Your homeowners insurance policy is only as good as the coverage you choose. Most Utah homeowners don’t realize how many gaps exist in their standard policies until they file a claim.

We at Archibald Insurance Agency help families understand the different types of homeowners insurance coverage available so they can protect what matters most. This guide breaks down your options, from dwelling protection to liability coverage, so you know exactly what you’re buying.

Protecting Your Home’s Structure

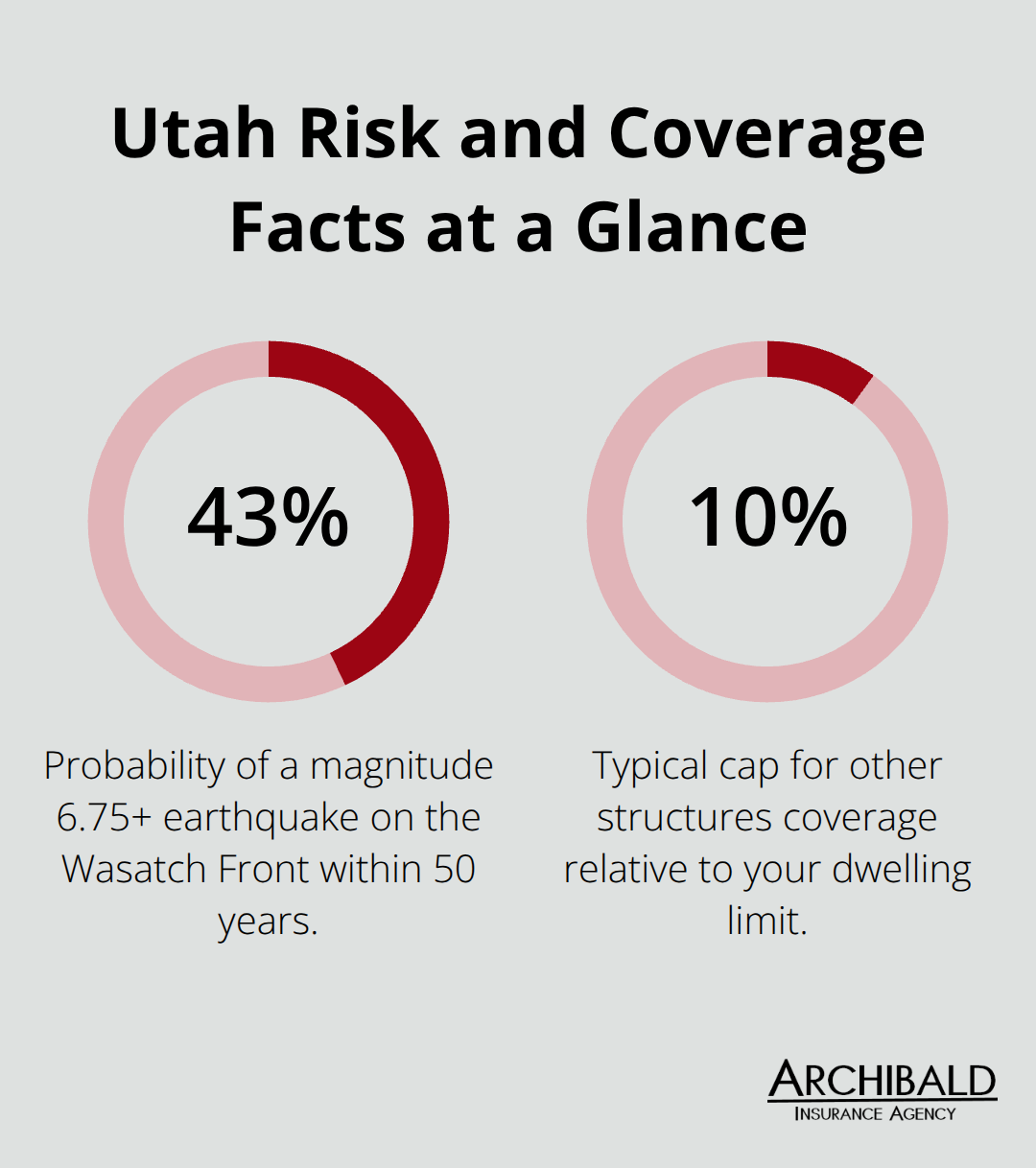

Your home’s structure is the foundation of everything you own, and dwelling coverage is the backbone of any homeowners policy. This coverage pays to rebuild or repair the physical structure of your house if fire, wind, hail, lightning, or other covered perils damage it. Most Utah homeowners carry dwelling coverage because their mortgage lender requires it, but many don’t understand what amount they actually need. The National Association of Insurance Commissioners recommends calculating your dwelling coverage based on the full replacement cost of rebuilding your home today, not its market value. Your home’s land value doesn’t factor into this calculation-only the structure itself. If you underestimate this amount, you’ll face a significant out-of-pocket expense when you file a claim. If you own detached structures like a garage, shed, or deck, those fall under other structures coverage, which typically covers up to 10 percent of your dwelling limit. This matters more than most homeowners realize, especially in Utah where many properties include separate garages or workshops that can cost $15,000 to $40,000 to rebuild.

Replacement Cost Protects Your Wallet

The difference between replacement cost value and actual cash value determines how much your insurer actually pays you after a loss. With replacement cost value, your insurer pays what it costs to rebuild or repair your home using current prices and materials, regardless of depreciation. With actual cash value, your insurer deducts depreciation from the payout, which can leave you far short of what you need to rebuild. Consider a roof damaged by hail that costs $12,000 to replace. Under replacement cost, you receive $12,000 minus your deductible. Under actual cash value, if your roof has depreciated 40 percent over 15 years, you receive only $7,200 minus your deductible. That $4,800 gap comes directly out of your pocket.

Policy Types and Coverage Levels

The HO-3 policy, which is the most common homeowners policy in Utah and across the nation, covers your home and other structures on an open-perils basis. The HO-5 policy, the second most popular option, covers both dwelling and personal property at replacement cost, offering significantly better protection for your belongings. Choose replacement cost coverage for your dwelling without hesitation. The premium difference is modest compared to the financial protection it provides when disaster strikes. Your choice between these two policies shapes how well your home and possessions hold up financially after a covered loss.

What Comes Next in Your Coverage Strategy

Beyond your dwelling and other structures, your policy must address what happens to your personal belongings and your liability exposure when someone gets injured on your property. These coverage types work together to create a complete protection plan that shields both your physical assets and your financial future.

Personal Property, Liability, and Guest Protection

Understanding Personal Property Coverage

Your dwelling and other structures coverage protects the building itself, but your belongings inside that home need separate protection. Personal property coverage pays to replace your furniture, electronics, clothing, and other items if fire, theft, or other covered perils damage or destroy them. Under an HO-3 policy, personal property coverage typically applies at actual cash value, meaning depreciation reduces what you receive. An HO-5 policy covers personal property at replacement cost, which is substantially better.

Consider what happens when fire destroys your five-year-old television worth $800 new. Actual cash value might pay only $320 after depreciation, while replacement cost covers the full $800 to buy a new one today. Most standard policies cap personal property coverage at 50 to 70 percent of your dwelling limit, so a $300,000 home might have only $150,000 to $210,000 in belongings coverage. This limit often falls short for Utah homeowners with valuable collections, high-end electronics, or significant jewelry.

Protecting High-Value Items

High-value items like art, jewelry, and electronics require scheduled personal property endorsements to receive full replacement cost protection without depreciation penalties. These endorsements list specific items and their values, guaranteeing coverage at the amount you specify regardless of age or condition. Without these endorsements, your standard policy may pay far less than what your valuables are actually worth.

Personal Liability Coverage Shields Your Financial Future

Personal liability coverage protects you financially if a guest is injured at your home or if you accidentally damage someone else’s property. This coverage pays legal defense costs and judgments up to your policy limit, which typically ranges from $100,000 to $500,000. Most Utah homeowners carry $300,000 in liability coverage, though higher limits cost only slightly more in premiums.

Liability coverage becomes critical when injuries are serious. A guest who falls down your stairs and suffers a permanent injury could sue for $250,000 or more in damages. Your liability coverage pays for their legal claim, your defense attorney, and any judgment up to your limit. Homeowners with pools, trampolines, or frequent guests should increase liability limits to $500,000 or $1,000,000 because these situations dramatically increase injury risk.

Medical Payments Coverage for Immediate Guest Injuries

Medical payments to others coverage is separate from liability and pays medical expenses for guests injured on your property without requiring fault. This coverage pays immediate medical bills up to $1,000 or $5,000 depending on your policy. A guest who slips on your icy walkway in January and incurs $2,000 in emergency room bills receives coverage under medical payments, avoiding a potential lawsuit. This protection prevents small injuries from escalating into legal disputes.

Planning for Gaps Beyond Standard Coverage

Your personal property, liability, and medical payments coverage work together to protect your belongings and shield you from injury claims. However, standard policies exclude certain risks that Utah homeowners face regularly-water damage from floods, earthquake damage, and coverage for valuable items all require additional attention and endorsements to fill protection gaps.

Filling the Coverage Gaps Standard Policies Leave Behind

Standard homeowners policies create dangerous blind spots that leave Utah homeowners exposed to some of the state’s most common disasters. Flood damage strikes outside designated flood zones more than 70 percent of the time in Utah, yet standard policies exclude all water damage from flooding. Earthquake coverage is similarly absent from every basic policy, despite the Wasatch Front region facing a 43 percent probability of a magnitude 6.75 or stronger earthquake within the next 50 years. Valuable items like jewelry, art, and high-end electronics receive limited protection under standard personal property coverage because most policies cap claims on these categories at just $1,000 to $2,500 total.

Why Flood Insurance Requires Advance Planning

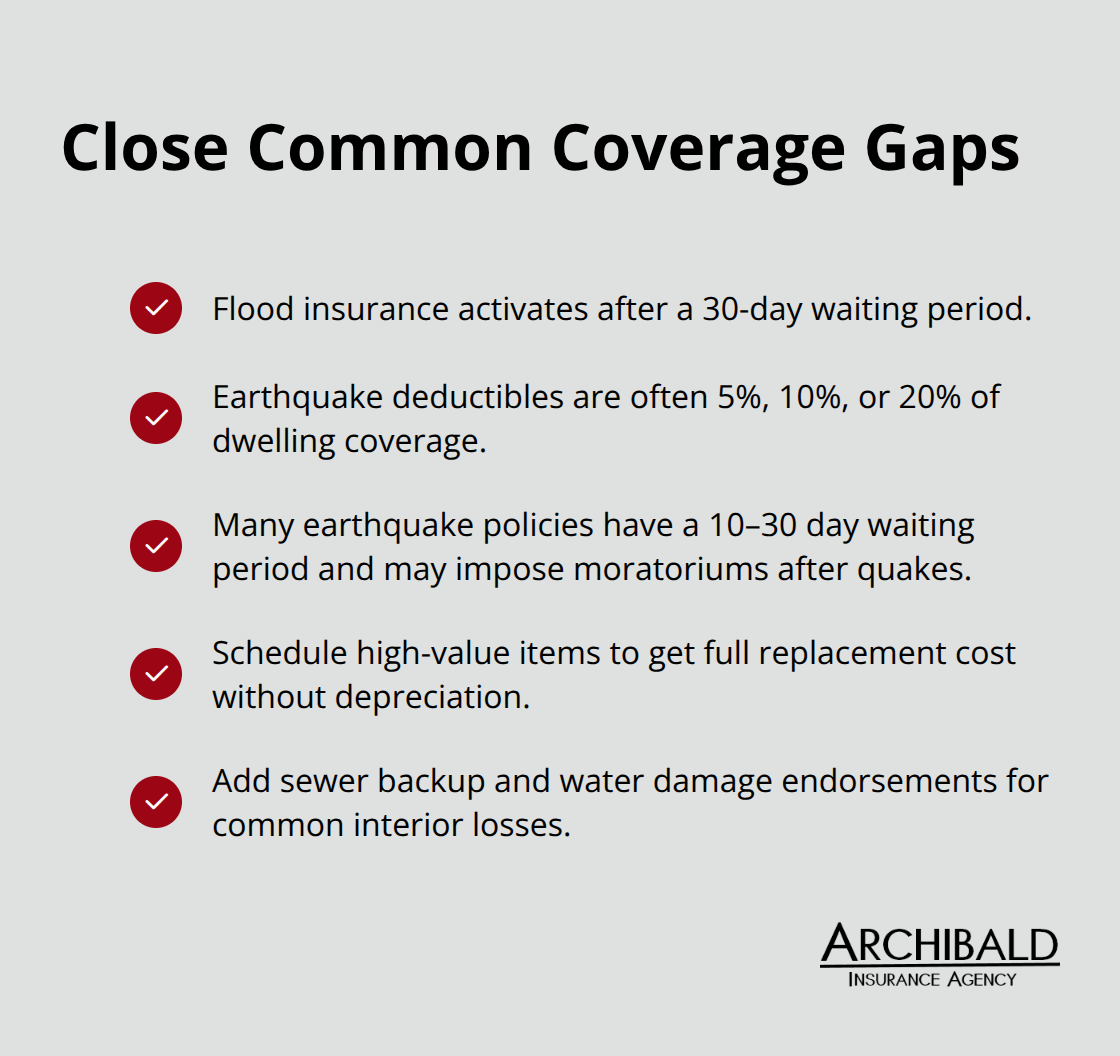

Flood insurance through the National Flood Insurance Program becomes effective only after a 30-day waiting period, meaning you cannot purchase it the day a flood threatens your neighborhood. This timing constraint makes advance planning essential rather than optional. Utah homeowners in flood-prone areas should obtain separate flood insurance immediately rather than waiting for storm warnings. The cost of this protection pales in comparison to the financial devastation that flood damage inflicts on homes and belongings.

Understanding Earthquake Deductibles and Waiting Periods

Earthquake coverage demands immediate attention for Utah homeowners because earthquake deductibles typically apply as a percentage of your dwelling coverage, commonly 5 percent, 10 percent, or 20 percent, rather than a flat dollar amount. On a $400,000 home with 10 percent earthquake deductible, you would pay $40,000 out of pocket before earthquake coverage activates. Most earthquake policies also require a 10 to 30-day waiting period before coverage binds, and insurers impose coverage moratoriums after recent earthquakes in affected regions. Those in earthquake zones should compare earthquake coverage options through your current insurer, alternative providers, or Difference in Conditions policies that layer additional catastrophe protection over your standard homeowners policy.

Protecting High-Value Belongings Through Scheduled Coverage

Scheduled personal property endorsements solve the valuable items problem by listing specific high-value belongings with their agreed-upon values, guaranteeing replacement cost protection without depreciation regardless of age or condition. This endorsement costs far less than you might expect, often adding only $100 to $300 annually while protecting items that might be worth $50,000 or more. High-value collections receive the full protection they deserve without the depreciation penalties that standard policies impose.

Addressing Water Damage Beyond Flood Coverage

Water damage from backed-up sewers and frozen pipes caused by negligence remains excluded even with endorsements, but sewer backup coverage and water damage endorsements address the most common interior water losses. These targeted endorsements fill specific protection gaps that standard policies leave unprotected, ensuring that common Utah water damage scenarios receive proper coverage.

Final Thoughts

Your home, your belongings, and your liability exposure are unique, and the types of homeowners insurance coverage you select should reflect that reality. We at Archibald Insurance Agency work with multiple carriers to customize coverage that matches your specific situation and budget rather than pushing policies that don’t fit your needs. Calculate what it would actually cost to rebuild your home today using current materials and labor, inventory your high-value items, and assess your liability exposure based on how often guests visit and whether you have a pool or trampoline.

One-size-fits-all policies fail Utah homeowners because they ignore the specific risks your property faces and the assets you need to protect. Flood insurance requires advance planning since coverage takes 30 days to activate, and earthquake coverage demands immediate attention given the Wasatch Front’s seismic risk. Scheduled personal property endorsements protect your valuable collections without depreciation penalties, while sewer backup and water damage endorsements address the interior water losses that standard policies exclude.

Contact Archibald Insurance Agency to review your current policy or build a new one from scratch. Our independent agents take time to understand your home, your assets, and your concerns before recommending coverage that actually protects what matters most. We answer your questions and ensure you’re protected against the disasters that pose the greatest threat to your financial security.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation

Protecting oneself from major claims or lawsuits and protecting assets and earnings is a priority for anyone. This is where an umbrella insurance policy comes into play, providing an additional layer of coverage that goes beyond traditional policies. By insuring your future, you can protect your home, cash savings, and future earnings from unforeseen circumstances.

Protecting oneself from major claims or lawsuits and protecting assets and earnings is a priority for anyone. This is where an umbrella insurance policy comes into play, providing an additional layer of coverage that goes beyond traditional policies. By insuring your future, you can protect your home, cash savings, and future earnings from unforeseen circumstances.