Does Homeowners Insurance Cover HVAC Systems?

Your HVAC system represents one of the largest investments in your Utah home, often costing $5,000 to $15,000 to replace. When it breaks down, the question “does homeowners insurance cover HVAC” becomes urgent.

We at Archibald Insurance Agency see this confusion daily among Utah homeowners. The answer depends on what caused the damage and how well you’ve maintained your system.

When Does Homeowners Insurance Cover HVAC Damage

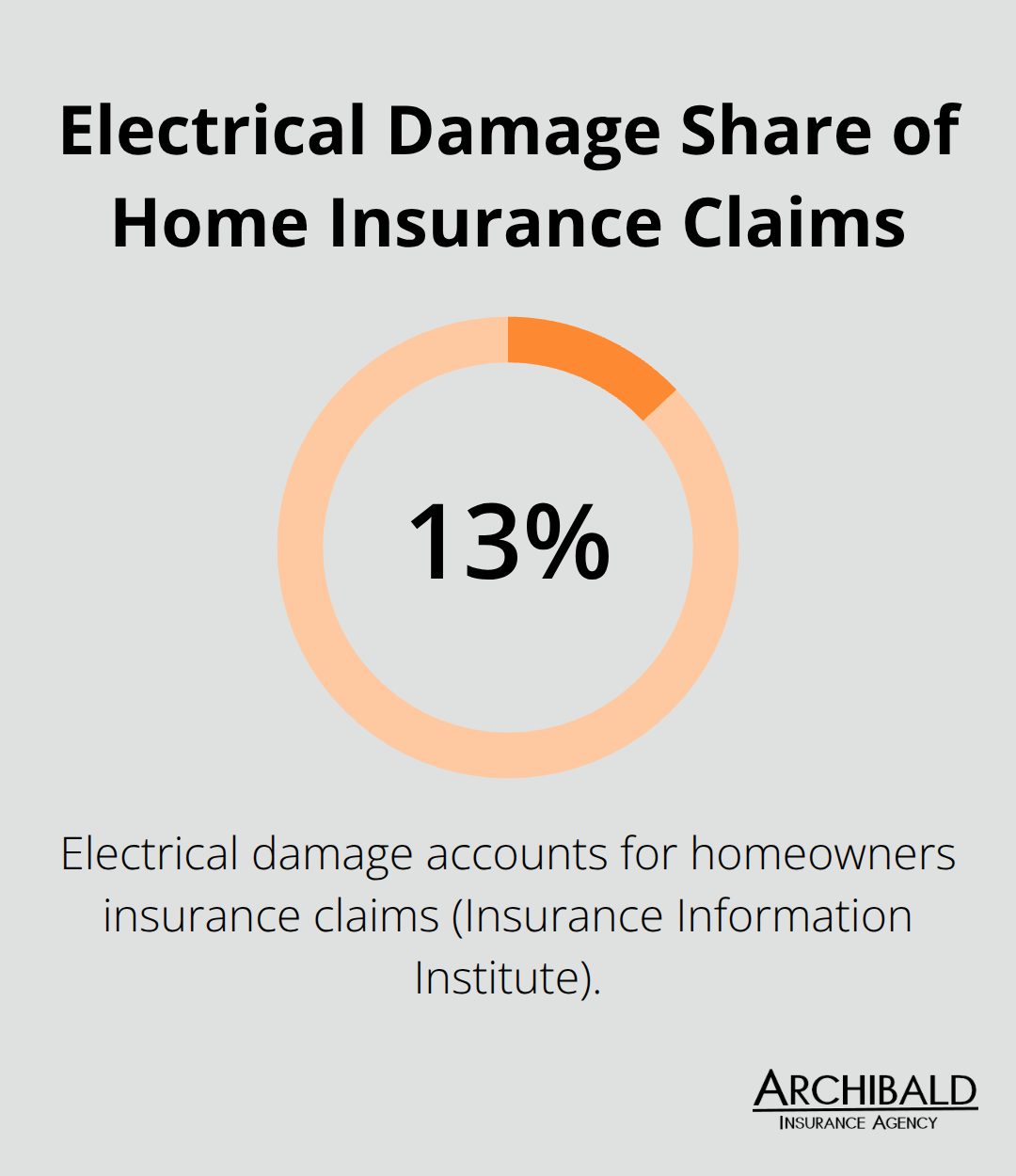

Standard homeowners insurance policies protect your HVAC system against specific types of damage, but the coverage is narrower than most Utah homeowners expect. Your policy will typically cover sudden mechanical breakdowns that electrical surges, lightning strikes, or power outages cause to your system’s components. The Insurance Information Institute reports that electrical damage accounts for roughly 13% of all homeowners insurance claims, which makes surge protection a valuable benefit.

Weather-related damage from hail, windstorms, or fallen trees also falls under dwelling coverage, provided the damage happens suddenly rather than gradually.

Electrical and Mechanical Failures

Power surges from lightning or utility company issues can destroy your HVAC system’s control boards, motors, and compressors instantly. These sudden failures cost Utah homeowners an average of $2,500 to $4,500 to repair according to local HVAC contractors. Your insurance will cover these repairs minus your deductible, but you must prove the damage occurred suddenly. Keep your electrical panel updated and document any power issues in your neighborhood to support potential claims.

Storm and Weather Protection

Utah’s severe weather poses real threats to outdoor HVAC units. Hail damage to condenser coils and fan motors receives coverage under your dwelling or personal property protection. Wind damage from storms that blow debris into your unit also qualifies for coverage. The National Weather Service maintains detailed records of severe weather events through their Storm Events Database, which makes this coverage especially relevant for local homeowners.

Theft and Vandalism Coverage

HVAC theft has increased nationwide due to rising copper prices. Your homeowners policy covers stolen outdoor units, copper coils, and damaged ductwork from break-ins. File police reports immediately and photograph all damage to speed up your claim process. Most Utah insurers require proof of forced entry to approve theft claims for HVAC components. For contractors and businesses, specialized HVAC insurance provides additional protection beyond standard policies.

However, these coverage scenarios represent only part of the story. Many common HVAC problems fall outside standard policy protection, which creates gaps that catch homeowners off guard.

When Homeowners Insurance Won’t Cover HVAC Repairs

Your homeowners insurance policy contains specific exclusions that leave Utah homeowners exposed to thousands of dollars in HVAC repair costs. The most expensive exclusion involves normal wear and tear, which accounts for the majority of HVAC failures. Components like compressors, heat exchangers, and blower motors naturally deteriorate over their 15 to 20-year lifespan, and your insurance policy explicitly excludes these gradual failures. Utah’s extreme temperature swings from subzero winters to 100-degree summers accelerate this wear, which makes these exclusions particularly costly for local homeowners.

Normal Wear and Tear Exclusions

Insurance companies refuse to cover components that fail through normal use. Your compressor will eventually wear out after years of operation, and your heat exchanger will develop cracks from repeated heating cycles. These failures cost $3,000 to $5,000 to repair but receive zero coverage under standard policies. The Insurance Information Institute classifies wear and tear as common exclusions rather than insurable events. Utah homeowners face higher replacement costs due to elevation changes that stress HVAC systems beyond their design limits.

