What is Universal Life Insurance?

Universal life insurance offers flexibility that other life insurance policies simply don’t match. You can adjust your premiums and death benefit as your circumstances change, making it a practical choice for people whose financial situations aren’t static.

At Archibald Insurance Agency, we help Utah residents understand whether universal life insurance fits their needs. This guide breaks down how it works, compares it to other options, and shows you who benefits most from this coverage.

How Universal Life Insurance Actually Works

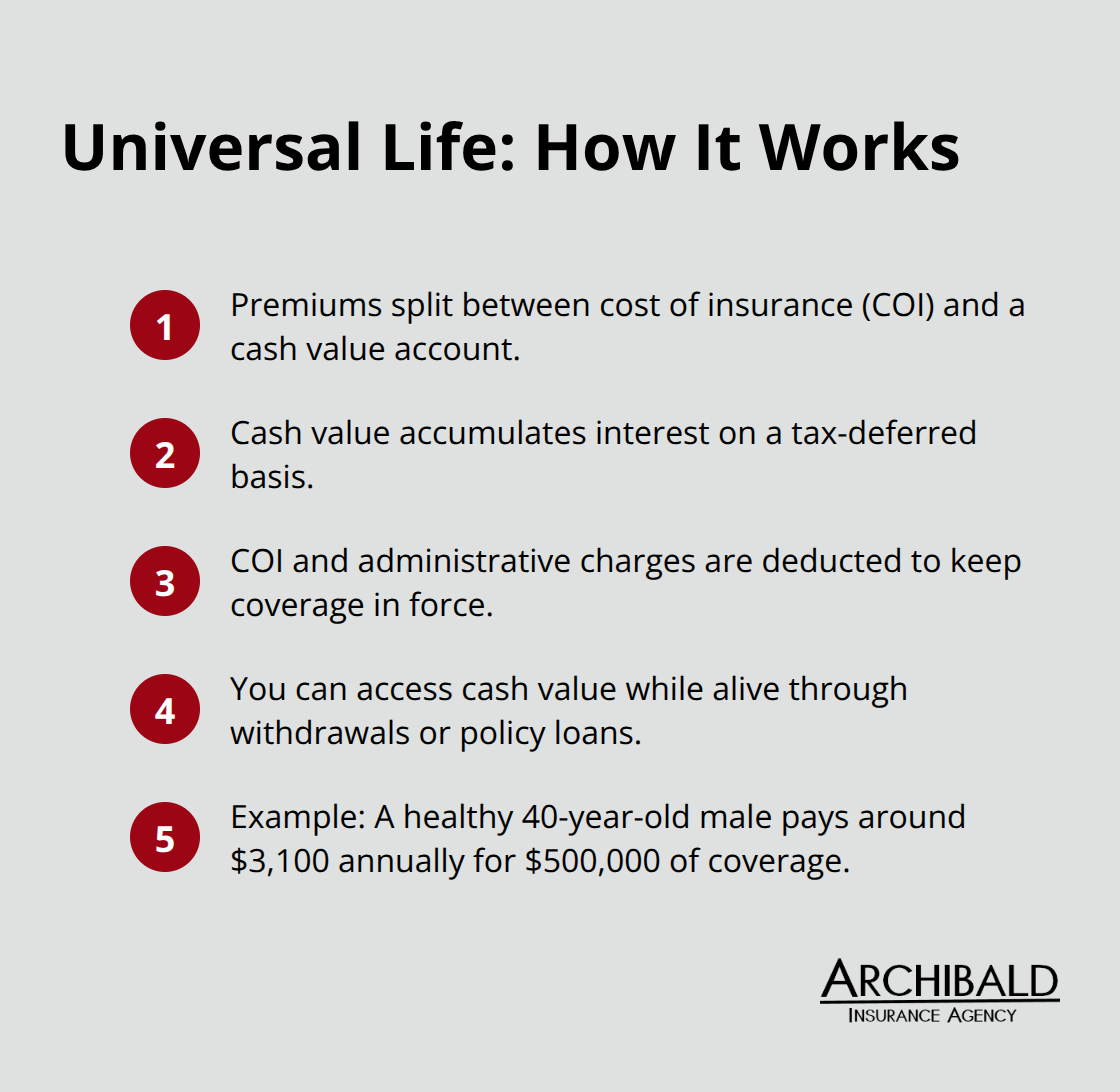

Universal life insurance functions differently from term coverage because your premiums don’t simply vanish after payment. When you pay a premium, that money splits into two parts: the cost of insurance (COI) and the remainder flows into a cash value account. The COI covers your death benefit and administrative fees, while everything else accumulates and earns interest.

According to the National Association of Insurance Commissioners, the cash value grows on a tax-deferred basis, meaning you won’t pay taxes on the growth until you access the money. This structure gives you something term insurance never provides: a living benefit you can tap into while you’re still alive. For a healthy 40-year-old male seeking $500,000 in coverage, expect minimum premiums around $3,100 annually, though your actual costs depend on age, health, and the specific policy terms.

Premium Flexibility That Adapts to Your Life

The appeal of universal life lies in its flexibility. You can increase or decrease your premiums within policy limits, and you can adjust your death benefit up or down as circumstances change. If your income drops, you lower payments temporarily. If you receive a promotion, you increase coverage without applying for a new policy. This flexibility makes universal life far superior to whole life for people whose finances fluctuate, like business owners or self-employed professionals. However, this freedom carries responsibility: underfunding your policy creates real problems. If your cash value plus credited interest falls below your ongoing charges, the account erodes and your coverage could lapse entirely. The cost of insurance rises with age, which means a 50-year-old pays more for the same death benefit than a 40-year-old. Front-load premiums in early years to build a stronger cash value cushion that protects you from future lapses when COI climbs.

How Cash Value Growth and Fees Shape Your Coverage

Your policy’s cash value determines how long you can maintain coverage without paying premiums. The guaranteed minimum interest rate sits at 2% annually, but current credited rates depend on company performance. Withdrawals from cash value work tax-free up to your cost basis, though anything beyond that triggers taxes and reduces your death benefit. Policy loans offer another option: you borrow against your cash value (typically available from year two onward), and these loans carry interest costs that reduce your death benefit if left unpaid. The real threat to universal life policies comes from fees that erode your cash value faster than it grows. Administrative charges, cost of insurance increases, and surrender charges in early years can slow growth significantly. This is why comparing guaranteed versus nonguaranteed features matters enormously when shopping policies. A policy with high fees might deliver less cash value than one with minimal charges. Before purchasing, obtain a year-by-year illustration showing projected cash value and death benefits (then verify the guaranteed minimum crediting rate and total fee structure with your agent).

What Happens When You Access Your Cash Value

You can withdraw funds from your cash value tax-free up to your cost basis, though withdrawals beyond that amount trigger tax consequences and reduce your death benefit. Policy loans provide an alternative that typically becomes available from year two onward, and you can access these funds without triggering immediate taxes as long as the policy remains in force. However, unpaid loans accumulate interest and reduce your death benefit if they’re not repaid. The key distinction between withdrawals and loans matters significantly for your long-term coverage. Withdrawals permanently reduce your cash value and death benefit, while loans preserve the death benefit structure but cost you interest. Overusing either option can eventually cause your policy to lapse if the remaining cash value can’t cover your cost of insurance charges.

Comparing Policies Before You Commit

Shopping for universal life insurance requires more than just comparing premiums. You need to examine the guaranteed minimum crediting rate, the current credited rate, total fees, surrender charges, and available riders. Request a year-by-year illustration from each carrier showing projected cash value and death benefits under different scenarios. Verify the guaranteed minimum crediting rate and total fee structure with your agent before making a decision. Understanding these details helps you avoid policies that look attractive initially but underperform over time due to hidden costs.

Now that you understand how universal life insurance works internally, comparing it to other life insurance types reveals which option truly fits your situation.

Universal Life Insurance vs. Other Life Insurance Types

Term Life Insurance: Affordable but Temporary

Term life insurance costs far less upfront because it provides pure death benefit coverage with no cash value component. A 40-year-old in good health pays roughly $30–$50 monthly for $500,000 in 20-year term coverage, compared to the $258+ monthly minimum for universal life with the same death benefit. Term makes sense if you need affordable coverage for a specific period-your mortgage years, your children’s education, or until retirement. However, term expires. Once your 20 or 30-year term ends, you face a choice: go without coverage or buy a new policy at an age when premiums skyrocket. Universal life solves this problem because it lasts your entire life as long as you fund it properly. The trade-off is clear: you pay significantly more annually, but you never outlive your coverage and you build cash value that term never provides.

Whole Life Insurance: Guaranteed but Expensive

Whole life insurance guarantees everything-your premiums never increase, your death benefit stays level, and your cash value grows predictably because the insurer credits a guaranteed rate plus dividends. This certainty appeals to people who dislike complexity, but whole life costs roughly 2–3 times more than universal life for identical death benefits. A $500,000 whole life policy for a 40-year-old costs approximately $600–$800 monthly versus $258+ for universal life. Universal life wins on cost flexibility because you adjust premiums and death benefits as circumstances change, while whole life locks you into fixed payments. However, universal life’s flexibility creates risk: if you underfund the policy or market returns underperform, your cash value erodes and coverage lapses. Whole life eliminates this risk entirely through guaranteed crediting.

Variable and Indexed Universal Life: Higher Growth, Different Risk Levels

Variable universal life (VUL) represents the aggressive alternative-your cash value invests directly in stocks, bonds, and mutual funds rather than earning a fixed interest rate. VUL offers higher growth potential than fixed universal life, but your cash value fluctuates with market performance and you absorb all investment losses. If the market crashes during your accumulation years, your policy’s cash value drops and your cost of insurance charges consume a larger percentage of remaining funds. Universal life with index participation (IUL) splits the difference: your cash value ties to stock market indices like the S&P 500 with typical caps around 10.5% annual returns and guaranteed floors preventing losses. IUL costs more than fixed universal life but delivers better growth potential than fixed rates while protecting you from market downturns-making it the sensible middle ground between fixed universal life’s safety and VUL’s volatility.

Understanding these distinctions helps you recognize which policy structure aligns with your financial goals and risk tolerance. The next section examines who benefits most from universal life’s unique combination of flexibility and permanent protection.

Who Should Consider Universal Life Insurance

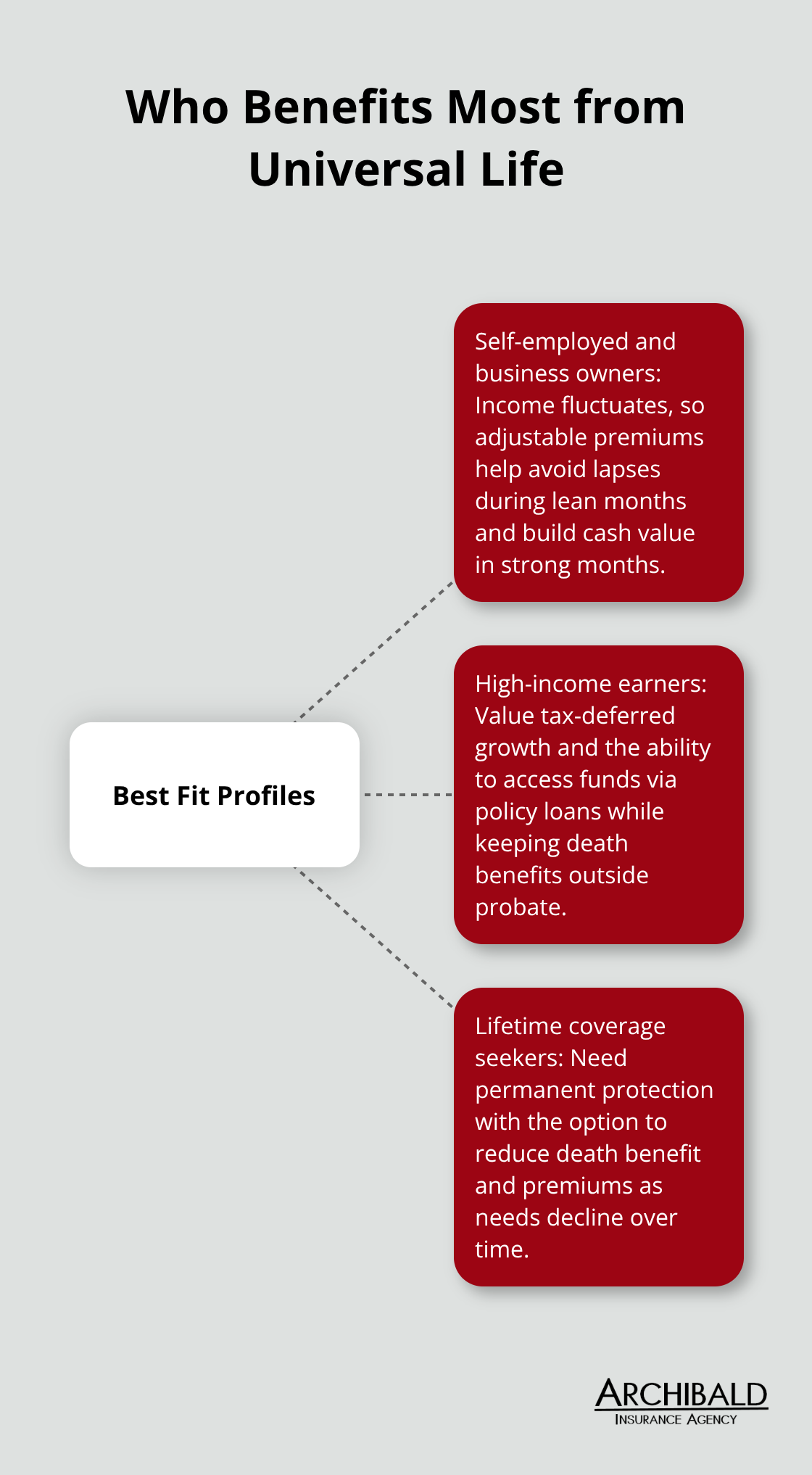

Universal life insurance appeals most to people whose financial situations shift regularly and who need coverage lasting decades. Business owners and self-employed professionals fit this profile perfectly because their income fluctuates month to month and year to year.

Self-Employed Professionals and Income Fluctuation

A self-employed consultant earning $80,000 one year and $150,000 the next cannot predict whether they can afford fixed whole life premiums, but universal life’s adjustable payments solve this problem entirely. During lean months, you lower premiums; during profitable months, you increase them to build cash value faster. This flexibility prevents policy lapse that would occur if you couldn’t maintain whole life’s rigid payment schedule.

Self-employed individuals also benefit from universal life’s cash value as a secondary retirement resource. If business revenue dries up at age 58, you can access policy loans against accumulated cash value to supplement income without triggering taxes (as long as the policy stays in force). This safety net protects your family when business conditions deteriorate unexpectedly.

High-Income Earners and Tax Advantages

High-income earners face a different but equally compelling reason to choose universal life: their tax situations improve substantially with tax-deferred cash value growth. Someone earning $250,000 annually pays taxes on every investment dollar, but universal life’s cash value grows tax-free until withdrawal. Over 30 years, this tax deferral compounds meaningfully.

If your cash value reaches $400,000 and you access it through policy loans rather than withdrawals, you avoid immediate tax consequences entirely. High earners also appreciate that universal life death benefits bypass probate and transfer directly to beneficiaries, protecting wealth during estate settlement. This feature streamlines the transfer process and reduces administrative costs for your heirs.

Lifetime Coverage with Adjustment Capability

People seeking genuine lifetime coverage with adjustment capability represent the third critical group for universal life. A 35-year-old professional might purchase $1,000,000 in coverage to protect their family and mortgage, but at 50, they’ve paid off the house and accumulated retirement savings, so they reduce the death benefit to $500,000 and lower premiums accordingly. Whole life doesn’t permit this adjustment without complex policy exchanges.

Universal life also outperforms term insurance for anyone who recognizes they’ll need coverage beyond their working years. Term policies expire at 65 or 70, forcing seniors to either go uninsured or purchase expensive new coverage when health issues emerge. Universal life eliminates this problem entirely if properly funded throughout your career. Regular policy reviews help monitor whether premiums, cost of insurance charges, and cash value remain aligned with your death benefit goals as you age. This ongoing relationship matters more than the initial policy selection because universal life’s flexibility only benefits you if you actively adjust it when circumstances change.

Final Thoughts

Universal life insurance delivers permanent protection with flexibility that term and whole life policies cannot match. You control your premiums and death benefit, your cash value grows tax-deferred, and you access funds through loans or withdrawals when life demands it. The trade-off is straightforward: you pay more than term insurance but gain lifetime coverage and a living benefit that builds over decades.

We at Archibald Insurance Agency work with Utah residents to match them with coverage that fits their financial reality, not some theoretical ideal. Our team represents multiple insurance carriers, which means we compare policies across different companies rather than pushing one product. Whether you’re self-employed with fluctuating income, a high earner seeking tax advantages, or someone who simply wants lifetime protection with adjustment capability, we help you evaluate universal life alongside term and whole life options.

Contact Archibald Insurance Agency for a conversation about your life insurance needs. We’ll ask questions about your family situation, financial goals, and timeline for coverage, then present options with honest comparisons of costs, fees, and projected cash value growth. You’ll have the information needed to make a decision that protects your family and aligns with your budget.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation