Life Insurance Quotes Utah: Quick Estimates for Your Family

Getting a life insurance quote in Utah doesn’t have to be complicated. We at Archibald Insurance Agency help families understand their options and find coverage that fits their budget and needs.

Whether you’re protecting your family’s financial future or replacing lost income, the right policy starts with accurate quotes. This guide walks you through the process, from gathering information to comparing carriers and securing the best rate for your situation.

How Life Insurance Quotes Work in Utah

Understanding What Insurers Need From You

Life insurance quotes in Utah require you to provide specific information upfront so carriers can calculate accurate premiums. You’ll supply your age, gender, height, weight, and tobacco use status, along with details about any prescription medications you take and your family’s health history. Your occupation and hobbies matter too-skydiving or motorcycle racing can substantially increase your rate. Income and outstanding debts like mortgages or loans help insurers understand how much coverage makes sense for your situation.

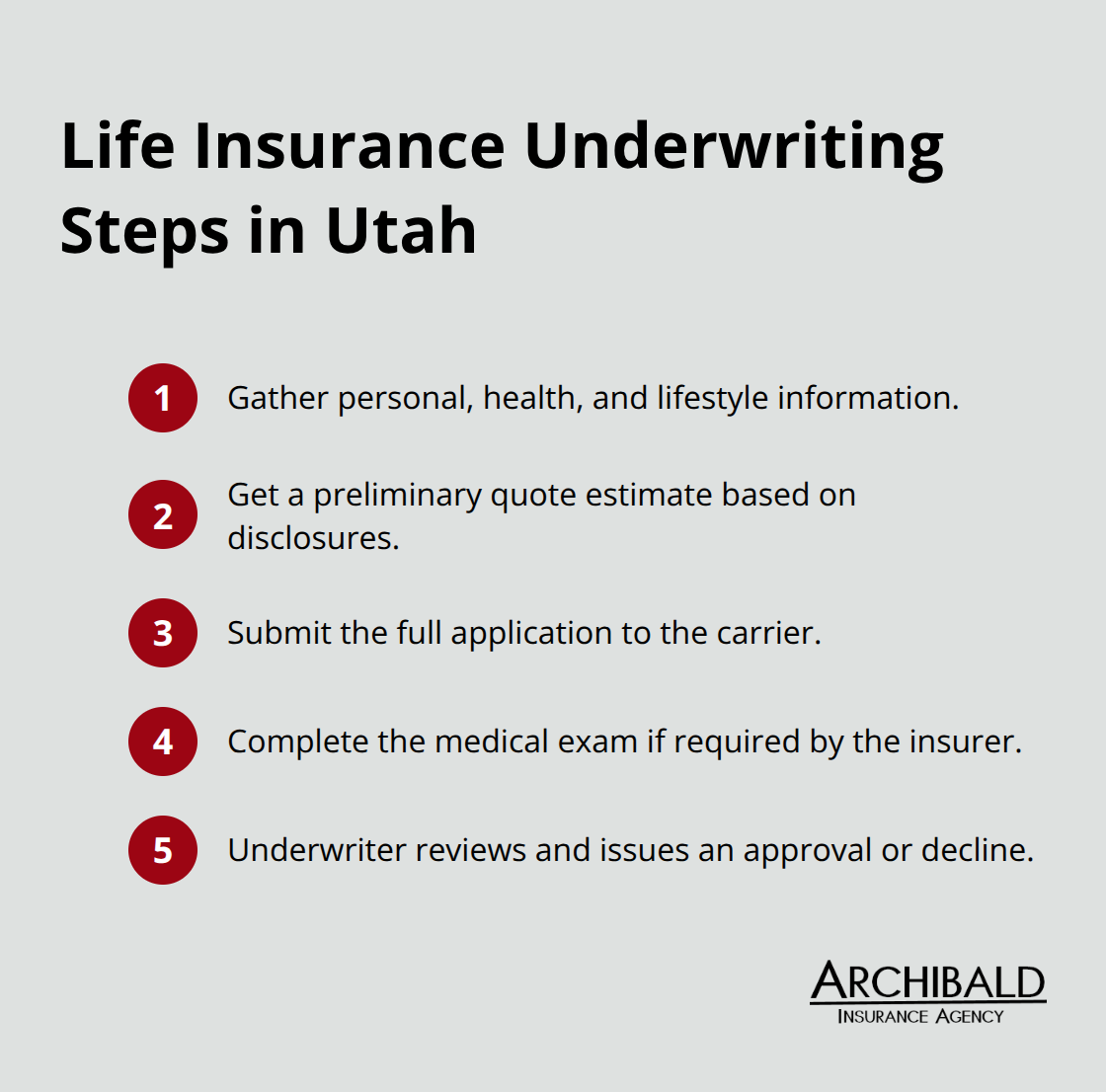

The Underwriting Process

The underwriting process follows a clear path: you gather information, receive a quote estimate, submit a full application, complete a medical exam if required, and then the underwriter reviews everything before accepting or declining your coverage. This structured approach protects both you and the insurer by confirming that the information you provided matches your actual health and lifestyle.

