Insurance Agents Salt Lake: Meet Trusted Local Advisors

Finding the right insurance coverage in Salt Lake City shouldn’t feel overwhelming. Insurance agents in Salt Lake understand your local needs better than anyone, and we at Archibald Insurance Agency believe that personal guidance makes all the difference.

Whether you’re protecting your home, your vehicle, or your business, having someone in your corner who knows Utah’s specific risks and requirements matters. That’s what local advisors bring to the table.

Why Local Agents Know Your Coverage Better

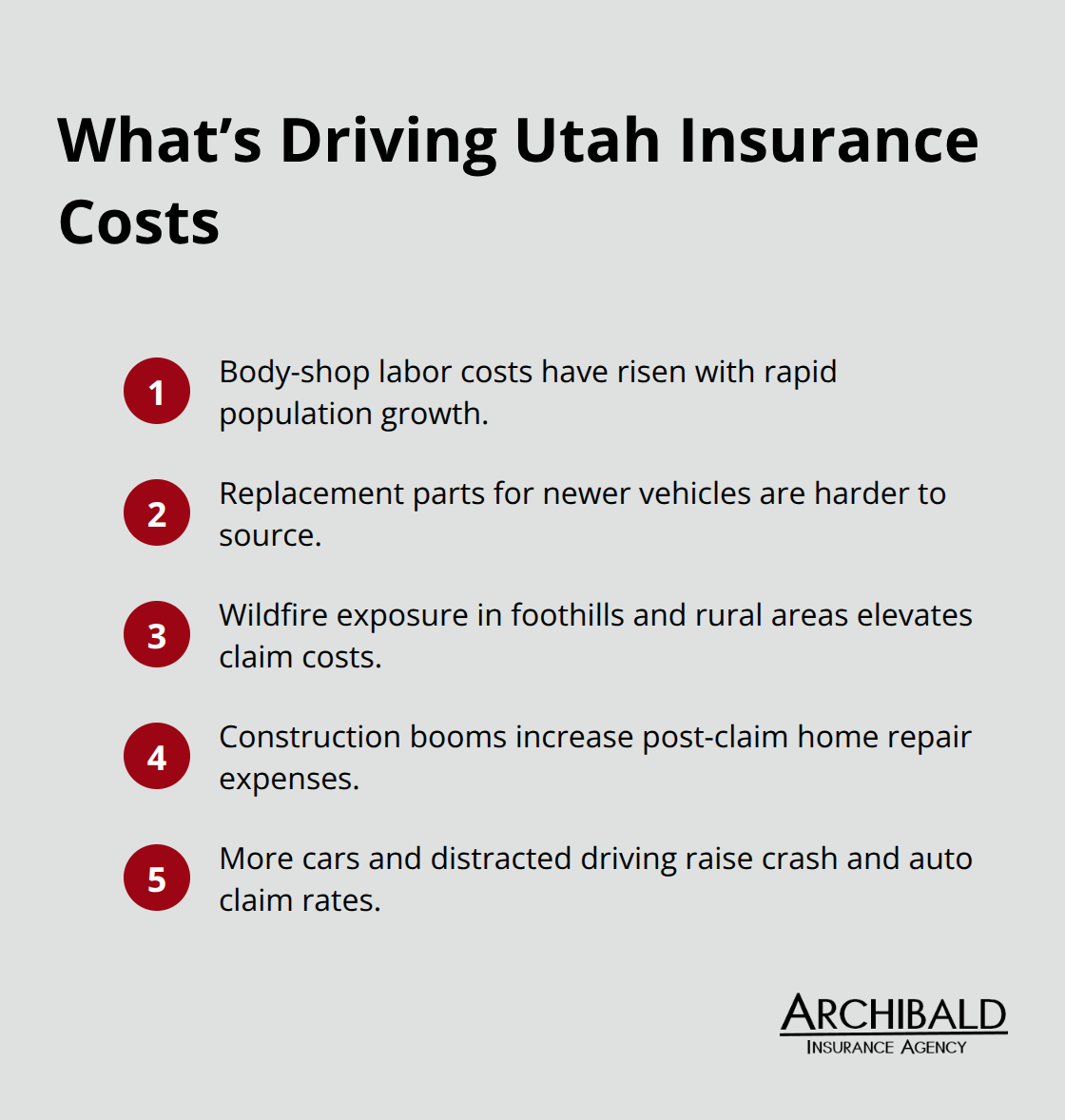

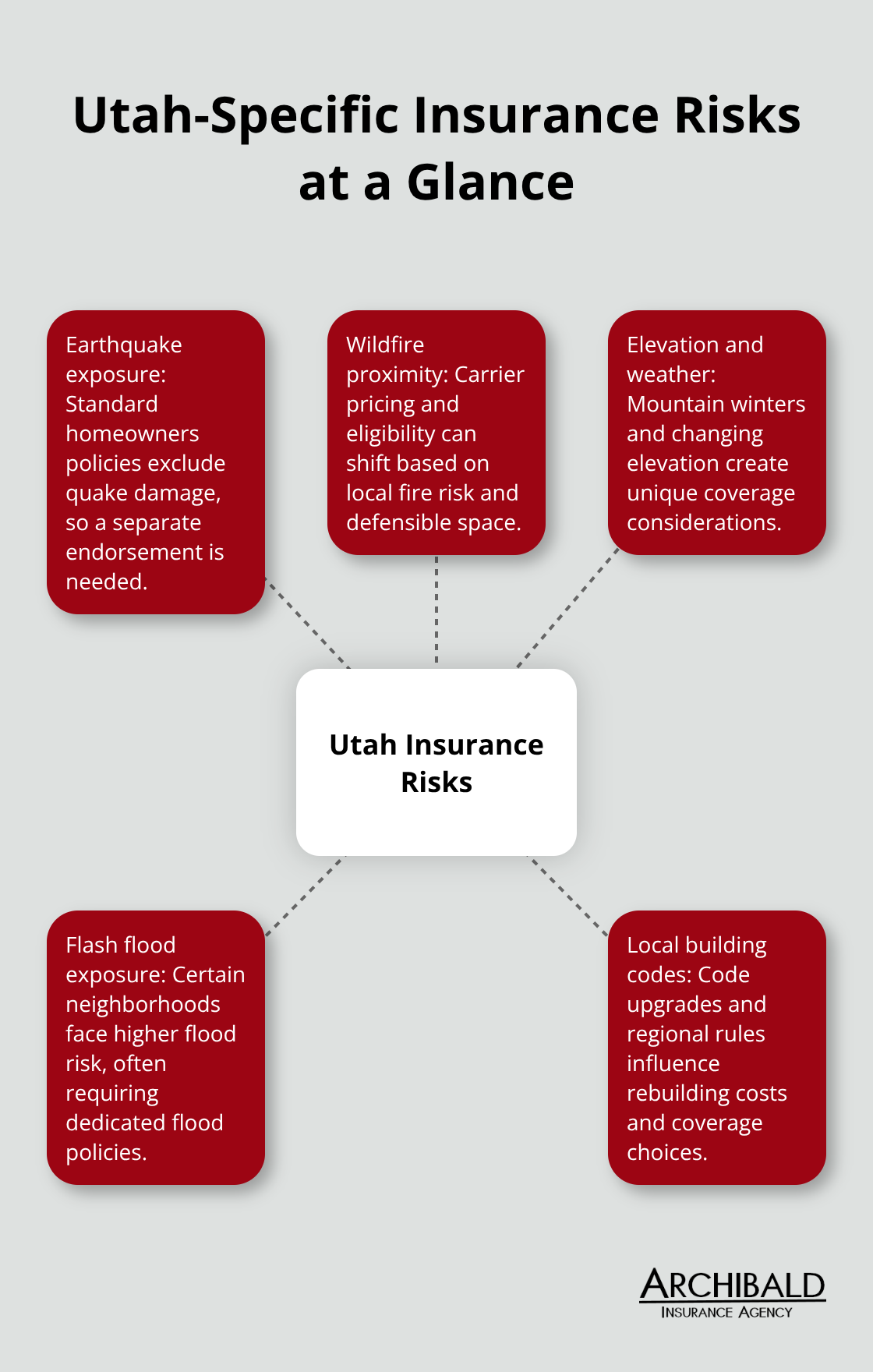

Salt Lake City insurance needs differ significantly from other parts of the country. Elevation, weather patterns, wildfire proximity, and local building codes create specific risks that generic online quotes miss entirely. When you work with a local insurance agent, you interact with someone who understands these nuances rather than a chatbot optimizing for the lowest premium. An agent in Salt Lake knows that your home sits in a region where flood and earthquake damage matter more than they do elsewhere, and they know which carriers price these appropriately for Utah properties.

They also understand that your auto insurance needs shift with seasons-winter driving conditions in the mountains demand different coverage considerations than summer commutes.

Multiple Carriers Mean Real Savings

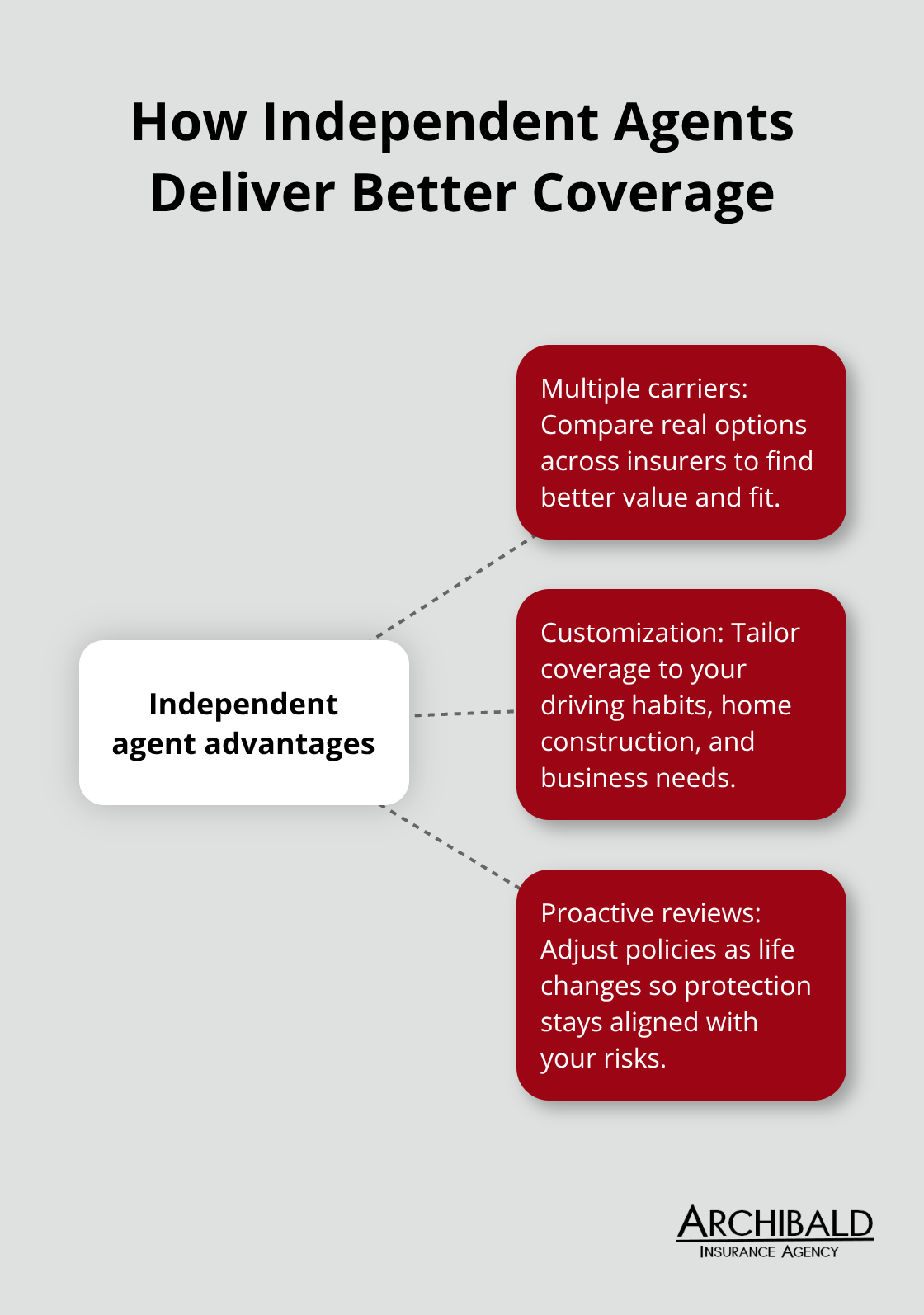

Direct insurers lock you into one company’s pricing and options. Independent agents represent numerous carriers, which gives you access to meaningfully different rates for identical coverage. The National Association of Insurance Commissioners found that homeowners insurance premiums vary dramatically between insurers, making shopping around essential to get real value. A local agent runs quotes across their carrier network in minutes, something you’d spend hours doing alone. They identify which carrier prices your specific risk profile best-not just offering the cheapest option, but the one that matches your situation. One client might receive the best rate from Carrier A for their older home, while another with a newer property qualifies for better pricing from Carrier B.

Trust Built on Repeated Interactions

A local agent becomes familiar with your life changes. When you marry, purchase a second vehicle, start a home-based business, or add a teenage driver, your agent remembers your situation and proactively reviews your coverage. This continuity prevents coverage gaps that emerge when policies sit untouched for years. You develop a relationship with someone who has accountability to your community, not a distant claims representative. This matters tremendously when you file a claim-you work with someone who knows you and your policy details rather than repeating your situation to different people on hold.

What This Means for Your Next Steps

Your coverage needs extend beyond what any single insurer offers. The right local agent connects you with options that address your specific risks, your budget, and your life circumstances. Understanding how independent agents access multiple carriers sets the stage for exploring the actual coverage types that protect Salt Lake residents most effectively.

Why Independent Agents Beat Captive Insurers

One Company, One Price, Limited Options

Direct insurers employ captive agents who sell only that company’s products. We at Archibald Insurance Agency operate differently as an independent agency representing multiple carriers, which fundamentally changes what we deliver to you. When a captive agent quotes your auto or home insurance, they optimize for their employer’s profitability, not your savings. Homeowners insurance premiums for identical coverage swing by hundreds of dollars between carriers. A captive agent never shows you those differences because they cannot. You see one quote, one price, one set of options. An independent agent runs your information across ten or fifteen carriers simultaneously, identifying which company prices your specific risk profile most competitively. That difference isn’t theoretical.

A homeowner in Salt Lake might pay $1,200 annually with one carrier and $950 with another for the same dwelling coverage and deductible. Captive agents eliminate that choice entirely.

Access to Competitive Rates Across Multiple Carriers

Independent agents show you those gaps, meaning you access rates that actually reflect your situation rather than settling for whatever one company charges. When you work with an independent agency, you gain exposure to pricing variations that captive agents cannot offer. A contractor in Salt Lake needs workers compensation coverage that reflects local wage standards and industry risk profiles specific to Utah construction. Direct insurers apply national templates that frequently miss regional nuances. Independent agents adjust coverage and pricing to match Utah’s actual business environment.

Utah-Specific Risks Require Specialized Carrier Knowledge

Utah-specific risks demand carriers who understand them. Earthquake coverage, wildfire proximity, elevation-related weather patterns, and flash flood exposure aren’t standardized across the country. Some carriers price these appropriately for Utah properties; others don’t. A captive agent selling nationwide policies applies generic pricing that often overcharges Utah residents for coverages they genuinely need or underprices protection they should carry. Independent agencies build relationships with carriers who understand Utah’s landscape and price accordingly. When you need flood insurance for a Salt Lake property or earthquake coverage for your home, an independent agent connects you with carriers experienced in these specific risks rather than forcing you into a one-size-fits-all policy.

Why Carrier Selection Matters When Claims Happen

This expertise extends beyond initial quotes. When you file a claim and discover whether your policy actually covers your situation or leaves gaps you didn’t anticipate, carrier selection becomes critical. A captive agent’s limited network means you’re stuck with whatever coverage that single company provides. An independent agent’s broader carrier relationships mean your policy was selected specifically for your risk profile and claim history, not just for the lowest premium at the time of purchase.

Understanding how independent agents access multiple carriers and Utah-specific expertise sets the stage for exploring the actual coverage types that protect Salt Lake residents most effectively.

What Coverage Do Local Agents Actually Recommend

Salt Lake residents face distinct insurance challenges that national carriers often mishandle. Auto insurance here demands consideration of mountain driving conditions, elevation-related weather shifts, and seasonal road hazards that don’t appear in standard online quote forms. Home insurance in the Salt Lake area requires understanding earthquake and flood exposure specific to your property’s location within the valley. Business insurance for Utah companies needs coverage tailored to local wage standards, industry-specific risks, and regulatory requirements that differ from other states. Life insurance decisions depend on family circumstances and income replacement needs unique to each household. Local agents recommend coverage based on actual risk exposure rather than policies that maximize commissions.

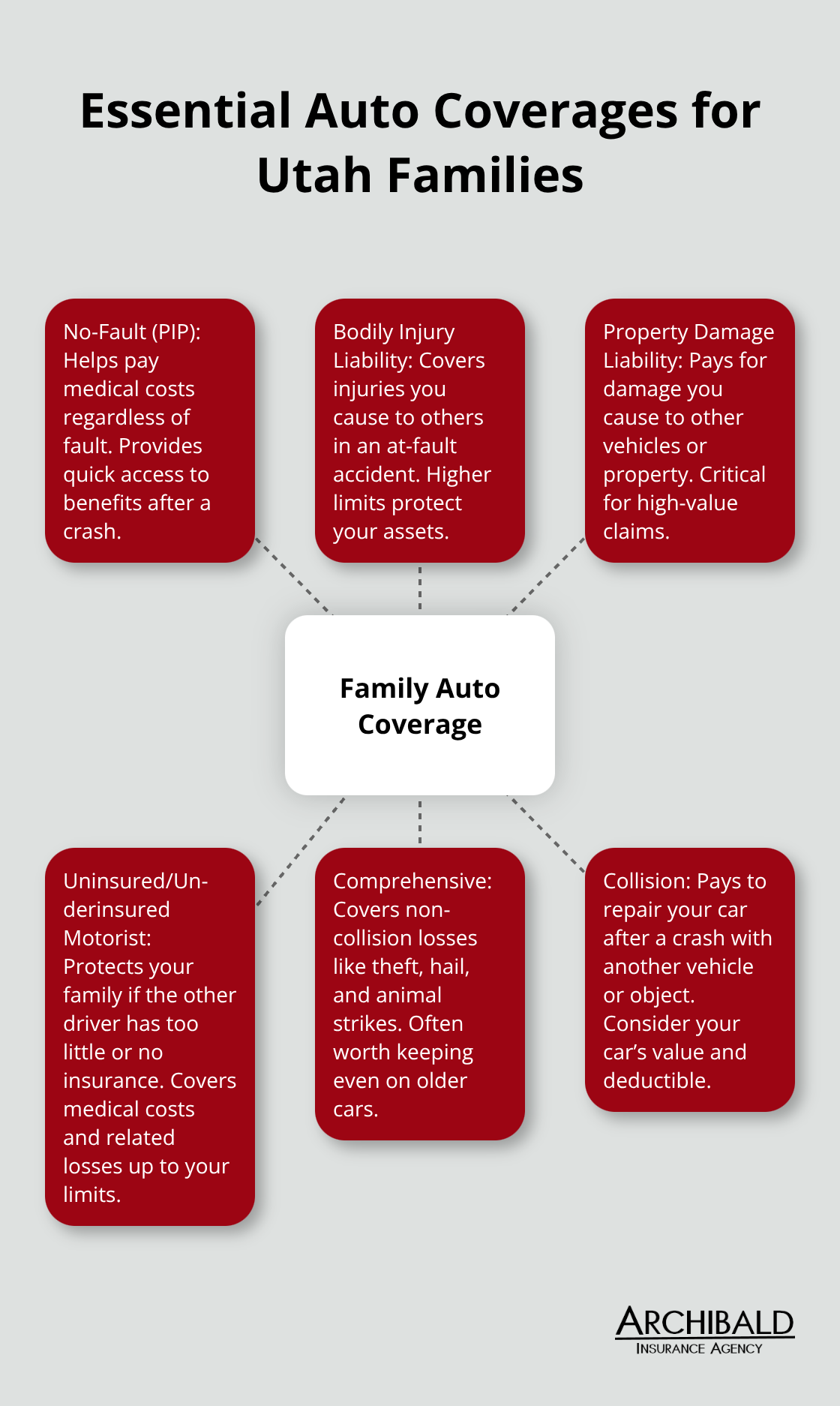

Auto Insurance for Utah Mountain Drivers

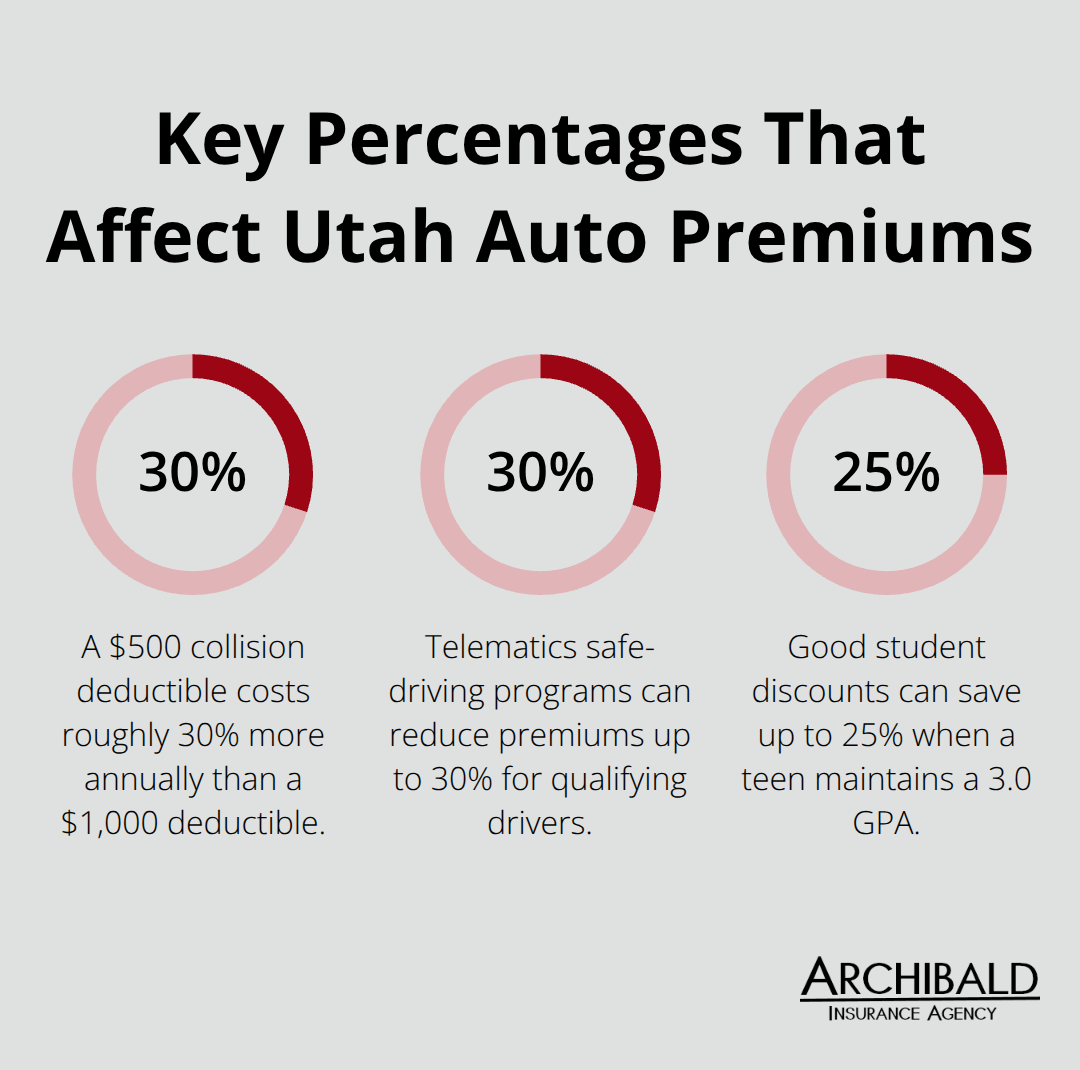

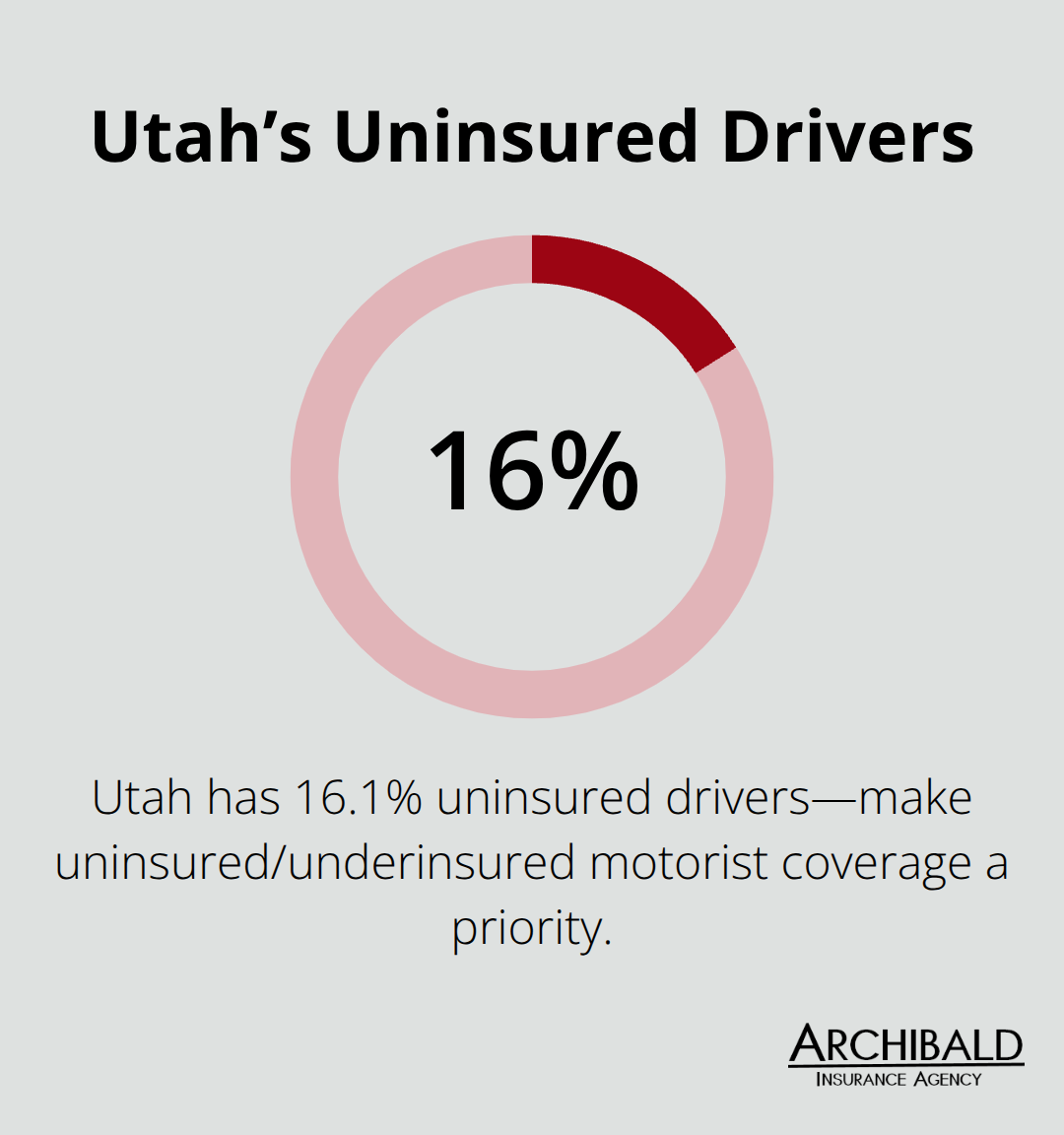

Utah drivers should prioritize collision and comprehensive coverage if financing a vehicle, since lenders require it. If your car is paid off, the calculation shifts toward your financial ability to replace it. A driver with $50,000 in savings can absorb a total loss more easily than someone with $5,000 set aside. Winter driving in Utah’s mountains justifies comprehensive coverage even for older vehicles, since weather-related damage happens frequently. Uninsured motorist coverage matters significantly in Utah since 16.1% of drivers carry no insurance. An agent in Salt Lake knows that your commute route and daily mileage affect your rates and risk profile in ways a generic quote engine cannot capture.

Home Insurance and Earthquake Protection

Home insurance for Salt Lake properties should include earthquake coverage as a separate endorsement, since standard homeowners policies exclude earthquake damage entirely. The Utah Insurance Department recommends evaluating whether your home’s location warrants flood insurance, particularly if you live near creeks, in a flood zone, or in areas prone to flash flooding. Replacement cost coverage outperforms actual cash value for most homeowners since depreciation can slash claim payments dramatically. A 15-year-old roof might be worth only $2,000 under actual cash value but cost $15,000 to replace, creating a massive gap in protection. Deductibles of $1,000 or higher reduce premiums significantly while remaining manageable for most households.

Business Insurance Tailored to Your Industry

Business insurance requirements vary dramatically by industry and company size. A contractor needs workers compensation coverage if employing anyone, plus general liability to cover third-party injuries. A home-based consulting business needs professional liability coverage to protect against claims that your advice caused financial loss. A retail shop needs property coverage for inventory and equipment plus liability for customer injuries. An agent in Salt Lake understands these distinctions and builds policies accordingly rather than applying templates designed for national averages.

Life Insurance Coverage That Matches Your Obligations

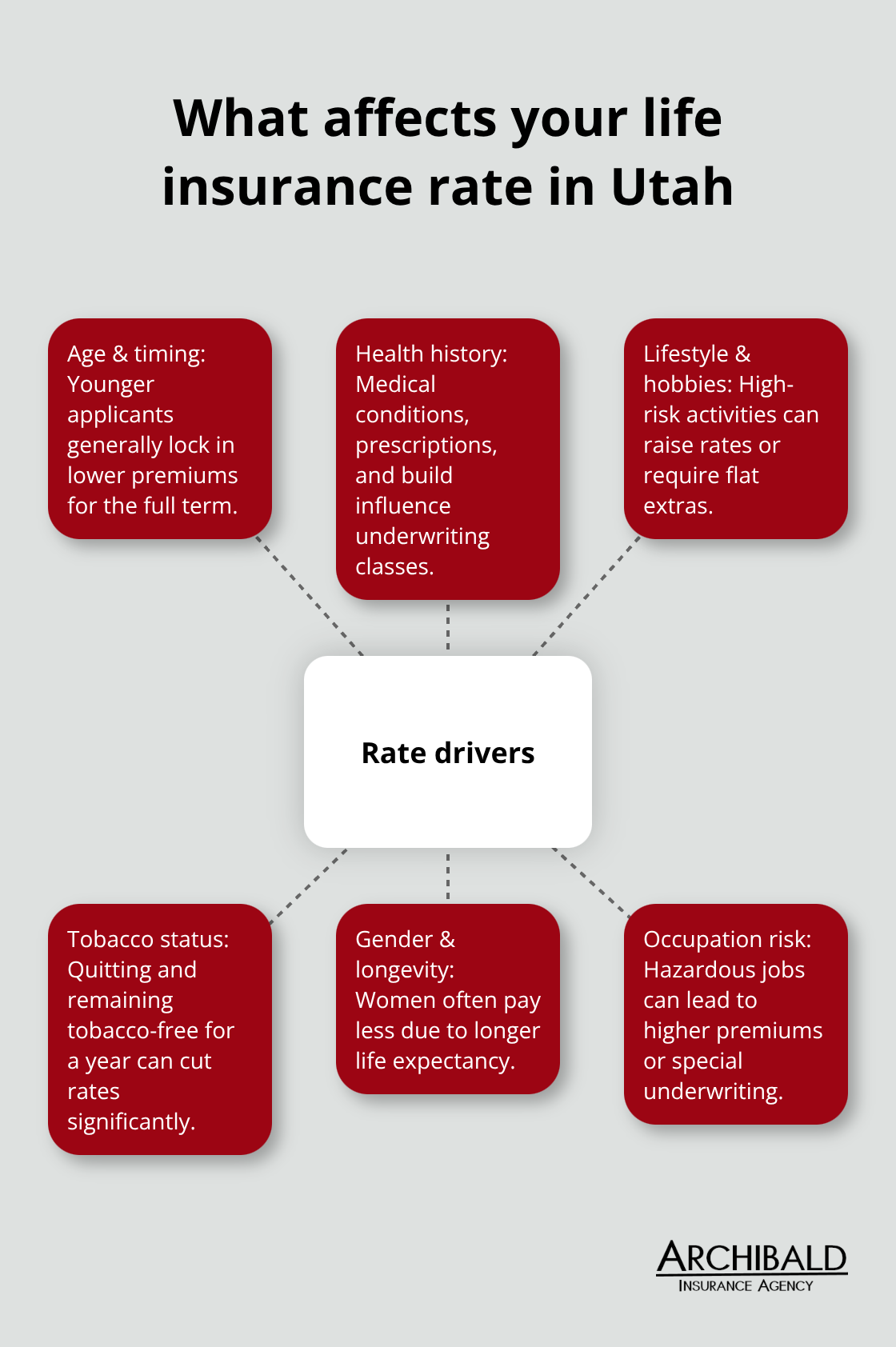

Life insurance for Utah families typically requires term coverage matching the period when dependents need income replacement. A 35-year-old with two children and a mortgage should carry 10 to 12 times annual income in coverage to protect against income loss. Once children finish college and the mortgage shrinks, that need declines. Local agents recommend coverage amounts based on your actual obligations rather than policies that cost five times more than term while building cash value you may never use.

Final Thoughts

When a pipe bursts at 2 AM and floods your basement, you need someone who answers the phone and knows your policy inside out. Insurance agents in Salt Lake understand your specific situation rather than treating you as a claim number, and they navigate the claims process with carriers they’ve worked with for years. This local support transforms insurance from paperwork into genuine protection for what matters most to you.

Salt Lake’s elevation, seasonal weather patterns, wildfire proximity, and earthquake exposure create insurance needs that differ fundamentally from other regions. An agent familiar with your neighborhood knows which carriers price flood coverage appropriately for your street and which policies address the actual hazards you face, preventing you from overpaying for irrelevant coverage or underinsuring against genuine threats. This local knowledge means your coverage evolves as your life changes-when you marry, buy a second home, hire employees, or add a teenage driver, your agent proactively adjusts coverage accordingly.

We at Archibald Insurance Agency represent multiple carriers and specialize in auto, home, business, and life insurance tailored to Salt Lake families and businesses. Our team builds lasting relationships based on understanding your specific needs rather than pushing generic policies. Contact us to discuss coverage that actually protects what matters to you.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation

As summer approaches, many of you are eagerly preparing to take your boats out on the water or perhaps even considering purchasing a new one. When it comes to insuring your boat, it’s important to prioritize having the right coverage rather than simply opting for the least expensive policy. While boating season offers incredible fun and excitement, being on the water also comes with certain risks. As you shop for boat insurance, make sure your policy includes three specific coverages, which are sometimes optional but highly recommended:

As summer approaches, many of you are eagerly preparing to take your boats out on the water or perhaps even considering purchasing a new one. When it comes to insuring your boat, it’s important to prioritize having the right coverage rather than simply opting for the least expensive policy. While boating season offers incredible fun and excitement, being on the water also comes with certain risks. As you shop for boat insurance, make sure your policy includes three specific coverages, which are sometimes optional but highly recommended: