Utah Life Insurance Basics: Essentials For Utah Families

Life insurance is one of the most important financial decisions Utah families make, yet many put it off because they’re unsure where to start.

At Archibald Insurance Agency, we’ve helped countless Utah families understand life insurance basics and find coverage that actually fits their situation. This guide walks you through what you need to know to protect your loved ones.

Why Life Insurance Protects What Matters Most

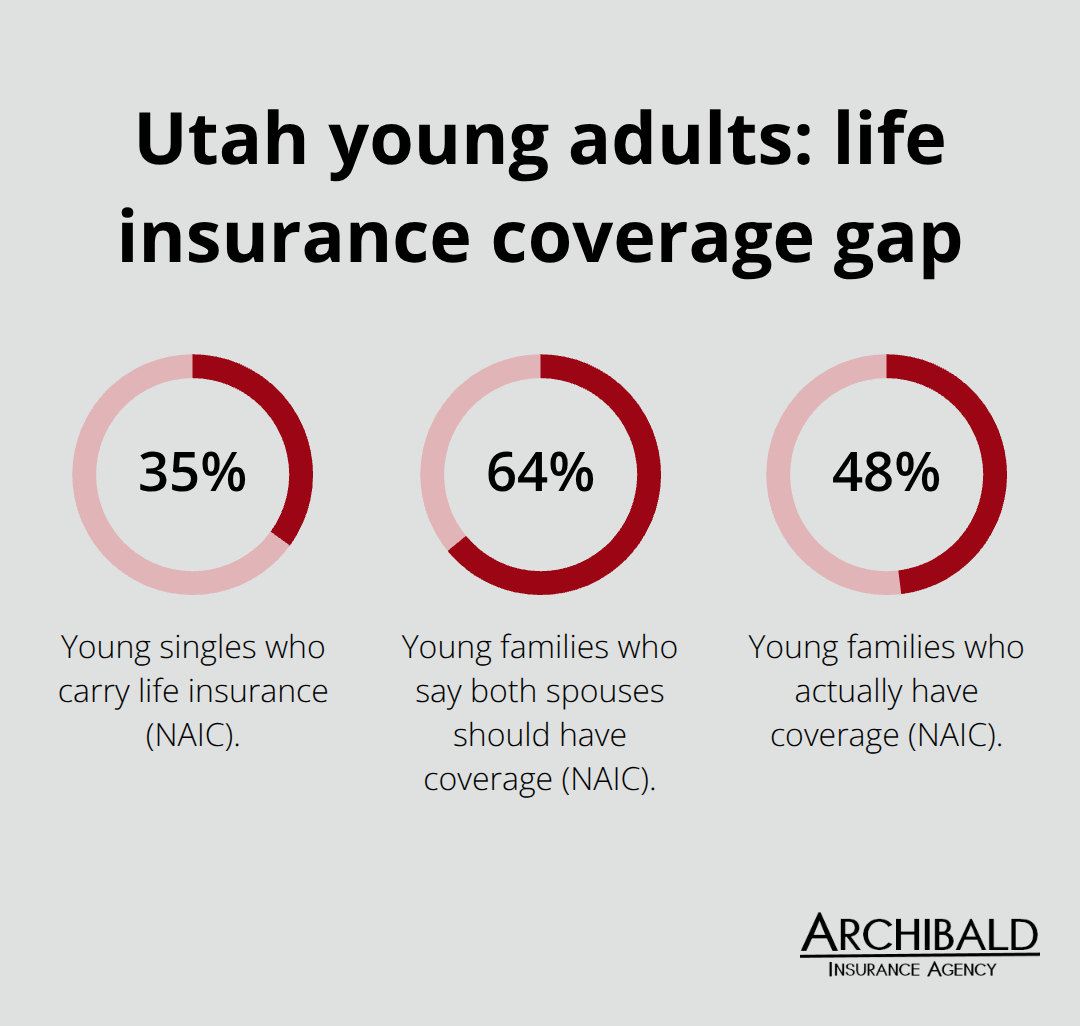

Life insurance protects what matters most. Utah families face specific financial pressures that make this protection non-negotiable. According to the National Association of Insurance Commissioners, roughly 35 percent of young singles carry life insurance, and while 64 percent of young families acknowledge both spouses should have coverage, only 48 percent actually do. That gap represents thousands of Utah households with zero protection. Your family’s mortgage, your kids’ education, your spouse’s ability to stay home or maintain childcare-all depend on income that vanishes the moment you die.

This isn’t about luck or hoping for the best. It’s about math. If you earn $60,000 annually and have a spouse, two kids, and a $300,000 mortgage, your death creates an immediate $600,000 income gap over the next decade alone, before accounting for college costs or inflation. Life insurance fills that gap with a tax-free death benefit your beneficiaries can use immediately.

Your Debts Don’t Disappear

Funeral costs in Utah average between $7,000 and $12,000 depending on the service you choose. That’s money your family must find while grieving. Your mortgage doesn’t pause. Property taxes don’t stop. Credit card balances, car loans, and personal debts all remain the responsibility of your estate or your surviving spouse. A $250,000 life insurance policy costs a healthy 35-year-old male roughly $9.82 per month for a 10-year term, yet it covers those immediate expenses and prevents your family from liquidating retirement accounts or selling the home at a loss. Many Utah families underestimate how long their dependents need protection. If you have children under 18, you need coverage that extends until they’re financially independent. A 20-year or 30-year term aligns with actual family obligations rather than arbitrary timeframes.

Income Replacement Is Non-Negotiable

Your family’s lifestyle depends on your paycheck. When that income stops, everything changes. A spouse who stayed home to raise children suddenly faces the choice between returning to work immediately or losing the house. Older children may need to leave school to help cover expenses. Life insurance prevents these scenarios. Financial experts recommend coverage equal to 10 to 15 times your annual income, adjusted for existing assets and debts. For a Utah family with $80,000 in household income, try a $400,000 to $600,000 policy to create a realistic safety net. Term life insurance accomplishes this affordably. The same 35-year-old male can secure $500,000 in 10-year coverage for $13.16 per month. That’s roughly $158 per year to protect everything your family has built.

What Happens Next

Understanding why life insurance matters is the first step. The next step involves identifying which type of coverage actually works for your situation-and that choice depends on your timeline, budget, and long-term financial goals.

Which Type of Life Insurance Works Best for Utah Families

Term Life Insurance Delivers Affordable Protection

Term life insurance is the right choice for most Utah families, and the data backs this up. A healthy 35-year-old male pays $13.16 monthly for $500,000 in 10-year coverage-roughly $158 per year. That same person would pay over $500 monthly for whole life providing identical death benefits. Term life delivers straightforward protection: you pay premiums for a fixed period, and your beneficiaries receive the death benefit if you die during that term. When the term ends, coverage stops unless you renew, but by then your mortgage may be paid, your kids through college, and your need for large death benefits reduced.

Matching Your Term to Your Timeline

The math is simple. If you have a 20-year mortgage and three children, a 20-year or 30-year term aligns perfectly with your actual financial obligations. You’re not paying for lifetime coverage you don’t need. A healthy 45-year-old female secures $500,000 in 10-year term coverage for $15.01 monthly-still affordable protection during peak earning years when dependents matter most. Utah families often ask whether they should purchase term now and upgrade to permanent coverage later. This strategy works if you lock in rates while young and healthy, since premiums only increase with age and health changes. Waiting five years costs significantly more.

When Whole Life and Universal Life Make Sense

Whole life and universal life insurance serve specific purposes, but they’re rarely the foundation of a young family’s protection strategy. Whole life provides lifetime coverage and builds cash value, making it useful for estate planning or business succession, but premiums run eight to ten times higher than term. Universal life offers flexibility-you can adjust premiums and death benefits-but it carries complexity and cost that most Utah families don’t need. If you own a business, expect a significant inheritance to go to your children, or want to leave a lasting legacy beyond your working years, permanent insurance deserves consideration.

Moving Forward With Your Coverage Decision

Otherwise, term life delivers the protection your family actually requires at a price that doesn’t strain your budget. The key decision isn’t between term and permanent-it’s between protection now and hoping nothing happens. Most Utah families choose wisely by starting with term coverage that matches their timeline. Once you’ve decided on the type of coverage that fits your situation, the next step involves calculating exactly how much protection your family needs and comparing quotes from multiple carriers to find the best rates.

How to Choose the Right Coverage for Your Family

Calculate Your Actual Financial Obligations

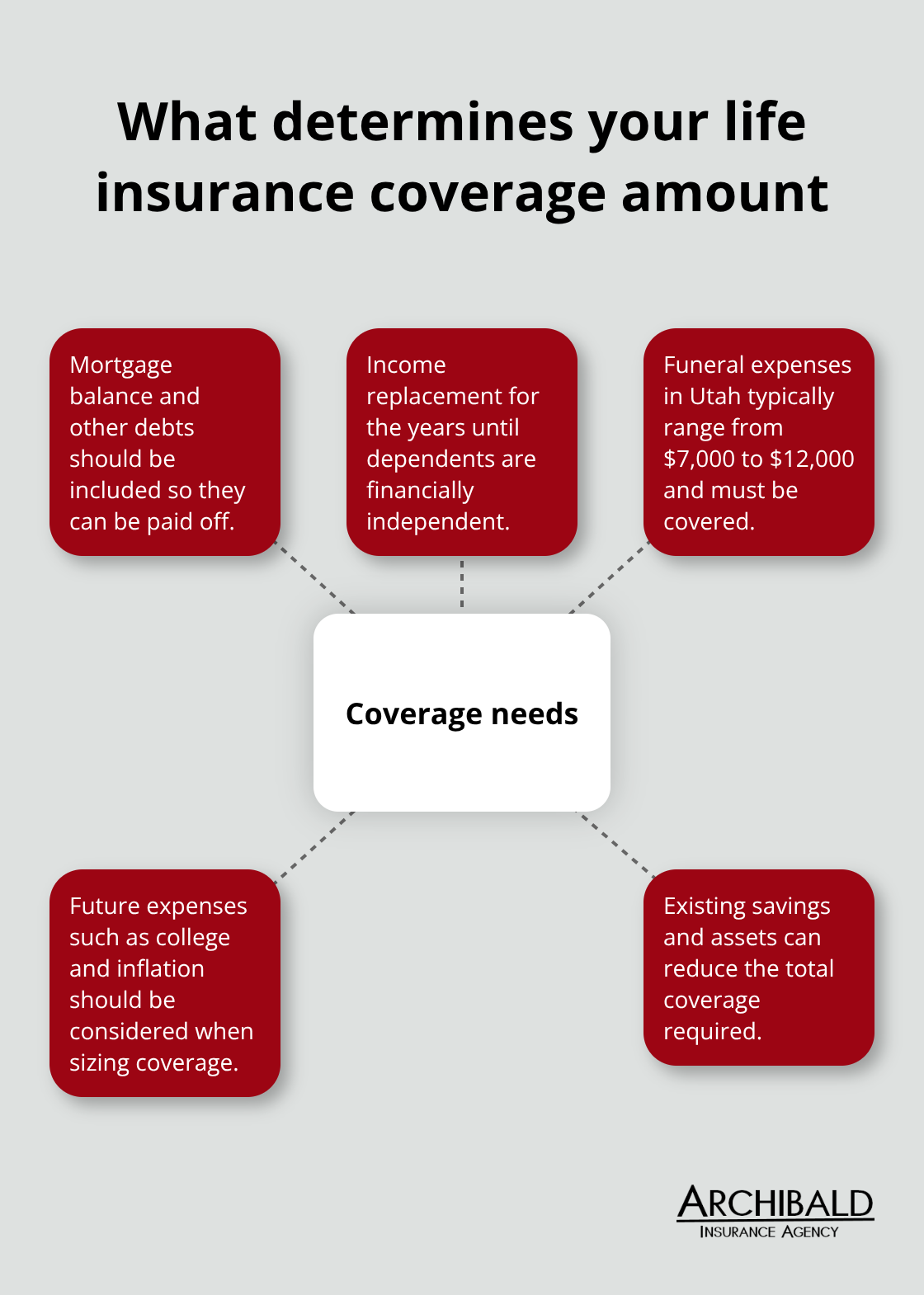

Choosing the correct coverage amount separates Utah families who sleep well at night from those who wake up worried they made the wrong call. The math here is straightforward, and it demands honesty about your actual situation. Start by listing every financial obligation your family would face if you died tomorrow. Your mortgage balance matters. Your car loans matter. Credit card debt matters. Funeral expenses between $7,000 and $12,000 in Utah matter. Then add income replacement. If you earn $70,000 annually and your youngest child is ten years old, your family needs eight years of income to bridge the gap until they’re independent.

That’s $560,000 right there, before accounting for inflation or college costs. Calculate your actual financial obligations by considering your debts, income, future expenses and your savings.

Apply the 10-to-15x Rule, Then Adjust

Most financial advisors recommend 10 to 15 times your annual income as a baseline, but this number only works if you actually sit down with pen and paper and do the calculation. A Utah family earning $80,000 combined with two children under twelve and a $350,000 mortgage needs roughly $550,000 to $700,000 in coverage, not some generic formula. Anything less leaves your spouse making impossible choices between keeping the house and paying for education. Anything dramatically more wastes premium dollars on protection you don’t need.

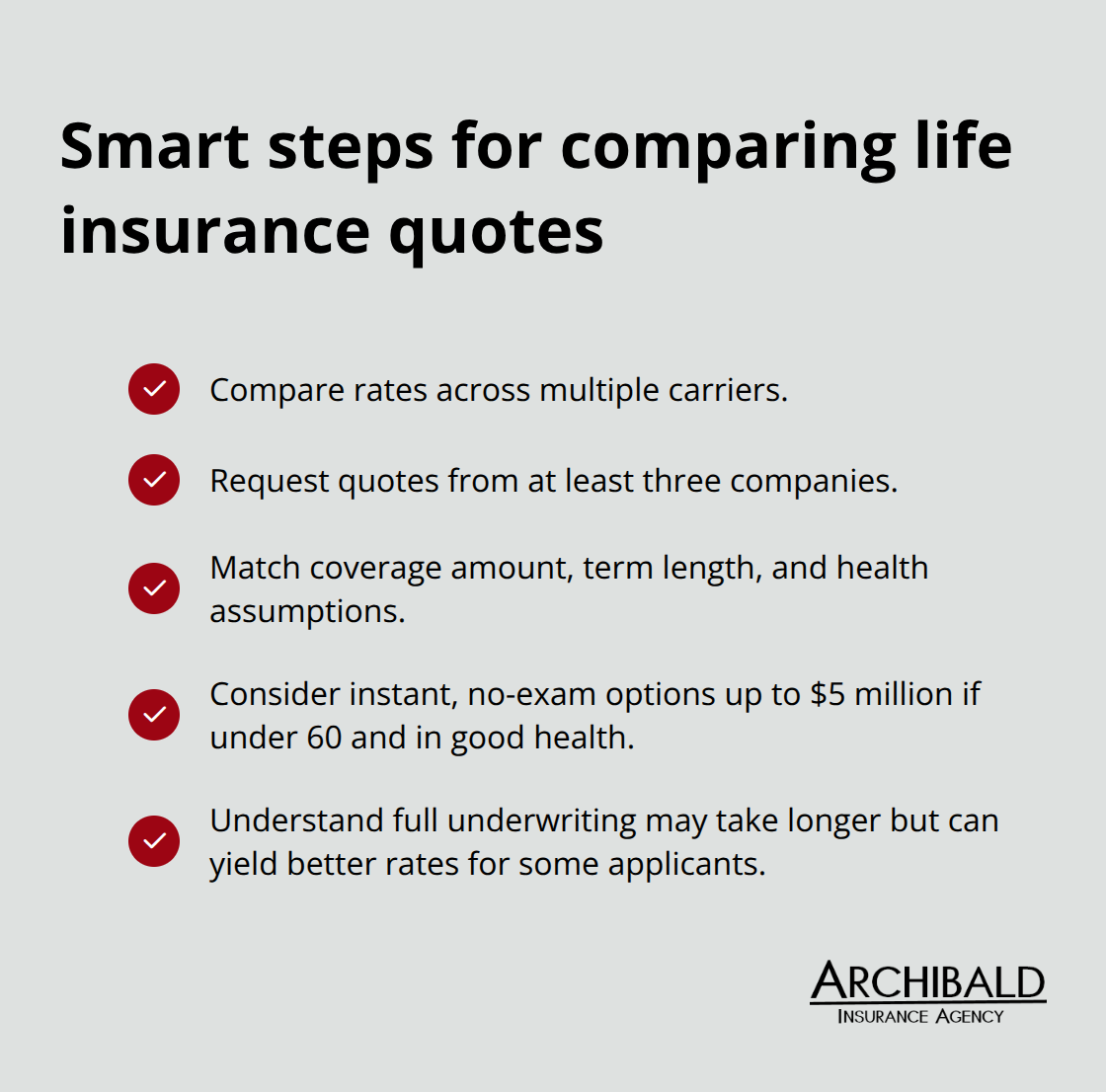

Compare Quotes Across Multiple Carriers

Once you know your target coverage amount, quote shopping becomes tactical rather than confusing. Compare quotes across multiple carriers to find the best rates for your situation. Request quotes from at least three carriers and compare apples to apples: same coverage amount, same term length, same health assumptions. Some insurers offer instant quotes online without medical exams for coverage up to $5 million if you’re under 60 and in good health, which accelerates the process significantly.

Others require full underwriting with blood work and medical records, which takes longer but sometimes produces better rates for applicants with health history.

Review Policy Illustrations and Terms Carefully

Once you’ve received quotes, read the actual policy illustration provided by each carrier. The Utah Life Insurance Illustration Rule requires standardized illustrations showing year-by-year cash value and death benefit projections. This transparency lets you see exactly what you’re purchasing rather than relying on sales talk. Verify that beneficiary designations match your wishes, confirm there are no surrender fees that would penalize early cancellation, and ask about renewal options if you’re considering a term policy that might need extension later. Ask each carrier about their underwriting timeline and what happens if you apply before receiving quotes elsewhere.

Final Thoughts

Life insurance protects your family’s financial future, and understanding Utah life insurance basics removes the confusion that keeps many families unprotected. A healthy 35-year-old male secures $500,000 in 10-year term coverage for $13.16 monthly, yet roughly 52 percent of young families still lack adequate protection. That gap exists because people delay the decision, not because protection is expensive or complicated.

Calculate your actual financial obligations by listing your mortgage, debts, funeral costs, and income replacement needs. Apply the 10-to-15x income rule, then adjust based on your specific situation-a Utah family with $80,000 in household income and two children under twelve typically needs $550,000 to $700,000 in coverage. Once you know your target amount, quote multiple carriers using identical coverage amounts and term lengths to find the best rates for your situation.

Premiums only increase with age and health changes, so waiting five years costs substantially more. Contact Archibald Insurance Agency to discuss your family’s protection needs and receive quotes that reflect your situation. Your family’s financial security is worth the conversation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation