Life insurance doesn’t have to mean sitting through medical tests and waiting weeks for results. No medical test life insurance offers a faster path to coverage, making it an attractive option for many Utah residents who want protection without the hassle.

At Archibald Insurance Agency, we help clients understand whether a no-exam policy fits their needs. This guide walks you through how these policies work, who qualifies, and how they compare to traditional coverage.

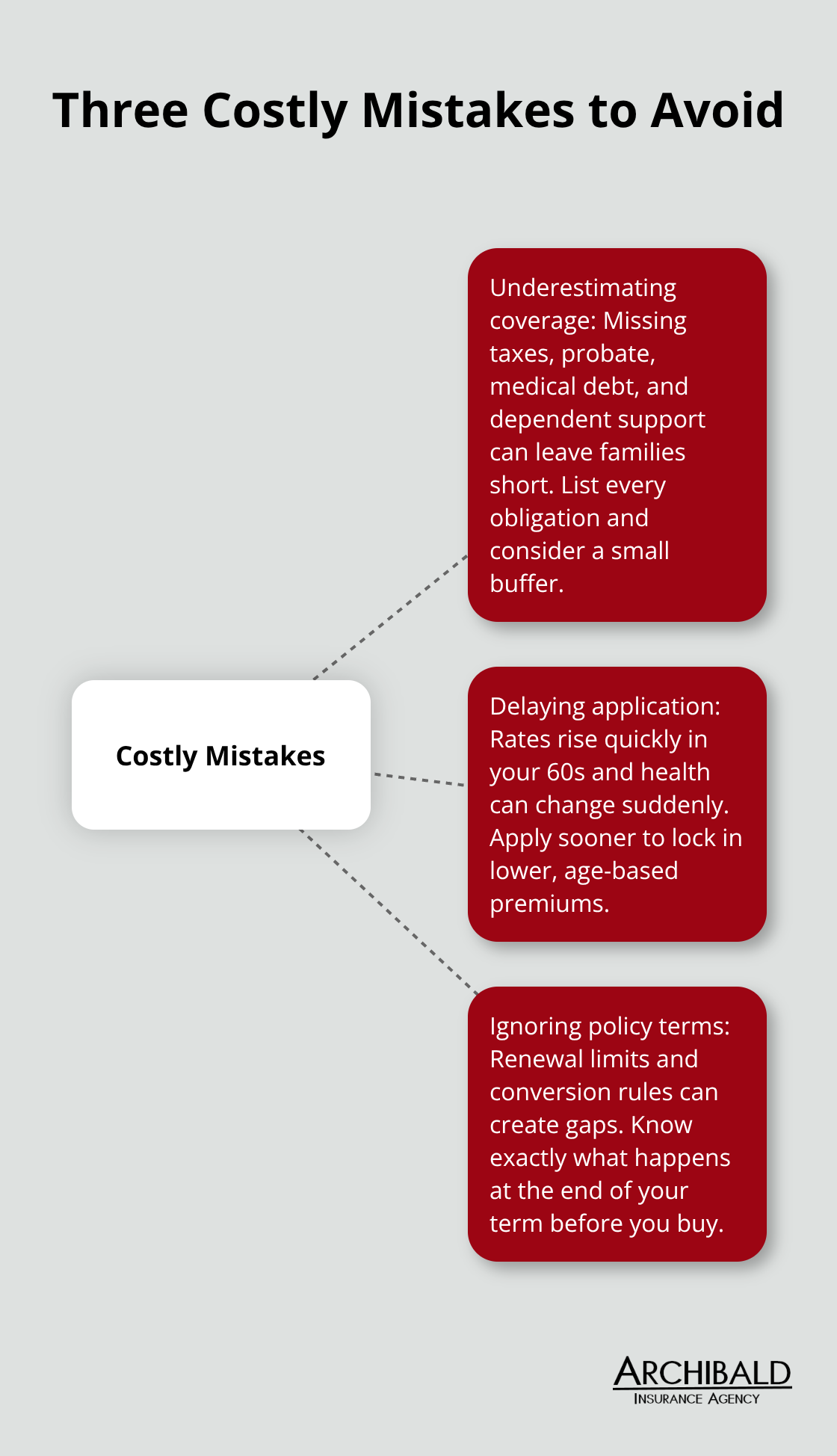

How No-Exam Life Insurance Actually Works

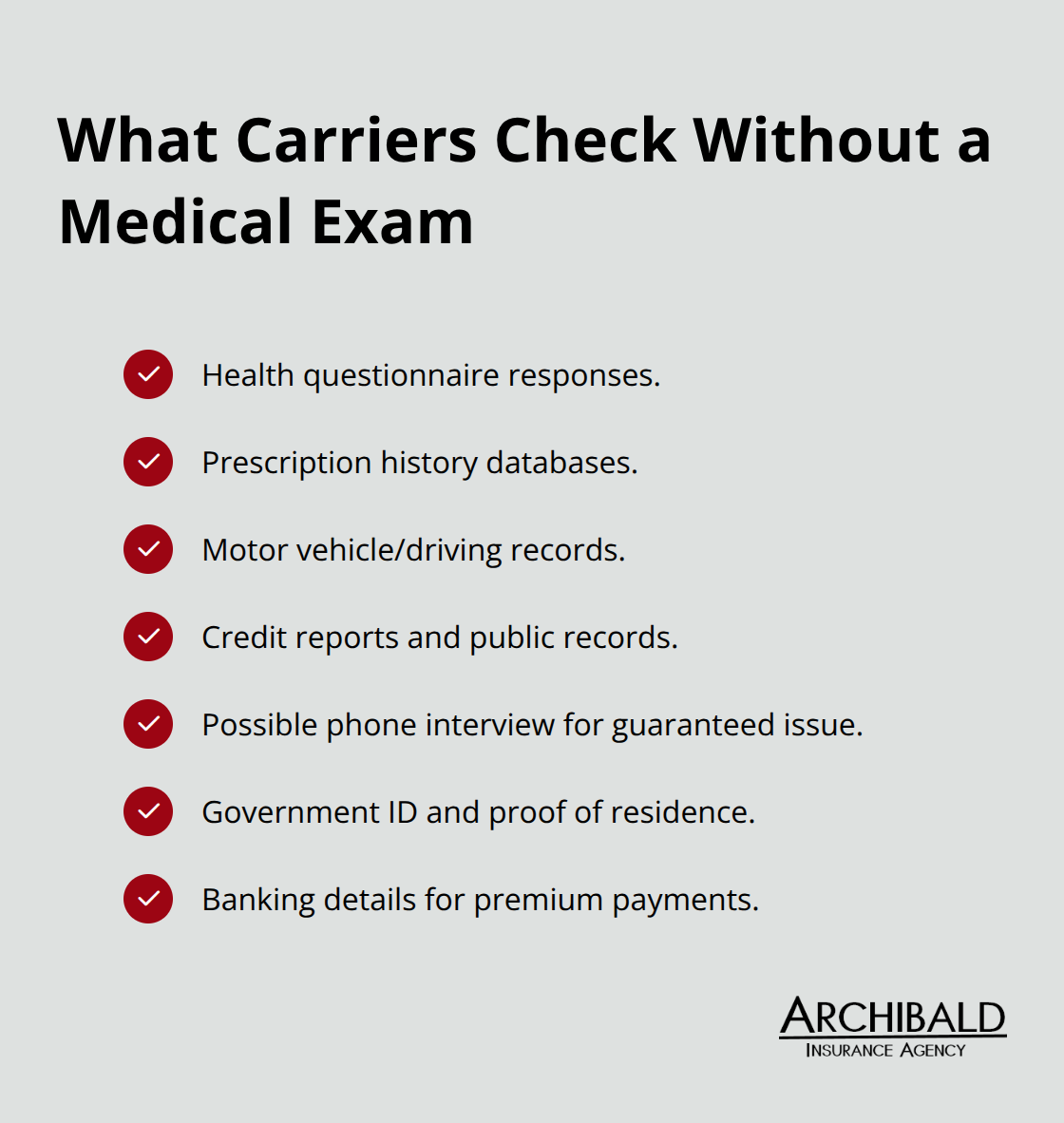

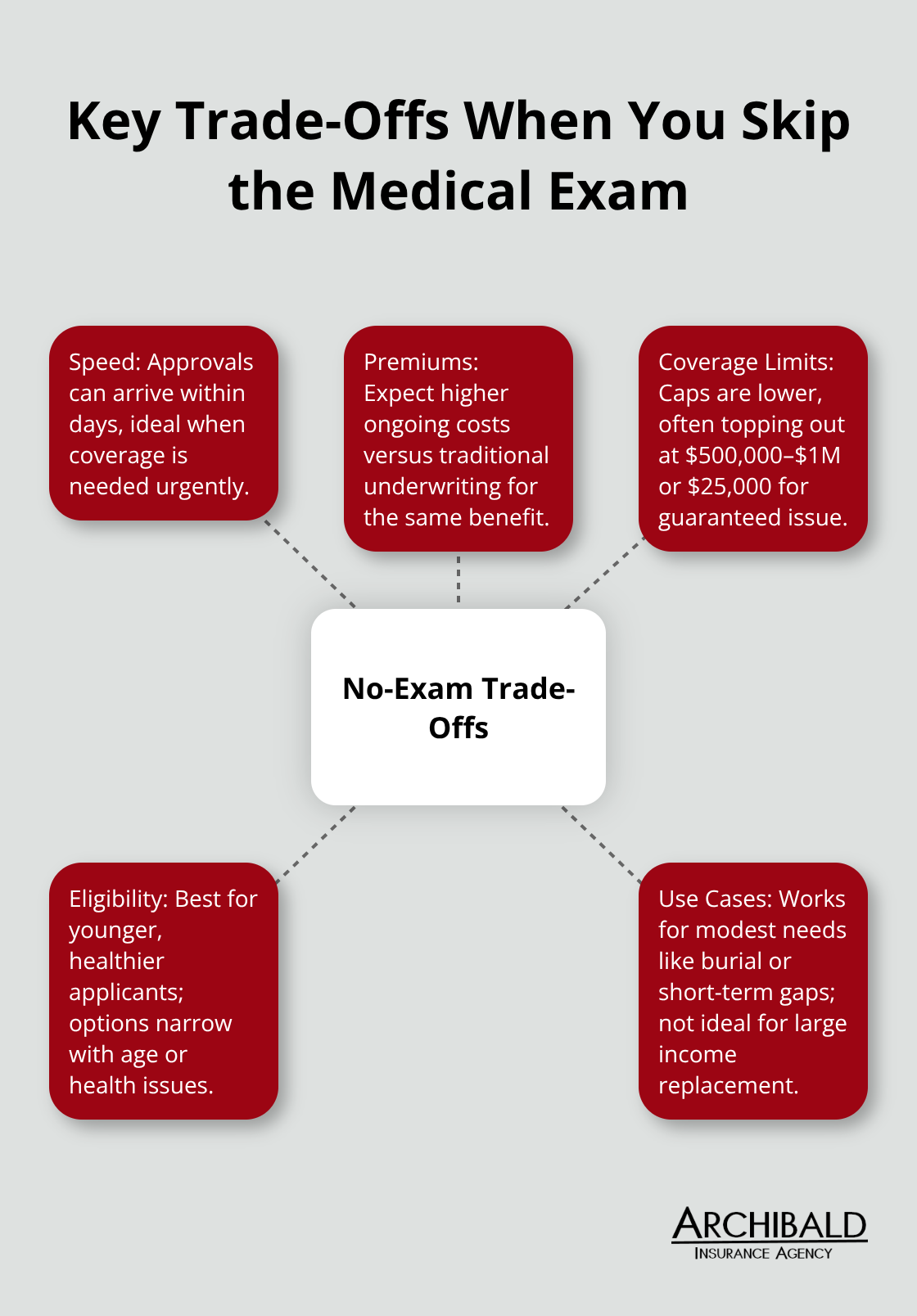

No-exam life insurance skips the medical exam, but it doesn’t skip underwriting entirely. Instead of sending you to a lab for blood work and tests, insurers use accelerated underwriting to assess your risk. They pull data from prescription records, medical histories, and past insurance applications to make a quick decision. This speed matters when you need coverage fast, whether you’re protecting a new mortgage or addressing a gap in your family’s finances. The trade-off is real though: no-exam policies typically cost more than fully underwritten term life because insurers accept higher risk without direct medical evidence. For a healthy 35-year-old in Utah seeking $250,000 in coverage, traditional underwriting might cost $25 to $35 per month, while a no-exam option could run $40 to $60 monthly.

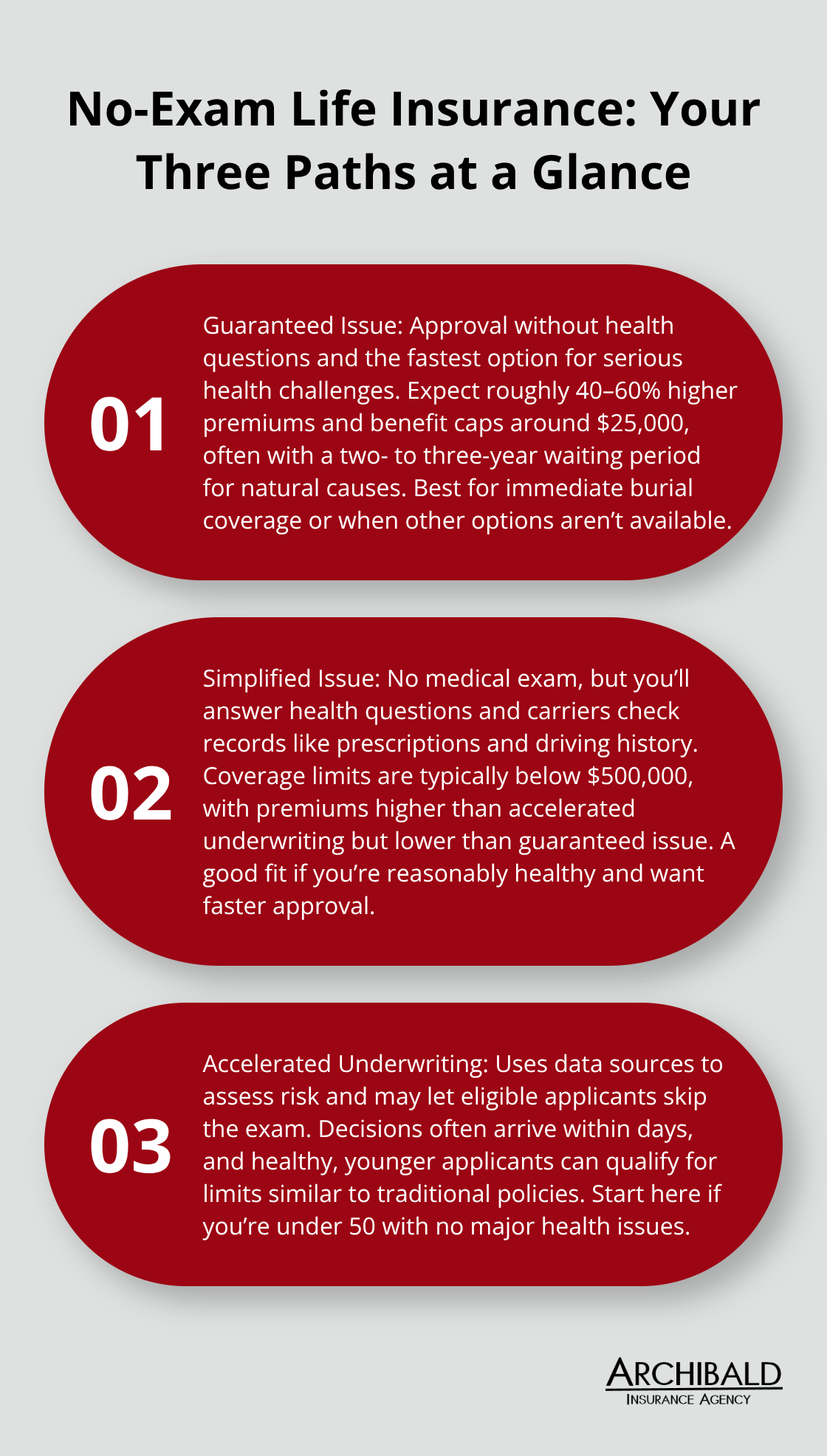

Three Types of No-Exam Policies

Accelerated underwriting policies offer the best value among no-exam options. These use algorithms and third-party data to approve coverage up to $1.5 million for qualified applicants, typically those under 55 with no major red flags in their records. Simplified issue policies ask fewer health questions than traditional underwriting but still require some basic health information. They cost more than accelerated underwriting but less than guaranteed issue, with coverage usually capped around $500,000. Guaranteed issue policies require zero health questions and guarantee acceptance regardless of health status, but premiums are steep and death benefits are minimal. This option exists mainly for final expense coverage, not income replacement. If you’re under 50 with decent health, accelerated underwriting delivers the best combination of speed and affordability. If you have health conditions or need coverage in days, simplified or guaranteed issue makes sense despite higher costs.

Speed Advantage for Utah Applicants

Traditional life insurance takes 4 to 8 weeks in Utah because insurers order exams, verify medical records, and conduct thorough underwriting. No-exam policies compress this dramatically. Accelerated underwriting can issue a policy in 24 to 72 hours once you submit your application. Simplified issue typically takes 5 to 10 business days. Guaranteed issue offers instant coverage with just a quote and application. The speed advantage matters most when you’re facing a health change or need protection quickly, but don’t assume no-exam means no waiting. Even accelerated underwriting policies require your approval before coverage activates, and some carriers still pull prescription records that take a few days to retrieve.

Age and Eligibility Restrictions

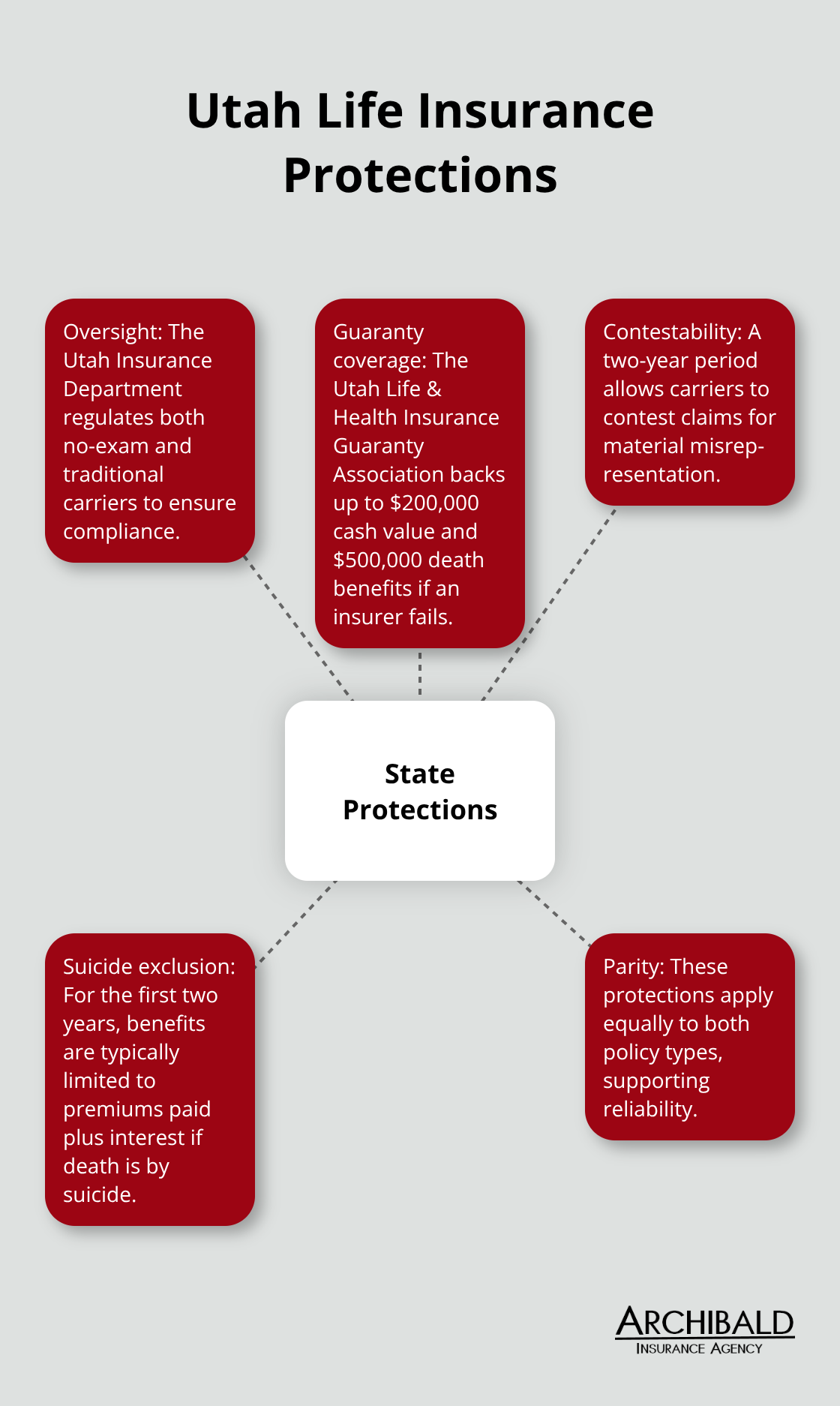

Age affects eligibility significantly. Applicants under 45 qualify for accelerated underwriting more easily, while those over 55 may find only simplified or guaranteed issue options available without a medical exam. Utah’s regulatory environment supports this faster process through streamlined approval timelines, though the Utah Insurance Department still requires carriers to maintain underwriting standards. Your age determines not just whether you qualify for no-exam coverage, but also which type of policy makes financial sense for your situation. Younger applicants should explore accelerated underwriting first, while older applicants need to understand that guaranteed issue, though expensive, may be their only rapid option.

Who Actually Qualifies for No-Exam Coverage

Age Determines Your Access to No-Exam Policies

Your age acts as the primary gatekeeper for no-exam life insurance eligibility. Applicants under 45 qualify easily for accelerated underwriting policies, which can be approved in just a few days or weeks. Those between 45 and 55 still access accelerated underwriting but face tighter scrutiny and potentially higher premiums. Once you hit 55, your options narrow significantly. Simplified issue becomes your primary choice, with guaranteed issue reserved for those who can’t qualify elsewhere. This age-based structure reflects how insurers price risk without medical exams-they rely heavily on actuarial data showing that younger applicants have fewer hidden health issues, making them safer bets for rapid approval.

Utah residents over 60 should focus instead on simplified or guaranteed issue policies, which prioritize speed over premium savings. The trade-off is clear: you sacrifice affordability for accessibility.

How Your Health History Affects Eligibility

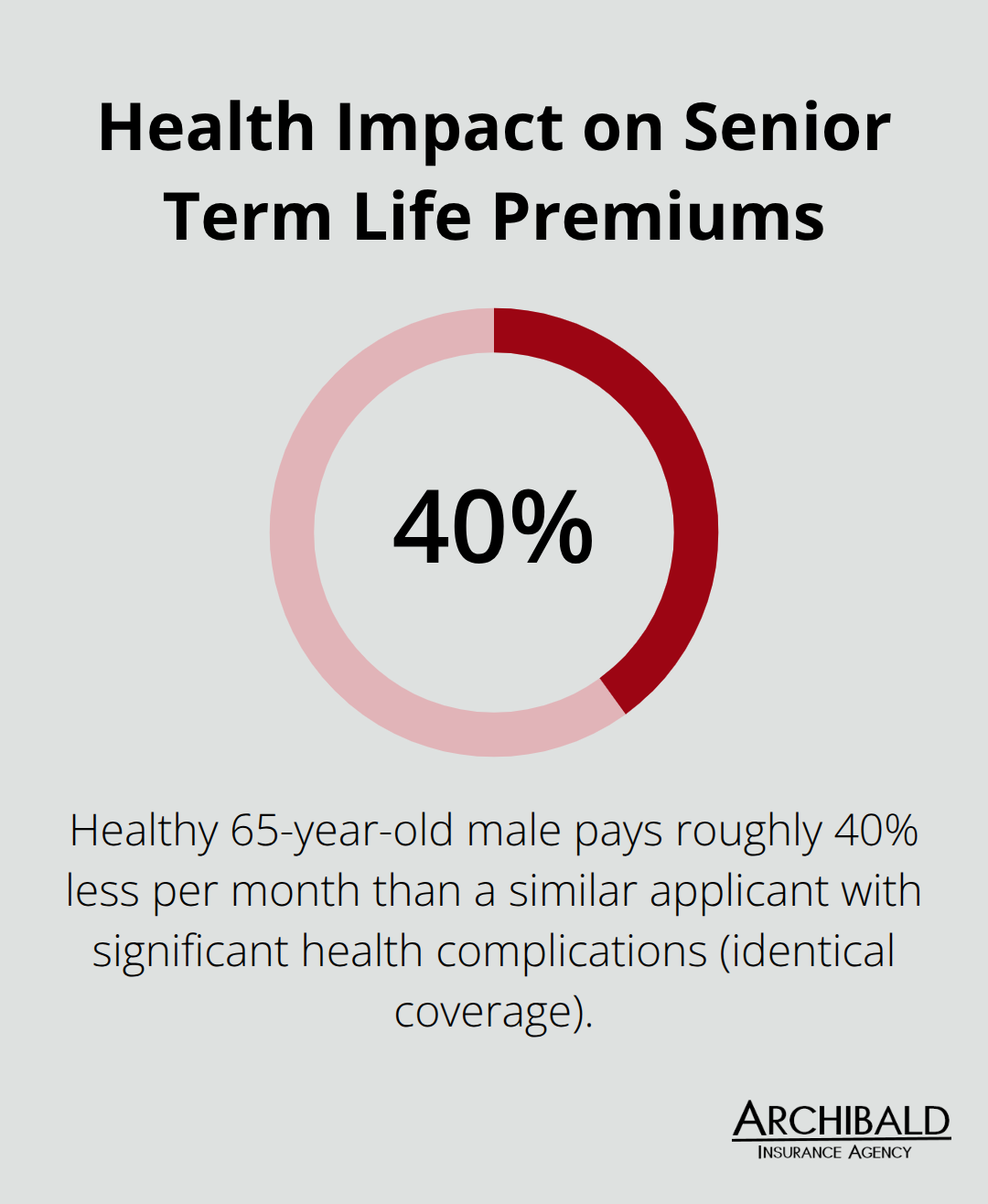

Your health history matters even without an exam. Insurers pull your prescription records, pharmacy data, and past insurance applications to assess risk. If you take medications for diabetes, heart disease, or cancer, you’ll likely qualify only for simplified or guaranteed issue policies, not accelerated underwriting. Minor conditions like high blood pressure or high cholesterol managed with common medications typically don’t disqualify you from accelerated underwriting, though your premiums will reflect this information.

Pre-existing conditions don’t automatically exclude you from coverage, but they do determine which policy type you access and how much you’ll pay monthly. The key difference: accelerated underwriting requires clean records, while simplified and guaranteed issue policies accept applicants with significant health histories.

Coverage Limits Vary by Policy Type and Health Profile

Coverage limits depend directly on what insurers learn during underwriting without exams. Accelerated underwriting policies max out around $1.5 million for the healthiest applicants, but most Utah residents qualify for $250,000 to $500,000 without extensive documentation. Simplified issue policies typically cap at $500,000, sometimes lower depending on your age and health profile. Guaranteed issue policies offer the least coverage, usually $10,000 to $25,000, designed specifically for funeral expenses rather than income replacement.

The National Funeral Directors Association reported in 2024 that median funeral costs with viewing and burial reached $8,300, making guaranteed issue adequate only for final expenses. Insurers make individual decisions based on data they uncover, meaning two 50-year-olds applying for the same policy might receive different coverage limits.

Important Restrictions and Exclusions

Suicide exclusions apply to most no-exam policies during the first two years, meaning beneficiaries receive only premiums paid plus interest if death results from suicide within this window. After two years, the full death benefit pays. Some carriers in Utah also include contestability periods of two years, allowing them to deny claims if you misrepresented health information on your application.

This protection exists because no-exam underwriting accepts higher risk, making insurers more cautious about fraudulent applications. Understanding these restrictions helps you make informed decisions about which policy type fits your situation and timeline.

Your eligibility and coverage amount ultimately depend on how insurers evaluate your age, health records, and application details. The next section compares how no-exam policies stack up against traditional life insurance in terms of cost, coverage, and real-world value for Utah residents.

No-Exam vs. Traditional Life Insurance

Premium Costs Reveal the Speed Tax

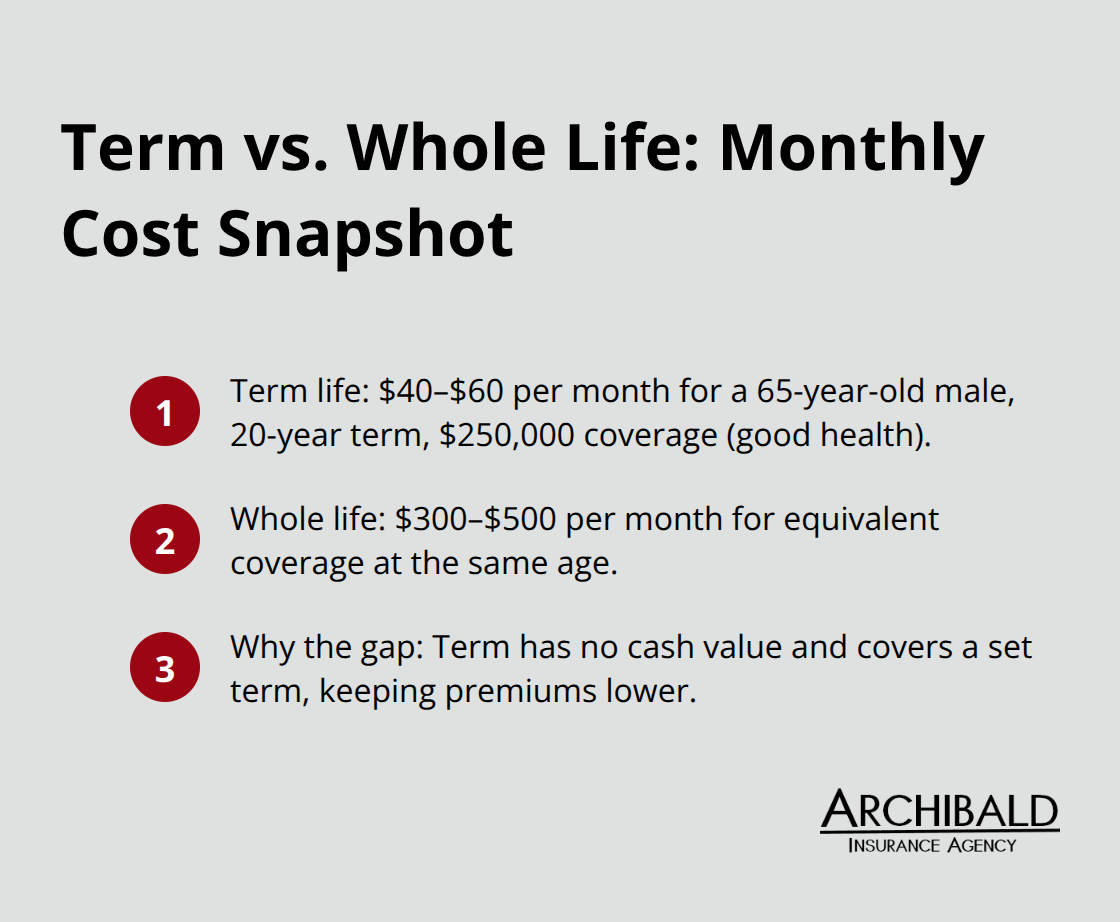

The cost difference between no-exam and traditional life insurance hits hard once you run actual numbers. A healthy 35-year-old Utah resident seeking $500,000 in term coverage pays roughly $25 to $40 monthly with traditional underwriting, while the same person pays $40 to $60 monthly for accelerated underwriting without exams. That $15 to $25 monthly gap compounds to $180 to $300 annually, or $2,160 to $3,600 over a decade. The premium penalty exists because insurers accept greater risk without direct medical evidence.

However, this cost premium vanishes if you need coverage in days rather than weeks. Traditional underwriting takes 4 to 8 weeks in Utah due to medical exam scheduling, record verification, and underwriting review. If you face a health change, job transition requiring proof of insurance, or mortgage closing within 30 days, the no-exam premium becomes irrelevant because traditional policies simply won’t close in time. Simplified issue policies run even higher, often $60 to $100 monthly for identical coverage.

Coverage Amounts and Policy Limits

Coverage amounts tell a different story than premiums. Accelerated underwriting policies cap around $1.5 million for the healthiest applicants, though most Utah residents qualify for $250,000 to $500,000 without extensive documentation. Simplified issue typically maxes at $500,000. Guaranteed issue policies offer only $10,000 to $25,000, adequate for funeral expenses but useless for income replacement.

Traditional underwriting imposes no such limits for healthy applicants, allowing coverage up to $1 million or beyond based on income and insurability. This matters enormously if you need substantial protection. A single parent earning $75,000 annually needs roughly 10 to 12 times annual income plus mortgage and education costs, totaling perhaps $1.2 million in coverage. No-exam policies may cap your options at $500,000, forcing you to supplement with traditional coverage or accept insufficient protection.

When No-Exam Policies Make Sense for Utah Residents

No-exam policies work for Utah residents in specific situations. Try accelerated underwriting if you are under 50, relatively healthy, need coverage within two weeks, and can afford the monthly premium increase. This option balances speed and affordability. Select simplified issue if you have minor health conditions, are between 50 and 60, and still need relatively quick approval without the medical exam burden. Reserve guaranteed issue only for final expense coverage when you cannot qualify elsewhere and speed matters more than death benefit size.

Avoid no-exam policies if you need substantial coverage amounts or plan to keep the policy for 20 or 30 years, since the premium penalty compounds significantly over time. A $15 monthly increase on a 30-year policy costs $5,400 in extra premiums-money that could fund traditional underwriting instead.

Regulatory Protections Apply Equally

Utah’s regulatory protections apply equally to both policy types. The Utah Insurance Department oversees both no-exam and traditional carriers, and the Utah Life & Health Insurance Guaranty Association protects policyholders up to $200,000 cash value and $500,000 death benefits if an insurer fails. Two-year contestability periods and suicide exclusions apply to both, meaning beneficiaries receive only premiums plus interest if death occurs within two years by suicide. These protections level the playing field regarding insurer reliability.

The real decision hinges on your timeline and coverage needs. If you need quick protection and can afford higher premiums, no-exam works. If you have substantial income to replace or want the lowest possible monthly cost, traditional underwriting delivers better value despite the wait.

Final Thoughts

No medical test life insurance solves a real problem for Utah residents who need coverage fast, but speed always costs money. Younger applicants under 45 with clean health records benefit most from accelerated underwriting, which balances affordability with speed, while those over 55 or with significant health conditions should focus on simplified or guaranteed issue policies, accepting higher costs in exchange for accessibility. Never sacrifice coverage amount just to avoid a medical exam, since traditional underwriting often delivers better long-term value despite the longer timeline if you need substantial protection to replace income or cover a mortgage.

We at Archibald Insurance Agency help Utah residents navigate these decisions every day by representing multiple carriers and comparing no-exam options from different insurers to find the policy that actually fits your situation. Our team understands Utah’s regulatory environment and how local protections through the Utah Life & Health Insurance Guaranty Association apply to your coverage, and we walk you through the trade-offs between speed and cost while explaining which policy type matches your age and health profile. We answer questions about exclusions and contestability periods without pressure or hidden fees, providing straightforward advice about whether no medical test life insurance makes sense for you.

Start by getting a quote online or calling for a free consultation to assess your coverage needs and review available options from top carriers. Visit Archibald Insurance Agency to begin exploring your options today.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation

Spring is the perfect time to dive into a deep cleaning session for your home. Instead of overwhelming yourself with an extensive checklist, let’s focus on five key things to keep in mind when tackling your spring cleaning tasks.

Spring is the perfect time to dive into a deep cleaning session for your home. Instead of overwhelming yourself with an extensive checklist, let’s focus on five key things to keep in mind when tackling your spring cleaning tasks.