Maintenance-Related Failures Cost You Everything

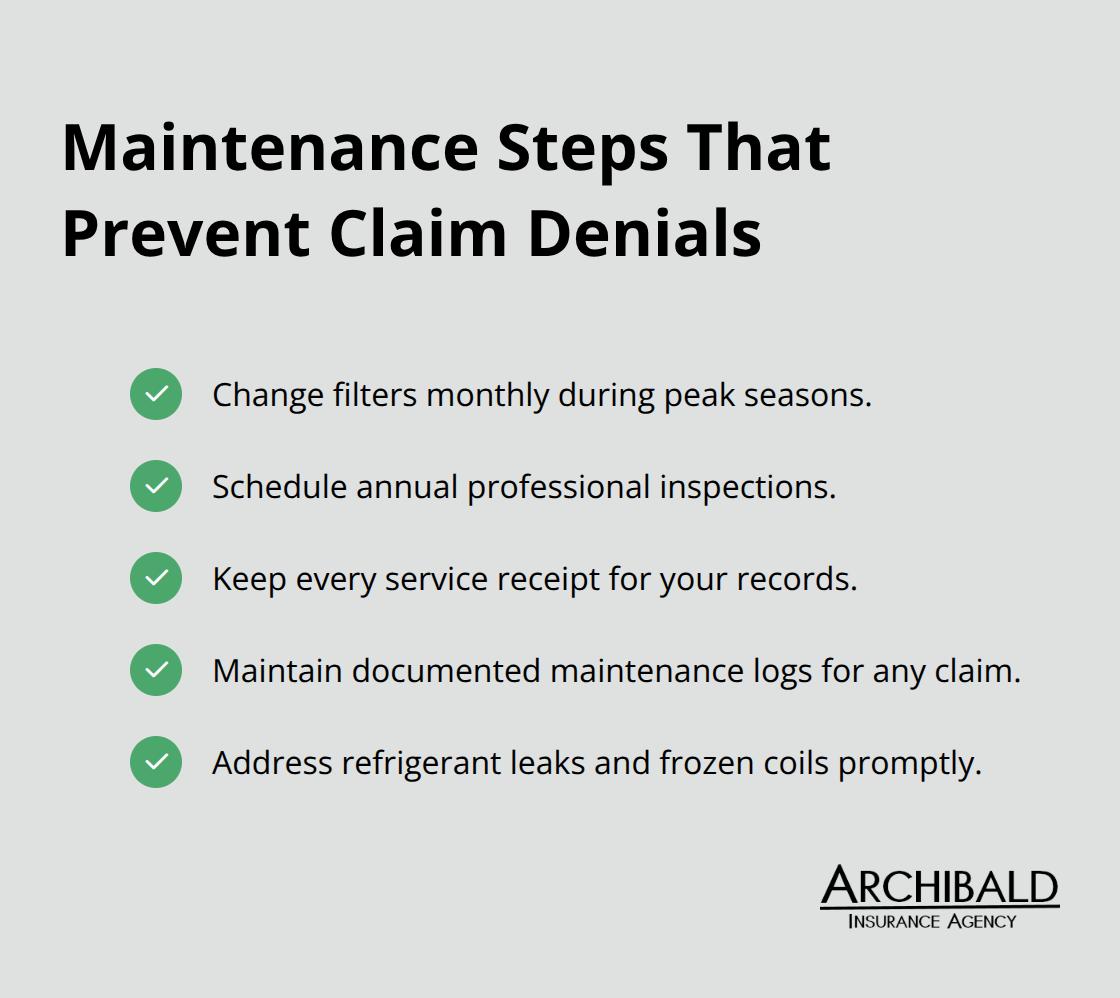

Insurance companies deny claims when poor maintenance causes HVAC damage. Dirty air filters restrict airflow and cause compressor burnout (costing $3,000 to $5,000 to replace). Skipped annual tune-ups lead to refrigerant leaks, frozen coils, and electrical failures that policies won’t cover. Insurers require documented maintenance records for any HVAC claim approval. Change filters monthly during peak seasons, schedule annual professional inspections, and keep every service receipt. Without this documentation, your insurer will classify expensive repairs as maintenance-related and deny coverage entirely.

Pre-Existing Problems Void Your Coverage

Insurance policies exclude damage from pre-existing conditions that existed before your coverage began. HVAC systems with existing problems like refrigerant leaks, failing capacitors, or worn ductwork receive no protection under new policies. Most insurers require HVAC inspections for homes over 20 years old specifically to identify these exclusions. Age-related deterioration in older systems creates ongoing liability that insurance companies refuse to accept.

Understanding these exclusions helps you prepare for the gaps in your coverage and explore additional protection options that can shield you from unexpected repair costs.

How to Maximize Your HVAC Coverage in Utah

Utah homeowners who document every HVAC maintenance activity create strong insurance claims that adjusters approve quickly. Keep detailed service records that include filter change dates, refrigerant level checks, and annual tune-up reports from licensed contractors. Documenting routine HVAC maintenance is crucial for both insurance claims and risk management to distinguish between covered sudden failures and excluded maintenance issues. Your maintenance log should record specific work performed, parts replaced, and contractor license numbers. Take photographs of your HVAC system before and after service calls to establish baseline conditions. Schedule professional inspections every spring and fall, because Utah’s extreme temperature swings stress systems beyond manufacturer specifications.

Document Everything for Claim Success

Your insurance company will scrutinize every detail when it processes HVAC claims worth thousands of dollars. Create a dedicated file that contains purchase receipts, warranty information, and every service invoice since installation. Digital photos of your system taken quarterly help establish pre-loss conditions that adjusters need for accurate damage assessments. Most Utah insurers accept claims faster when homeowners provide this comprehensive documentation package immediately after damage occurs.

Know Your Policy Limits Before You Need Them

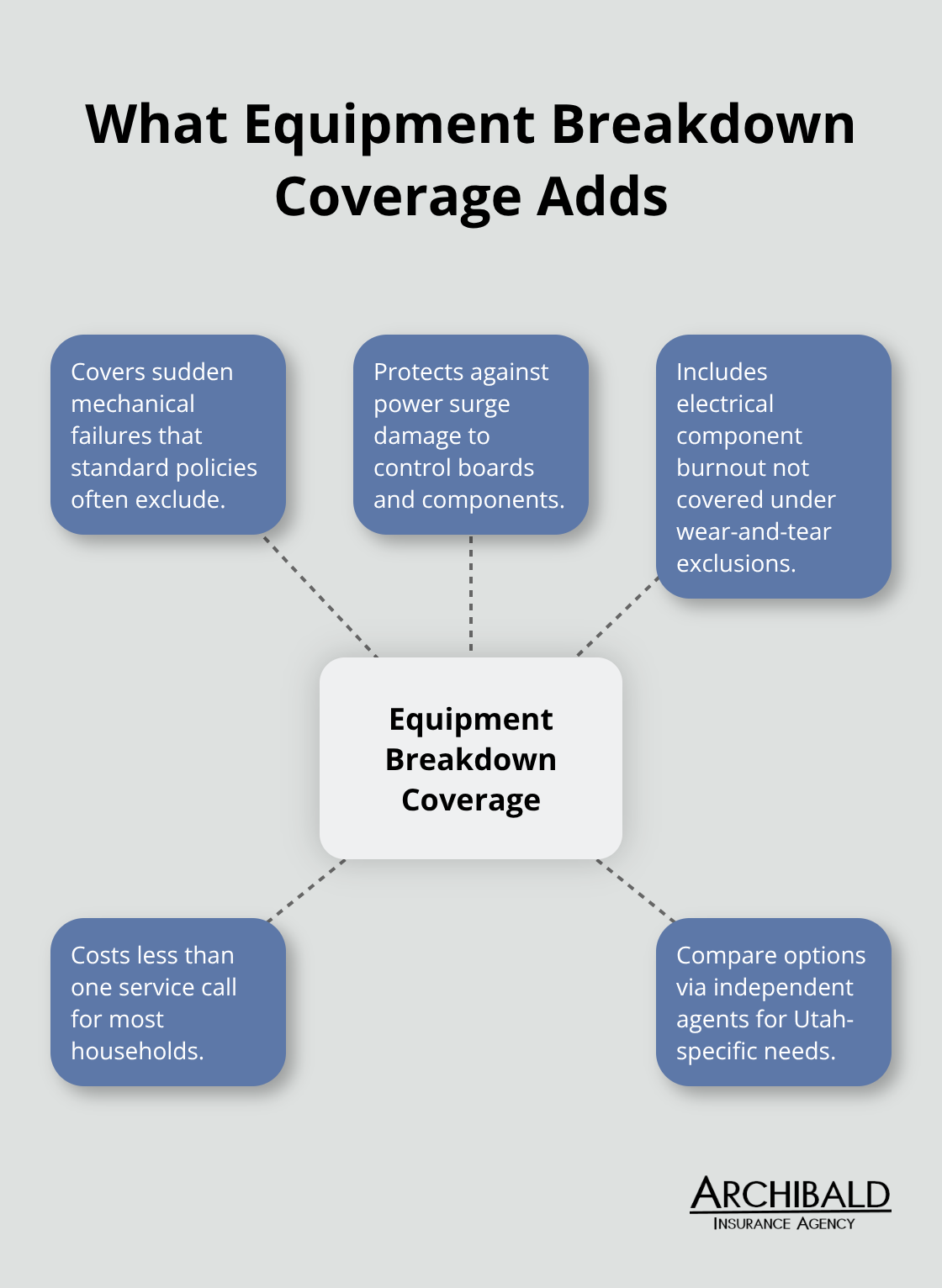

Standard Utah homeowners policies cap HVAC coverage between $5,000 and $25,000 (depending on your dwelling coverage limits). Equipment breakdown coverage provides additional protection for mechanical failures that basic policies exclude. These endorsements cost $50 to $150 annually but cover expensive compressor replacements and control system failures that normal wear exclusions would deny. Review your deductible amounts because $2,500 deductibles make small HVAC repairs financially worthless to claim.

Add Equipment Breakdown Protection Now

Equipment breakdown coverage transforms your policy from basic protection into comprehensive HVAC insurance that covers sudden mechanical failures, power surge damage, and electrical component burnout. This endorsement costs less than one service call but covers repairs that standard policies reject. Contact independent agents who represent multiple carriers to compare equipment breakdown options that fit Utah climate conditions and your specific HVAC system requirements (many agents can quote multiple options within hours).

Final Thoughts

The question “does homeowners insurance cover HVAC” has a complex answer that depends on the cause of damage and your maintenance history. Standard policies protect against sudden electrical failures, storm damage, and theft but exclude normal wear and tear that causes most HVAC problems. Utah homeowners face higher risks due to extreme temperature swings that stress systems beyond typical limits.

Equipment breakdown coverage fills the gaps that standard policies leave open. This endorsement costs $50 to $150 annually but covers mechanical failures worth thousands of dollars (often exceeding $5,000 for major component replacements). Document every maintenance activity with receipts and photos to support future claims.

Contact your insurance agent immediately after any HVAC damage occurs. Review your policy limits annually because standard coverage caps may not cover full replacement costs for newer high-efficiency systems. We at Archibald Insurance Agency help Utah homeowners compare coverage options from multiple carriers to find comprehensive protection.