Affordable Life Insurance Options for Seniors

Many seniors believe life insurance is no longer relevant once they reach retirement age. That’s simply not true-affordable life insurance for seniors serves a real purpose by protecting your family from financial hardship and covering final expenses.

At Archibald Insurance Agency, we work with Utah seniors every day who discover the right coverage fits their budget and their needs. This guide walks you through your actual options so you can make an informed decision.

Why Seniors Really Need Life Insurance

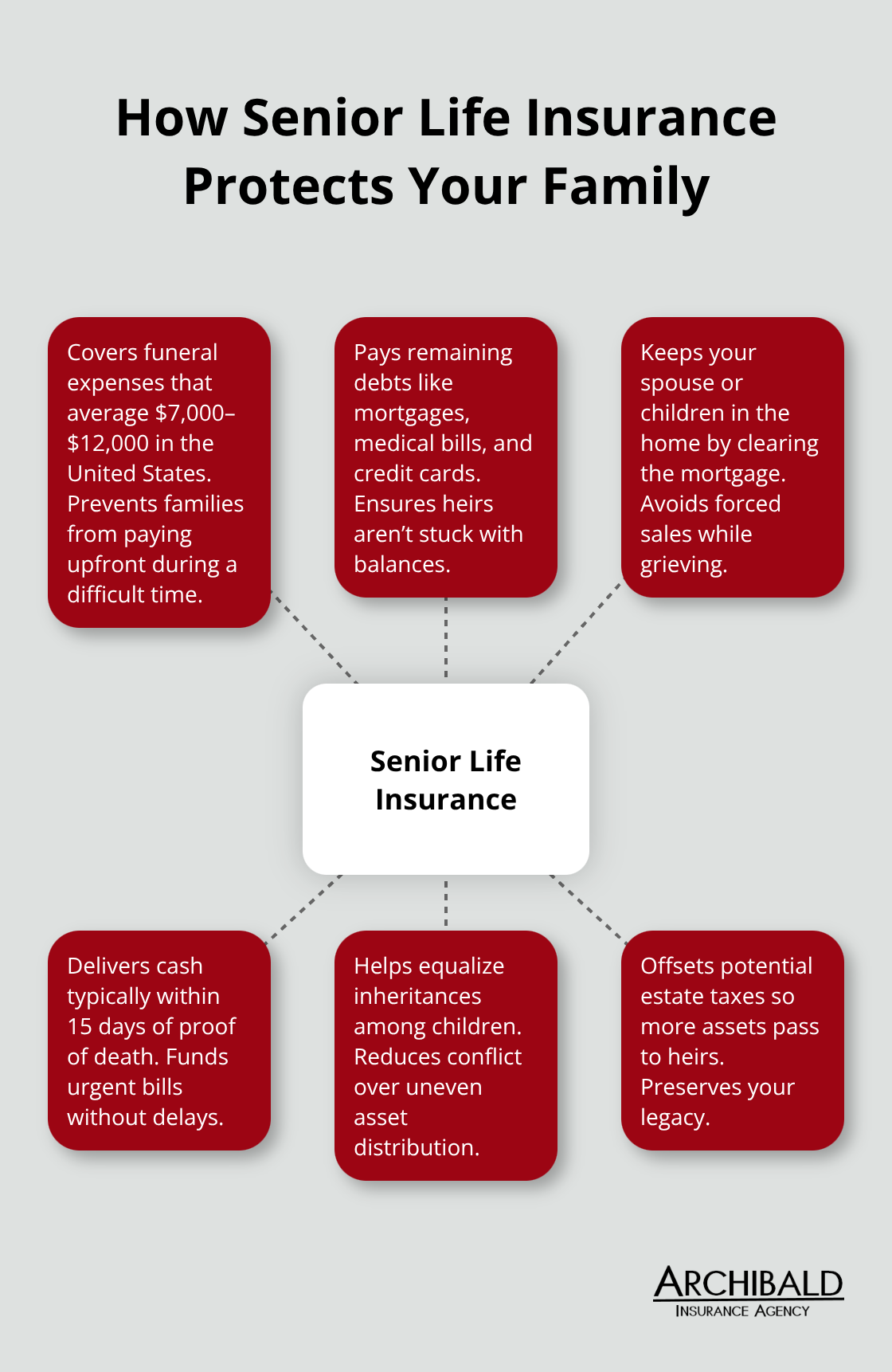

Life insurance for seniors isn’t about replacing income anymore-it’s about protecting what you’ve built and managing costs your family would otherwise face alone. Funeral expenses in the United States average between $7,000 and $12,000, according to industry data. That’s a significant burden to leave behind, especially if your family isn’t prepared. Beyond funerals, seniors often carry remaining debts like mortgages, medical bills, or credit card balances that don’t disappear when you do. Life insurance covers these tangible expenses so your heirs inherit your legacy, not your financial problems.

Some seniors also use coverage to equalize inheritances among children or to cover estate taxes that could consume a substantial portion of assets. The misconception that life insurance is only for working parents with young children misses the reality that life insurance solves a different but equally important problem in retirement.

The Real Cost of Ignoring Coverage

Many seniors assume their savings alone will cover final expenses, but that thinking often leaves families scrambling. A 70-year-old in good health can purchase a 10-year term policy with $250,000 in coverage for roughly $1,283 to $1,382 annually if female, or around $1,872 annually if male, based on current market data from major carriers like Protective Life and Pacific Life. These aren’t expensive premiums when spread across a year, yet they eliminate the need for families to liquidate investments or take loans to cover costs. The alternative-leaving no coverage-means your family absorbs 100 percent of expenses immediately, which can derail their own financial plans and retirement security.

How Coverage Actually Protects Your Family

Life insurance isn’t abstract protection; it’s cash that arrives when your family needs it most. The death benefit typically arrives within 15 days after proof of death, which gives your heirs immediate liquidity to handle pressing bills, funeral arrangements, and outstanding debts without delay. This matters because funeral homes require payment upfront, and creditors don’t pause their collection efforts out of sympathy. If you own a home with a mortgage, life insurance can cover the remaining balance so your spouse or children aren’t forced to sell the property during a time of grief. If you’ve supported adult children financially or co-signed loans, coverage protects them from inheriting those obligations. The protection extends beyond immediate expenses to long-term security-your family keeps their home, maintains their lifestyle, and avoids financial stress during an already difficult period.

What Happens When You Wait

Your age directly affects what you’ll pay for coverage. Life insurance rates typically rise as you age, which means a policy purchased at 65 costs significantly less than the same coverage purchased at 75. A 10-year term for a $1,000,000 policy for females costs roughly $292 per month at age 60, but that same policy jumps to about $855 per month by age 70. Waiting doesn’t make sense financially-you lock in lower rates when you act sooner rather than later. The longer you postpone, the more expensive your options become, and some health conditions that develop later may disqualify you from standard rates altogether.

Understanding Your Options

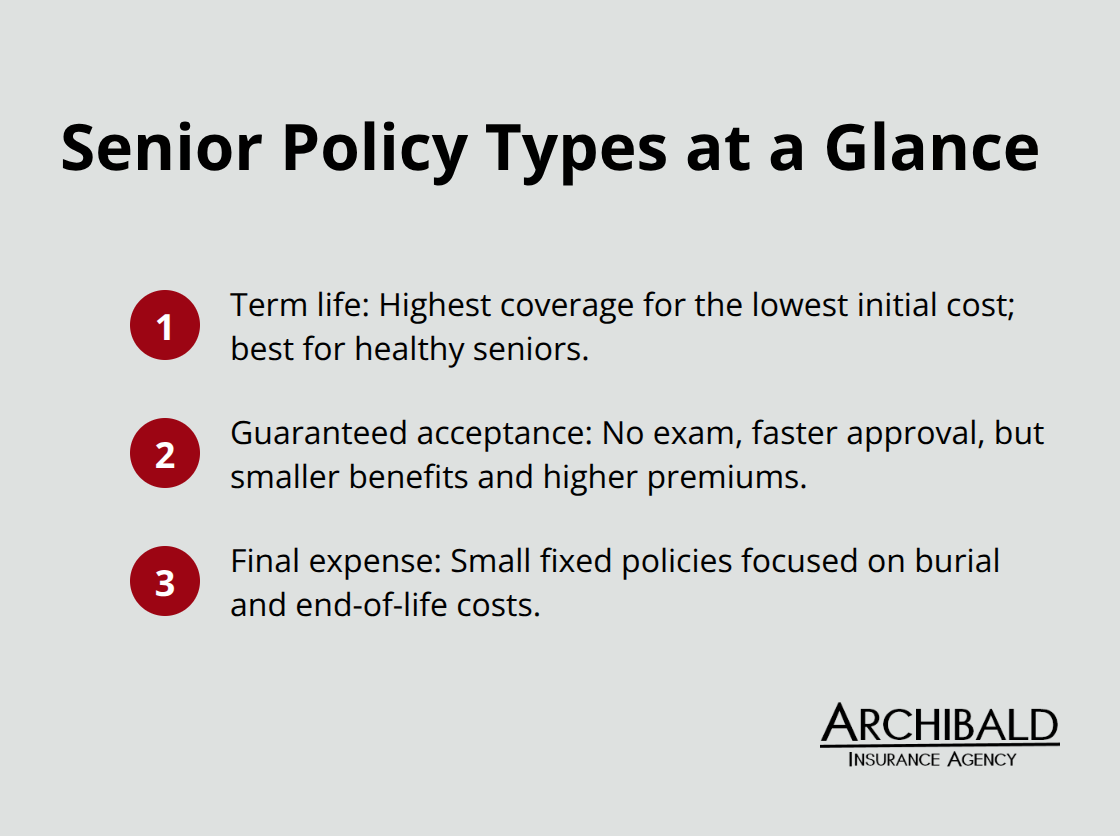

Three main policy types serve seniors well: term life (which offers higher coverage at lower initial cost), guaranteed acceptance life insurance (which requires no medical exam but offers lower coverage), and final expense insurance (which covers burial and end-of-life costs with small, fixed policies). Final expense policies typically range from $5,000 to $35,000 in coverage and don’t require a medical exam. Term life remains the most affordable path for seniors in reasonable health, while guaranteed acceptance policies suit those with serious health issues who want coverage quickly. Understanding which type matches your situation-and your budget-sets the foundation for finding the right protection.

The next section explores each policy type in detail so you can evaluate what actually works for your circumstances.

Which Policy Type Actually Fits Your Budget

Term Life Insurance: Maximum Coverage at Minimum Cost

Term life insurance remains the most practical choice for Utah seniors who want real coverage without overspending. A healthy 70-year-old female can secure a 10-year term policy with $250,000 in coverage for roughly $1,283 to $1,382 annually through carriers like Protective Life or Pacific Life, while males at the same age pay around $1,872 annually for identical coverage. These premiums deliver substantial death benefits at prices that fit retirement budgets, which explains why term policies consistently outperform whole life for affordability.

If you need $500,000 in coverage, expect to pay around $2,319 to $2,460 annually as a female or $3,390 as a male at age 70. The math is straightforward: term life costs far less than whole life because you pay only for the death benefit itself, not cash value accumulation or internal policy costs that eat into permanent coverage. For seniors in good health, term life solves the protection problem without creating a new budget problem.

Whole Life Insurance: When Permanent Coverage Makes Sense

Whole life insurance carries a completely different purpose and price tag, which is why it makes sense only for specific situations. A whole life policy builds cash value over time, meaning a portion of your premium goes toward an investment account you can borrow against or withdraw from later. That flexibility comes at a cost: whole life premiums run 5 to 15 times higher than comparable term policies, according to industry analysis from Policygenius.

For a senior who simply wants to cover final expenses or protect their family from debt, whole life becomes an expensive solution to a straightforward problem. However, if you have substantial assets, want lifetime coverage that never expires, or need a policy that builds wealth for your heirs, whole life deserves consideration despite the higher cost. The decision hinges on whether you need permanent protection or temporary coverage that solves your immediate financial concerns.

Guaranteed Acceptance: Coverage When Health Complications Arise

Guaranteed acceptance life insurance serves a different population entirely-seniors with serious health conditions who cannot qualify for standard term rates. These policies require no medical exam and accept applicants with pre-existing conditions, but coverage limits stay small, typically $10,000 to $25,000, and premiums run considerably higher than term policies for the same amount of benefit.

Ethos offers the cheapest guaranteed acceptance policies, starting around $20 monthly for females and $29 monthly for males for approximately $10,000 of coverage. If you have diabetes, heart disease, or other chronic conditions that disqualify you from standard underwriting, guaranteed acceptance provides the only realistic path to coverage, despite the cost and modest benefit amounts. Once you understand which policy type matches your health and financial situation, the next step involves comparing actual quotes from multiple carriers to lock in the best rates available to you.

Shopping for the Best Senior Life Insurance Rates

Compare Quotes Across Multiple Carriers

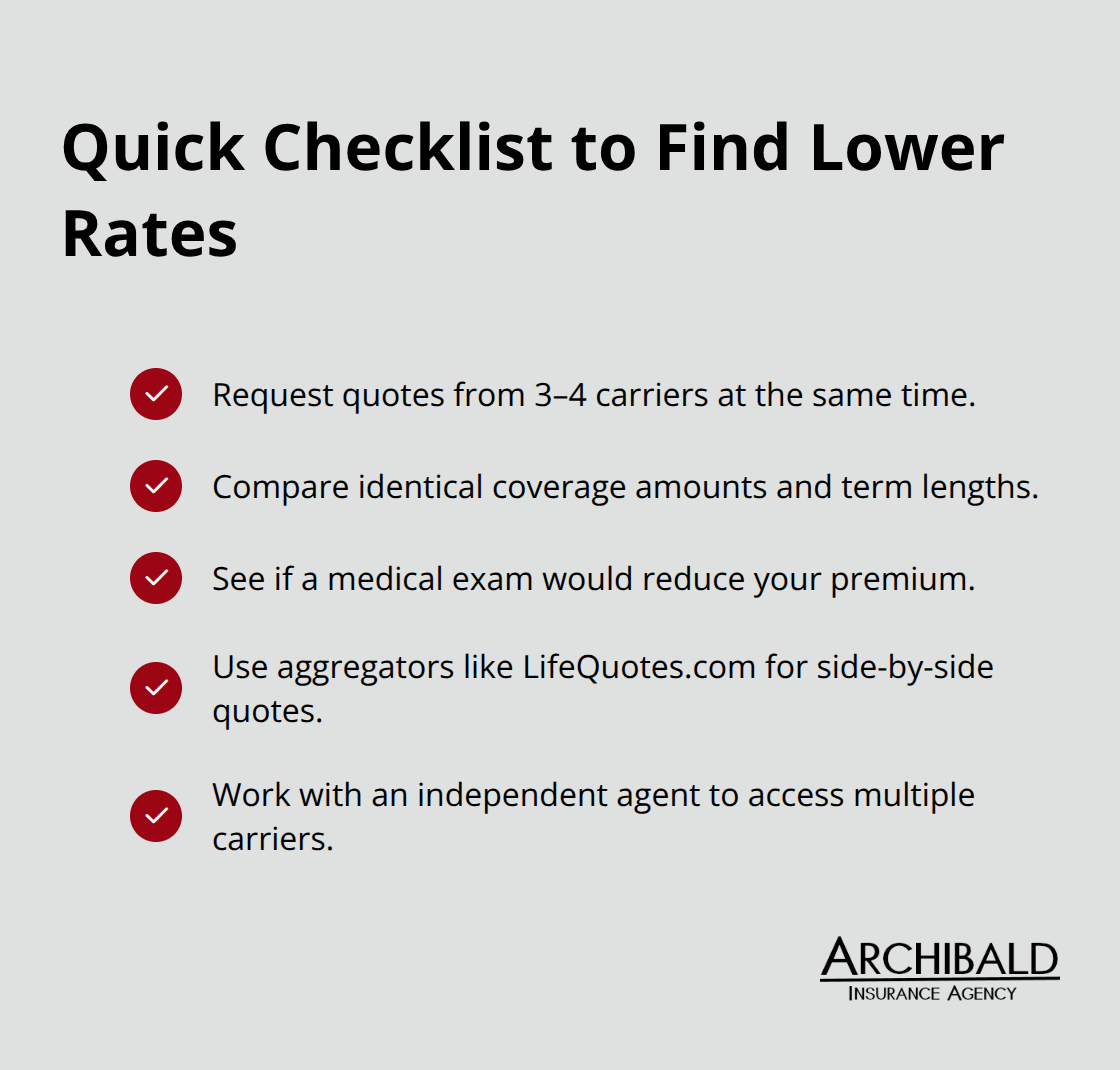

Finding affordable life insurance requires comparing actual quotes rather than relying on advertised rates or assumptions about what coverage costs. When you request quotes from three or four carriers simultaneously, you discover that premiums vary significantly based on how each insurer assesses your health and age. A 70-year-old female might pay $1,283 annually through Protective Life for a $250,000 10-year term but $1,382 through Pacific Life for identical coverage-a $99 difference that compounds over a decade. For males at the same age, Penn Mutual and Transamerica often deliver the lowest rates, with Penn Mutual quoting around $1,872 for $250,000 coverage while Transamerica quotes considerably higher for $500,000 policies.

These differences matter because choosing the cheaper carrier saves hundreds of dollars without sacrificing coverage quality or financial strength. Sites like LifeQuotes.com allow you to input your information once and receive quotes from multiple carriers side by side, eliminating the need to contact each company individually. The comparison process takes roughly 15 minutes and reveals whether a medical exam will lower your rates or whether guaranteed acceptance makes more financial sense given your health history.

Evaluate Whether a Medical Exam Saves Money

Your health status determines whether undergoing a medical exam actually saves money. Healthy seniors consistently pay less with full underwriting because insurers reward lower risk with lower premiums, but seniors with serious health conditions often find guaranteed acceptance policies cheaper than paying standard rates adjusted for their medical history. Nationwide consistently ranks as the cheapest overall option for healthy seniors, with 10-year term policies running about $121 monthly for men and $86 monthly for women for $500,000 coverage.

However, if you smoke or have pre-existing conditions, carriers like Protective Insurance, Assurity, and Lincoln Financial offer more competitive rates than standard quotes suggest. Some carriers reduce rates after one year of quitting smoking, so if you recently quit, mention this to each insurer since not all carriers update rates automatically.

Work with an Independent Agent

An independent agent who represents multiple carriers eliminates the legwork of contacting insurers individually while ensuring you receive consistent rate quotes across the same coverage amounts and policy lengths. This approach saves time and helps you identify which carrier offers the best value for your specific situation. Premium differences at age 70 represent substantial money over a 10-year term, making the effort to compare worthwhile.

Final Thoughts

Affordable life insurance for seniors becomes straightforward once you understand your options and what each policy type delivers. Term life remains the most practical choice for Utah seniors who want substantial coverage without excessive premiums, while guaranteed acceptance policies serve those with health conditions that prevent standard underwriting. Gather quotes from three to four carriers using your actual health information, then compare the premiums side by side for identical coverage amounts and policy lengths-this process takes roughly 15 minutes and reveals whether a medical exam will lower your rates.

Working with an independent agent eliminates the burden of contacting multiple insurers individually while ensuring you receive consistent quotes that allow for genuine comparison. At Archibald Insurance Agency, our team represents numerous carriers and specializes in helping Utah seniors find coverage that fits both their protection needs and their retirement budgets. We understand that life insurance decisions feel overwhelming, which is why we guide you through each option and explain what you’re actually paying for.

Contact Archibald Insurance Agency to discuss your situation and receive personalized recommendations based on your health, age, and financial goals. The protection your family needs is within reach, and the time to act is now while your rates remain as low as possible.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation