Affordable Life Insurance Utah: Protecting Your Family on a Budget

Life insurance is one of the smartest investments you can make for your family’s financial security. Many Utah families assume quality coverage requires spending thousands annually, but that’s simply not true.

At Archibald Insurance Agency, we help families find affordable life insurance in Utah that fits their actual budget. The right policy protects your loved ones without straining your finances.

Why Life Insurance Matters for Your Family Right Now

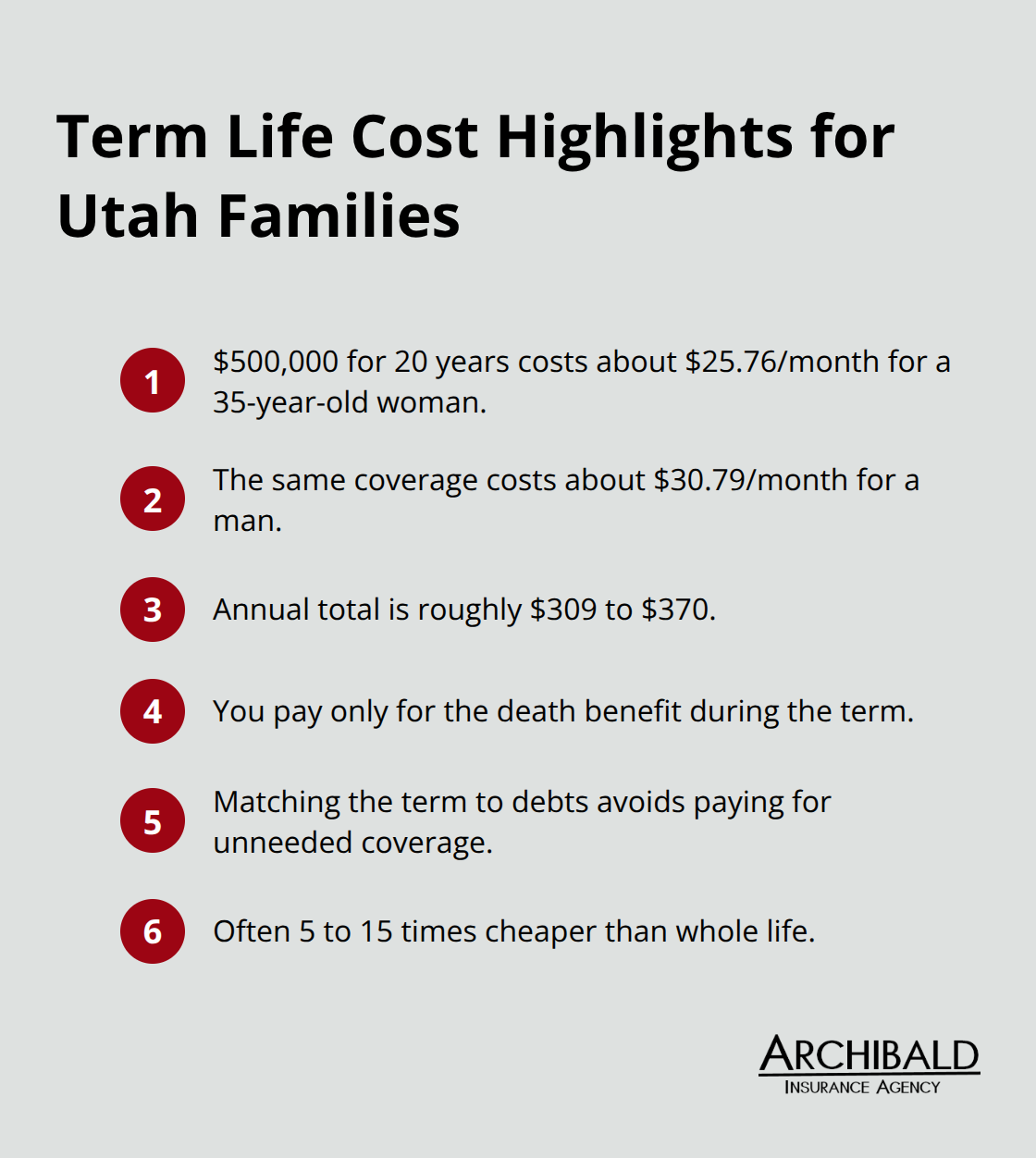

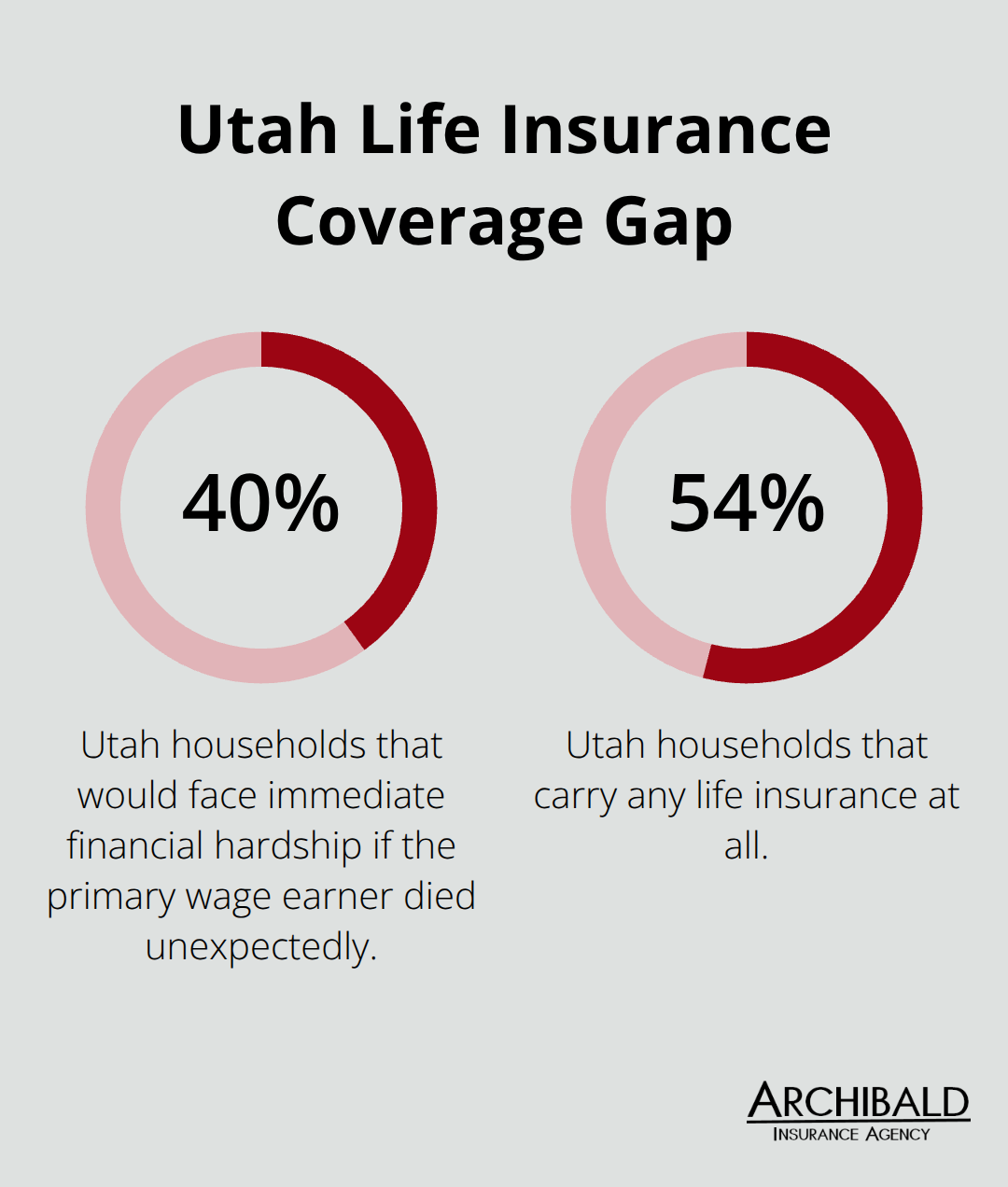

Life insurance isn’t a luxury item that only the wealthy need. It’s a financial tool that protects the people who depend on you most. When you die, your family faces immediate costs: funeral expenses averaging $7,848, plus lost income they relied on. If you carry a mortgage, car loans, or credit card debt, those obligations don’t disappear when you do-they fall to your spouse or adult children. A 20-year term policy with a $500,000 death benefit costs about $25.76 monthly for a 35-year-old Utah woman and $30.79 for a man, according to 2023 Policygenius data. That’s less than most people spend on streaming services. Without coverage, your family might need to sell the home, tap retirement savings, or struggle to pay for your children’s education. Life insurance prevents that scenario entirely.

The Real Cost of Being Uninsured

Most Utah families underestimate what happens financially when a breadwinner dies. Your mortgage doesn’t pause. Property taxes still arrive. Groceries still cost money. If your family has two children, college costs will eventually come due. A life insurance death benefit covers all of this without forcing your family into debt or selling assets.

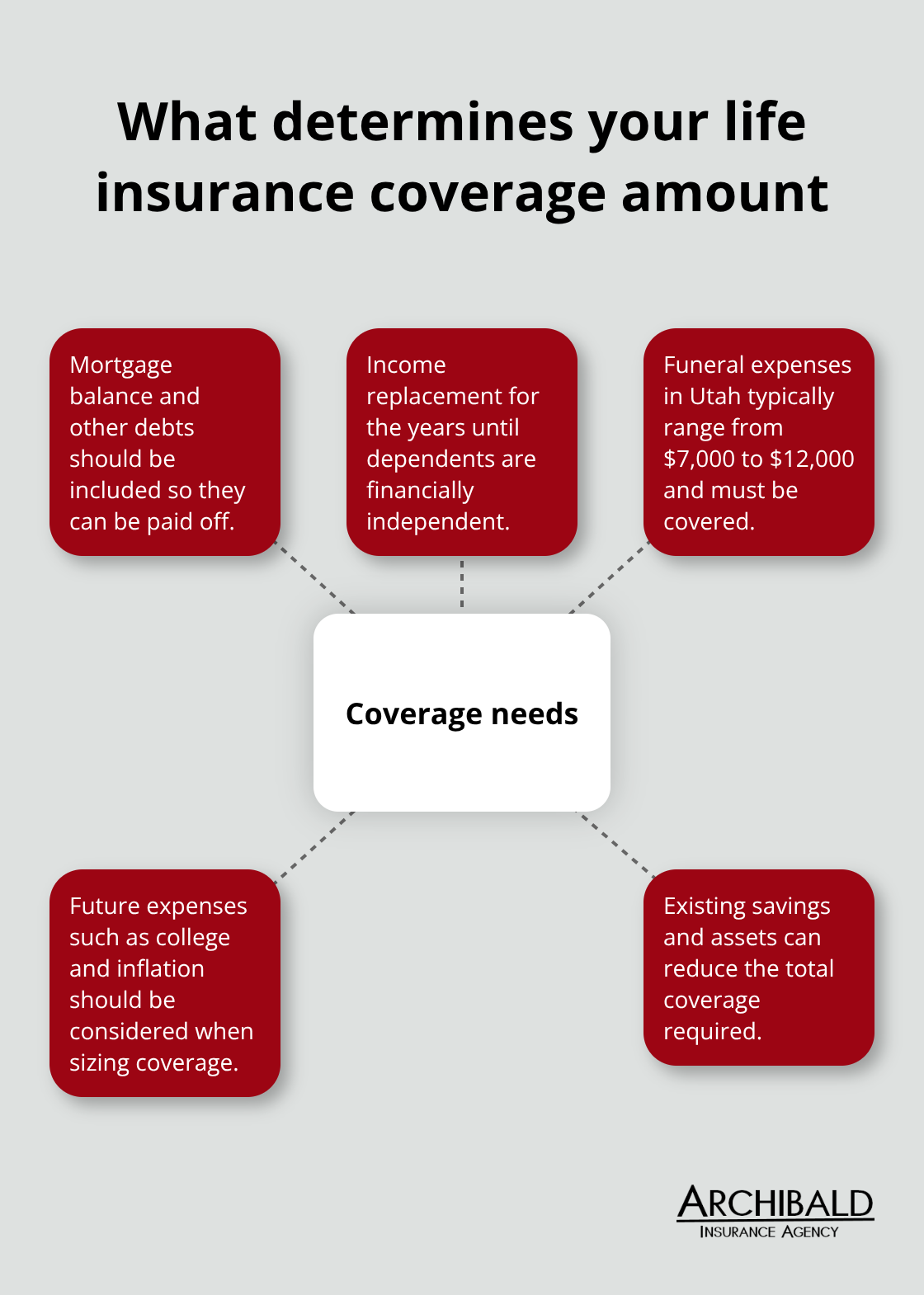

How Much Coverage You Actually Need

The math is straightforward: calculate your annual household expenses, multiply by the number of years you want covered, add outstanding debts, then add final expenses. That total is roughly what your coverage should be. Most Utah families need between $250,000 and $750,000 in protection, which term life insurance delivers affordably.

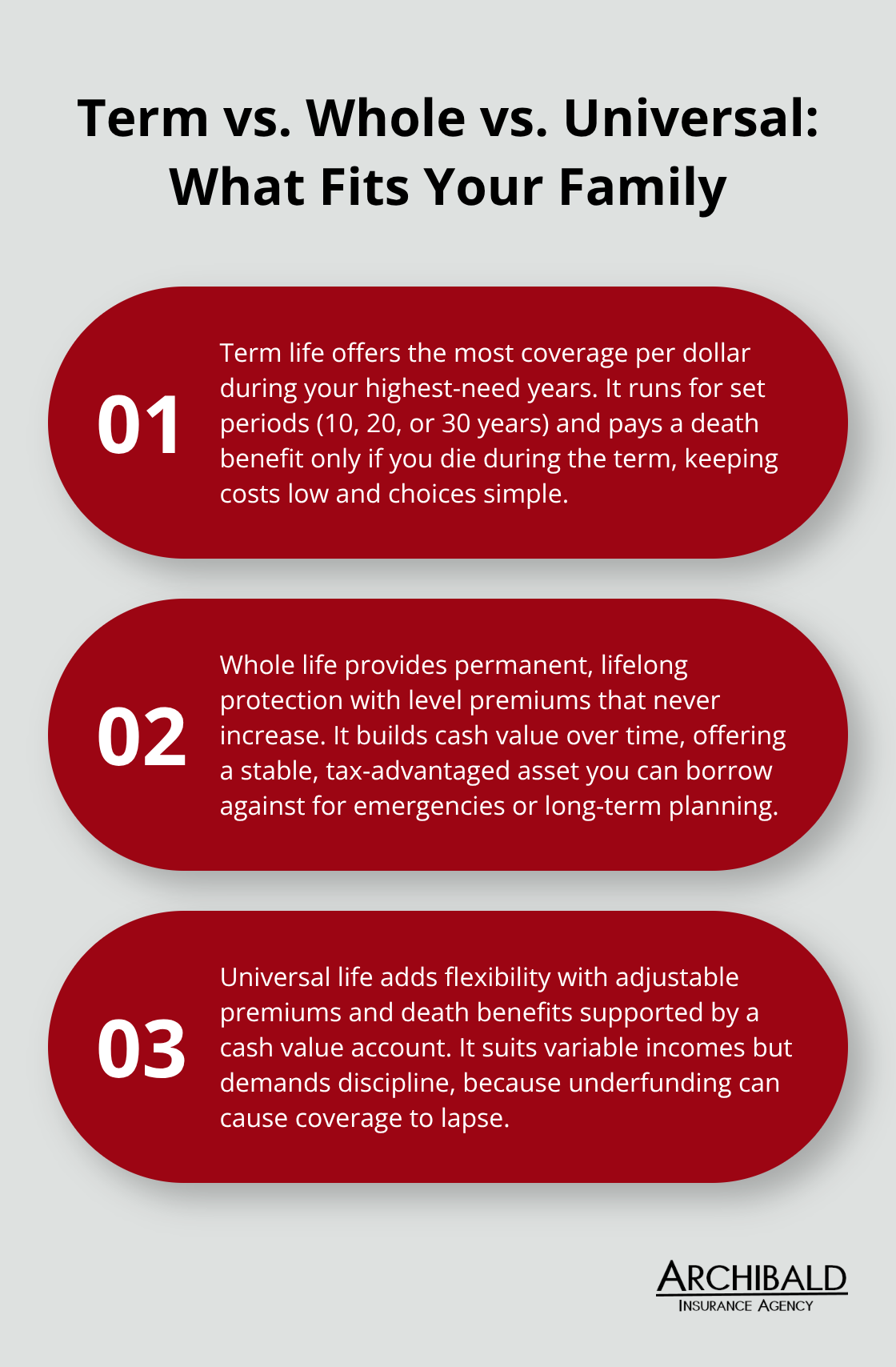

Term Life Versus Permanent Coverage

Whole life insurance costs roughly 10 times more than term but provides lifetime coverage and builds cash value. It makes sense only if you want permanent protection and have the budget for it. Term life offers the most affordable path to protect your family during your working years, when your dependents need you most. Understanding these options helps you move forward with confidence toward the coverage type that matches both your timeline and your wallet.

Types of Life Insurance and Cost Comparisons

Term Life Insurance: The Budget-Friendly Foundation

Term life insurance wins for Utah families focused on affordability. A 20-year term with $500,000 in coverage costs roughly $25.76 monthly for a 35-year-old woman and $30.79 for a man according to 2023 Policygenius data. That amounts to approximately $309 to $370 annually, which most families can absorb without sacrifice. Term life is typically 5 to 15 times cheaper than whole life, making it the practical choice when you need to protect dependents during your peak earning years. You pay only for the death benefit during your selected term, with no cash value component inflating costs. If your mortgage will be paid off in 20 years or your youngest child graduates college in 15 years, a matching term length eliminates unnecessary coverage expenses after your protection window closes. Legal & General America stands out in Utah’s market for competitive term rates across various lengths and offers no-medical-exam options that streamline the application process, backed by their A+ financial strength rating from AM Best.

Whole Life Insurance: Permanent Protection at a Premium

Whole life insurance serves a different purpose and requires a fundamentally different budget. Monthly premiums for a $1,000,000 whole life policy at age 40 run significantly higher than term options, depending on gender and health. That translates to substantial annual costs, which explains why whole life makes sense only for specific situations. You gain lifetime coverage that never expires and cash value that grows tax-deferred, allowing you to borrow against it or use it for retirement funding. MassMutual offers whole life with guaranteed cash value growth and potential dividends paid annually since 1868, though future dividends remain unguaranteed.

Universal Life: Flexibility Between Two Extremes

Universal life splits the difference between term and whole life by offering flexible premiums and lifetime coverage without whole life’s premium shock. However, it requires careful funding to prevent lapse. Pacific Life provides no-medical-exam coverage up to age 70 with death benefits reaching $3 million, useful when you’ve already exhausted term options or face health complications that make traditional underwriting difficult. This flexibility appeals to families whose financial situations shift over time, though the trade-off involves more complex policy management than term life demands.

Most Utah families should start with term life to establish baseline protection affordably. Once you’ve secured that foundation, you can explore whether permanent options align with your long-term wealth-building goals and actual cash flow capacity. The next step involves calculating exactly how much coverage your family needs and where to find the best rates.

How to Find the Right Coverage Amount and Quotes

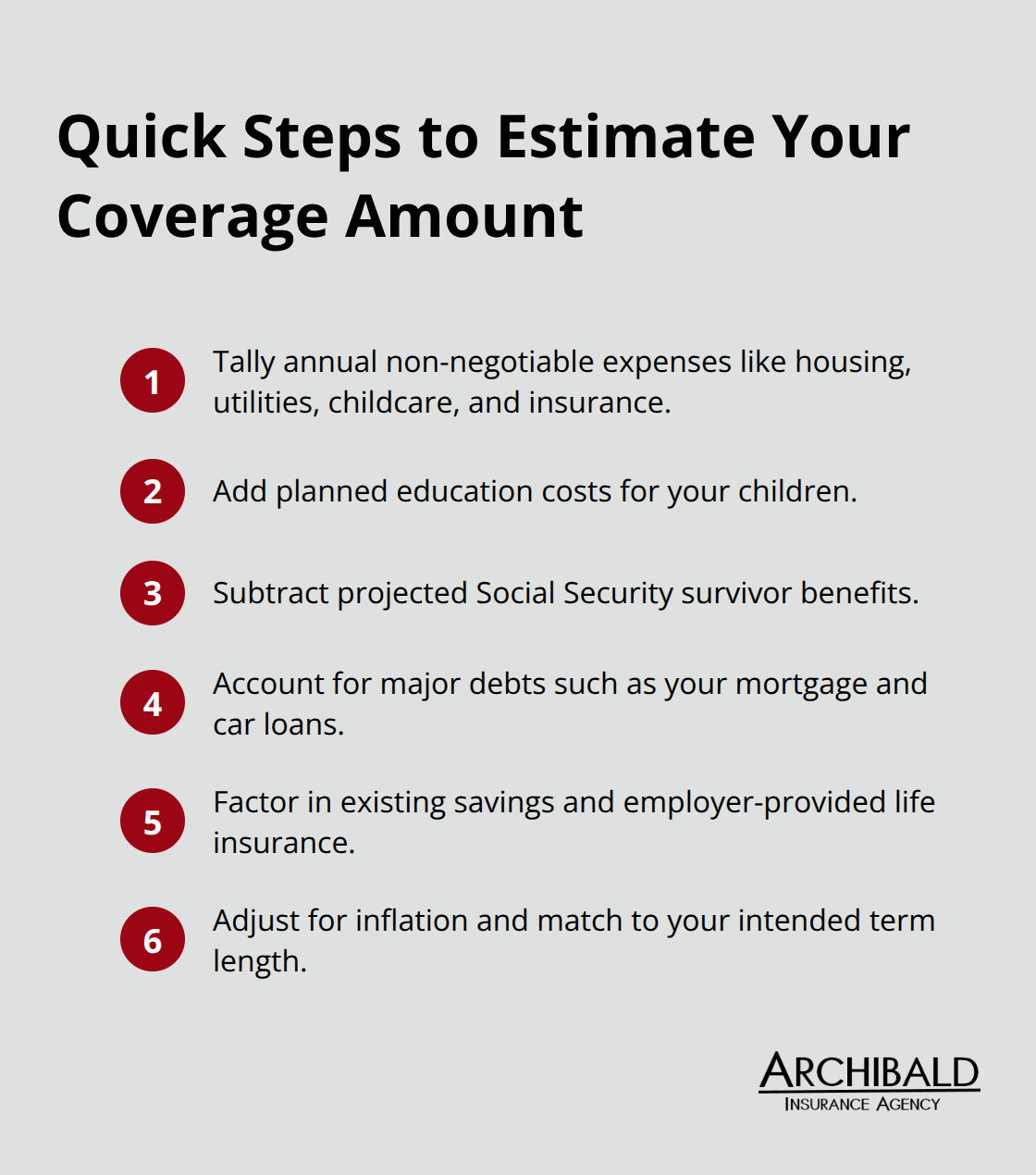

Calculate Your Actual Coverage Needs

The most common mistake Utah families make is guessing at coverage amounts instead of calculating them. One straightforward approach is to multiply your annual income by the number of years until retirement, then purchase term coverage in that amount. You can also add your annual household expenses multiplied by the years until your youngest child finishes college or your mortgage is paid off, then add outstanding debts like car loans and credit cards. Include final expenses of approximately $7,848 for funeral and burial costs. That precision eliminates both overbuying expensive permanent policies and underbuying inadequate term coverage.

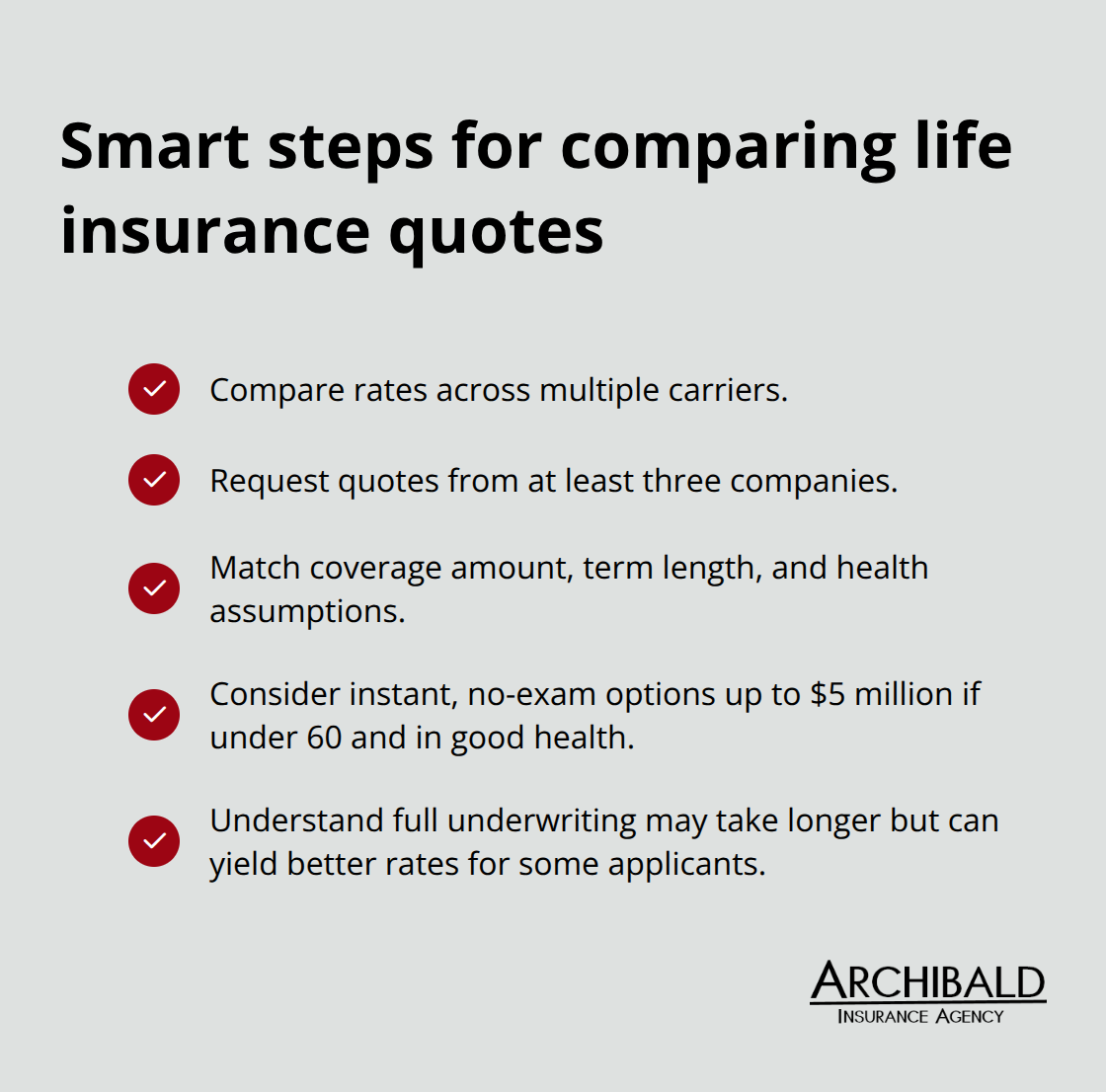

Compare Quotes from Multiple Carriers

Once you know your target amount, start collecting quotes from multiple carriers. Legal & General America, Banner Life, Pacific Life, MassMutual, Lincoln Financial, and Prudential all operate in Utah with competitive rates and strong AM Best financial ratings. A 35-year-old woman seeking $500,000 in 20-year term coverage pays approximately $25.76 monthly according to 2023 Policygenius data, while the same coverage for a man costs about $30.79 monthly. Rates fluctuate by carrier, health history, and underwriting requirements, so comparing five quotes typically reveals $10 to $30 monthly differences for identical coverage. Online tools help you collect initial quotes quickly, but guaranteed rates require medical underwriting or simplified issue processes depending on the insurer.

Account for Health Status and Lifestyle Factors

Your health status and lifestyle directly impact what you’ll pay. Smokers face substantially higher premiums across all carriers, though Legal & General America offers relatively competitive rates even for smokers and may reduce costs after one year of quitting. Lincoln Financial treats daily marijuana use more favorably than competitors who group it with tobacco, which matters for some Utah applicants. Pre-existing conditions like depression or heart issues don’t automatically disqualify you either. Lincoln Financial maintains favorable underwriting for common health complications that other insurers penalize heavily.

Lock in Rates While You’re Young

Age remains the single most powerful cost factor, so locking in rates in your 20s or 30s saves thousands over your policy lifetime compared to waiting until 40 or 50. Once you’ve narrowed carriers to three or four options, connect with a local agent who can explain policy details, confirm medical exam requirements, and address questions about conversion options or renewable terms. A local agent helps you match specific carriers and policy features to your individual budget and timeline, ensuring you understand exactly what you’re buying before committing to decades of premiums.

Final Thoughts

Affordable life insurance in Utah protects your family without straining your finances. A 20-year term with $500,000 in coverage costs roughly $25 to $31 monthly for a 35-year-old, which amounts to less than $370 annually. That protection covers your mortgage, replaces lost income, pays outstanding debts, and funds your children’s education if something happens to you.

Every year you delay locks in higher premiums due to age, and unexpected health changes can make coverage expensive or unavailable later. Locking in rates while you’re young and healthy protects your family’s financial future. Whole life and universal life options exist for families seeking permanent coverage and cash value growth, but they demand substantially higher budgets that don’t fit most Utah households.

Calculate how much coverage your family actually needs by totaling your annual expenses, outstanding debts, and final costs. Then collect quotes from multiple carriers to see which offers the best rates for your specific situation. Contact Archibald Insurance Agency to discuss your family’s protection needs and find affordable life insurance that works for your situation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation

Experiencing a home disaster is a situation nobody wants to face, but unfortunately, it can happen unexpectedly. If such a disaster were to strike, would you be able to provide a detailed list of all the valuables in your home? If your answer is uncertain or no, it’s crucial to create a comprehensive home inventory list that includes all your valuable possessions.

Experiencing a home disaster is a situation nobody wants to face, but unfortunately, it can happen unexpectedly. If such a disaster were to strike, would you be able to provide a detailed list of all the valuables in your home? If your answer is uncertain or no, it’s crucial to create a comprehensive home inventory list that includes all your valuable possessions.