How Health and Lifestyle Shape Your Premium

Age and gender influence premiums, with younger individuals and females typically paying less. Health, tobacco use, and family history all affect your monthly costs. Women typically pay lower premiums due to longer life expectancy, and younger applicants always secure better rates by locking in coverage early. Your medical history carries real weight-conditions like heart disease, diabetes, or cancer, plus early-onset disease in your family, will increase your quote. High cholesterol or well-controlled hypertension won’t tank your rate, but untreated conditions absolutely will.

Fast-Track Options Without Medical Exams

Some carriers offer no-medical-exam options like RAPIDecision Life or Instant Term policies up to $5 million for applicants under 60 in good health, allowing faster approval when you need coverage quickly. These streamlined options eliminate delays and let you activate protection within days rather than weeks.

Why Comparing Multiple Carriers Matters

The key is comparing quotes from multiple carriers because underwriting factors can vary by insurer, and rates can vary significantly among companies. This comparison reveals which carriers value your specific profile most favorably and helps you identify real savings opportunities.

With your quote information in hand, you’re ready to explore the different policy types available to Utah families.

Which Life Insurance Type Fits Your Utah Family

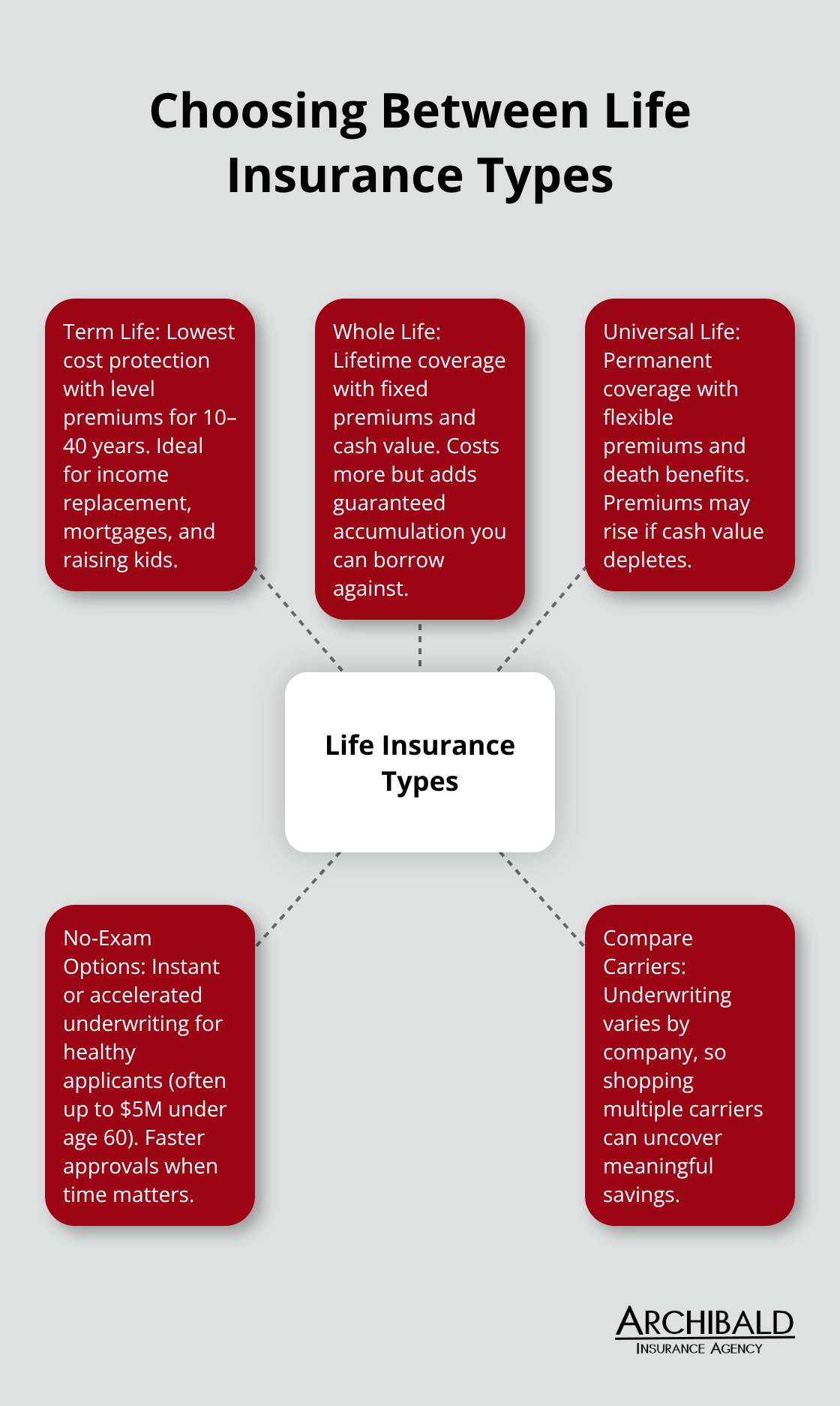

Term Life Insurance for Temporary Obligations

Term life insurance offers the most straightforward protection for Utah families with temporary financial obligations. A 10-year term costs roughly $8.48 per month for a 25-year-old woman seeking $250,000 in coverage, while the same woman pays about $14.95 monthly for $1 million. A 55-year-old man pays $36.72 monthly for $250,000 and $120.82 for $1 million over 10 years. Term lengths in Utah range from 10 to 40 years with guaranteed level premiums throughout the initial period, making budgeting predictable.

This structure works best when you have a mortgage to protect, young children to support, or specific debt obligations that will eventually disappear. Once your obligations end, your coverage expires without forcing you into permanent insurance you don’t need. Utah residents should seriously consider term as the starting point, since it delivers death benefit protection at roughly one-tenth the cost of permanent options.

Whole Life Insurance and Permanent Protection

Whole life insurance guarantees lifetime coverage with fixed premiums that never increase, plus accumulated cash value you can borrow against during your lifetime. This approach makes sense when you have long-term obligations like aging parents depending on you, a business requiring continuity, or substantial wealth transfer goals. However, permanent policies cost substantially more-often $100 or more monthly for modest coverage-and that expense compounds over decades.

Universal Life and Flexible Coverage

Universal life provides permanent protection with more flexibility, allowing you to adjust premiums and death benefits as your circumstances change. This flexibility comes with a trade-off: your premiums could rise if cash value depletes. Universal life appeals to those whose financial situations shift over time and who want options to modify their protection without purchasing an entirely new policy.

Choosing the Right Type for Your Situation

Most Utah families with working spouses, dependent children, and typical mortgages should lock in 20 to 30-year term coverage first, then evaluate whole or universal life only after securing adequate term protection. The math strongly favors term for income replacement and debt protection, while permanent coverage serves specific wealth and legacy planning needs that most families address later, not immediately. With your policy type selected, the next step involves calculating exactly how much coverage your family actually needs.

How Much Coverage Does Your Family Actually Need

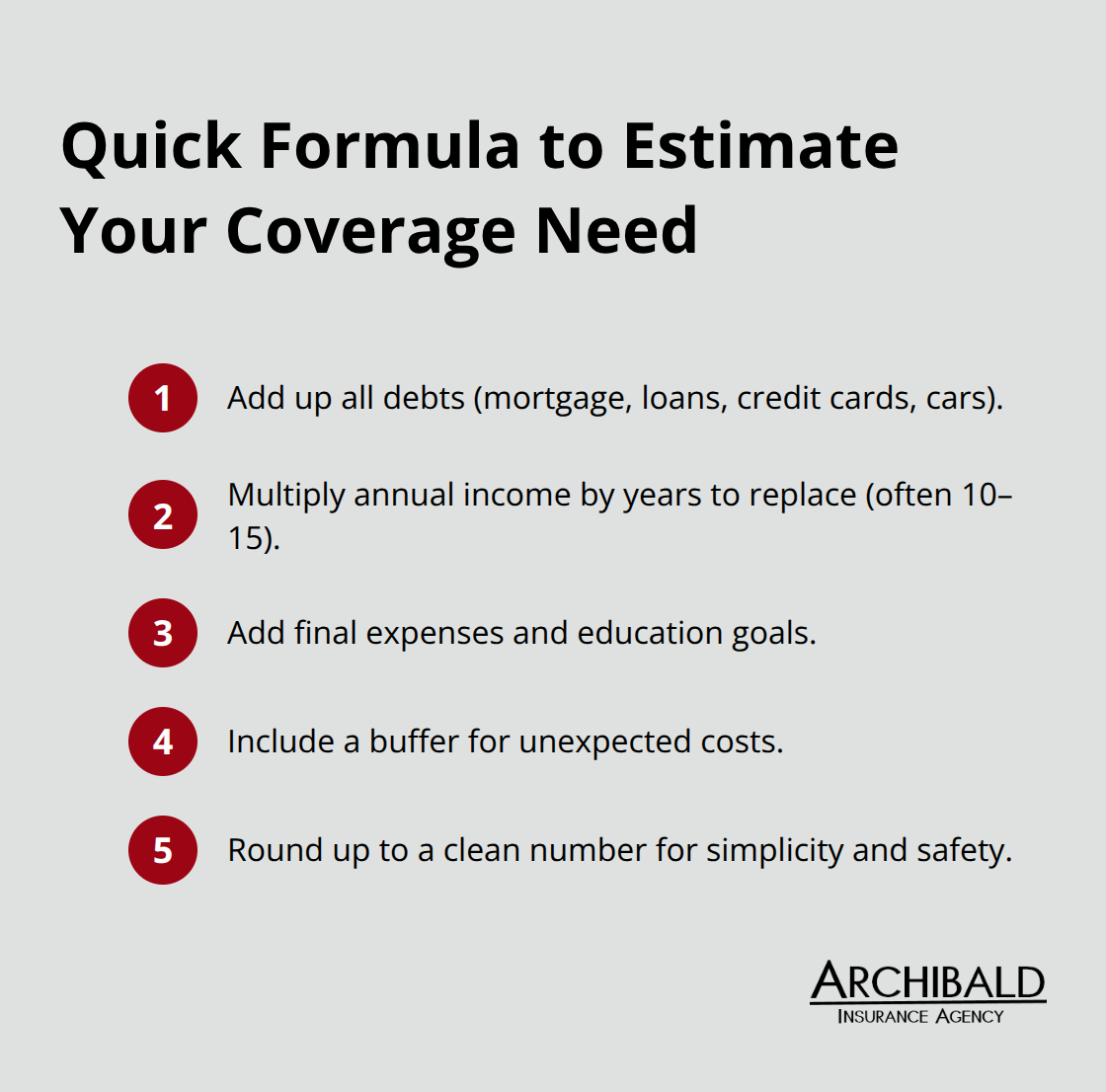

Calculate Your Total Financial Obligations

Start with brutal honesty about your financial obligations. Add up your mortgage balance, outstanding loans, credit card debt, and car payments-this is your debt total. Then multiply your annual household income by the number of years you want to replace that income if you died today; most families need 10 to 15 years of income replacement. Factor in funeral costs, which average about $8,300 in Utah, plus any education funding goals for your children. A practical formula: total your debts plus income replacement needs plus final expenses, then add a buffer for unexpected costs.

Work Through a Real Example

For a 35-year-old earning $65,000 annually with a $300,000 mortgage and two young children, the math works like this: $300,000 in debt plus $650,000 in income replacement (10 years) plus $8,300 for funeral costs lands near $958,300 in coverage. Round up to $1 million for safety. This isn’t theoretical-it’s the actual gap between what your family has and what they’d need to maintain their lifestyle without you.

Address Weight and Health Before You Apply

Tobacco use crushes your rate, so if you’ve quit within the past year, waiting a few more months before applying saves hundreds annually. Weight matters more than most realize; a 40-year-old male at 250 pounds might pay 25 to 40 percent more than the same person at 190 pounds, so addressing weight before applying genuinely reduces costs. High cholesterol and well-controlled hypertension barely move your quote, but untreated conditions or multiple medications for chronic issues will spike your premium substantially.

Optimize Your Term Length and Disclosure Strategy

Avoid risky hobbies when possible, or at least disclose them accurately-lying about skydiving or motorcycle racing creates a policy that won’t pay out if something happens. Skip the coffee for two weeks before your medical exam; elevated blood pressure from caffeine can trigger a higher rating. Consider a 20-year term instead of 30 years if your obligations end sooner; a 45-year-old with a 15-year mortgage needs protection only until age 60, not 75. Many families realize that a slightly shorter term cuts their monthly payment by 20 to 30 percent while still covering their actual needs.

Stack Discounts Through Bundling

Bundling life insurance with your home or auto policy through the same carrier often unlocks discounts of 5 to 15 percent, so mention any existing policies when you quote. This simple step compounds your savings and simplifies your coverage management across multiple policies.

Final Thoughts

Life insurance quotes in Utah put you in control of your family’s financial protection. Your age, health history, tobacco use, and occupation directly shape what you’ll pay each month, which is why locking in protection early delivers real savings over time. A 25-year-old non-smoker in good health will pay a fraction of what a 55-year-old smoker pays for identical coverage.

You control some factors and cannot change others. You cannot alter your age or family health history, but you can quit smoking before applying, address weight issues, and treat untreated conditions before your medical exam. You cannot avoid your occupation, but you can disclose hobbies and lifestyle choices accurately rather than hiding them and risking a denied claim later.

Calculate how much coverage your family actually needs by totaling your debts, income replacement goals, and final expenses. Compare life insurance quotes Utah from at least three different carriers, since rates vary significantly based on how each company evaluates your specific profile. Contact Archibald Insurance Agency to work with an independent agent who represents multiple carriers and matches you with the best option for your situation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation