Full Coverage Auto Utah: Understanding What It Covers

Many Utah drivers think full coverage auto insurance is optional or too expensive. The truth is that understanding what full coverage actually includes can save you money and protect your assets.

At Archibald Insurance Agency, we’ve helped countless Utah residents navigate their coverage options and avoid costly mistakes. This guide breaks down exactly what full coverage means and how to choose the right limits for your situation.

What Full Coverage Actually Includes

Beyond Utah’s Minimum Requirements

Full coverage in Utah means more than just meeting the state’s minimum liability requirements. Utah requires drivers to carry at least $25,000 in bodily injury liability per person, plus additional limits per accident and property damage liability. However, full coverage adds three critical layers on top of these minimums: liability protection beyond the state minimum, collision coverage, and comprehensive coverage.

How Liability Coverage Protects You

Liability coverage protects you financially if you cause an accident and injure someone or damage their property. Most drivers should carry higher liability limits than the minimum because if you cause a serious accident, the other person’s medical bills and property damage can easily exceed the state minimum. Your lender almost certainly requires both collision and comprehensive coverage as a condition of the loan if you financed your vehicle.

Collision and Comprehensive Coverage

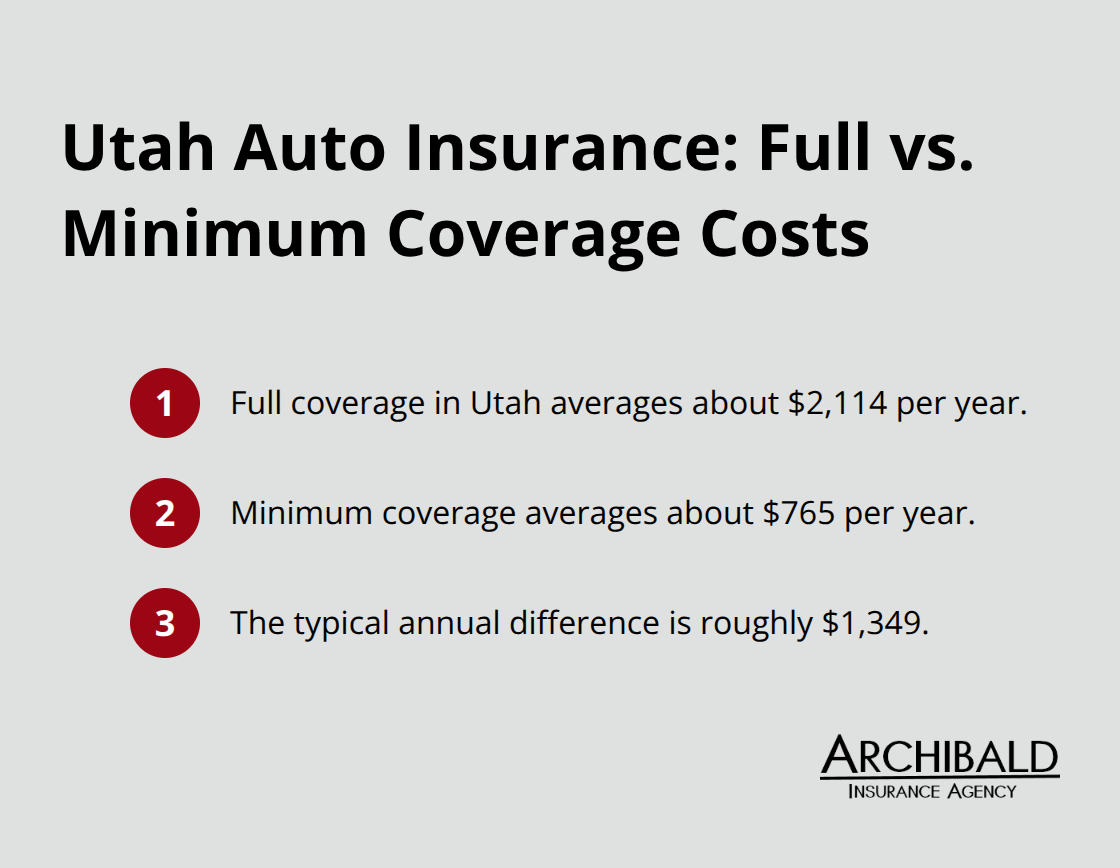

Collision coverage pays for repair or replacement costs if you hit another vehicle, an object, or flip your car. Comprehensive coverage handles damage from events outside your control, including theft, vandalism, falling objects, natural disasters, floods, fires, and animal strikes. The annual cost for full coverage in Utah averages around $2,114 according to WalletHub, compared to approximately $765 for minimum coverage-a roughly $1,349 annual difference that many drivers find reasonable.

Utah’s Required Protections: PIP and UM/UIM Coverage

Utah mandates Personal Injury Protection (PIP) on all auto policies, which covers medical expenses for you and your passengers regardless of who caused the accident. PIP typically provides $3,000 for medical costs, $20 per day for household services, and either $250 or 80% of lost wages, whichever is less. You also need uninsured motorist and underinsured motorist coverage (required in Utah unless you waive them in writing) to protect yourself if someone hits you and they’re uninsured or underinsured.

Matching Coverage to Your Financial Reality

The real question isn’t whether full coverage costs more, but whether you can afford a total loss without it. If your car is worth $15,000 and you only carry minimum liability coverage, you’re personally responsible for the entire repair bill if you cause an accident. Full coverage isn’t about buying more insurance for the sake of it, but about matching your coverage to your financial reality. If you drive a newer vehicle with a loan or lease, full coverage makes financial sense. If you own an older vehicle outright and can afford unexpected repairs from savings, you might skip collision and comprehensive on that specific car. The decision depends entirely on whether you could absorb a major repair or total loss without derailing your finances.

Now that you understand what full coverage includes, the next step is recognizing the common misconceptions that lead Utah drivers to either overpay or under-protect themselves.

What Full Coverage Actually Doesn’t Cover

Many Utah drivers believe full coverage means complete protection from any car-related expense, which leads to unrealistic expectations and poor decisions about their policies. Full coverage protects against specific situations, not every possible scenario. It won’t cover maintenance costs, wear and tear, mechanical breakdowns, or intentional damage you cause yourself. If your transmission fails or your brake pads wear out, full coverage won’t pay for repairs. If you deliberately drive through a fence or crash your car on purpose, your insurer will deny the claim.

This distinction matters because drivers sometimes drop coverage thinking they’re over-insured, only to face unexpected bills when they misunderstand what their policy actually covers.

Liability Protection Matters More Than Vehicle Age

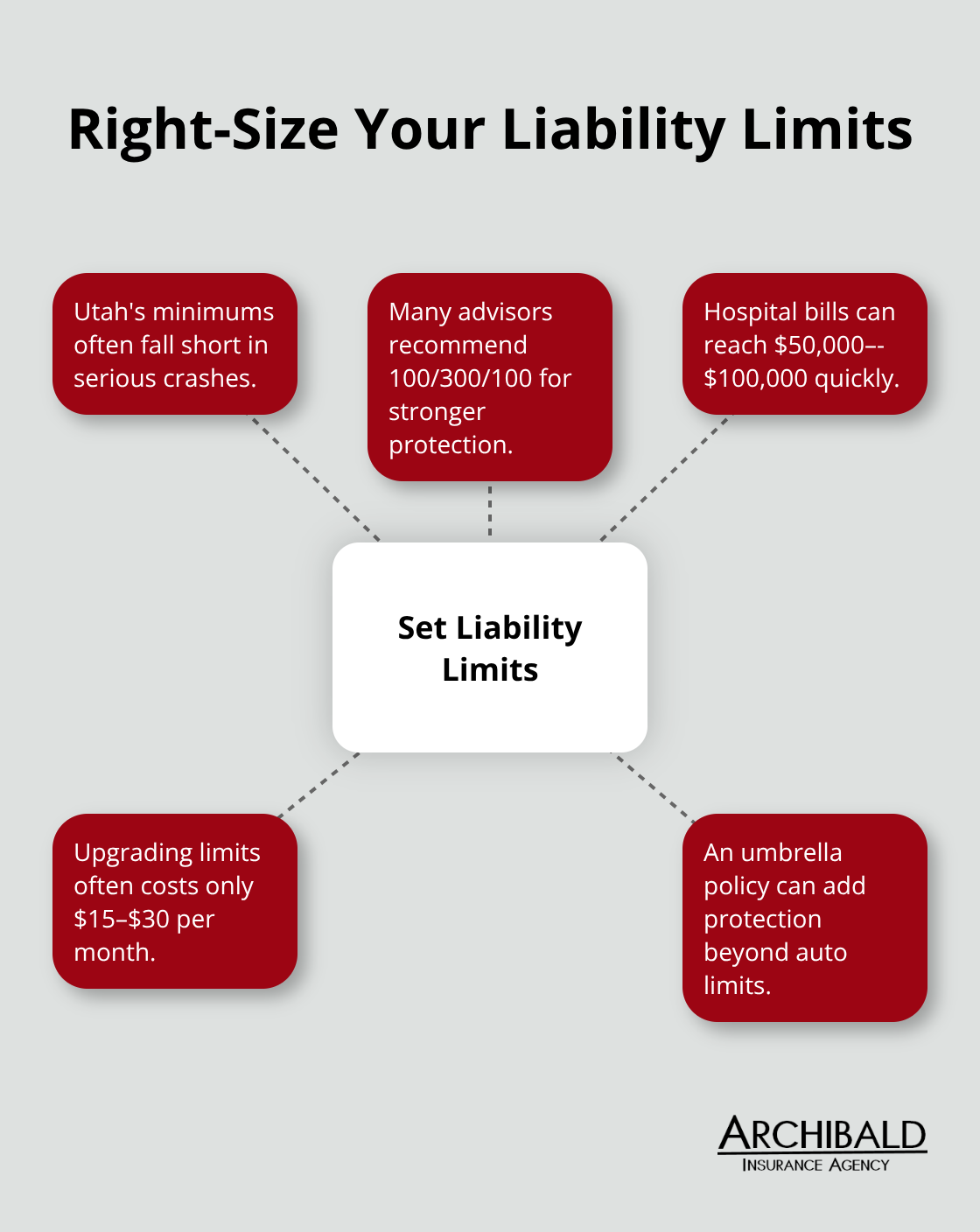

Some Utah drivers assume that owning a car outright means they can skip full coverage entirely, but this reasoning ignores the most important component: liability protection. Even if you own a ten-year-old vehicle worth $5,000, liability coverage protects your personal assets if you cause a serious accident. If you hit someone and cause $100,000 in medical bills and property damage, your liability coverage shields your home, savings, and future wages from a lawsuit. Utah’s minimum liability limits won’t cover that scenario, which is why most financial advisors recommend carrying higher limits regardless of your vehicle’s age.

The Real Cost Comparison for Owned Vehicles

Drivers often overestimate the cost difference between full coverage and minimum coverage, assuming the annual difference is too high. However, if you’re financing or leasing your vehicle, your lender requires collision and comprehensive coverage anyway, so you don’t have a choice. The real cost comparison applies only to vehicles you own outright. If your car is worth $12,000 and collision coverage costs $400 annually, you break even financially in just thirty years of accident-free driving. One serious accident can total your vehicle, wiping out your transportation and forcing you to buy a replacement immediately.

Matching Coverage to What You Can Actually Afford

The real question isn’t whether your car is paid off, but whether you have enough liability protection for your actual financial situation. Dropping collision and comprehensive on an older vehicle makes sense if you can afford repairs from savings, but reducing liability coverage below adequate limits is a dangerous gamble that costs almost nothing to fix. For newer vehicles with loan balances, full coverage typically costs far less than the financial risk you’d face without it. The expense becomes irrelevant when you compare it to replacing a vehicle or paying out-of-pocket for major repairs.

Understanding what full coverage excludes helps you make informed decisions, but the next step involves calculating exactly how much coverage your specific situation requires.

Choosing Coverage Limits That Protect Your Assets

Calculate Your Vehicle’s Actual Value

Start with your vehicle’s actual cash value, not what you paid for it or what you owe on a loan. If your car is worth $18,000 according to Kelley Blue Book, that’s your baseline for collision and comprehensive coverage decisions. An $18,000 vehicle doesn’t justify $500 monthly premiums, but it absolutely justifies $150 to $200 monthly for full coverage. Next, calculate what you could realistically pay out of pocket for repairs or a total loss without affecting your mortgage payment, rent, or emergency fund. If you have $8,000 in savings and your car is worth $6,000, dropping collision coverage means you’d deplete your emergency fund with one accident. That’s not a smart financial move, regardless of how much you save on premiums.

Assess Your Liability Coverage Needs

For liability coverage, the math is different and far more important. Utah’s minimum liability limits are $25,000 per person for bodily injury, $65,000 total per accident for bodily injury, and $25,000 for property damage. These limits won’t protect you in serious accidents. A single hospitalization can cost $50,000 to $100,000, and you’ll personally owe anything above your coverage limits. Most financial advisors recommend carrying at least $100,000 per person and $300,000 per accident in bodily injury liability, with $100,000 in property damage.

The premium difference between $25,000 and $100,000 in bodily injury coverage is typically $15 to $30 monthly, making it one of the cheapest ways to protect your assets. For additional protection beyond standard liability limits, a personal umbrella policy can shield both your current assets and future earnings from major lawsuits.

Match Coverage to Your Financial Situation

Your vehicle financing situation should heavily influence your decision. If you’re financing or leasing, your lender requires full coverage anyway, so the choice is already made for you. If you own your car outright, the decision depends on three factors: your vehicle’s value, your liquid savings, and your income level. Someone earning $35,000 annually with $3,000 in savings should carry full coverage on any vehicle worth more than $5,000 because a total loss would be financially devastating. Someone earning $150,000 annually with $50,000 in savings can comfortably skip collision on a $7,000 vehicle because they could replace it immediately.

Understand Utah’s Required Protections

Utah’s PIP requirement of $3,000 in medical coverage is also too low for most drivers. If you or a passenger requires surgery or hospitalization, $3,000 disappears in hours. You can’t waive PIP in Utah, but you should understand that uninsured motorist coverage and underinsured motorist coverage provide additional protection if someone hits you. These coverages are required in Utah unless you specifically waive them in writing, and they cost almost nothing compared to the protection they provide.

Review Your Coverage Annually

A practical approach involves reviewing your coverage annually or whenever your financial situation changes. If you received a significant raise, paid off your mortgage, or accumulated more savings, your coverage needs shift upward. Conversely, if you’re experiencing financial hardship, you might reduce coverage on older vehicles while maintaining strong liability limits across all vehicles you drive.

Final Thoughts

Full coverage auto insurance in Utah protects your vehicle and your financial future, but only if you understand what it actually covers and match it to your specific situation. The components we’ve discussed-liability protection beyond state minimums, collision coverage, comprehensive coverage, and Utah’s required PIP and uninsured motorist protections-work together to shield you from catastrophic financial loss. Your coverage needs change as your life changes, and a promotion, a paid-off mortgage, or a new vehicle purchase all shift what you should carry.

Reviewing your policy annually prevents you from overpaying for protection you don’t need while ensuring you’re not dangerously underinsured. Many Utah drivers discover they’ve been carrying inadequate liability limits or paying for collision coverage on vehicles worth less than their deductible. Others realize they dropped coverage they actually needed after a financial setback, and these mistakes are entirely preventable with a straightforward annual review.

We at Archibald Insurance Agency understand that full coverage auto Utah decisions aren’t one-size-fits-all, and our team works with you to calculate your vehicle’s value, assess your liability exposure, and match your coverage to your financial reality. Contact us to review your current coverage or get a quote for full coverage that actually makes sense for your situation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation