Homeowners Insurance for Rental Property Owners

Owning rental property in Utah comes with unique insurance challenges that standard homeowners policies simply don’t address. Regular homeowners insurance for rental property falls short when protecting against tenant-related risks and lost rental income.

We at Archibald Insurance Agency see landlords make costly mistakes by assuming their existing coverage will protect their investment properties. The right rental property insurance protects both your physical investment and your income stream.

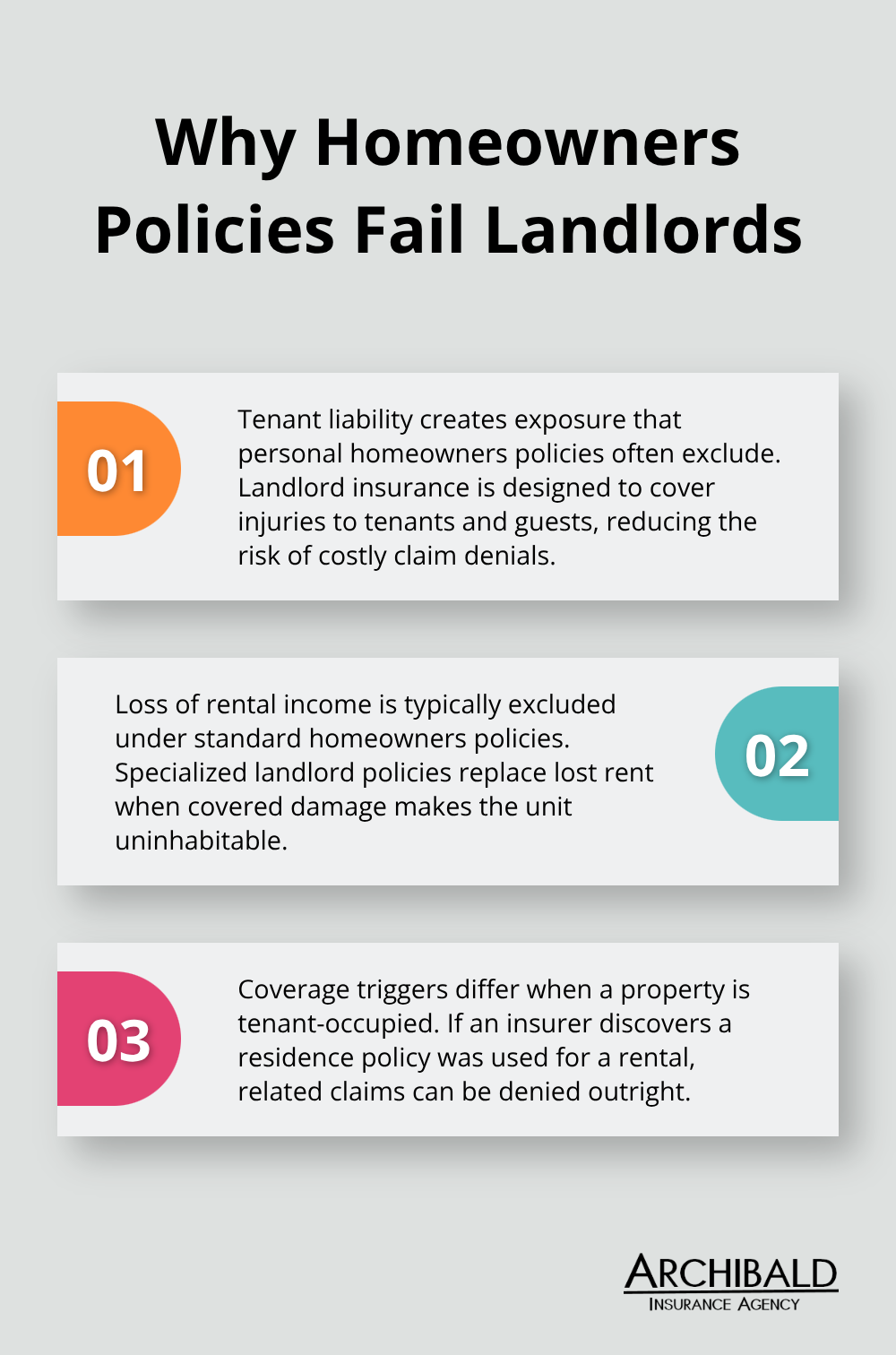

Why Standard Homeowners Insurance Fails Rental Property Owners

Standard homeowners insurance assumes you live in the property, which creates massive coverage gaps for rental properties. The Insurance Information Institute reports that property damage, including theft, accounted for 97.3 percent of homeowners insurance claims, highlighting the importance of proper coverage for tenant-related damages and rental income loss. Your homeowners insurer will deny claims if they discover you rent out a property covered under a personal residence policy.

Tenant Liability Exposes You to Higher Risks

Rental properties face higher insurance costs than owner-occupied homes due to increased liability risks. The average monthly cost increased from $39 per unit in 2019 to $68 per unit in 2024, an increase of more than 75 percent. Landlord insurance provides liability protection up to $1 million for tenant injuries on your property, while homeowners insurance may deny these claims entirely.

Loss of Rental Income Protection Matters

Loss of rental income coverage protects against disasters that make your property uninhabitable. Standard homeowners policies exclude this protection completely, which leaves you without income while you repair covered damage. This coverage becomes essential when considering the rising costs of property insurance and potential extended repair periods.

Property Damage Coverage Works Differently

Landlord insurance covers fire, wind, hail, vandalism, and theft specifically for rental properties, while homeowners insurance excludes coverage when tenants occupy the property. Your policy must include replacement cost coverage for the structure and any appliances you provide to tenants. Personal property coverage in landlord insurance protects maintenance equipment and appliances, not tenant belongings.

These specialized coverage differences become even more important when you consider the various types of protection available for rental insurance property.

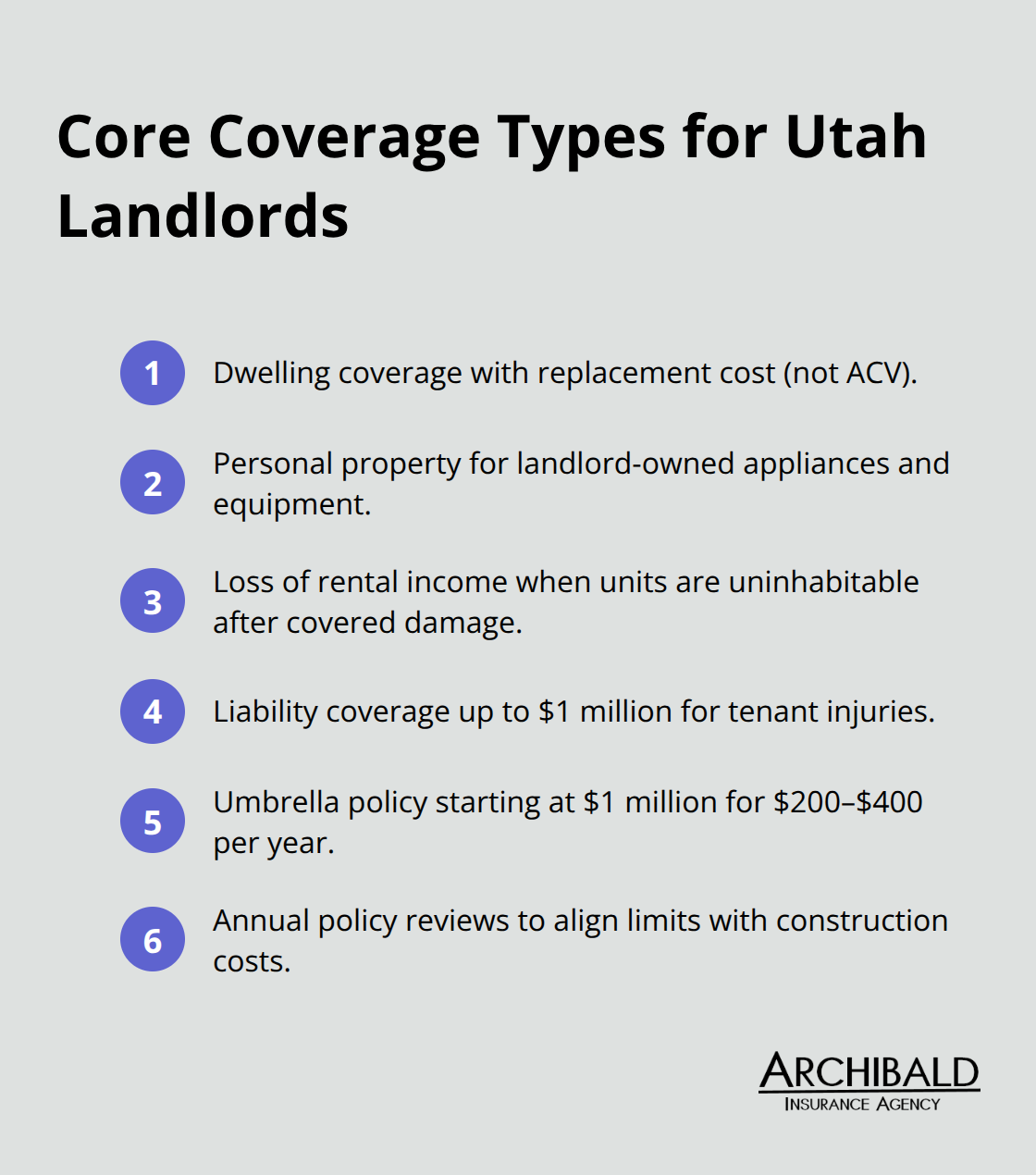

What Coverage Types Protect Rental Property Investments

Dwelling coverage forms the foundation of rental property insurance and protects the physical structure against fire, wind, hail, vandalism, and theft. The National Association of Insurance Commissioners recommends replacement cost coverage rather than actual cash value, which depreciates over time. Replacement cost coverage costs approximately 10% more but pays the full rebuilding cost without depreciation deductions.

Property owners should calculate dwelling coverage based on current construction costs, which have increased significantly nationwide in recent years according to federal data. We recommend annual policy reviews to adjust coverage limits as construction costs continue to rise.

Personal Property Protection for Landlords

Personal property coverage in landlord policies protects appliances, maintenance equipment, and fixtures you provide to tenants. This coverage typically ranges from $10,000 to $50,000 and includes refrigerators, washers, dryers, and lawn equipment stored on the property. Coverage excludes tenant belongings (which require separate renters insurance).

Appliance coverage becomes valuable when you consider that tenant-caused damages affect rental properties annually. Typical repair costs can be substantial per claim, making this protection essential for landlords who provide appliances.

Umbrella Insurance Adds Essential Protection

Umbrella insurance provides additional liability protection beyond standard landlord policy limits and typically starts at $1 million coverage for $200 to $400 annually. This coverage protects against lawsuits that exceed your base policy limits, which becomes essential when landlord claims frequently involve property damage and liability protection issues.

Umbrella policies also cover legal defense costs, which can reach $50,000 even for unsuccessful lawsuits. Property owners with multiple rentals or high-value properties should consider umbrella coverage mandatory protection against catastrophic liability claims (especially in today’s litigation-heavy environment).

These coverage types work together to protect your investment, but their costs vary significantly based on several key factors that affect your premium calculations.

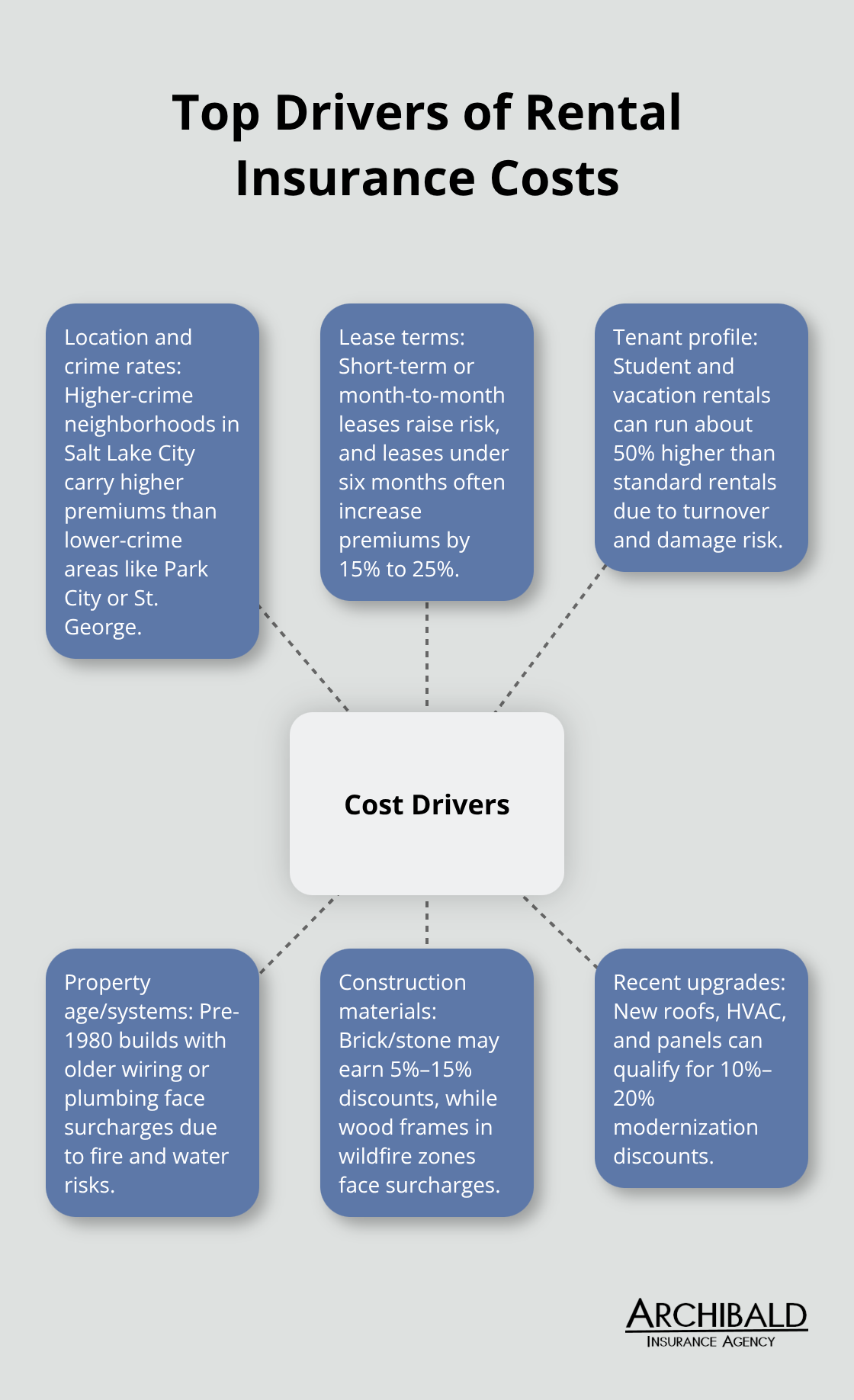

What Drives Your Rental Property Insurance Costs

Property location dominates insurance rates more than any other factor, with crime rates creating significant premium differences between neighborhoods. Utah properties in Salt Lake City’s higher-crime areas pay significantly more than those in Park City or St. George. High-crime areas can quickly increase insurance premiums, while living in low-crime areas helps keep costs manageable. Landlords should check local crime statistics before they purchase rental properties, as insurance costs can eliminate profit margins in high-risk locations.

Tenant Types and Lease Terms Impact Premiums

Insurance companies charge higher premiums for short-term rentals and month-to-month leases due to increased turnover risks. Properties with leases under six months face premium increases of 15% to 25% because frequent tenant changes create more liability exposure and property damage risks. Student rentals and vacation properties command the highest premiums (often 50% above standard rental rates). Long-term tenants with stable employment histories reduce insurance costs, while properties that require tenant background checks and security deposits qualify for discounts with many insurers.

Property Age and Materials Determine Base Rates

Properties built before 1980 face higher premiums due to outdated electrical, plumbing, and heating systems that increase fire and water damage risks. Older homes often have character but can result in higher insurance rates, as insurers view aging plumbing and wiring as risks. Construction materials significantly affect rates, with brick and stone structures that receive discounts of 5% to 15%, while wood frame construction in wildfire-prone areas faces surcharges. Properties with updated roofs, HVAC systems, and electrical panels within the last 10 years qualify for modernization discounts that can reduce premiums by 10% to 20% (making these upgrades financially worthwhile for most landlords).

Final Thoughts

Utah rental property owners require specialized coverage that standard homeowners insurance for rental property cannot provide. The increased liability risks and potential income loss make proper protection essential for investment success. Property owners who rely on basic homeowners policies expose themselves to significant financial risks.

Document your property value, monthly rental income, and local risk factors to establish appropriate coverage limits. Request quotes that include dwelling protection, liability coverage up to $1 million, and loss of rental income benefits. Multiple carriers offer different rates for identical properties, so comparison shopping saves money while maximizing protection.

We at Archibald Insurance Agency work with multiple insurance carriers to find solutions that match your specific needs and budget (our team understands Utah’s rental market challenges). Our Salt Lake City experts help landlords navigate coverage options that protect both property investments and income streams. Contact Archibald Insurance Agency today to review your rental property insurance requirements and secure comprehensive protection.