What Is Personal Liability in Homeowners Insurance?

Personal liability protection stands as one of the most important yet misunderstood components of your homeowners policy. This coverage protects you financially when someone gets injured on your property or when you accidentally cause damage to others.

At Archibald Insurance Agency, we see Utah homeowners overlook this protection until they face a costly lawsuit. Understanding homeowners insurance personal liability coverage can save you from devastating financial consequences.

How Does Personal Liability Coverage Actually Work?

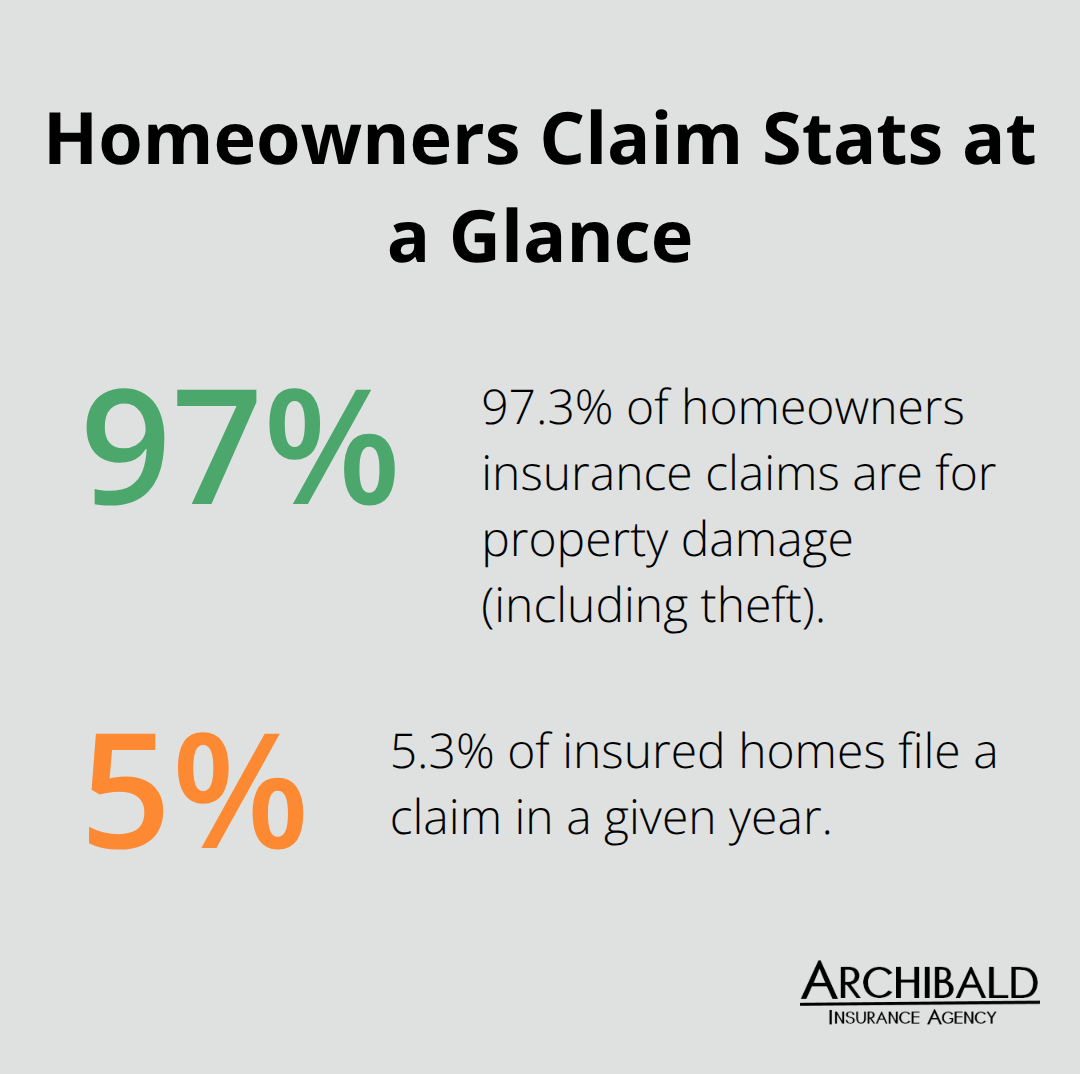

Personal liability coverage operates as Coverage E in your homeowners policy, typically starting at $100,000 but extending up to $500,000 or more based on your needs. Property damage claims, including theft, account for 97.3 percent of homeowners insurance claims, with only 5.3 percent of insured homes filing claims annually according to recent data. This coverage activates when you become legally responsible for bodily injury or property damage to others, whether the incident occurs on your property or away from home.

Standard Coverage Amounts in Utah

Most Utah homeowners policies include minimum personal liability limits of $100,000, though this amount falls short for many households. The National Association of Insurance Commissioners recommends coverage that matches or exceeds your net worth. If your assets total $150,000, select at least $300,000 in coverage. Utah homeowners with pools, trampolines, or frequent guests should consider $500,000 limits due to increased exposure risks.

What Personal Liability Covers

Your policy covers legal defense costs, medical expenses, and court judgments when accidents happen. Coverage extends to incidents like guests who fall on icy walkways, your child who accidentally breaks a neighbor’s window, or dog bite injuries that occur on your property. The policy also protects you when household members cause damage away from home (such as your teenager who accidentally damages school property).

Key Exclusions You Must Know

However, intentional damage, auto accidents, business activities, and injuries to household members remain excluded from coverage. Unintentional injuries represent a significant concern for property owners, highlighting why adequate protection remains essential. These exclusions mean you need separate auto insurance and business liability coverage to fill potential gaps.

Understanding these coverage details helps you evaluate whether your current limits provide sufficient protection, especially when you consider the various scenarios where liability claims commonly arise. For additional protection beyond standard homeowners insurance limits, consider an umbrella policy to safeguard your assets.

When Does Personal Liability Coverage Kick In?

Real-world liability scenarios happen more frequently than Utah homeowners expect, with unintentional injuries leading to significant emergency room visits annually. These incidents translate directly into potential liability claims against your homeowners policy.

