both stock and mutual companies, giving you genuine options rather than a single company’s pricing. An independent agent requests quotes across several insurers simultaneously, saving you hours of phone calls and online forms while understanding Utah’s specific insurance requirements and local market conditions. They review your coverage annually to catch new discounts or rate reductions you may have missed.

We at Archibald Insurance Agency are a family-owned, independent agency in Salt Lake City specializing in auto, home, business, and life insurance. Contact Archibald Insurance Agency for a personalized quote, and our team will gather your information once, request quotes from multiple carriers with your exact coverage needs, and present you with side-by-side comparisons showing price, discounts, and service ratings.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation

Owning a swimming pool is a delightful luxury that requires diligent maintenance, but the joy it brings on a scorching summer day is truly priceless. If you have children, the pool quickly becomes their favorite gathering spot with friends. While owning a swimming pool can offer a fantastic experience, it also comes with a unique insurance liability risk.

Owning a swimming pool is a delightful luxury that requires diligent maintenance, but the joy it brings on a scorching summer day is truly priceless. If you have children, the pool quickly becomes their favorite gathering spot with friends. While owning a swimming pool can offer a fantastic experience, it also comes with a unique insurance liability risk.