Understanding Life Insurance Policies A Simple Guide

Life insurance is one of the most important financial decisions you’ll make, yet many people put it off because the options feel overwhelming. We at Archibald Insurance Agency help Utah families cut through the confusion and find coverage that actually fits their lives.

Understanding life insurance policies doesn’t require a finance degree. This guide walks you through the main types of policies, how they work, and how to pick the right one for your situation.

The Three Main Types of Life Insurance

Term Life Insurance: Affordable Short-Term Protection

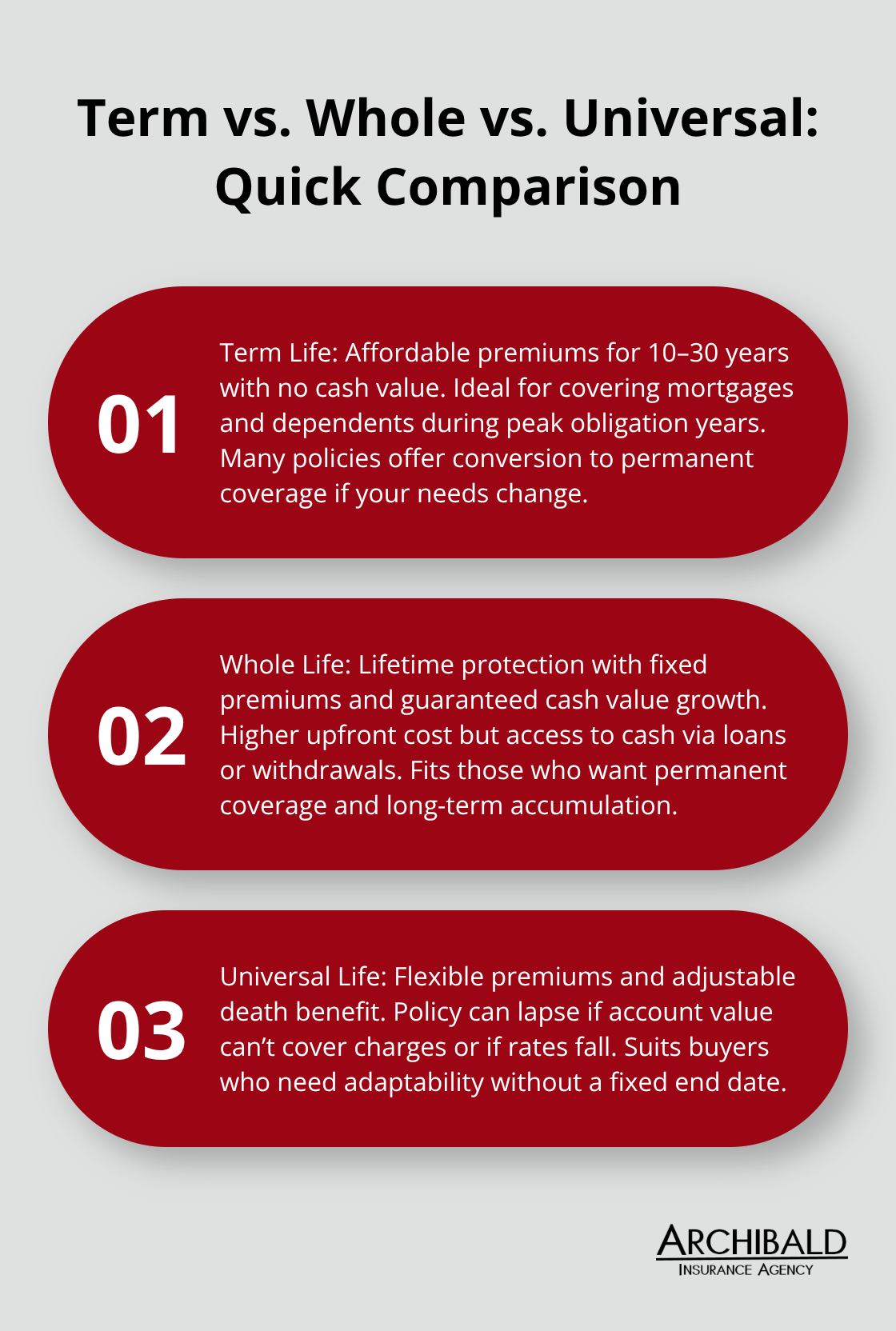

Term life insurance covers you for a specific period-typically 10 to 30 years-with no cash value component. Term life insurance costs an average of $26 per month, though rates vary based on age, gender, and health status. You pay lower premiums in exchange for temporary protection. When the term expires, coverage ends unless you renew, though renewal premiums climb significantly. Many term policies convert to permanent coverage, which protects you if your health changes later.

This option makes sense if you have dependents now but expect fewer financial obligations in 15 or 20 years.

Whole Life Insurance: Permanent Coverage with Cash Value

Whole life insurance provides lifetime coverage with fixed premiums that never increase. Your policy builds cash value at a guaranteed rate, which you can borrow against or withdraw later. MassMutual delivers strong whole life options in Utah with lifetime coverage and potentially higher dividends, though premiums run substantially higher upfront. Term life typically costs five to 15 times less than whole life at the same death benefit amount. Whole life insurance cash value allows policyholders to make withdrawals that are generally income tax-free up to the amount of premiums paid. Whole life suits people who seek permanent protection and cash accumulation alongside their death benefit.

Universal Life Insurance: Flexibility Between Term and Whole Life

Universal life occupies the middle ground: initial premiums are lower than whole life but higher than term, and both your death benefit and premium payments can adjust over time. The flexibility appeals to people whose financial situations change, but account value can decline if interest rates drop or charges exceed earnings. If account value falls below charges, your policy lapses unless you increase premiums or reduce the death benefit. Universal life works for those wanting flexibility without term’s expiration date.

Comparing Your Options in Utah’s Market

Legal & General America leads Utah’s market with competitive rates across all three types and includes options like no-medical-exam approval for faster decisions. Each policy type serves different financial goals and life stages. Your next step involves assessing how much coverage your family actually needs and which policy structure aligns with your long-term plans.

How Life Insurance Actually Works

The underwriting process determines your approval

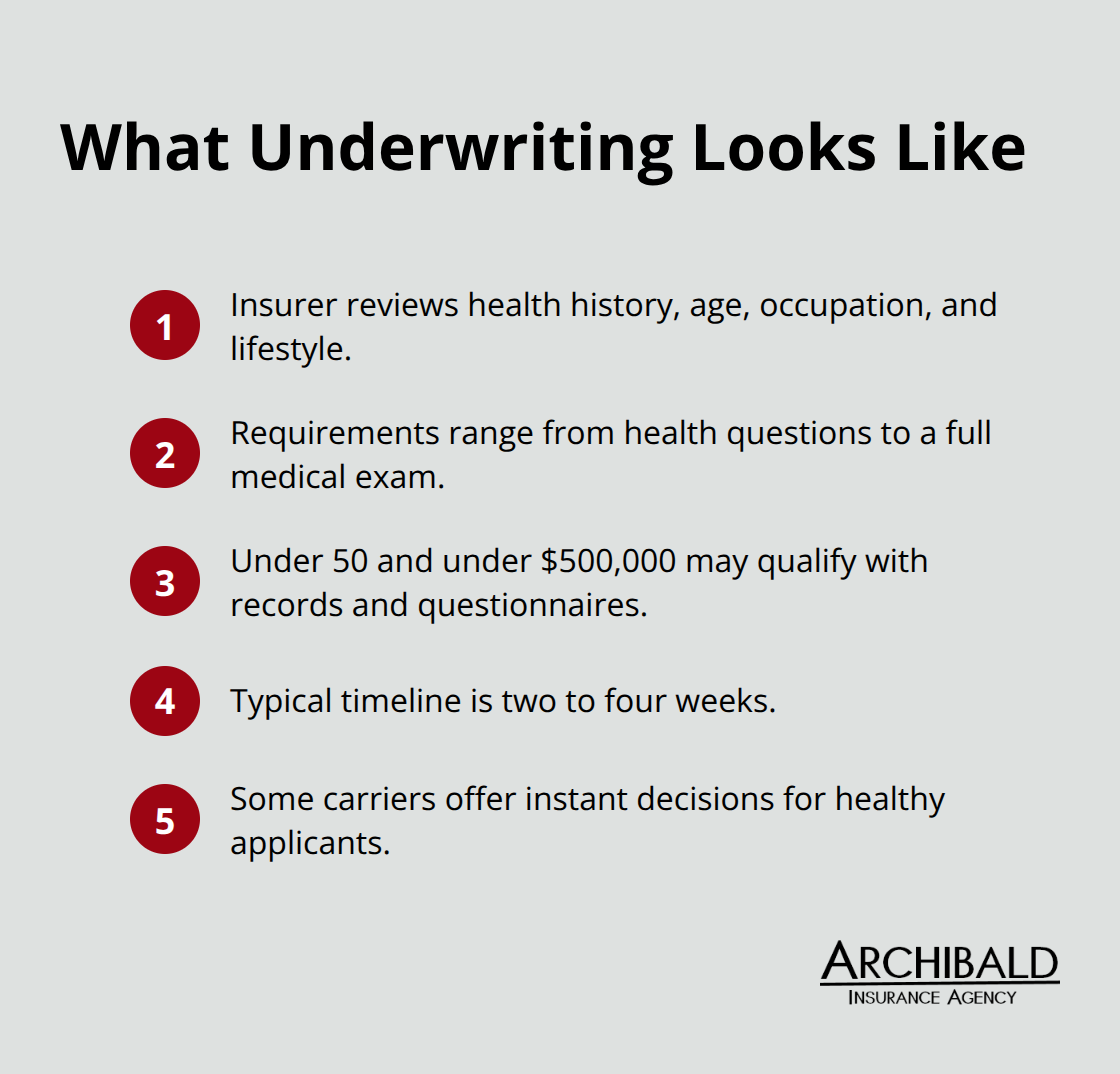

Getting approved for life insurance hinges on underwriting, which is far simpler than most people think. When you apply, the insurer reviews your health history, age, occupation, and lifestyle through a medical assessment that ranges from basic health questions to a full exam depending on the death benefit amount. Applicants under 50 seeking coverage under $500,000 often qualify with just medical records and questionnaires, while larger policies or older applicants typically require blood work and a physical exam. The underwriting process takes two to four weeks on average, though some carriers now offer instant decisions for healthy applicants under certain thresholds.

Honesty during underwriting matters tremendously. Misrepresenting information about your health status or habits can give the insurer grounds to deny claims within the first two years under the contestability period that Utah law establishes. The insurer will verify your statements, so inaccuracies create serious problems when your family needs the death benefit most.

Age, Gender, and Smoking Status Drive Premium Costs

Your age, gender, and smoking status drive premium costs more than anything else. A healthy 35-year-old female pays roughly $25.76 per month for a $500,000 20-year term policy, while a male at the same age pays about $30.79 monthly according to 2023 data, showing how gender affects pricing. Smokers face substantially higher premiums than nonsmokers, though quitting for about one year can reduce your rates significantly. These factors lock in your premium at the time of approval, so applying sooner rather than later protects you from age-related increases.

Payment Options and Premium Structure

Once approved, you’ll choose your payment frequency-monthly, quarterly, annual, or sometimes annual-only options-and your premium remains locked in for term policies. Universal life policies work differently; premiums can adjust depending on account performance and interest rates. Understanding your payment schedule helps you budget for coverage without surprises. Most people select monthly payments for convenience, though annual payments sometimes offer small discounts.

Beneficiary Designation and Death Benefit Distribution

The death benefit flows to your named beneficiaries when you pass away, and in Utah claims must be settled within 15 days of proof of death provided to the insurer. Name specific beneficiaries rather than leaving the payout to your estate, as direct beneficiary designations bypass probate and reach families faster. If your beneficiary is a minor, the insurer won’t pay them directly; instead, name a guardian, your estate, or a trust to manage the funds until they reach legal age.

Update beneficiary information whenever major life events occur-marriage, divorce, birth of a child-because outdated designations create legal complications and delays that frustrate grieving families. Keeping these details current takes minutes but prevents months of confusion later. With underwriting complete and beneficiaries named, you’re ready to evaluate which policy type actually fits your family’s financial situation and long-term goals.

How Much Life Insurance Do You Actually Need

Calculate Your Income Replacement Need

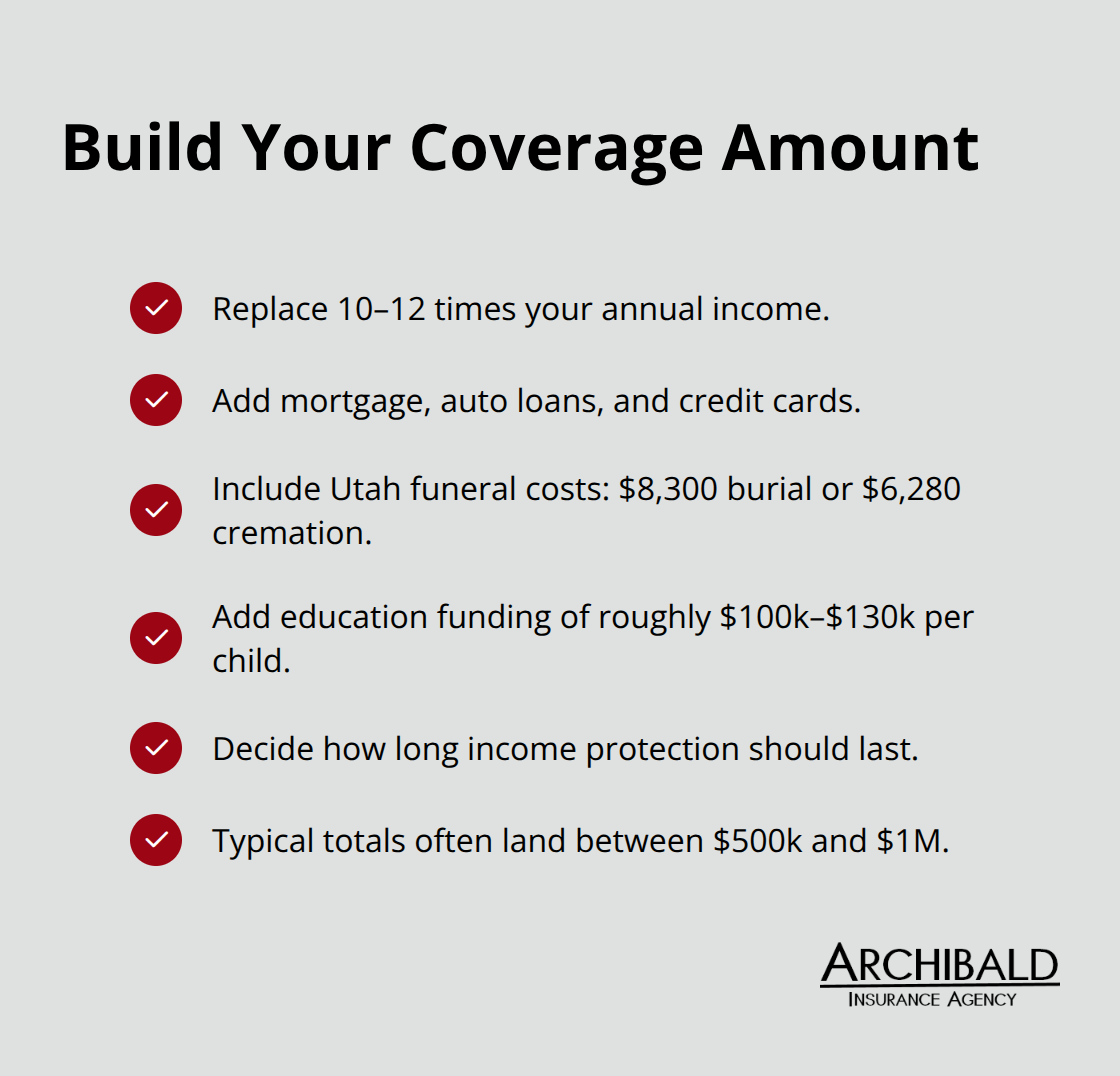

Figuring out your coverage amount stops most people cold, but the math is straightforward once you strip away the noise. Start with income replacement: aim for life insurance coverage equal to 10–12 times your annual income to provide your family with a comfortable financial cushion. This calculation protects your family’s standard of living without forcing them into financial hardship.

Account for Debts and Final Expenses

Add your outstanding debts-mortgage balance, car loans, credit cards-because your family shouldn’t inherit financial obligations alongside grief. Include final expenses; the average cost of a funeral is $8,300 for burial and $6,280 for cremation in Utah. These two categories often total $200,000 to $400,000 for Utah families, making them impossible to ignore when calculating your target coverage amount.

Factor in Education and Long-Term Goals

Include education funding if you have children; four years of in-state university costs roughly $100,000 to $130,000 today and will climb with inflation. Consider how long you want income protection to last-typically until your youngest child finishes college or until you reach retirement age. Most families discover they need $500,000 to $1,000,000 in coverage, though your specific number depends entirely on dependents, debt levels, and your timeline.

Get this number right before shopping for quotes, because it drives everything else.

Compare Quotes Using Identical Parameters

Once you know your target coverage amount, request quotes from at least three carriers using identical policy parameters so you compare apples to apples. Ask each carrier for a year-by-year illustration showing how cash value grows in permanent policies, since some policies accumulate value slowly in early years while others build faster-this detail matters when you evaluate whole life or universal life options.

Work with a Licensed Agent on Your Terms

Request the highest premium you might face if rates adjust, particularly with universal life policies, so you know the worst-case scenario and can budget accordingly. A licensed agent who listens to your situation rather than pushing you toward the highest commission product will serve your interests better. Your agent should take time to understand your family’s needs, income, debts, and long-term goals before recommending coverage, because the right policy is the one you’ll actually keep paying for and benefit from when it matters most.

Final Thoughts

Term, whole life, and universal life policies serve fundamentally different purposes. Term provides affordable temporary protection when you have dependents and financial obligations, making it ideal for younger families. Whole life builds permanent coverage with guaranteed cash value growth, suiting people who want lifelong protection and a savings component. Universal life offers flexibility between the two, allowing you to adjust premiums and death benefits as your circumstances change.

Understanding life insurance policies becomes straightforward once you focus on your actual needs instead of industry jargon. The right policy is the one you’ll afford and maintain for decades, not the one with the lowest initial quote or the most features you’ll never use. We at Archibald Insurance Agency believe that life insurance should protect your family’s financial future without creating stress in your present.

Our team represents multiple carriers, which means we can match you with coverage that fits your budget and goals rather than steering you toward a single company’s products. Whether you need term protection for the next 20 years or permanent coverage with cash value, we’ll walk you through your options and answer every question before you commit. Contact Archibald Insurance Agency in Salt Lake City to discuss your life insurance needs with an agent who listens.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation