Low Cost Auto Quotes: How to Save on Your Next Policy

Auto insurance doesn’t have to drain your budget. At Archibald Insurance Agency, we help Utah drivers find low cost auto quotes by understanding what actually moves the needle on your rates.

The difference between paying too much and getting a fair deal often comes down to knowing which factors insurers weigh most heavily and which discounts you qualify for. This guide walks you through the concrete steps to reduce your premiums without sacrificing coverage.

What Really Drives Your Auto Insurance Rates

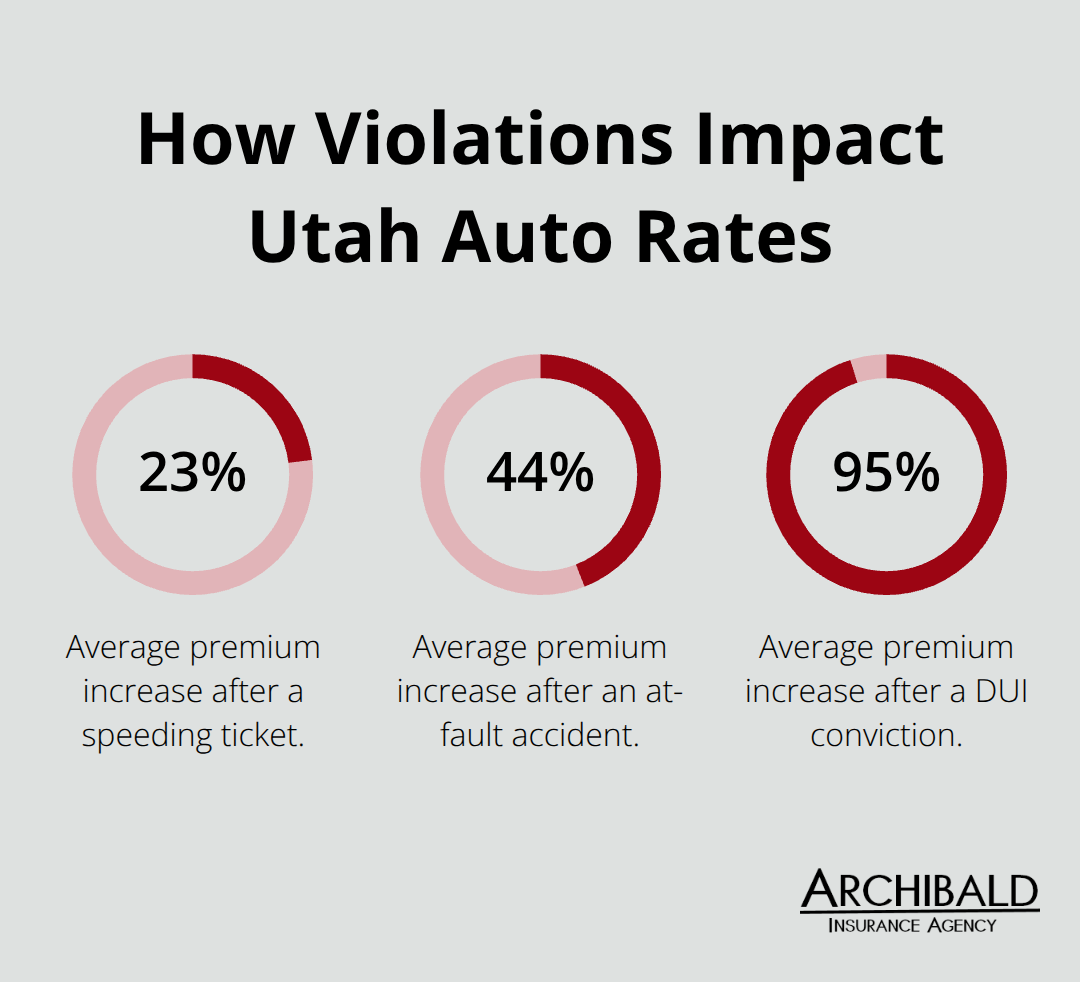

Your driving record is the single biggest factor insurers examine, and the numbers prove it. A single speeding ticket raises your rate by roughly 23%, while an at-fault accident jumps it by about 44%, according to Bankrate’s analysis. A DUI conviction nearly doubles your premium, with increases around 95% compared to a clean record.

These aren’t minor adjustments-they’re the difference between paying $1,800 and $3,500 annually for full coverage in Utah. Your past three years matter far more than most drivers realize. If you’ve had violations or accidents, your rates reflect that immediately, but the good news is that these impacts fade over time as older incidents age off your record.

Your Vehicle Influences Your Quote More Than You Think

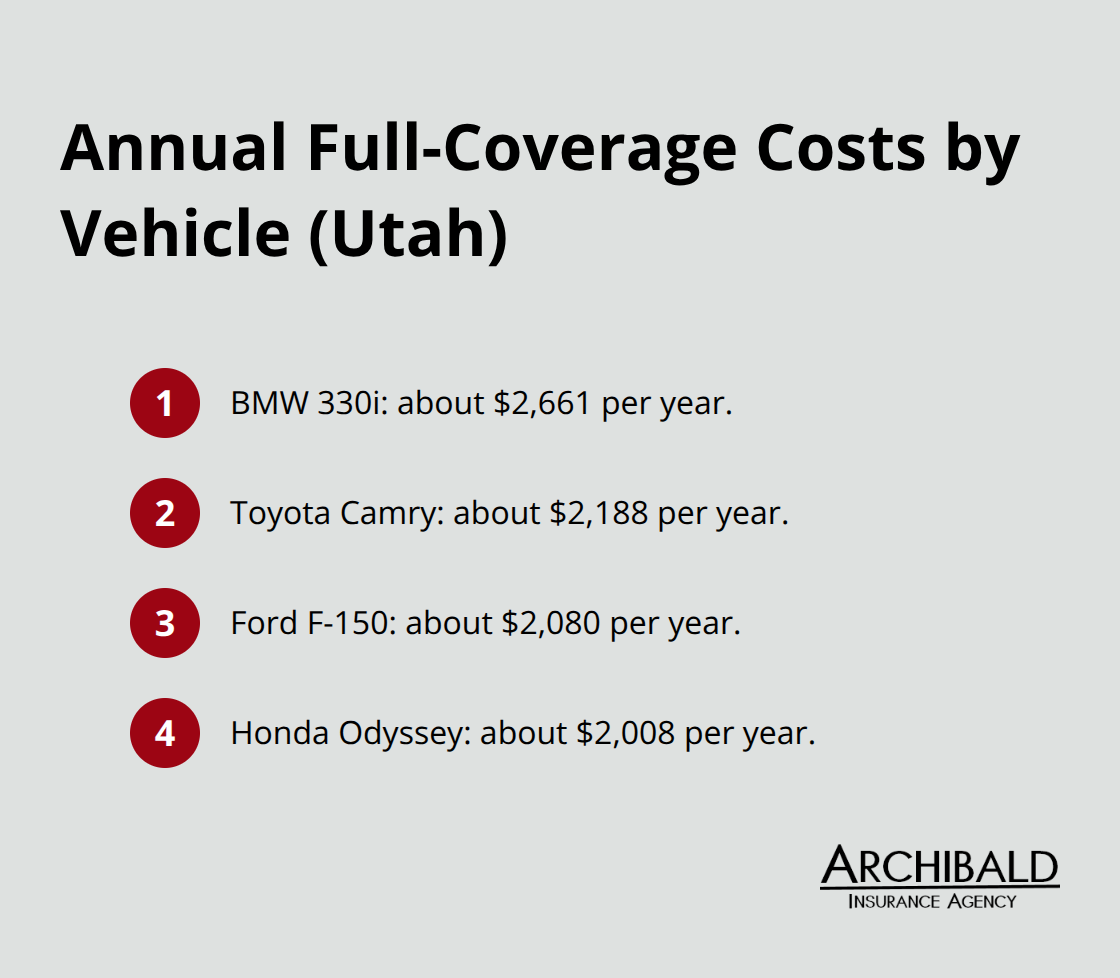

The car you drive affects your quote more than many Utah drivers expect. A BMW 330i costs roughly $2,661 per year for full coverage, while a Toyota Camry sits at $2,188, a Ford F-150 at $2,080, and a Honda Odyssey at $2,008, all according to Bankrate data. Safety features and theft deterrence reduce the likelihood of claims, which is why insurers price them differently.

Before you buy a vehicle, check the Insurance Institute for Highway Safety ratings to understand how your choice affects future premiums. Older vehicles with lower market values sometimes make collision and comprehensive coverage unnecessary-if your car is worth $3,000 but your collision premium costs $400 annually, you should consider dropping that coverage.

Where You Live Shapes Your Final Price

Your location in Utah directly impacts your quote. Salt Lake City averages around $2,375 annually for full coverage, roughly 8% above the state average, while Provo sits around $2,219, about 1% above. These differences reflect local accident rates, theft frequency, and traffic patterns in each area. Your age and credit history also shift rates significantly-poor credit can raise full-coverage premiums by up to 84% compared to the state average, while excellent credit reduces them by roughly 17%.

Age and Coverage Limits Create Real Cost Differences

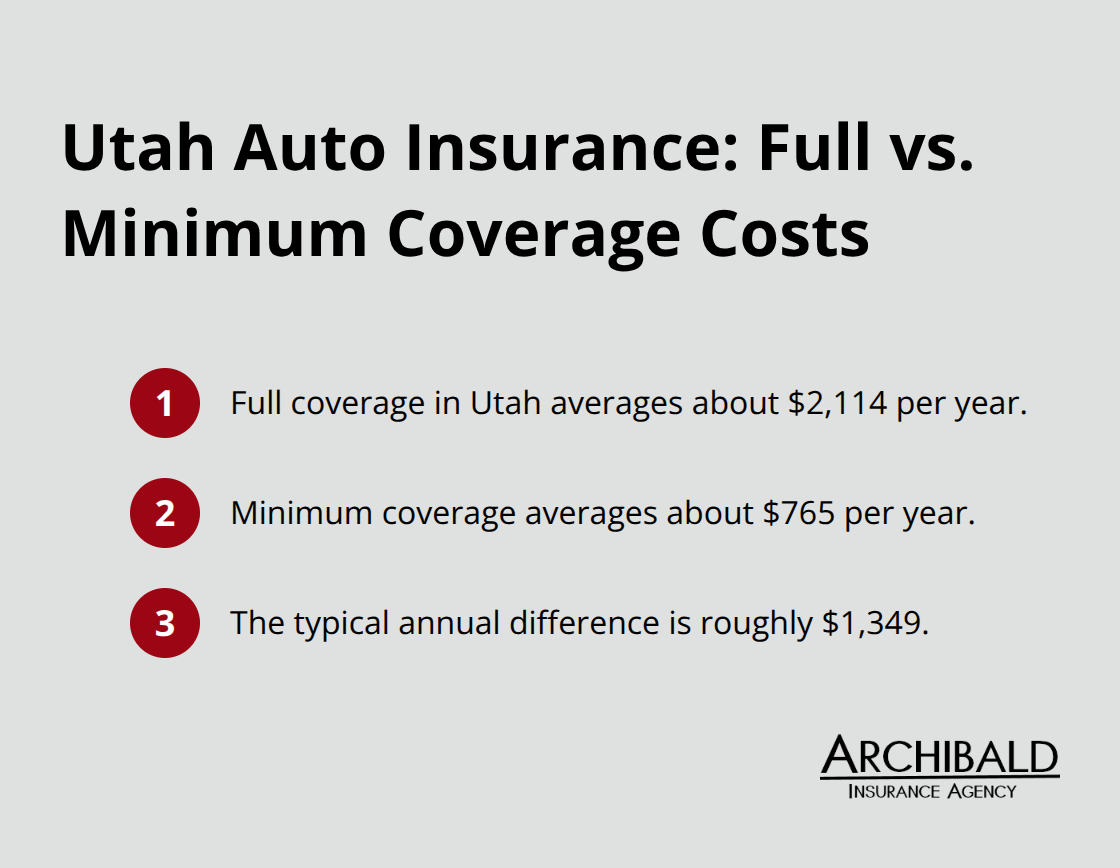

Teen drivers on a parent’s policy pay substantially less than those who buy independently; an 18-year-old on a parent’s policy costs about $4,467 annually versus $6,910 for an independent policy. Your coverage limits matter too-minimum coverage in Utah averages $831 annually, while full coverage runs about $2,188, giving you a clear choice between legal compliance and comprehensive protection. Understanding these rate drivers positions you to make smarter decisions about which factors you can control and which ones require a different approach to savings.

How to Cut Your Premiums Without Cutting Coverage

Bundle Policies to Unlock Immediate Savings

Bundling your auto policy with homeowners or renters insurance can unlock multi-policy discounts when you have an auto policy and homeowners, condo, renters, or manufactured home insurance with the same carrier. That’s real money-if you’re paying $2,188 annually for full coverage in Utah, bundling could significantly reduce your costs. Many insurers offer discounts when you stack multiple policies, so insuring your home and car with the same carrier often beats shopping them separately. Some carriers reward multiple vehicles on one policy too, which compounds your savings if your household has more than one car. The key is asking your agent explicitly about multi-policy discounts during your quote-don’t assume they’re automatically applied.

Raise Your Deductible Strategically

Increasing your deductible directly lowers your collision and comprehensive premiums. Raising your deductible from $200 to $500 typically cuts these costs by 15–30%, while jumping to $1,000 can save 40% or more. The trade-off is straightforward: you pay more out of pocket if you file a claim, so only raise your deductible if you have emergency savings to cover it. For older vehicles worth under $5,000, low-mileage discounts and safety feature discounts often matter more than collision coverage itself.

Qualify for Low-Mileage and Safety Discounts

Ask your insurer whether you qualify for low-mileage rates if you drive 7,500 miles annually or less, and disclose any anti-theft devices or Advanced Driver-Assistance Systems your vehicle has-insurers reduce premiums for cars equipped with these features because they reduce claim frequency. Utah drivers who carpool or work from home frequently qualify for mileage discounts that shave hundreds off annual premiums, yet many don’t mention their driving patterns when getting quotes. These discounts compound when combined with bundling and higher deductibles, creating a layered approach to cost reduction that protects your coverage while shrinking your bill.

How to Compare Auto Insurance Quotes Effectively

Gather Quotes from Multiple Carriers

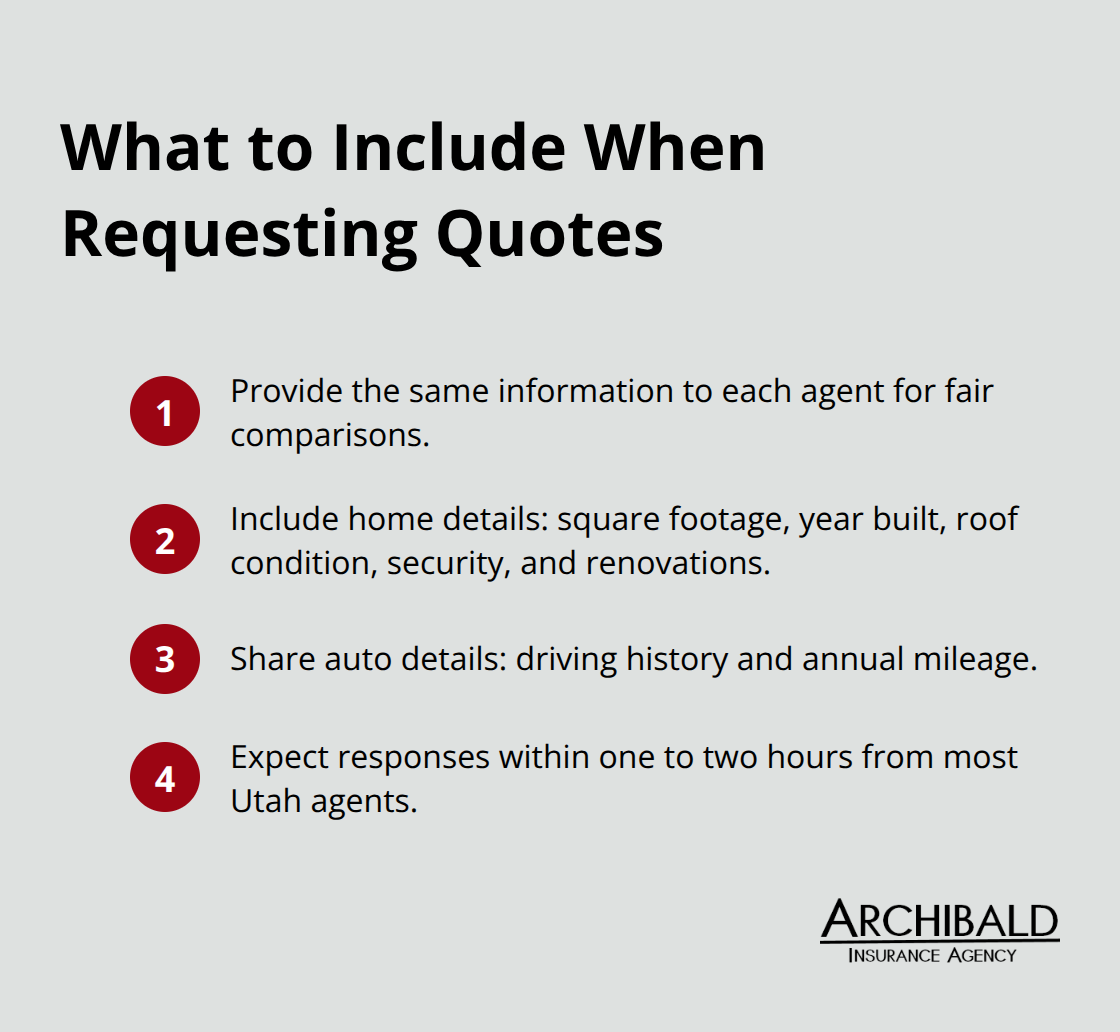

Three or more quotes from different insurers is the fastest way to find low cost coverage, yet most Utah drivers stop after one or two. Each carrier prices risk differently based on their claims data and underwriting models, which means your rate at one insurer can differ by $500 or more annually from another carrier offering identical coverage. When you shop, use the same coverage limits across all quotes so you’re genuinely comparing apples to apples-minimum liability, collision deductibles, and comprehensive limits should match exactly.

Bankrate’s analysis shows that Utah’s average full coverage costs $2,188 annually, but that figure masks real variation between carriers. An independent insurance agent can pull quotes from multiple companies at once, saving you hours of form-filling on individual insurer websites. If you prefer shopping solo, most major carriers offer online quote tools that generate estimates within minutes, though you’ll need your vehicle identification number, driving history, and current coverage details ready before you start. Online quotes are estimates that may shift slightly when you actually bind a policy, but they’re accurate enough to compare carriers fairly.

Compare Coverage Levels Side by Side

The temptation to pick the lowest quote without examining what else matters is strong, but it’s a mistake. Check your potential insurer’s financial strength rating through AM Best to confirm they can pay claims when you need them, and verify their customer service reputation by reviewing state insurance department complaint data rather than relying on online reviews alone. Some carriers advertise lower prices but deliver slower claims processing or harder claims experiences, which costs you time and stress when you file a claim.

Utah drivers benefit from asking each insurer explicitly about discounts you might qualify for-some carriers offer bundling discounts averaging around 7% when you add auto to homeowners insurance, while others lead with low-mileage or telematics program discounts. The total final premium matters more than the number of discounts advertised, so focus on the bottom-line annual cost rather than counting how many discount labels appear on your quote.

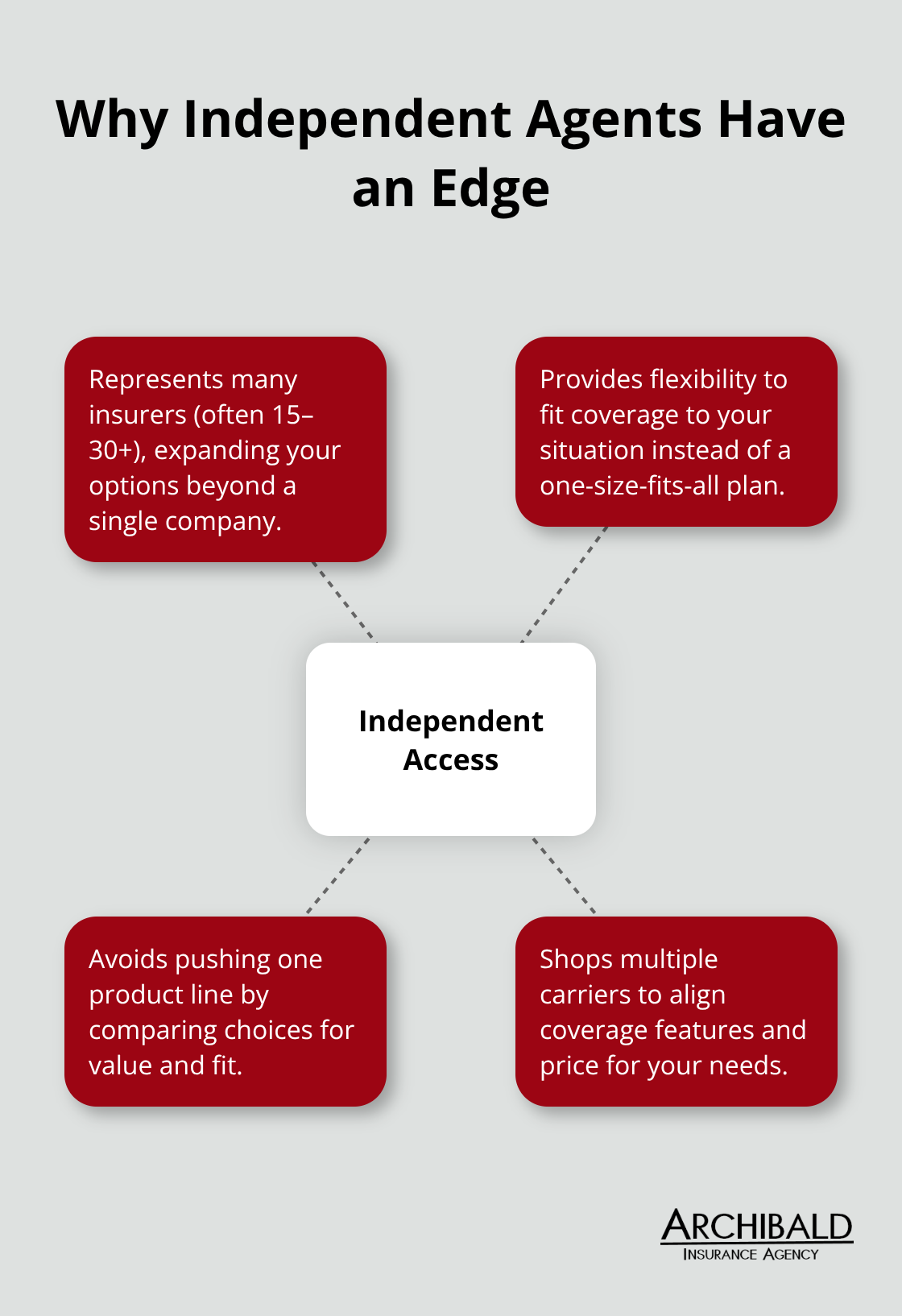

Work with an Independent Agent for Broader Options

An independent insurance agency represents numerous carriers, which means you can see options from different companies and weigh not just price but claims handling speed and customer support quality. At Archibald Insurance Agency, we represent multiple carriers and help Utah drivers find coverage that fits both their budget and their protection needs. This approach gives you access to a wider range of quotes than you’d typically find shopping individual insurer websites, and it saves you the administrative burden of contacting each company separately.

Final Thoughts

Finding low cost auto quotes in Utah requires you to understand what drives your rates, use every discount available, and compare quotes across multiple carriers. Your driving record, vehicle choice, location, and coverage limits determine your baseline cost, but bundling policies, raising deductibles strategically, and qualifying for low-mileage or safety discounts can reduce that number significantly. The difference between a $2,188 annual premium and $1,500 often hinges on whether you ask the right questions and shop thoroughly.

Shopping alone works, but it consumes time and makes it easy to miss discounts you qualify for. An independent insurance agent represents multiple carriers, which means you see options from different companies without contacting each one separately. We at Archibald Insurance Agency work with numerous insurers to help Utah drivers find coverage that fits both their budget and their protection needs, focusing on affordability paired with reliable claims support.

Contact Archibald Insurance Agency in Salt Lake City, and our team will pull quotes from multiple carriers, explain which discounts apply to your situation, and help you understand the trade-offs between different coverage levels. We build lasting relationships based on trust, which means we answer questions not just at quote time but whenever your coverage needs change. Your next policy doesn’t have to cost more than it should.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation

We often come across advertisements urging us to bundle our insurance policies together, promising savings and convenience. But what lies behind this recommendation, and is it truly a better option for your insurance needs? Let’s dive into the benefits of bundling and explore whether it’s the right choice for you.

We often come across advertisements urging us to bundle our insurance policies together, promising savings and convenience. But what lies behind this recommendation, and is it truly a better option for your insurance needs? Let’s dive into the benefits of bundling and explore whether it’s the right choice for you.