Local Utah Insurance Broker: Your Community Connection

Insurance decisions shouldn’t feel like you’re navigating alone. A local Utah insurance broker understands your community’s specific risks and can match you with coverage that actually fits your life.

At Archibald Insurance Agency, we’ve spent years building relationships with Utah families and businesses. We know what matters to you because we live here too.

Why Local Brokers Understand Utah Better

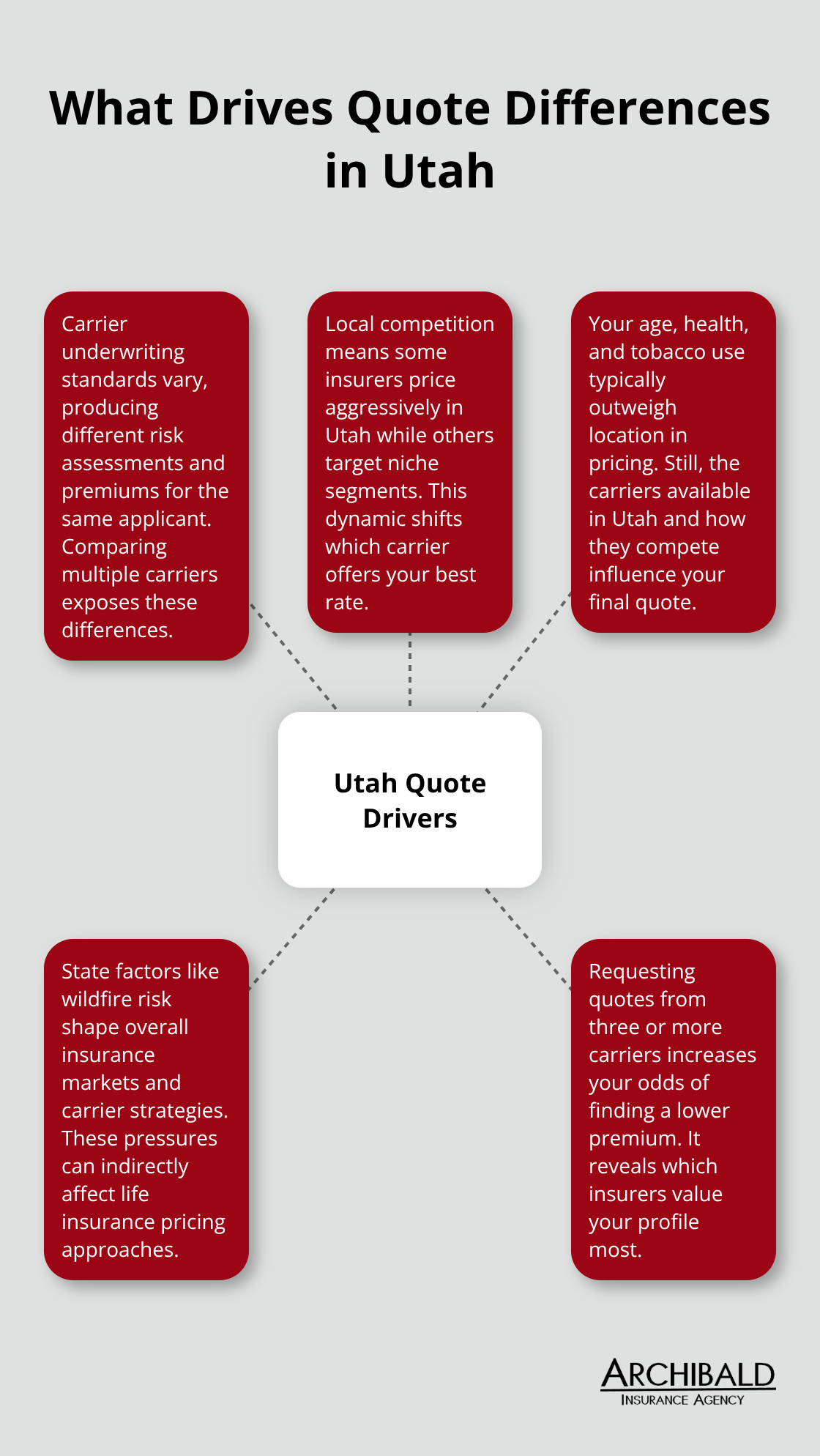

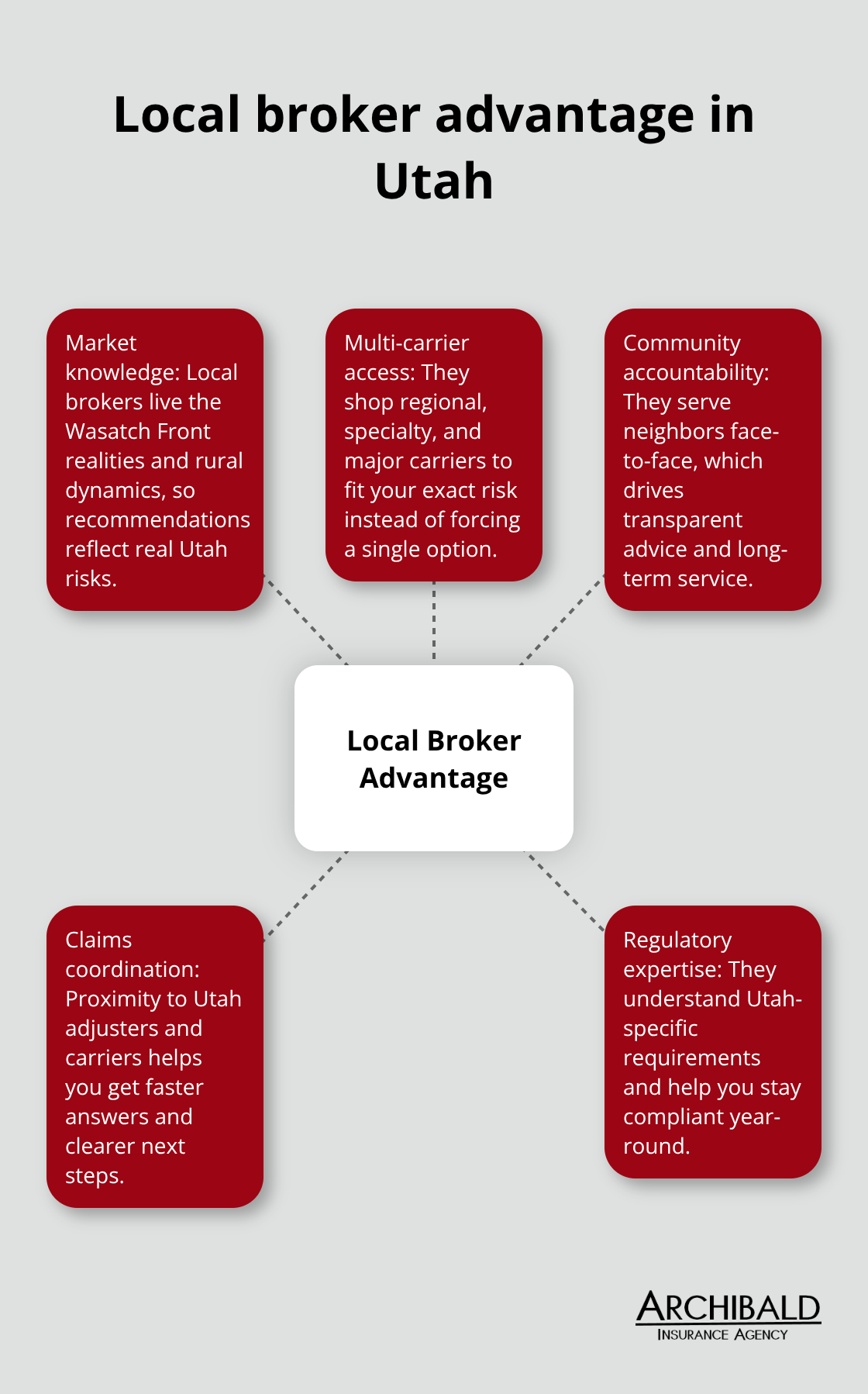

Utah’s insurance landscape differs significantly from national markets. The state’s rapid population growth, concentrated along the Wasatch Front, creates distinct patterns in auto claims and home values that national insurers often miss. Utah’s winter weather patterns, elevation variations, and unique driving corridors mean that coverage needs in Salt Lake City differ from those in rural counties. Local brokers grasp these specifics because they operate within the market daily, not from distant corporate centers. When you work with a local broker, you already have someone who knows the regional context without explanation.

What sets local brokers apart from national companies

National insurance companies operate through captive agents tied to a single insurer’s products. Captive agents cannot shop your risk across multiple carriers, leaving you with whatever that one company offers. Independent brokers represent multiple carriers, which means we can access smaller and specialty insurers alongside major names. For Utah homeowners facing rising costs or nonrenewal letters, this multi-carrier access uncovers affordable options that direct online shopping never surfaces. For high-risk drivers, independent brokers place nonstandard auto policies with carriers that captive agents simply cannot reach. National companies prioritize efficiency and scale; local brokers prioritize fit and outcomes for individual clients.

Trust built on shared community stakes

A local broker’s reputation depends on the community where they live. Unlike national customer service centers, local brokers face their clients at the grocery store, at church, and at community events. This creates accountability that remote relationships cannot match. Maintaining continuous liability coverage protects both your driving privilege and your financial security. A local broker helps you stay compliant because your compliance reflects directly on their credibility. When you renew your policy or file a claim, you work with someone who understands Utah’s specific regulatory environment and maintains professional relationships with local carriers and adjusters. This proximity matters when you need fast answers about coverage gaps or claims support.

How local market knowledge translates to better coverage

Local brokers understand which carriers write policies in your specific area and which ones have pulled back from certain regions. They know which insurers respond quickly to Utah claims and which ones have strong financial ratings. This knowledge (built through years of direct experience) helps them match you with carriers that actually want your business, not ones that will cancel you after a claim. A broker who operates in your community can also alert you to coverage gaps before problems arise, whether that means adjusting your homeowners limits for Utah’s elevation or adding uninsured motorist protection for local driving conditions.

Moving toward personalized solutions

Understanding Utah’s market is only the first step. The real value emerges when a local broker applies that knowledge to your specific situation, assessing what coverage you actually need rather than what a national algorithm suggests.

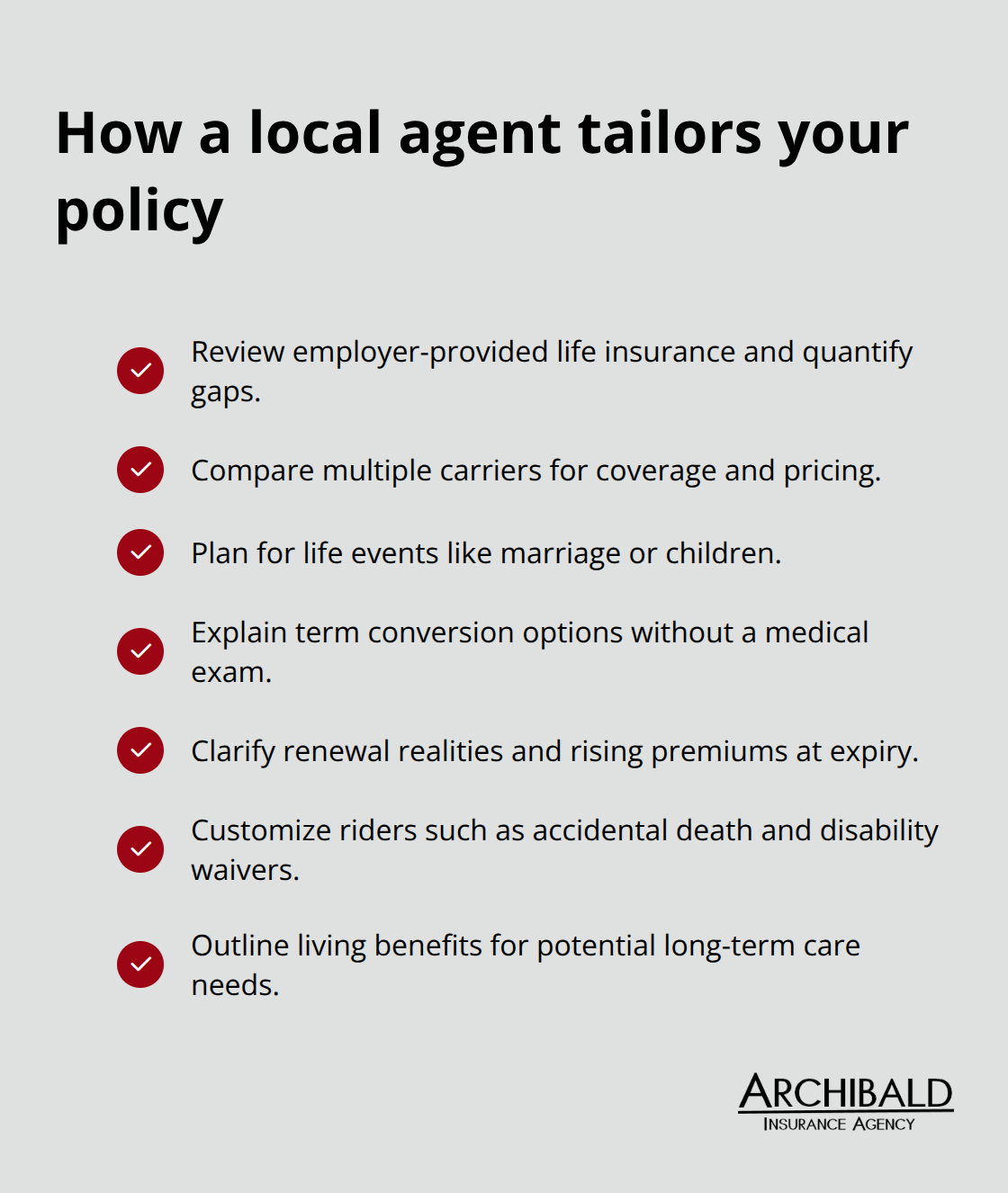

What Coverage Do You Actually Need in Utah?

Most Utah residents carry insurance they don’t fully understand, leaving gaps where they need protection and paying for coverage they’ll never use. A local broker’s first job involves asking hard questions about your actual situation, not selling you a predetermined package. Do you own your home or rent? How many miles do you drive annually on I-15 versus rural roads? Does your business operate from a fixed location or involve client visits across the state? These specifics matter because Utah’s elevation, weather patterns, and driving corridors create different risk profiles than national averages suggest.

How Utah’s geography shapes your coverage needs

Someone in Park City faces avalanche risks and seasonal road conditions that don’t apply in St. George. A contractor working across multiple counties needs different coverage than an office-based professional. A broker who knows Utah assesses these factors directly with you, then matches carriers accordingly. National online tools cannot replicate this conversation because they rely on demographic shortcuts rather than your actual exposure. Your zip code alone tells a national algorithm almost nothing about whether you need additional liability limits or specialized coverage for your specific situation.

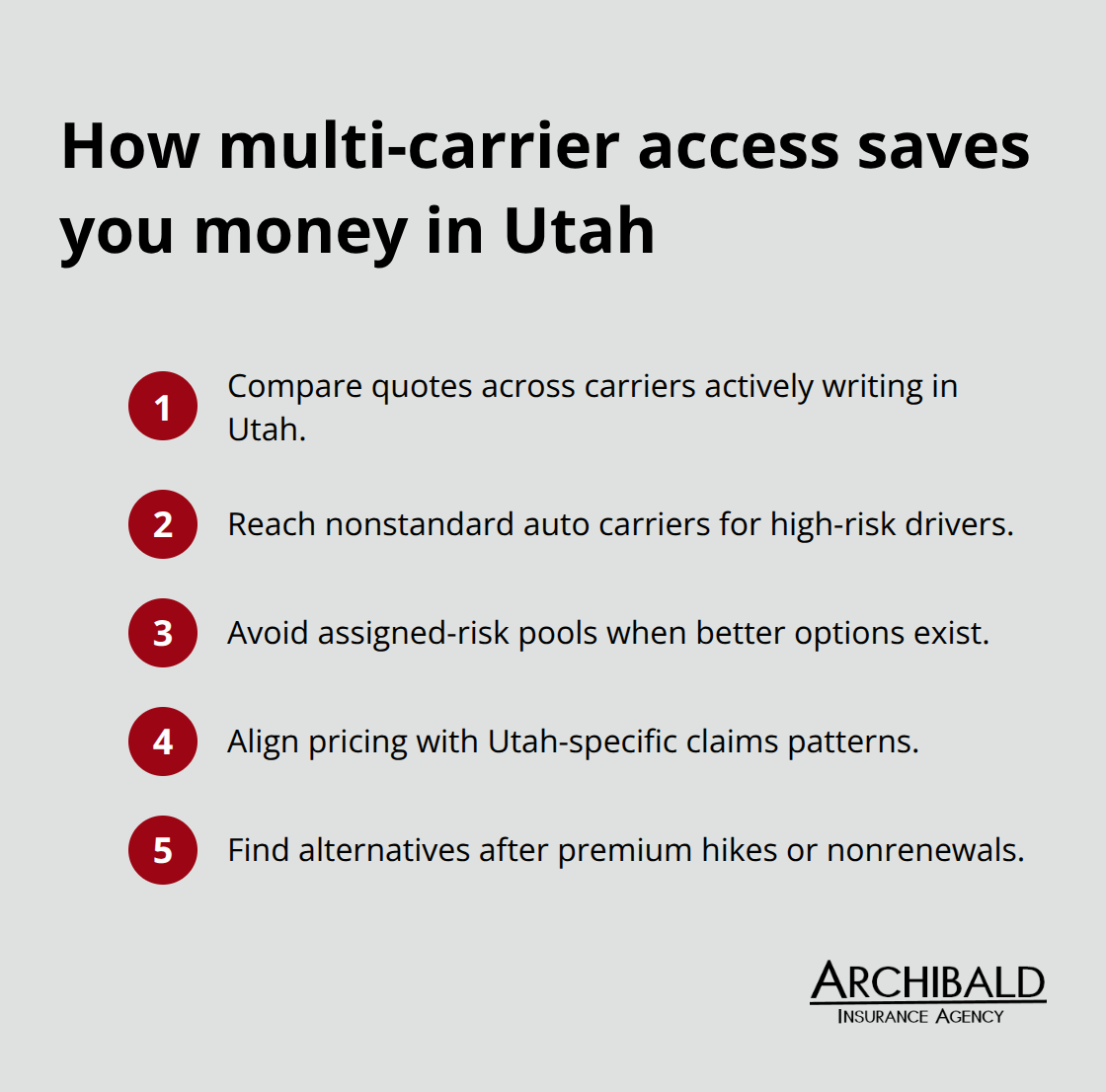

Why multi-carrier access matters for your wallet

Once your coverage needs are clear, a local broker’s multi-carrier access becomes your competitive advantage. Instead of accepting whatever one company offers, you see quotes from carriers that actively write in Utah and understand regional claims patterns. For auto insurance, independent brokers access nonstandard carriers for high-risk drivers that captive agents cannot reach, potentially saving hundreds annually compared to assigned-risk pools.

For homeowners insurance, Utah residents facing rising premiums or nonrenewal notices benefit from brokers who shop specialty carriers and regional insurers that major national companies have deprioritized.

Finding coverage for complex situations

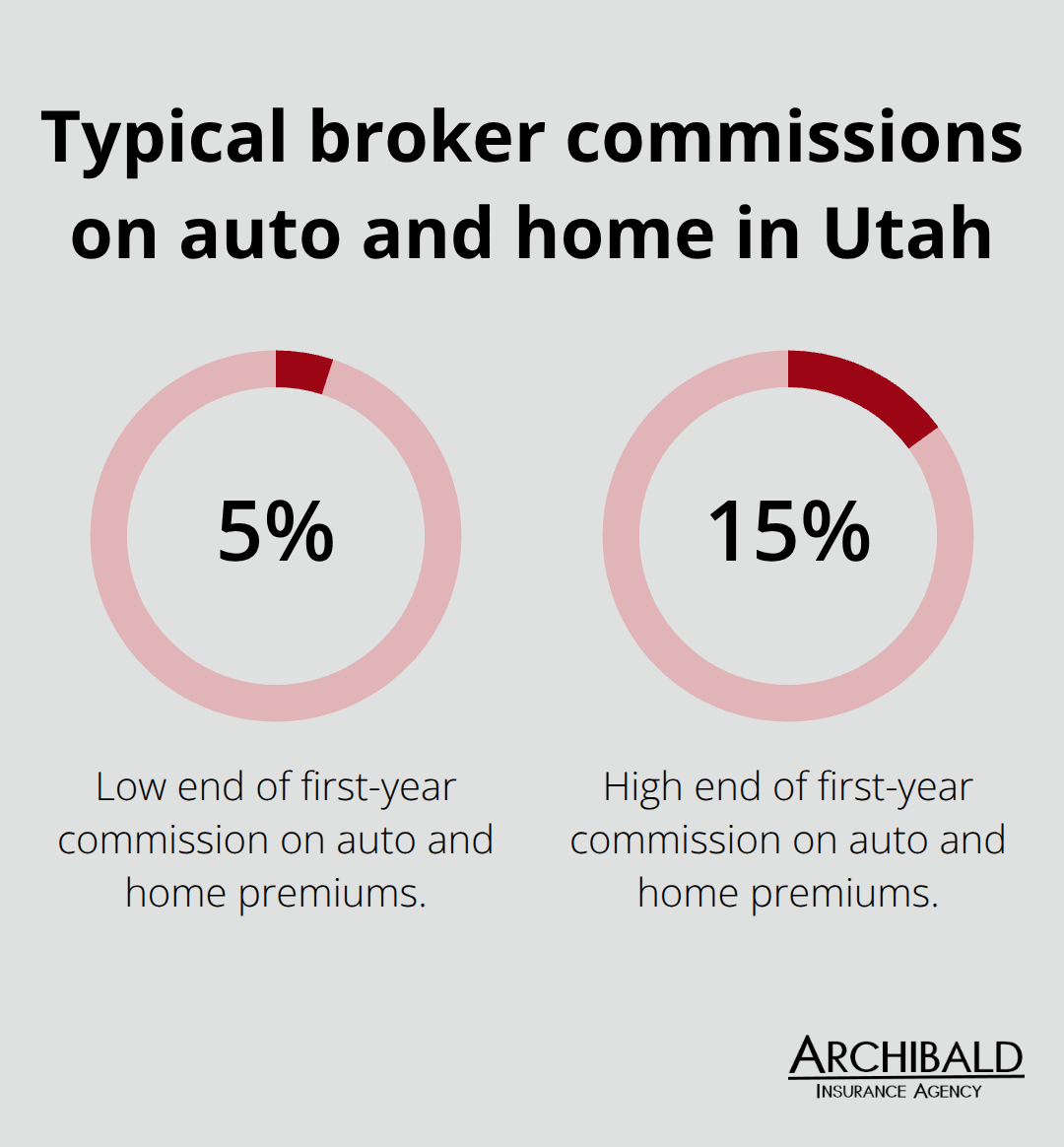

Life insurance buyers with pre-existing conditions or hazardous occupations find carriers through independent brokers who specialize in impaired-risk underwriting, making coverage affordable where direct applications would face decline or heavy loadings. The commission structure for brokers (typically five to fifteen percent of first-year auto and home premiums) aligns incentives toward finding you the right fit rather than the most expensive option, since a lower premium still generates reasonable commission while keeping you satisfied long-term.

Comparing options that actually fit your risk

Cost-effective coverage emerges not from shopping the cheapest quote but from matching your actual risk to carriers positioned to serve it. Brokers filter options so you see clear comparisons rather than endless possibilities. This approach works because carriers specialize in different risk profiles-some excel at insuring young families in suburban areas, while others focus on rural properties or business owners with complex exposures. A broker who understands Utah’s market knows which carriers want your specific type of risk and which ones will simply decline or price you out of the market.

When you’ve identified what you actually need and understand which carriers fit your situation, the next step involves protecting that coverage and staying compliant with Utah’s insurance requirements.

How We Serve Your Insurance Needs

At Archibald Insurance Agency, we handle auto, home, business, and life insurance because Utah families and business owners need someone who understands all these areas together, not separately. When you own a home and operate a side business, your insurance picture becomes complex fast. A homeowners policy does not cover business liability. Your personal auto policy will not protect you if you use your vehicle for commercial purposes. Life insurance needs change once you have dependents relying on your income or a business that others depend on. We work across all four lines because we have learned that compartmentalized insurance leaves gaps. Someone who only sells auto insurance misses the fact that your business vehicle needs different coverage than your family car, or that your life insurance should reflect both personal obligations and business continuity.

Coordinating Coverage Across Multiple Lines

We represent numerous carriers across these lines, which means we can coordinate your coverage so everything works together rather than against each other. When you file a claim on your home, we already know your auto history and life situation, so we can advise whether additional coverage might have prevented the loss or will prevent future ones. This integrated approach costs nothing extra but catches problems that single-line agents never see. Your coverage needs shift when you marry, buy a second property, start a business, or retire. Most agents see you at purchase and disappear. We review your policies periodically because what worked five years ago may leave you exposed today.

Questions That Reveal Coverage Gaps

Expert guidance means we ask questions most agents skip. How often do you drive your business vehicle versus personal use? Are your business assets adequately covered under your homeowners policy, or do you need commercial property coverage? If something happened to you, could your family maintain the mortgage, or does your life insurance need adjustment? Do you have adequate liability limits for Utah’s legal environment, or are you underinsured relative to your actual exposure? These conversations take time, which is why we do not rush through applications or push policies out the door.

Understanding Utah’s Regulatory Requirements

When you work with us, you get someone who knows Utah’s regulations and carrier landscape well enough to spot what you are missing. Utah Code Ann. Section 31A-22-302 requires continuous liability coverage for all registered vehicles, and we make sure you understand what that means and how to maintain proof. We also know which carriers respond quickly to Utah claims and which ones have pulled back from certain counties, so we match you with insurers positioned to serve your specific situation rather than ones that will deny you at renewal.

Adapting Coverage as Your Life Changes

If your home value has increased with Utah’s real estate market, your limits might be inadequate. If you have added business income, your liability needs have changed. If your children have moved out and your dependents have decreased, your life insurance amount might be excessive. These reviews cost nothing but often reveal savings or necessary upgrades that protect you better than your current setup.

Final Thoughts

A local Utah insurance broker does more than sell policies-we understand your community’s specific risks, coordinate coverage across multiple lines, and stay accountable to the people we serve. When you work with an independent broker, you gain access to carriers that captive agents cannot reach, which translates directly to better options and often lower costs. Utah families and businesses choose independent brokers because we know the regional market, ask the right questions about your actual needs, and review your coverage as your life changes.

At Archibald Insurance Agency, we have built our reputation on reliability and trust with Utah families and business owners. We represent numerous carriers across auto, home, business, and life insurance, which means we can coordinate your entire coverage picture rather than leaving gaps between separate policies. Our team takes time to understand your situation, assess what you actually need, and match you with carriers positioned to serve your specific risk.

Contact Archibald Insurance Agency to discuss your coverage needs without pressure or predetermined packages. Your insurance should fit your life, not force you into someone else’s standard offering-that is what a local Utah insurance broker provides.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation

Leaving your home for an extended period of time, whether for a vacation or as a snowbird seeking warmer climates, requires careful preparation to ensure the safety and security of your property. The last thing you want is to return to a home damaged by a burst pipe or burglarized. To protect your home and give yourself peace of mind while you’re away, follow this comprehensive checklist:

Leaving your home for an extended period of time, whether for a vacation or as a snowbird seeking warmer climates, requires careful preparation to ensure the safety and security of your property. The last thing you want is to return to a home damaged by a burst pipe or burglarized. To protect your home and give yourself peace of mind while you’re away, follow this comprehensive checklist:

“I was involved in an accident, and to make matters worse, the other party doesn’t have insurance.” It’s a frustrating and stressful situation that no one wants to experience. However, there are measures you can take to protect yourself from such incidents. One important aspect is having the right insurance coverage, specifically uninsured motorist coverage, which can provide you with the necessary financial support in these unfortunate circumstances.

“I was involved in an accident, and to make matters worse, the other party doesn’t have insurance.” It’s a frustrating and stressful situation that no one wants to experience. However, there are measures you can take to protect yourself from such incidents. One important aspect is having the right insurance coverage, specifically uninsured motorist coverage, which can provide you with the necessary financial support in these unfortunate circumstances.