Life Insurance and Types: Complete Guide

Life insurance protects your family’s financial future when you’re no longer here to provide for them. Most Utah families are underinsured, leaving their loved ones vulnerable to unexpected hardship.

At Archibald Insurance Agency, we help you understand life insurance and types of policies available so you can make the right choice for your situation. This guide walks you through your options and shows you how to find the coverage that fits your needs.

What Life Insurance Actually Does

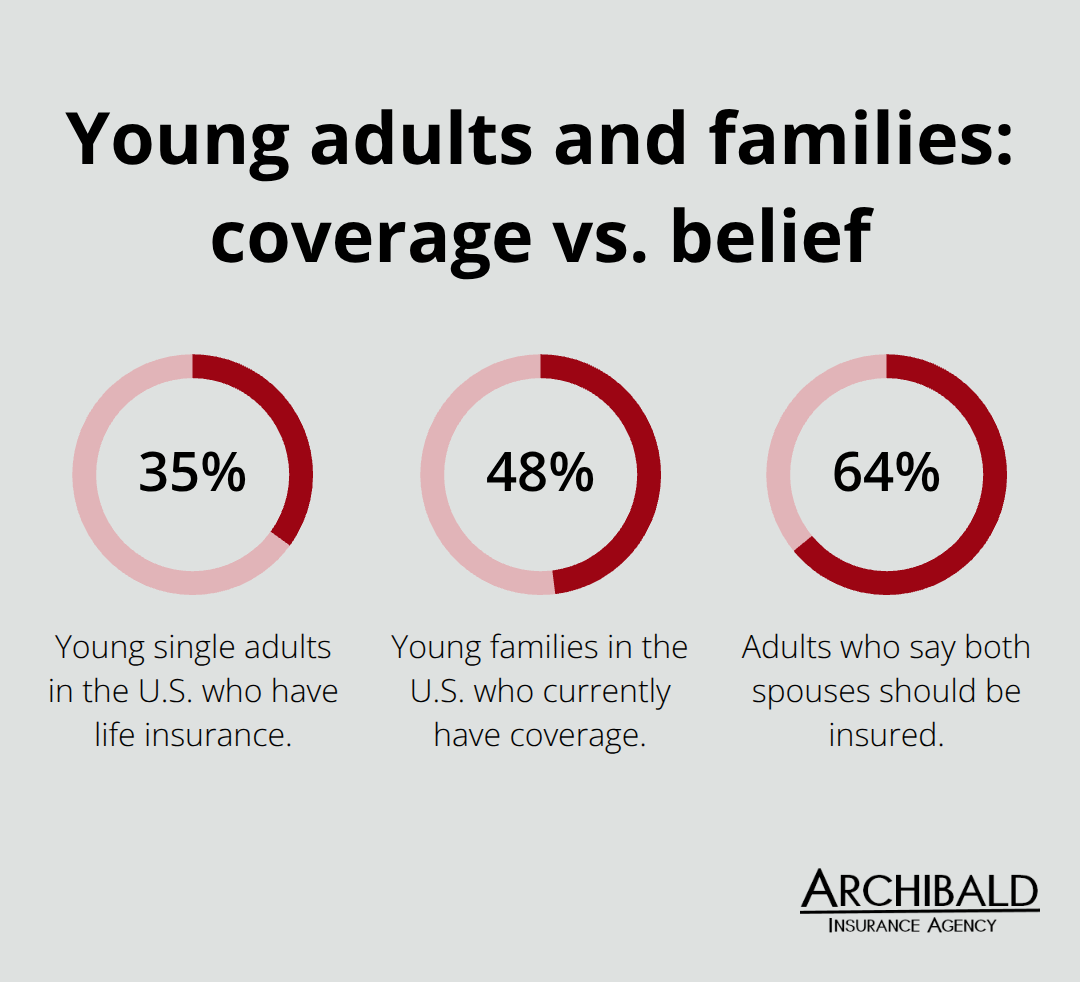

Life insurance replaces your income when you die, paying a tax-free lump sum to your beneficiaries. That money covers immediate expenses like funeral costs, pays off debts, replaces lost income, and funds future goals like college. Without it, your family faces a financial cliff. The National Association of Insurance Commissioners reports that only about 35 percent of young single adults in the United States have life insurance, and roughly 48 percent of young families have coverage despite 64 percent saying both spouses should be insured. In Utah, this coverage gap is particularly risky because families often depend on a single income or two incomes with minimal backup savings.

A $500,000 policy for a healthy 35-year-old costs about $25 to $31 monthly for a 20-year term, making protection affordable for most households. The real problem isn’t cost-it’s that many people delay purchasing coverage or underestimate how much they need.

Why Most Utah Families Stay Underinsured

Utah families face unique financial pressures that make adequate coverage essential. Many households rely on one primary earner or two incomes with little emergency savings to fall back on. When a breadwinner dies, the surviving family loses not just immediate income but also the ability to maintain their current lifestyle, pay property taxes, or fund children’s education. Most Utah families calculate coverage based on current needs alone, ignoring inflation and long-term obligations. This approach leaves them short when unexpected expenses arise or when inflation erodes the purchasing power of their death benefit over time.

Calculate Your Actual Coverage Needs

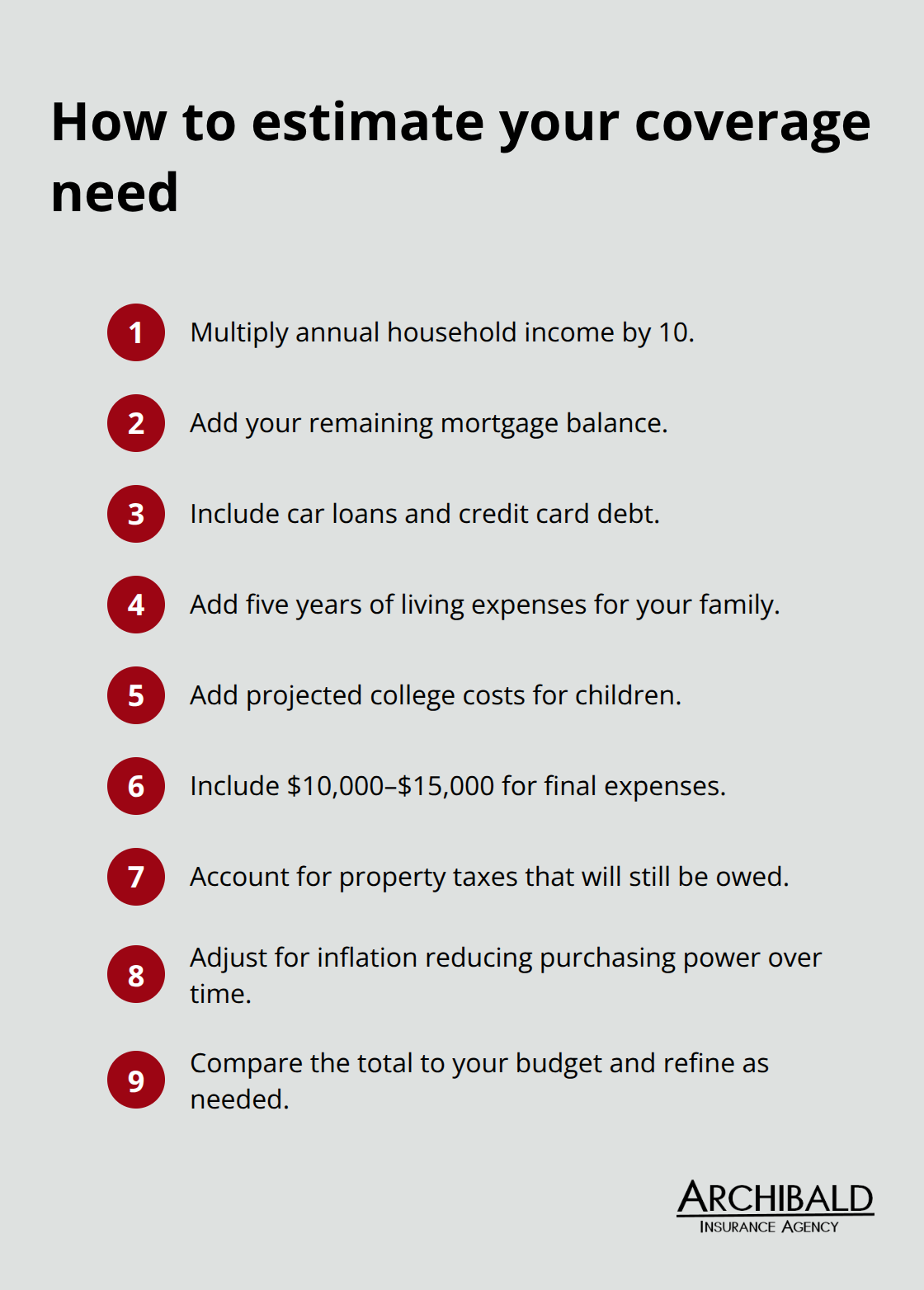

Start with a simple calculation: multiply your annual income by 10, then add major expenses. If you earn $60,000 annually and carry a $300,000 mortgage, you need roughly $900,000 in coverage. Add college costs for young children, and your number climbs higher. Account for final expenses, property taxes your family will still owe, and the fact that inflation will erode the purchasing power of that lump sum. Most people need more coverage than they think, and term life is cheap enough that overestimating is smarter than underestimating.

A financial professional can help you model different scenarios and account for variables you might miss on your own. This step matters because it transforms a vague sense of “needing protection” into a concrete number you can shop for with confidence. Once you know your target coverage amount, you’re ready to explore which type of policy fits your timeline and budget.

The Three Main Life Insurance Types and How They Work

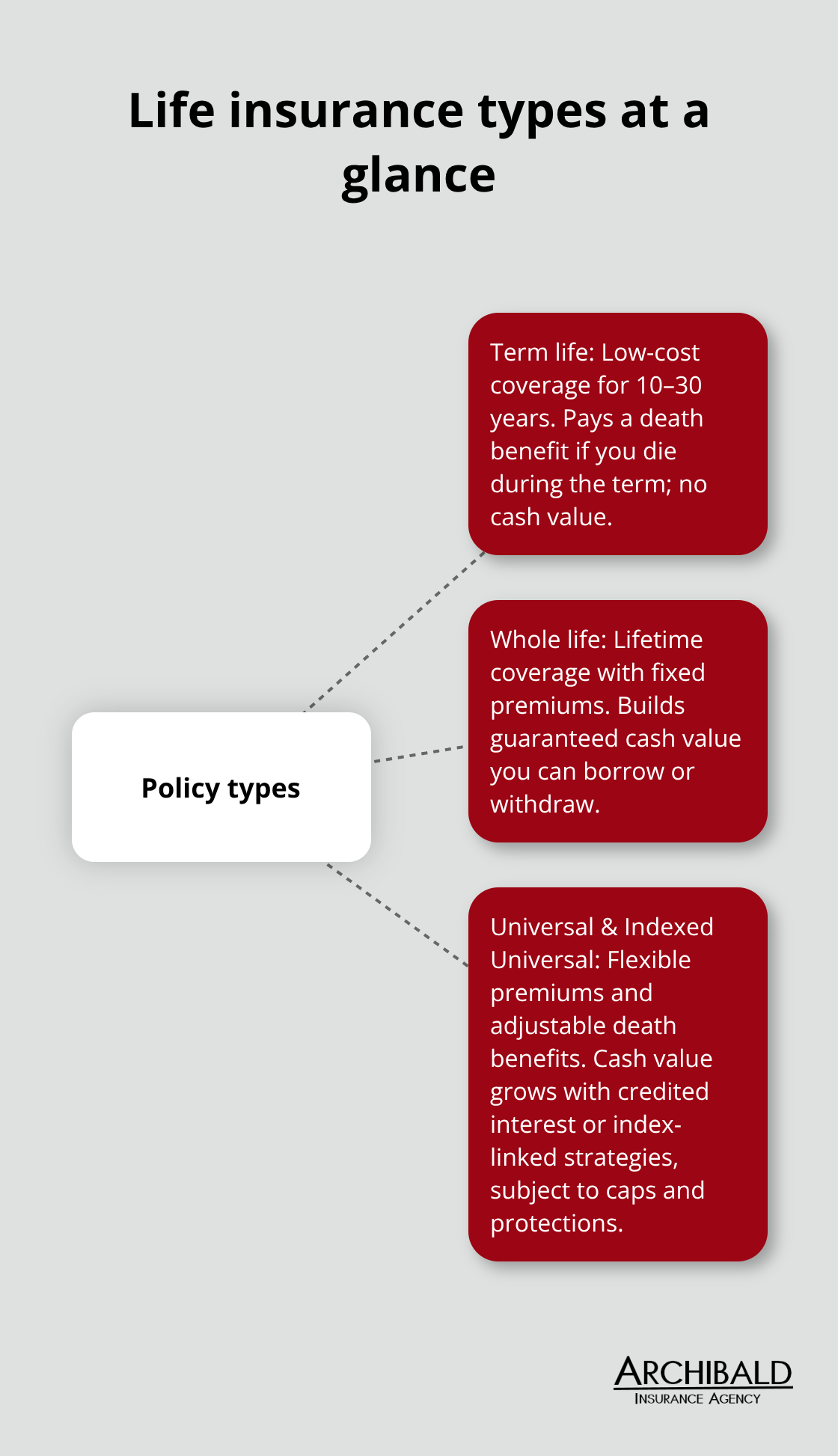

Term Life Insurance: Affordable Protection for Your Peak Years

Term life insurance covers you for a set period-typically 10, 20, or 30 years-and pays a death benefit only if you die during that term. Once the term ends, coverage stops unless you renew or convert to permanent coverage. For a healthy 35-year-old, a $500,000 20-year term policy costs roughly $25 to $31 monthly, making it the cheapest option available. According to NerdWallet data from May 2025, a $500,000 term policy for a 40-year-old costs about $334 annually for men and $282 for women. Term premiums have declined significantly over the past decade as life expectancy has increased, which means term life offers more affordability than ever before.

The trade-off is straightforward: you receive low premiums and clear coverage for a defined period, but no cash value builds inside the policy. If you outlive the term, the policy expires and you walk away with nothing. Term works best for covering your peak financial obligations-your mortgage, your kids’ education years, your earning potential-when you need protection most and premiums matter most.

Whole Life Insurance: Permanent Coverage with Cash Value

Whole life insurance builds cash value inside the policy that you can borrow against or withdraw, and it provides lifetime coverage with a guaranteed death benefit as long as you pay premiums. According to NerdWallet, a $500,000 whole life policy for a 40-year-old costs about $6,387 annually for men and $5,860 for women, roughly 19 times more than term. The higher cost purchases permanent protection and the ability to access your policy’s cash value during your lifetime through loans or withdrawals. Whole life premiums remain fixed for life, which means your cost never increases due to age or health changes.

Some whole life policies from mutual insurers pay annual dividends-Guardian Life has paid dividends every year since 1868-which can increase your policy’s cash value and death benefits over time. This dividend history demonstrates how permanent policies can compound value across decades.

Universal Life and Indexed Universal Life: Flexible Permanent Options

Universal life offers a middle ground with flexible premiums and adjustable death benefits, allowing you to increase coverage or skip payments when your financial situation changes. The cash value in universal life grows based on credited interest rates, but charges are deducted from that value, which means insufficient funding can cause the policy to lapse. Indexed universal life links cash value growth to a stock index like the S&P 500 with downside protection and upside caps, offering market exposure without unlimited downside risk.

The fundamental choice comes down to your timeline: term life works for temporary needs at minimal cost, while whole life and universal life work for permanent protection when you want a policy that builds value and lasts your entire life. Understanding which type matches your situation requires honest assessment of how long you need coverage and what you can afford to pay each month.

How Much Coverage Do You Actually Need

The gap between what people think they need and what actually protects their family is staggering. Most Utah families calculate coverage by guessing instead of using concrete numbers. Start with your annual household income and multiply it by ten as a baseline, then add specific expenses: your mortgage balance, outstanding car loans, credit card debt, and five years of living expenses for your family. If you have children, add college costs at current rates. Include final expenses of $10,000 to $15,000 for funeral and burial costs.

Factor in property taxes your family will still owe and account for inflation eating into that lump sum over time. A family earning $75,000 with a $350,000 mortgage and two young children often needs $1.2 to $1.5 million in coverage, not the $500,000 they initially thought. The math is straightforward, but most people skip it entirely and underestimate by 30 to 50 percent.

Comparing Quotes Reveals Real Price Differences

Once you know your target coverage amount, request quotes from at least three different carriers. Legal & General America, the cheapest option in Utah for standard term policies, quotes about $27 monthly for a healthy 35-year-old male seeking $500,000 in 20-year term coverage. A competing carrier might quote $35 or $40 for identical coverage on the same person. That $8 to $13 monthly difference compounds to $960 to $1,560 over ten years-real money that matters when you’re already stretching your budget. Request quotes with the exact same specifications: same death benefit, same term length, same health profile. Policygenius data from 2023 shows a 35-year-old male paying roughly $30.79 monthly for $500,000 in 20-year term, while a female at the same age and coverage pays about $25.76. These real benchmarks help you spot whether a quote is competitive or inflated. Never accept the first quote. Shopping takes 30 minutes online and saves hundreds of dollars annually.

Understanding Agent Types and Their Incentives

Captive agents must submit all business to one insurer or give that company first refusal rights, which eliminates genuine comparison shopping. Independent agents conduct price, service, and financial strength comparisons across multiple carriers before presenting your options-you receive an unbiased market view instead of a single company’s pitch. Ask your agent directly whether they work with multiple carriers and whether they can show you quotes from at least three different companies for the exact same coverage. Verify the agent’s license using the Licensee Search tool on the Utah Division of Insurance website to confirm they’re licensed for the product they’re selling. The best agent will ask detailed questions about your dependents, your debts, your timeline, and your budget before recommending a specific policy type.

Getting Personalized Recommendations

A strong agent explains why term makes sense for your mortgage payoff timeline but why you might add a small whole life policy for permanent final expense coverage. They won’t push you toward the product with the highest commission-they’ll push you toward the policy that actually solves your problem. At Archibald Insurance Agency, we represent numerous insurance carriers, which means we can compare policies and prices across the entire market instead of being locked into one company’s products. This approach lets us match your specific needs and budget with the right coverage from carriers that fit your situation.

Final Thoughts

Life insurance and types of policies available give you options that match your timeline and budget. Term life delivers affordable protection during your peak earning years when your family depends on your income most, while whole life and universal life provide permanent coverage with cash value growth for those who want lifelong protection. The right choice depends on how long you need coverage, how much death benefit actually protects your family, and what monthly premium fits your budget without strain.

Avoid the trap of selecting based on price alone, since a $27 monthly term policy means nothing if you bought half the coverage you actually need. Calculate your real coverage requirement by adding your mortgage, debts, final expenses, and income replacement for your family’s timeline, then request quotes from multiple carriers using identical specifications so you can spot genuine price differences. Verify that your agent represents multiple insurance companies and can show you options instead of pushing a single product.

Contact Archibald Insurance Agency to discuss your situation with an independent agent who represents numerous carriers and asks the right questions about your dependents, obligations, and budget before recommending specific coverage. Our team helps you understand life insurance and types of policies that actually solve your problem instead of creating confusion. Request quotes this week and lock in affordable protection while you’re healthy and insurable.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation