How to Get Life Insurance on a Mortgage Loan

Your mortgage is likely your biggest financial obligation. If something happens to you, life insurance on a mortgage loan protects your family from losing their home.

At Archibald Insurance Agency, we help Utah homeowners understand their options for mortgage protection. The right coverage gives your loved ones financial security when they need it most.

Why Life Insurance Matters for Your Mortgage

Your mortgage balance likely represents the single largest debt your family will ever face. According to the Federal Reserve, mortgage balances totaled $13.17 trillion at the end of December 2025, with most borrowers carrying this obligation for 15 to 30 years. If you pass away unexpectedly, your family faces a difficult choice: sell the home to cover the remaining loan balance, or struggle to make monthly payments on a reduced household income. Life insurance on a mortgage loan eliminates this pressure by providing funds specifically designed to clear the debt when you need protection most.

What Happens Without Mortgage Protection

Lenders hold a lien on your home, meaning they have a legal claim to the property if the mortgage goes unpaid. Your surviving family members cannot simply keep the home without addressing this obligation. Even if your estate has other assets, liquidating them to pay off the mortgage can take months or years through probate. Meanwhile, property taxes, homeowners insurance, and maintenance costs continue accumulating. Many families lose their homes not because they lack resources, but because they face immediate financial pressure without a clear plan. This reality makes mortgage protection a practical necessity, not an optional add-on.

Understanding Your Protection Options

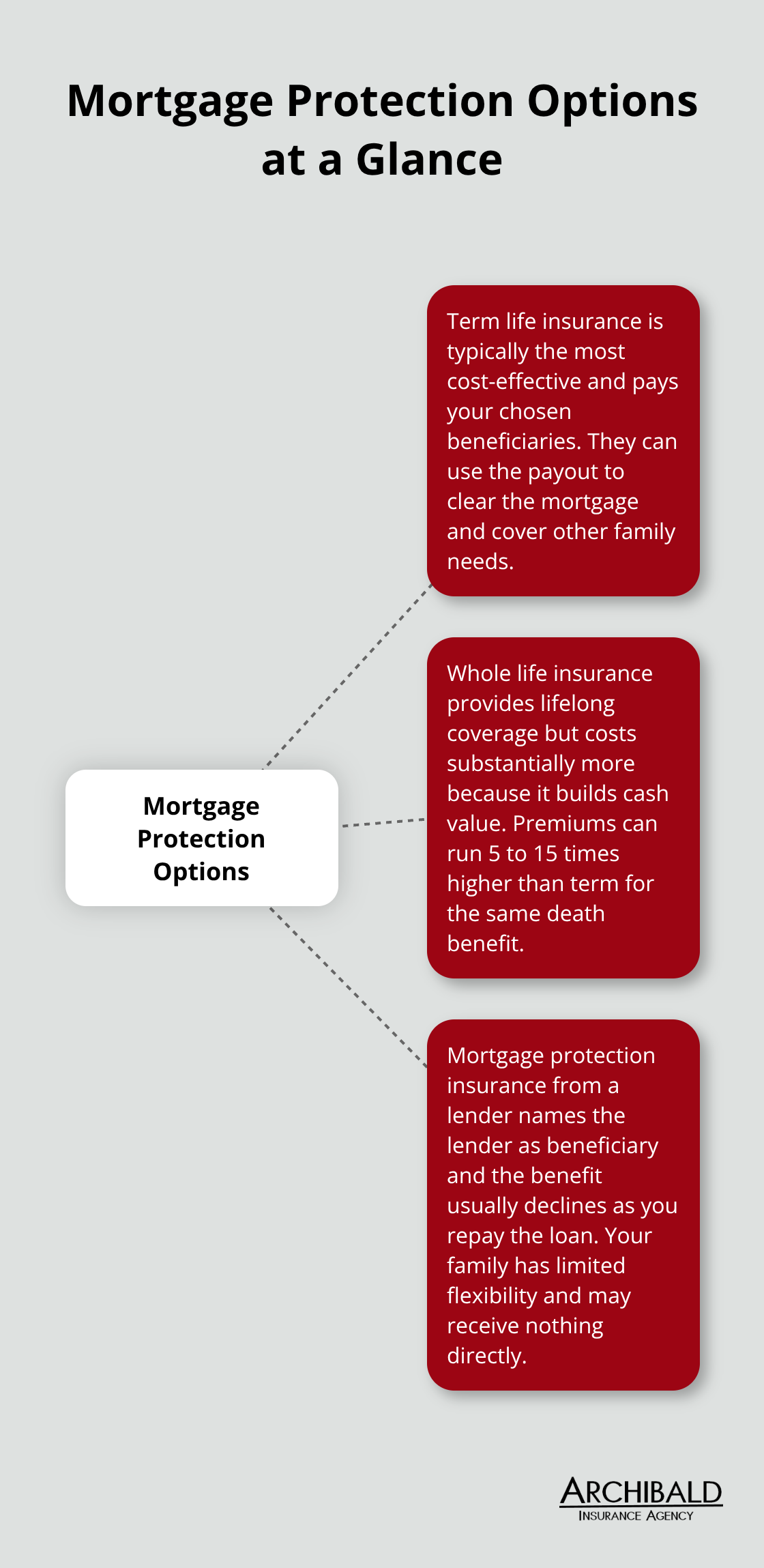

You have three primary paths to protect your mortgage: term life insurance, whole life insurance, or mortgage protection insurance from your lender. Term life insurance stands out as the most cost-effective choice for mortgage payoff.

A 40-year-old male with a $500,000 30-year mortgage pays approximately $59 to $66 monthly for mortgage protection insurance, according to Forbes Advisor data. That same individual could secure a 30-year term life policy covering $500,000 for substantially less-often in the $40 to $50 range monthly-while gaining flexibility to use the payout for any family need beyond the mortgage.

Why Flexibility Matters in Your Payout

With mortgage protection insurance, the lender receives the death benefit directly, meaning your family cannot redirect funds toward other debts, final expenses, or living costs. Term life insurance pays your named beneficiaries, who can allocate the funds strategically based on actual family needs. Your family might use the proceeds to pay off the mortgage first, then address credit card debt, medical bills, or everyday expenses. This flexibility transforms life insurance from a single-purpose product into a comprehensive financial safety net. Understanding these differences helps you select coverage that truly protects your family’s future, not just your lender’s interests.

Which Life Insurance Product Works Best for Your Mortgage

Term Life Insurance Delivers Maximum Value

Term life insurance for mortgage protection stands out as the clear winner for most homeowners protecting a mortgage. A 30-year term policy matches your loan timeline perfectly, providing level premiums and a consistent death benefit throughout the repayment period. The cost difference compounds significantly over 30 years.

Your beneficiaries receive the full payout as a lump sum they control completely. They can pay off the mortgage immediately, address credit card debt at higher interest rates, cover funeral expenses, or preserve funds for living costs while adjusting to life without your income. Term life also offers conversion options; if your health declines later, you can typically convert remaining term coverage into whole life without new underwriting, protecting your ability to maintain insurance as you age.

Whole Life Insurance Costs Too Much for Mortgage Protection

Whole life insurance serves a different purpose and carries substantially higher costs that make it inefficient for mortgage protection alone. Whole life premiums run 5 to 15 times higher than term life for equivalent death benefits because you also fund a cash value component that grows tax-deferred. A whole life policy works better when you need lifetime coverage beyond mortgage payoff or want to access cash value while living. For most homeowners focused solely on protecting their mortgage, whole life represents unnecessary expense that drains resources without proportional benefit.

Mortgage Protection Insurance from Lenders Falls Short

Mortgage protection insurance from your lender presents the worst financial outcome for most borrowers. The lender becomes the beneficiary, receiving the death benefit directly to satisfy the loan. Your family receives nothing. Mortgage protection insurance decreases as you pay down principal, yet premiums often remain level, meaning you pay full price for declining protection. If you pay off your mortgage early, the policy becomes worthless. These policies also lack flexibility for riders or customization.

The only scenario where mortgage protection insurance makes sense is if you cannot qualify for traditional coverage due to serious health conditions. Even then, comparison shopping with a broker remains essential since some insurers accept higher-risk applicants at reasonable rates. Once you understand which product fits your situation, the next step involves calculating exactly how much coverage your family actually needs.

How Much Life Insurance Do You Actually Need

Start With Your True Financial Obligations

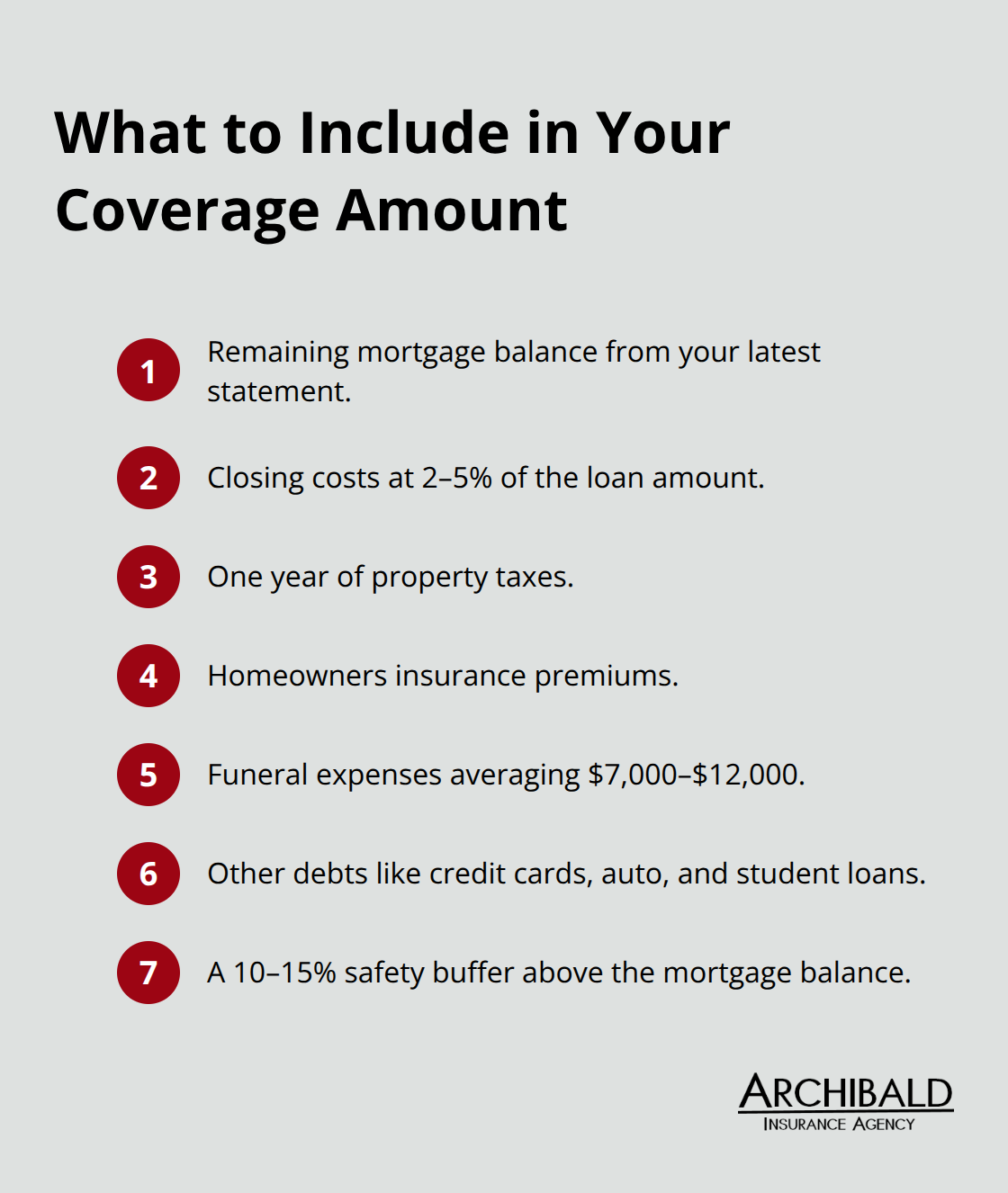

Your mortgage balance alone does not tell the complete story of what your family actually needs. Your remaining mortgage balance from your latest statement forms the foundation, but you must add closing costs (typically 2 to 5 percent of the loan amount), property taxes for one year, and homeowners insurance premiums. The National Funeral Directors Association reports that funeral expenses average $7,000 to $12,000, and your family will face these costs immediately after your death. If your family carries other debts-credit cards, auto loans, student loans-those obligations demand coverage as well.

Most homeowners underestimate their needs by focusing only on the mortgage principal without accounting for these real expenses that will arrive at the worst possible time. A practical approach involves adding 10 to 15 percent to your mortgage balance as a safety buffer for these additional costs.

Account for Inflation Over Your Loan Term

Inflation poses a serious threat to coverage adequacy over a 30-year term. A dollar in 2026 will not purchase the same goods and services in 2056. Historical inflation rates average approximately 2.5 to 3 percent annually, meaning your coverage needs grow each year. If you purchase a $500,000 policy today, that amount covers your current mortgage and expenses, but in 10 years the same $500,000 will protect significantly less real purchasing power. Try purchasing coverage at 110 to 120 percent of your current mortgage balance to account for this inflation effect, giving your family a genuine safety margin rather than a false sense of security.

Consider Your Family’s Income Replacement Needs

Your family’s income replacement needs matter equally to the mortgage payoff itself. If your spouse or co-borrower relies on your income to maintain the household, life insurance should cover not just the mortgage but also several years of living expenses. Financial professionals typically suggest coverage equal to 5 to 10 times your annual income, with the mortgage payoff representing only one component of that total need. This approach recognizes that your family faces months or years of adjustment while your spouse potentially returns to work or restructures household finances. The conversation about coverage amount ultimately requires honest assessment of your family’s actual financial vulnerabilities, not generic rules of thumb that ignore your specific circumstances.

Final Thoughts

Term life insurance delivers the coverage, affordability, and flexibility that most Utah homeowners require for protecting a mortgage loan. It costs substantially less than whole life, provides far greater payout control than mortgage protection insurance, and matches your loan timeline perfectly. Your family receives funds they can direct toward the mortgage, other debts, final expenses, or living costs based on their actual situation.

Calculating your coverage amount requires honesty about your complete financial picture-start with your mortgage balance, add closing costs and funeral expenses, account for inflation over your loan term, and consider your family’s income replacement needs. This comprehensive approach prevents the dangerous mistake of purchasing coverage that looks adequate today but falls short when your family actually needs it. The next step involves getting quotes from multiple insurers to compare rates and terms.

Contact Archibald Insurance Agency today to discuss your mortgage protection needs. We’ll help you find life insurance on a mortgage loan that genuinely protects your family’s future.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation