Water damage is one of the most common claims homeowners file, yet many don’t understand what their policy actually covers. At Archibald Insurance Agency, we’ve seen Utah homeowners face unexpected bills because they didn’t know whether homeowners insurance covers water damage.

The answer isn’t simple-some water damage is covered, while other types aren’t. This guide breaks down exactly what your policy protects and where gaps might exist.

What Water Damage Does Your Homeowners Policy Actually Cover

Your homeowners insurance covers water damage that happens suddenly and accidentally, but only when it originates from inside your home or results from a covered weather event. Most approved water damage claims fall into sudden and accidental categories such as burst pipes and appliance failures, and roof leaks caused by storms. If a pipe freezes and bursts during a Utah winter, your policy protects you. If your water heater fails unexpectedly and floods your basement, coverage applies. If heavy rain damages your roof and water pours through the ceiling, you’re protected. The key word is sudden. Damage that develops slowly over weeks or months typically isn’t covered, even if it eventually causes significant harm.

Burst Pipes and Appliance Failures

Burst pipes rank among the most common water damage claims Utah homeowners file, and your policy protects you when the rupture happens without warning. A pipe that freezes solid and cracks during winter qualifies for coverage if you took reasonable preventive steps, such as maintaining heat in your home or insulating exposed pipes. However, if your thermostat drops below 55°F or your home sits vacant without winterization, insurers often deny these claims. Appliance leaks work similarly. A dishwasher, washing machine, or refrigerator that suddenly malfunctions and floods your kitchen floor receives coverage under your personal property and dwelling protections. Water damage claims average $13,954, which makes coverage knowledge vital for protecting your home. Act fast when you discover the damage. Insurers typically expect you to report a claim within 24 to 48 hours and take immediate steps to stop the water flow and prevent further damage.

Storm Damage and Ice Dams

Water damage from storms and heavy rainfall receives coverage when water enters through damaged roof structures, broken windows, or compromised exterior walls caused by wind, hail, or falling debris. If a severe thunderstorm tears shingles from your roof and rain saturates your attic and upper floors, your policy covers that loss. Ice dams form along roof edges during freeze-thaw cycles and can trap water, forcing it under shingles and into your home. Ice dams can cause hidden damage that worsens over time, and coverage depends on whether the water intrusion was sudden or stemmed from maintenance neglect like clogged gutters. The distinction matters significantly. If you failed to clean gutters and an ice dam formed as a result, an insurer might deny your claim based on negligence. If you maintained your gutters properly and an unusually severe ice dam still caused sudden water entry, coverage typically applies. The weight of accumulated snow can also damage roof structures, and that structural collapse receives coverage. Document everything with photographs or video immediately after you discover damage, and don’t remove or repair anything until an adjuster inspects the property.

What Happens Next With Your Coverage

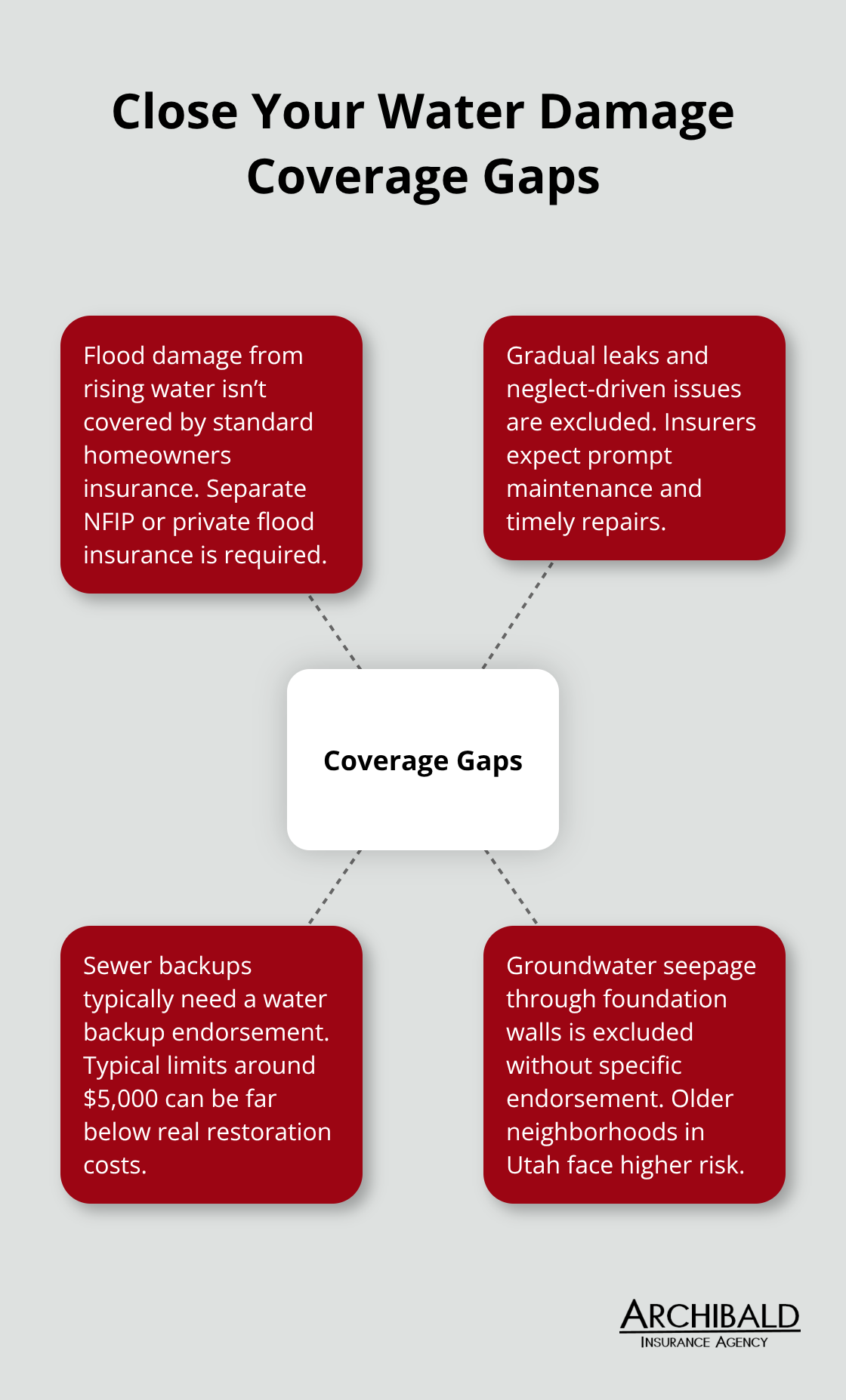

Once you understand what your policy covers, the next critical step involves identifying the gaps. Many Utah homeowners assume their standard policy protects them completely, only to face denial when they file a claim for damage that falls outside standard coverage. Flood damage, sewer backups, and gradual seepage represent common exclusions that leave homeowners vulnerable. Knowing these gaps now allows you to add the right endorsements and separate policies before water damage strikes your home.

What Your Homeowners Insurance Won’t Cover for Water Damage

Flood Damage: The Biggest Coverage Gap

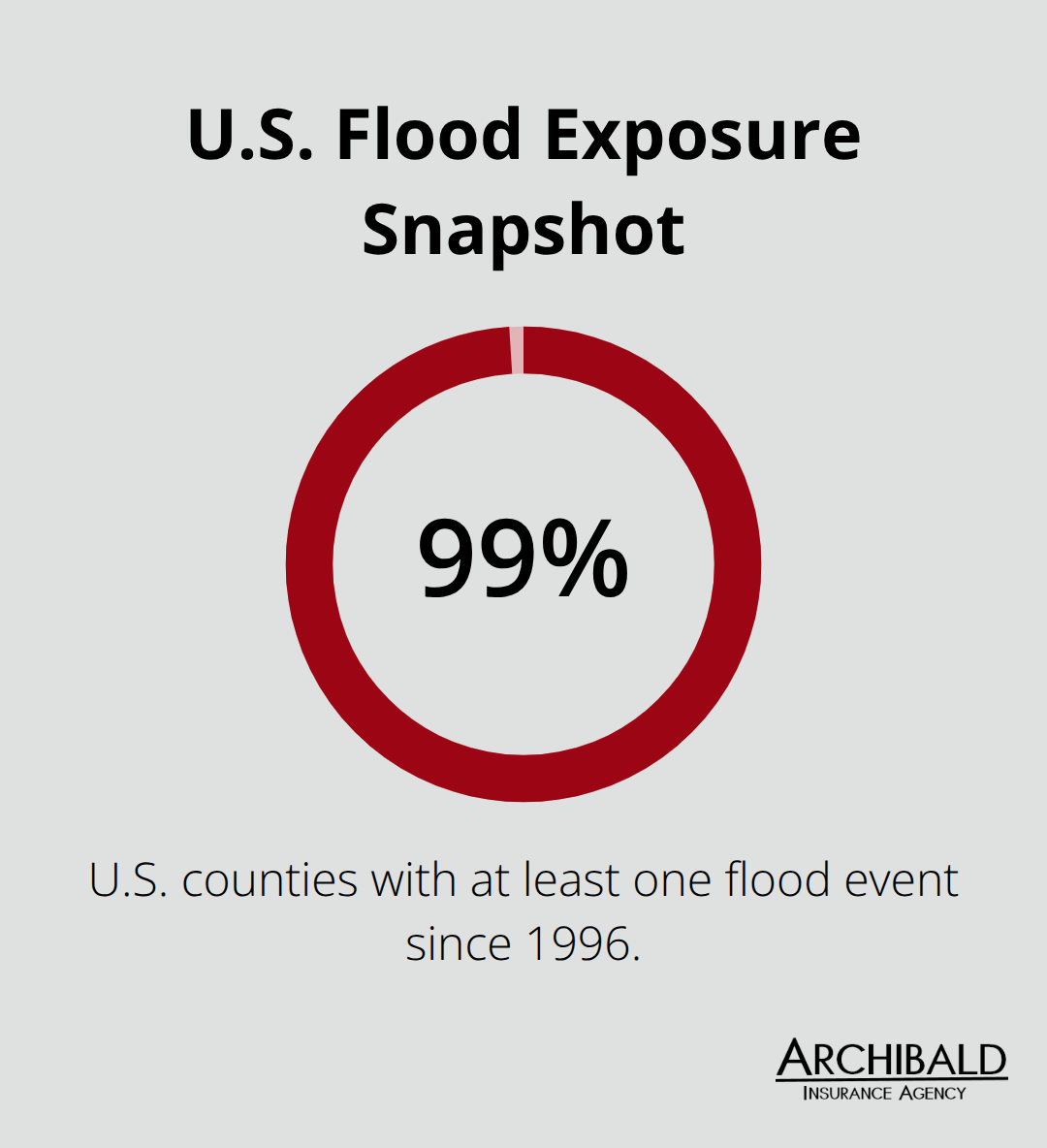

Flood damage represents the largest coverage gap in standard homeowners policies, and it’s the reason most Utah homeowners end up uninsured for the water damage that actually strikes their homes. When heavy rain overwhelms local drainage systems, rivers overflow their banks, or storm surge pushes water inland, your homeowners insurance provides no protection. The National Flood Insurance Program reports that flood insurance through NFIP costs roughly $700 per year, yet NFIP claim payments average around $52,000-a stark contrast that shows how devastating floods become when you lack protection. Since 1996, 99 percent of U.S. counties have experienced at least one flood event, and urban flooding now occurs roughly every two to three days across America.

If you live anywhere near a river, in a low-lying area, or in a region that experienced flooding in recent years, you need separate flood insurance. Your homeowners policy distinguishes sharply between wind-driven rain that enters through storm damage and rising water that floods your property. A broken window from hail that lets rain inside receives coverage. Water that rises from the ground or flows in from overwhelmed drainage systems does not.

Gradual Leaks and Maintenance Failures

Gradual leaks and maintenance failures create another massive exclusion that catches homeowners off guard. Homeowners insurance generally covers sudden and accidental water damage like burst pipes or ruptured appliances, but excludes damage from neglect and deferred maintenance. A slow bathroom sink leak that you notice but ignore for weeks falls squarely into this excluded category.

Your insurer expects you to maintain your home and address problems promptly. Damage that develops slowly over time-even if it eventually causes significant harm-receives no coverage. This exclusion protects insurers from covering preventable damage while placing responsibility on homeowners to act responsibly.

Sewer Backups and Groundwater Seepage

Sewer backups and groundwater seepage complete the coverage gap. When your home’s sewer line fails or groundwater seeps through basement walls, standard homeowners insurance provides zero protection unless you purchased a specific water backup endorsement. Most water backup endorsements carry limits around $5,000, which sounds reasonable until you face $20,000 to $100,000 in basement restoration costs.

Groundwater intrusion happens particularly in Utah’s older neighborhoods where foundation drainage systems have deteriorated over decades. Hydrostatic pressure from groundwater pushes water through foundation walls and cracks, and this damage remains excluded without an endorsement. If you’ve never added water backup coverage to your policy, contact your agent immediately.

Identifying Your Coverage Gaps

These gaps between what your policy covers and what actually happens during water events create financial exposure that most homeowners underestimate. The good news is that you can fill many of these gaps with targeted endorsements and separate policies. Understanding exactly which types of water damage your current policy excludes allows you to make informed decisions about additional protection before disaster strikes. Your next step involves taking concrete action to protect your home from the water damage that your standard policy won’t cover.

Stop Water Damage Before It Starts

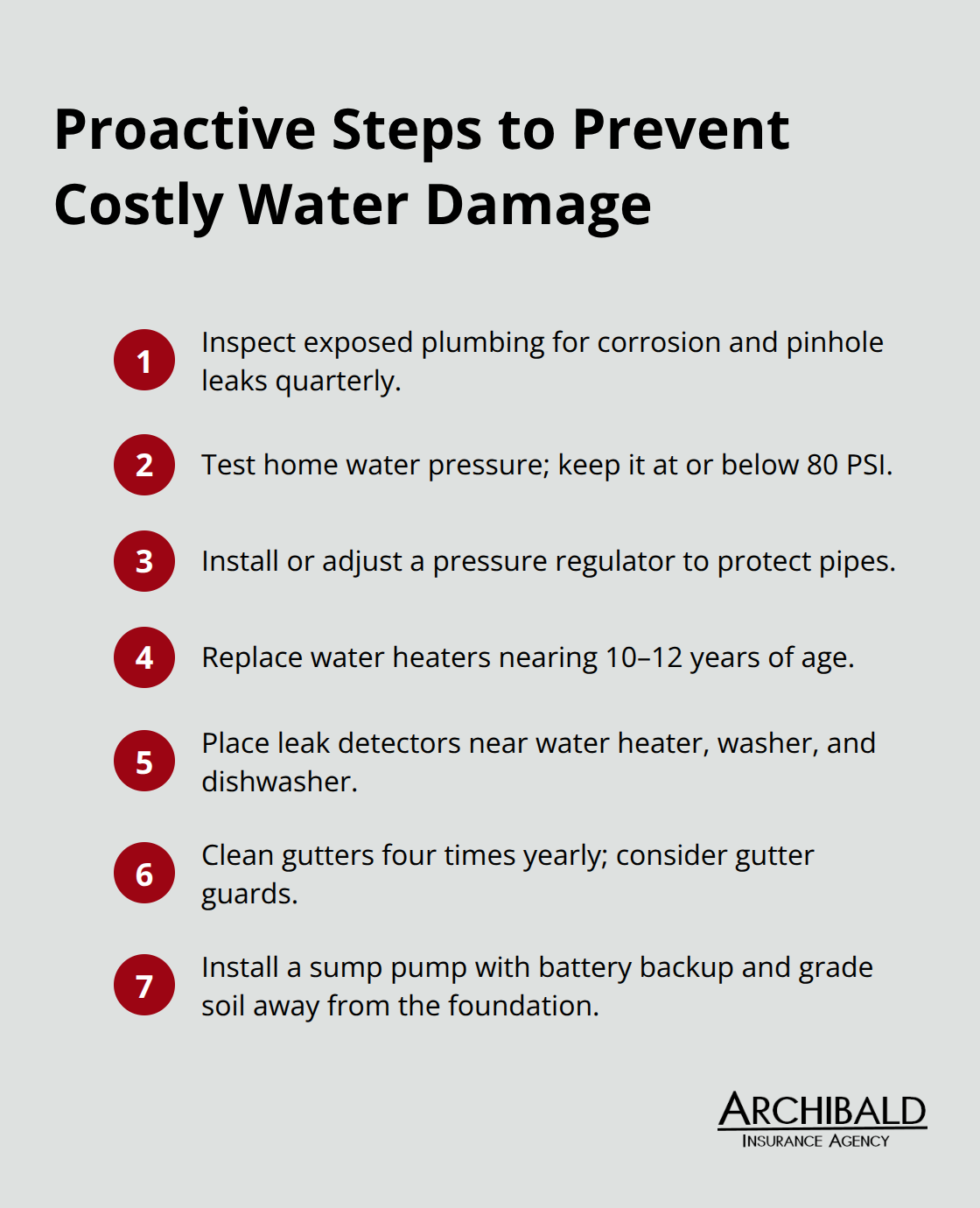

The most effective water damage protection happens before water enters your home. Maintenance prevents costly water damage claims that most Utah homeowners face. Start with your plumbing system, which fails more often than any other water damage source. According to the Insurance Information Institute, water damage and freezing claims represent a significant portion of homeowners insurance claims each year. Inspect visible pipes under sinks, around your water heater, and in the basement for corrosion, mineral buildup, or pinhole leaks. Corroded copper pipes fail without warning, and replacing them requires professional plumbing work that typically costs $45 to $200 per hour.

Address Aging Pipes and Water Pressure

If your home was built before 1980, galvanized steel pipes are likely deteriorating right now. Test your water pressure with an inexpensive gauge from any hardware store. Pressure above 80 PSI stresses pipes and accelerates failure. A pressure regulator costs under $200 and prevents premature pipe rupture. Check your water heater’s age by looking at the manufacture date on the tank.

Most water heaters last 10 to 12 years before failure becomes likely. If yours is older, schedule replacement before it ruptures and floods your home.

Install Early Detection Systems

Install water leak detectors near your water heater, washing machine, and dishwasher. These battery-powered devices cost $15 to $50 and alert you immediately when moisture appears, catching leaks within hours instead of weeks. Early detection stops small problems from becoming expensive disasters.

Maintain Your Roof and Gutters

Your roof requires equal attention because storm damage creates a major category of water intrusion claims. Walk your roof twice yearly, in spring and fall, looking for missing shingles, deteriorated flashing, and gaps where water can enter. Clean gutters four times per year in Utah, where spring snowmelt and fall leaves create blockages that force water under roof edges and into fascia boards. Clogged gutters transform into ice dams during winter freeze-thaw cycles, trapping water and forcing it through shingles. Installing gutter guards reduces cleaning frequency to twice yearly and costs $1,000 to $2,000 for most homes. Trim tree branches hanging over your roof to prevent limb damage during winter storms and reduce debris accumulation.

Protect Your Foundation and Basement

If your home sits in a flood-prone area or near groundwater seepage risk, install a sump pump in your basement now, not after water damage occurs. Sump pumps cost $500 to $2,000 installed and remove water automatically before it damages foundations or finishes. Check that your pump runs properly by pouring water into the sump pit to trigger activation. A battery backup system costs an additional $400 to $600 and keeps the pump running during power outages that often accompany storms. Grade your property so water slopes away from your foundation. Standing water against foundation walls creates hydrostatic pressure that forces groundwater through cracks and seepage points. Proper grading costs under $500 and prevents thousands in basement damage.

Add Targeted Insurance Coverage

After addressing these maintenance fundamentals, add the specific insurance protections your home needs. Water backup endorsements cost $50 to $100 annually and cover sewer backups and sump pump failures up to typical limits of $5,000. If your home sits in a flood zone, NFIP flood insurance at roughly $700 per year provides building coverage up to $250,000 and contents coverage up to $100,000. Private flood insurers sometimes offer higher limits or broader coverage in specific situations. Your independent insurance agent can review your current policy and identify which endorsements and separate policies make sense for your Utah home’s specific risks.

Final Thoughts

Water damage protection requires three distinct actions working together. First, you must understand exactly what your homeowners insurance covers and what it doesn’t-does homeowners insurance cover water damage? Yes, but only sudden and accidental damage from inside your home or covered weather events. Flood damage, gradual leaks, sewer backups, and groundwater seepage remain excluded unless you purchase separate coverage. Knowing these boundaries prevents costly surprises when you file a claim.

Second, maintenance stops water damage before it starts. You should inspect your plumbing for corrosion and test water pressure regularly, replace aging pipes and water heaters before they fail, and clean gutters four times yearly to prevent ice dams and roof leaks. These steps cost far less than water damage restoration, which ranges from $1,381 to $6,350 for typical claims and can exceed $100,000 for basement flooding. Early detection systems catch leaks within hours instead of weeks, preventing the mold growth that begins within 24 to 48 hours of water exposure.

Third, you need to fill your coverage gaps with targeted endorsements and separate policies. Water backup coverage costs $50 to $100 annually and protects against sewer backups and sump pump failures, while flood insurance through NFIP costs roughly $700 per year and covers the rising water that standard policies exclude entirely. Contact Archibald Insurance Agency today to review your water damage coverage and add the protections that give you genuine peace of mind.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation

Distracted driving has become a major concern, with thousands of injuries and fatalities reported each year. Not only does it pose a significant risk to ourselves and others on the road, but it has also led to skyrocketing insurance premiums and an increase in traffic accidents.

Distracted driving has become a major concern, with thousands of injuries and fatalities reported each year. Not only does it pose a significant risk to ourselves and others on the road, but it has also led to skyrocketing insurance premiums and an increase in traffic accidents.

Jewelry holds not only aesthetic value but also sentimental significance. Whether it symbolizes decades of marriage, has been passed down through generations, or commemorates a special occasion, its worth goes beyond monetary value. With this in mind, our local insurance agency aims to ensure that you have comprehensive protection for your precious pieces.

Jewelry holds not only aesthetic value but also sentimental significance. Whether it symbolizes decades of marriage, has been passed down through generations, or commemorates a special occasion, its worth goes beyond monetary value. With this in mind, our local insurance agency aims to ensure that you have comprehensive protection for your precious pieces.