Family Car Insurance Utah: Protecting Your Loved Ones on the Road

Every day, Utah families navigate roads with real risks-accidents happen, and the right insurance makes all the difference.

Family car insurance in Utah isn’t just a legal requirement; it’s your financial safety net when the unexpected occurs. We at Archibald Insurance Agency help families understand their coverage options so they can drive with confidence.

What Coverage Do Utah Families Actually Need?

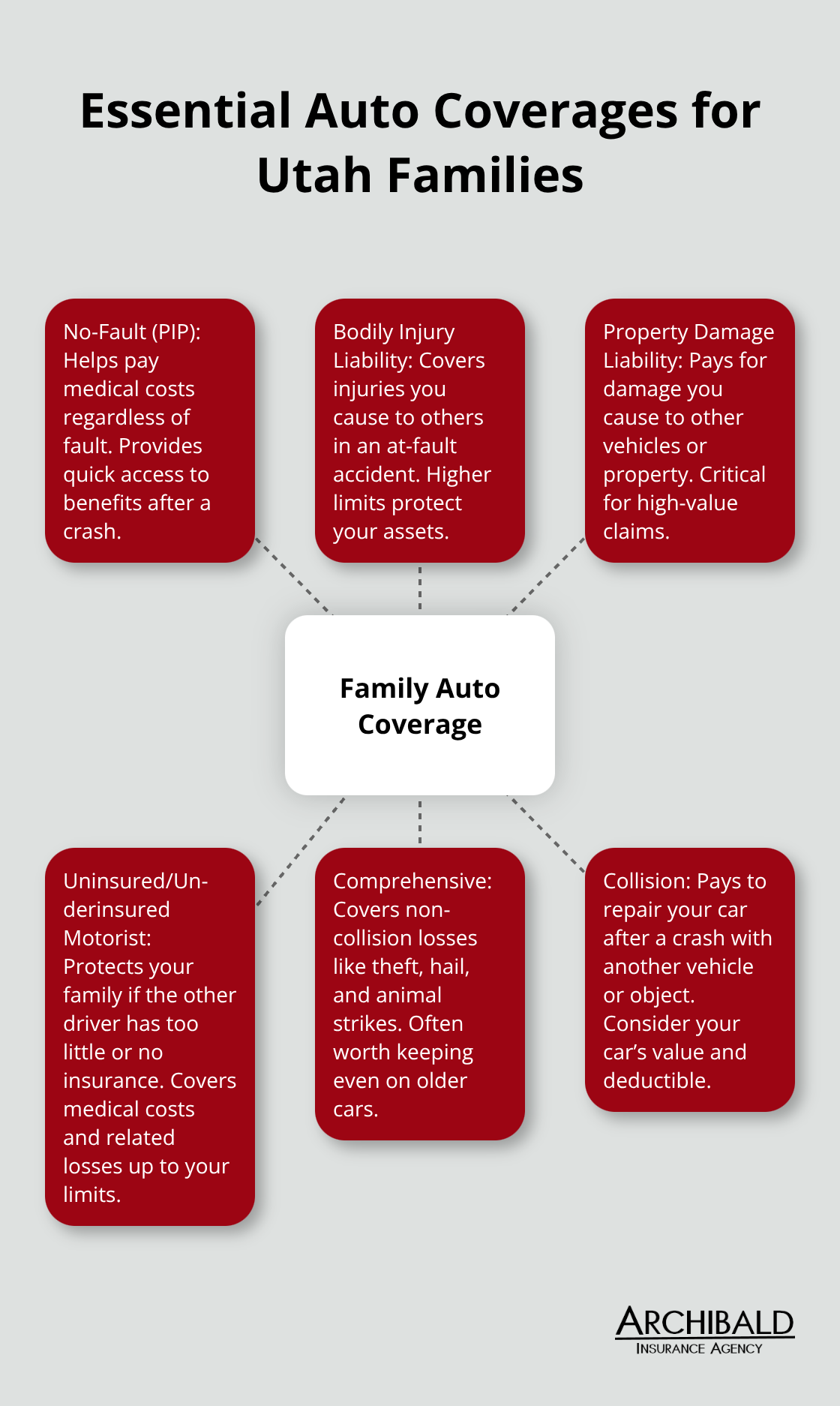

Utah law requires all registered vehicles to carry No-Fault coverage, bodily injury liability, and property damage liability under Utah Code Ann. §31A-22-302, but minimum coverage alone leaves most families dangerously exposed. The state minimum liability limits fail to protect your family’s assets if you cause a serious accident. We recommend carrying liability limits well above the state minimum-at least 100/300/100, meaning $100,000 per person and $300,000 per accident for bodily injury, plus $100,000 for property damage. This protects your family’s home, savings, and future income if a lawsuit follows an at-fault collision.

Comprehensive and Collision Coverage for Your Vehicles

Comprehensive and collision coverage protects your own vehicles from damage caused by accidents, theft, weather, or vandalism. Comprehensive covers non-collision events like hail, theft, and animal strikes, while collision covers damage from accidents with other vehicles or objects. For vehicles financed or leased, lenders require both coverages; for owned vehicles, the decision depends on your car’s value and your financial situation.

If your vehicle is worth less than $5,000, dropping collision coverage may make financial sense, but comprehensive is worth keeping for theft and weather protection.

Uninsured and Underinsured Motorist Protection

Uninsured motorist coverage protects your family when another driver causes an accident but lacks adequate insurance-a real problem in Utah where some drivers still operate uninsured despite legal penalties starting at $400 for first offenses. Nearly 1 in 8 drivers nationally operate without insurance, according to the Insurance Research Council, and Utah’s Insure-Rite verification system has identified thousands of uninsured vehicles. When an uninsured driver hits your family, your uninsured motorist coverage steps in to pay for medical expenses, lost wages, and pain and suffering up to your coverage limit. Underinsured motorist coverage fills the gap when another driver’s insurance limits fall short of covering your family’s damages. Try setting these limits equal to your liability limits-if you carry 100/300 liability, carry 100/300 uninsured and underinsured motorist coverage.

Medical Payments Coverage for Immediate Protection

Medical payments coverage or personal injury protection, available depending on your insurer, pays medical bills regardless of fault, which matters for families with young children or members with existing health conditions. This coverage activates immediately after an accident and covers hospital visits, surgeries, and rehabilitation without waiting for a liability determination. Utah families with multiple drivers or teenage drivers should seriously consider medical payments coverage, since even low-speed accidents can trigger expensive emergency room visits. Your choice of coverage limits and deductibles directly shapes how well your family is protected when accidents happen-and the next section shows you how to evaluate these options against your family’s actual driving patterns and financial situation.

Choosing the Right Coverage for Your Family’s Situation

Map Your Household’s Actual Driving Patterns

Your family’s insurance needs depend entirely on how you actually drive, not on what the law requires or what your neighbor carries. Start by documenting your household’s driving patterns over the past year-annual mileage, commute distances, whether teen drivers participate, and how often you drive in winter conditions. A family with one parent commuting 40 miles daily in Salt Lake City faces different risks than a family using vehicles primarily for weekend errands in rural areas. Driving patterns and risk factors like urban theft and accident rates differ from rural driving, which increases comprehensive claims from weather and animal strikes. Document these patterns honestly, because they directly determine whether you need higher liability limits, comprehensive coverage, or medical payments protection.

Account for Teen Drivers in Your Premium Calculations

If your household includes a teen driver under 21, expect your premiums to increase significantly, which makes every coverage decision more expensive and therefore more important to get right. This reality forces families to think strategically about which coverages matter most and where they can adjust deductibles to manage costs without sacrificing protection.

Compare Deductibles Across Coverage Types

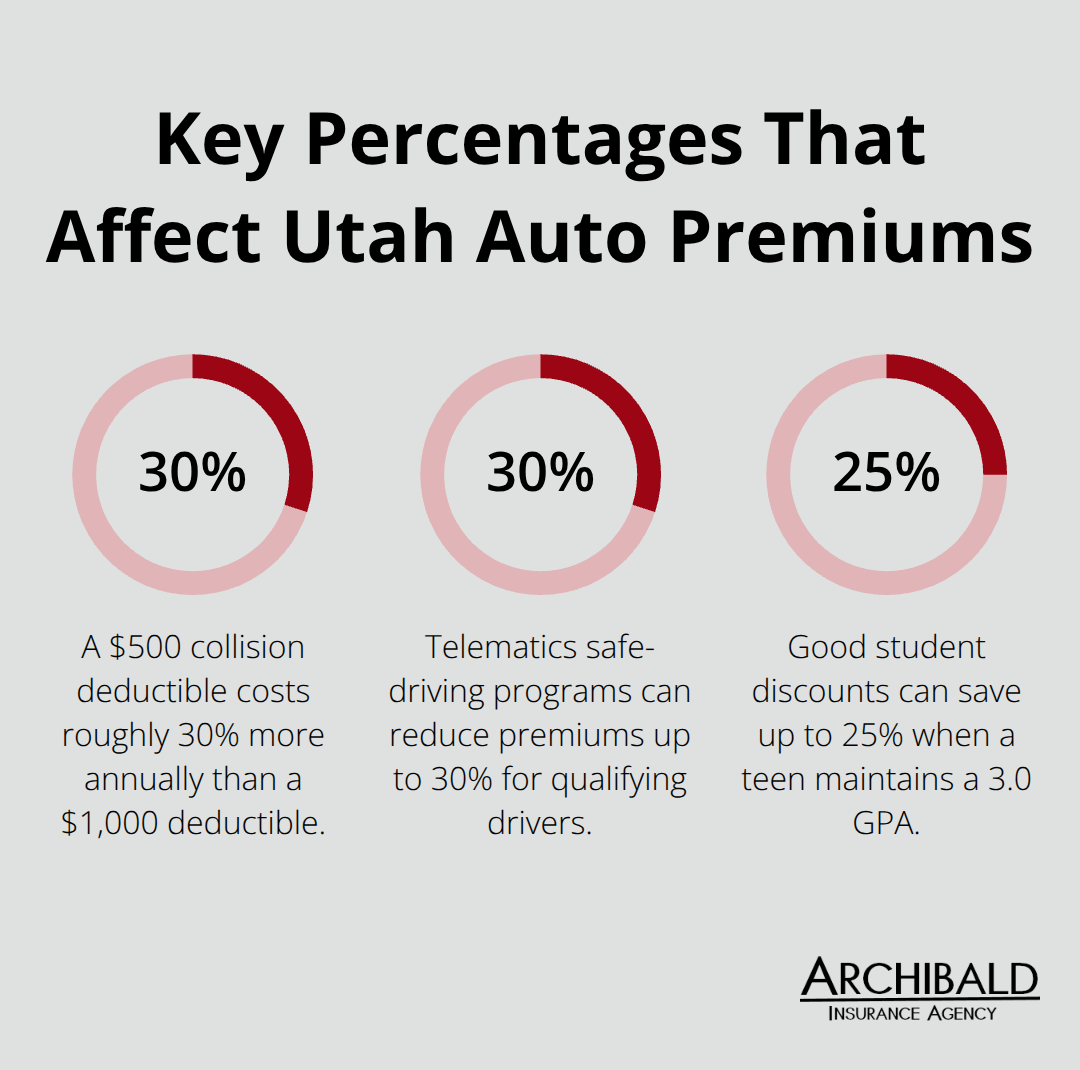

Comparing deductibles across coverage types is where most families leave money on the table. A $500 collision deductible costs roughly 30 percent more annually than a $1,000 deductible, but you only benefit from that lower deductible if you file a claim-and most drivers go years without filing one. If you have three months of expenses in savings, a $1,000 deductible is financially sensible and cuts your annual premium substantially.

However, if your vehicle is financed or leased, your lender mandates specific deductible limits, typically $500 or $1,000 maximum.

Verify Credit-Based Scoring and Stack Your Discounts

Utah families should verify whether their chosen insurer applies credit-based scoring to pricing, since some carriers weight credit history heavily in their rate calculations. Discount stacking matters more than any single coverage choice-bundling auto with homeowners or renters insurance, enrolling in telematics programs like Drive Safe & Save that can reduce premiums up to 30 percent for safe drivers, maintaining a clean driving record, and qualifying for good student discounts if your teen maintains a 3.0 GPA or higher can collectively save your family hundreds annually. Request quotes from at least three different carriers and ask each agent specifically which discounts apply to your household; many families miss savings simply because they don’t ask. These conversations with agents reveal which carriers offer the best combination of rates and discounts for your specific situation-and that’s where the real work of selecting the right plan begins.