Visitor Accidents on Your Property

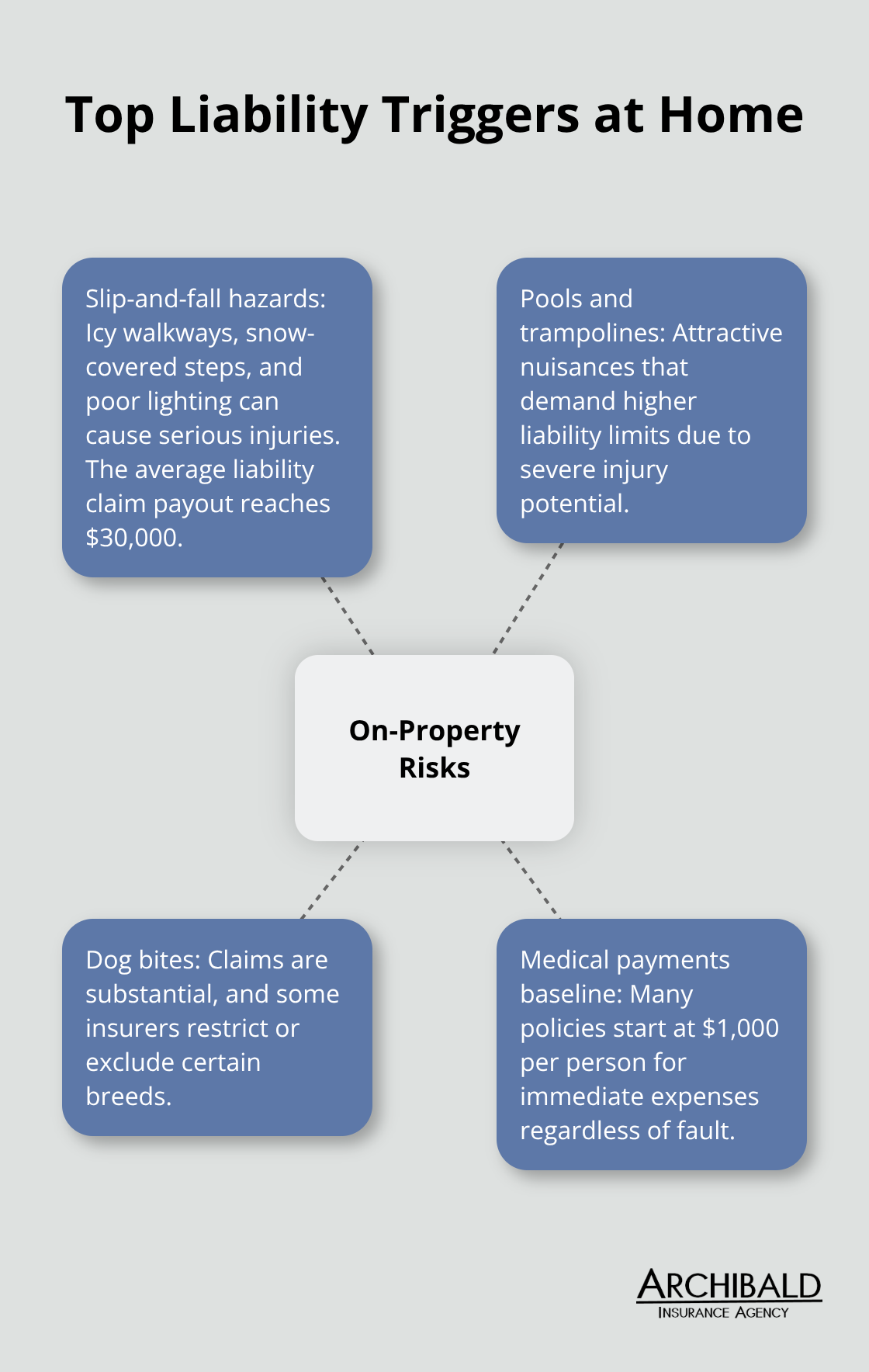

Slip and fall accidents represent the most common liability claims, with winter conditions in Utah creating heightened risks. Icy walkways, snow-covered steps, and inadequate lighting frequently lead to serious injuries. The Insurance Information Institute data shows the average liability claim payout reaches $30,000, making these incidents expensive for underinsured homeowners.

Swimming pools and trampolines increase your exposure significantly. Properties with these attractive nuisances require higher liability limits due to the severe injury potential. Dog bite claims account for substantial liability payouts, with certain breeds creating coverage restrictions from insurers (some companies exclude specific breeds entirely).

Utah homeowners must understand that medical payments coverage starts at $1,000 per person for immediate medical expenses, regardless of fault determination.

Away-From-Home Liability Risks

Your coverage follows you and household members beyond your property boundaries. Children who accidentally damage school property, family members who cause injury during recreational activities, or situations where you accidentally damage rental property all trigger your homeowners liability protection.

These off-premises incidents often surprise homeowners who assume coverage only applies to their property. Legal defense costs alone can exceed $10,000 even for unfounded claims (making adequate coverage limits essential for protecting your financial stability).

When Standard Limits Fall Short

The $100,000 minimum coverage that many Utah policies carry proves insufficient for serious accidents. Medical bills from severe injuries can reach six figures quickly, and legal settlements often exceed basic policy limits. This reality leads many homeowners to consider higher coverage amounts or umbrella insurance protection options.

How Much Coverage Do You Actually Need?

Standard Utah homeowners policies offer liability limits of $100,000, $300,000, and $500,000, but you must carefully consider your specific risk factors when you select the right amount. Personal liability claims represent a significant portion of homeowners insurance claims, with costs that can vary dramatically based on the severity of incidents. However, severe accidents can generate costs far above typical averages.

Standard Coverage Guidelines for Utah Homeowners

Utah homeowners with net worth of $200,000 should select minimum coverage of $300,000, while those with higher assets need proportionally more protection. Properties with pools, trampolines, or dogs create elevated risks that demand $500,000 limits or higher. The National Association of Insurance Commissioners emphasizes that you should match your coverage to your total assets plus potential future income.

When You Need Umbrella Protection

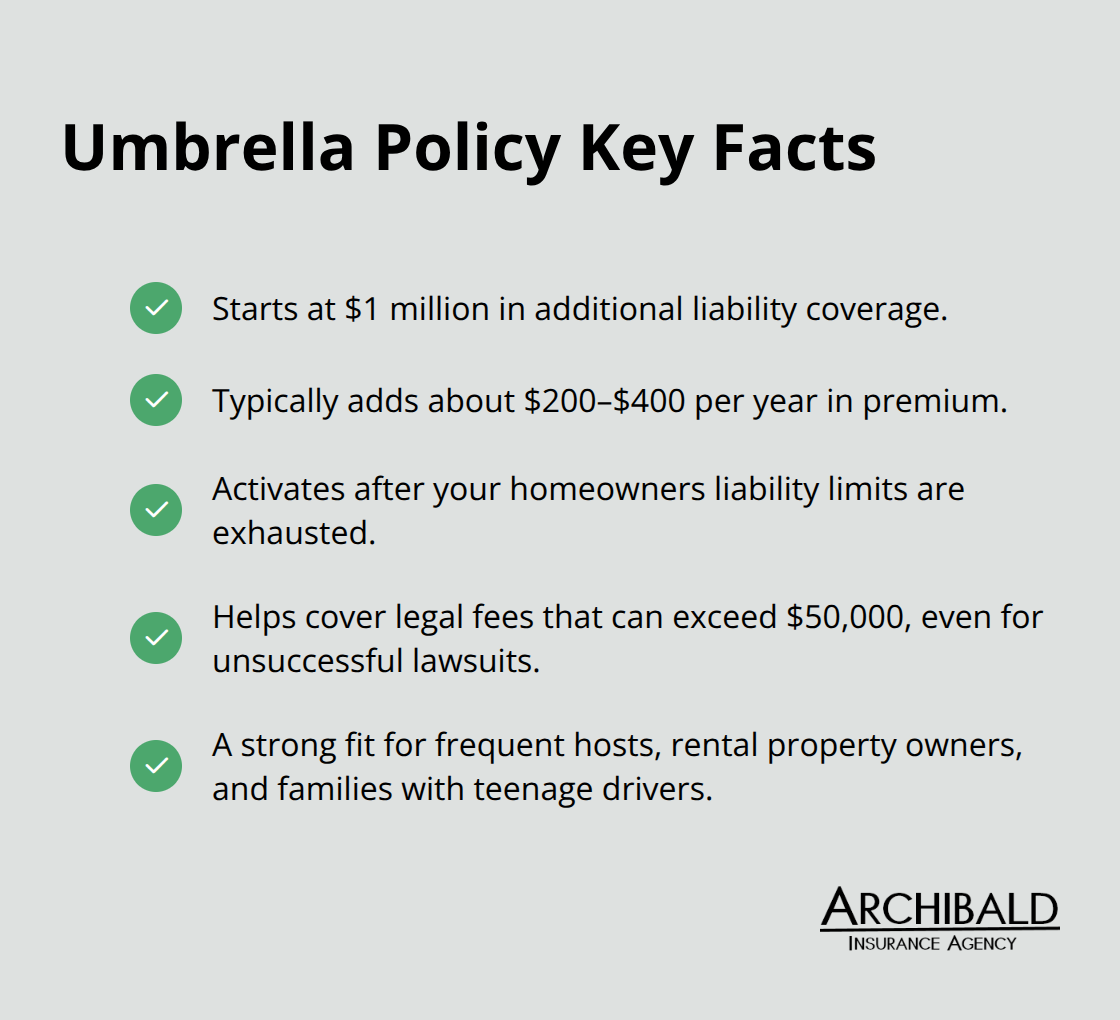

Umbrella policies provide additional liability coverage that starts at $1 million and extends beyond your homeowners policy limits for a relatively small premium increase of $200 to $400 annually. These policies activate when your base coverage reaches its limit and cover legal fees that can exceed $50,000 even for unsuccessful lawsuits. Utah homeowners who entertain frequently, own rental properties, or have teenage drivers should strongly consider umbrella coverage.

Risk Factors That Increase Your Coverage Needs

Your coverage needs depend on asset value, lifestyle factors, and property characteristics rather than generic recommendations. Homeowners with pools face claim frequencies three times higher than those without pools (according to insurance industry data). Dog ownership increases liability exposure significantly, with breed restrictions that affect coverage availability from certain insurers. Regular parties, home-based businesses, or teenage family members all elevate your risk profile and coverage requirements. Proper home maintenance also plays a role in reducing potential liability risks.

Final Thoughts

Personal liability coverage protects your financial future when accidents happen and offers legal defense, medical expense coverage, and settlement protection that can save you from bankruptcy. The average liability claim payout of $30,000 demonstrates why this protection remains essential for Utah homeowners, yet many carry insufficient coverage limits that leave them exposed to devastating financial losses. Regular coverage reviews become necessary as your assets grow, family circumstances change, or property modifications increase your risk exposure.

Life events like pool purchases, rental property acquisitions, or teenage drivers all demand coverage adjustments to maintain adequate protection levels. When you evaluate your homeowners insurance personal liability needs, start by calculating your net worth and select coverage that exceeds this amount. Consider umbrella policies for additional protection beyond standard limits, especially if you own high-risk property features or entertain frequently.

We at Archibald Insurance Agency help Utah families navigate these coverage decisions with personalized solutions from multiple carriers (our independent agency approach means we can compare options and find the right protection for your specific situation and budget). Contact us today to review your current coverage and protect your assets with appropriate liability limits. We build relationships based on trust and reliability within our local community.