Where Utah Families Waste the Most Money on Auto Insurance

Minimum Liability Coverage Leaves Your Assets Exposed

Utah families routinely make three expensive mistakes when selecting auto insurance, and each one costs hundreds or thousands of dollars over time. The first mistake is selecting minimum liability coverage strictly to lower premiums without understanding that Utah’s state minimums provide almost no asset protection. Utah requires only 25/65/15 liability coverage (meaning $25,000 per person, $65,000 per accident for bodily injury, and $15,000 for property damage), which sounds adequate until a serious accident happens. If your teenage driver causes an accident that injures multiple people or damages expensive property, the injured parties will pursue claims against your family’s assets when your insurance limits run out. A single at-fault accident involving serious injuries can generate medical bills exceeding $200,000 to $500,000, and when your policy covers only $25,000 per person, a lawsuit targeting your home and savings becomes inevitable.

Carrying at least 100/300/100 coverage costs roughly $20 to $40 more monthly than minimum coverage but protects your family’s financial future. That $30 monthly difference amounts to $360 annually, a trivial cost compared to defending a lawsuit or losing your home.

Annual Policy Reviews Catch Coverage Gaps and New Discounts

The second mistake is failing to review policies annually, which means families miss changing life circumstances and new discount opportunities. A family that bundled auto and homeowners insurance five years ago might have switched homes, changed jobs, or added a teen driver without updating their agent, missing potential discounts or leaving dangerous coverage gaps. Utah families should review policies each year in January or when major life changes occur-adding a teen driver, purchasing a second vehicle, moving to a different neighborhood, or paying off a vehicle loan. Life changes shift your risk profile, and your coverage should shift with it. An agent who understands your household can identify discounts you never knew existed and adjust deductibles to match your current financial situation.

Discount Stacking Delivers Savings Most Families Never Claim

The third mistake is not stacking discounts aggressively, since most Utah families qualify for multiple discounts they never claim. A family with a teen driver who maintains a 3.0 GPA qualifies for good student discounts up to 25 percent, yet many parents never mention their child’s grades to their agent. Bundling auto with homeowners or renters insurance typically saves 15 to 25 percent on both policies combined. Enrolling in telematics programs like Drive Safe & Save can reduce premiums up to 30 percent for drivers with safe habits, but requires intentional enrollment and setup. A household with two vehicles, a good student driver, bundled home insurance, and a telematics program active could save $1,500 to $2,500 annually compared to a family carrying minimum coverage with no discounts applied (yet most families never calculate or pursue this combination strategically). The gap between what families actually pay and what they could pay through smart discount stacking represents the largest waste in Utah auto insurance.

Final Thoughts

Protecting your family on Utah roads requires three concrete actions: carry liability coverage well above state minimums, stack every discount your household qualifies for, and review your policy annually when life changes occur. Family car insurance in Utah isn’t about meeting legal requirements-it’s about ensuring that an accident doesn’t destroy your family’s financial security. The families who sleep soundly at night aren’t those with minimum coverage; they’re the ones who took time to assess their actual driving patterns, compared deductibles honestly against their savings, and built a coverage plan that matches their real situation.

A local agent makes this process dramatically simpler because they understand Utah’s specific risks-winter driving conditions, rural road hazards, and the prevalence of uninsured motorists in your area. An agent who knows your household identifies discount combinations you’d never find alone and adjusts your coverage when you add a teen driver, purchase a second vehicle, or move to a different neighborhood. We at Archibald Insurance Agency specialize in this work as an independent agency representing numerous carriers, which means we compare options across multiple insurers rather than locking you into a single company’s limited choices.

Your next step is straightforward: gather your household’s driving information, document your vehicles and drivers, and contact an agent to compare quotes from at least three carriers. Ask specifically which discounts apply to your situation-good student discounts, bundling savings, telematics programs, and multi-vehicle discounts add up quickly. Contact Archibald Insurance Agency to ensure your current coverage matches your family’s needs and budget.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation