Your homeowners insurance policy should fully protect your home if disaster strikes. At Archibald Insurance Agency, we see too many Utah homeowners underestimate what it actually costs to rebuild.

Replacement value for homeowners insurance is the amount your insurer will pay to reconstruct your home with new materials at current prices. Understanding this concept is the difference between recovering fully after a loss and facing a financial gap you didn’t expect.

What Replacement Value Actually Means

Replacement value is straightforward: it’s what your insurer pays to rebuild your home with new materials at today’s prices, without deducting depreciation. This differs fundamentally from actual cash value, which reduces your payout based on how old your home and belongings are. With replacement cost coverage on your dwelling, a $10,000 damage claim pays $10,000 minus your deductible to repair or rebuild. With actual cash value, that same $10,000 in damage might only pay $6,000 or $7,000 after depreciation is factored in, leaving you to cover the gap yourself. The National Association of Insurance Commissioners reports this difference can be substantial depending on your home’s age and condition. Most standard homeowners policies cover the dwelling at replacement cost, but personal property inside often defaults to actual cash value unless you upgrade. This creates a critical gap many Utah homeowners don’t realize until they file a claim.

Why Replacement Cost Reflects Reality

Insurers use replacement cost as the standard for dwellings because it reflects reality: rebuilding costs actual money at current prices. If you suffer a total loss, you need funds to hire contractors, purchase materials, and bring everything up to current building codes. Actual cash value doesn’t accomplish this. A 20-year-old roof might be worth only $3,000 on the depreciation scale, but replacing it today costs $8,000 to $12,000 depending on materials and complexity. When you face reconstruction after a fire or major damage, depreciation math doesn’t pay your contractor. Utah’s real estate market and construction costs have climbed steadily, making replacement cost estimates critical to adequate coverage limits.

How Construction Costs Shape Your Coverage Needs

The National Association of Home Builders estimated construction costs at approximately $166 per square foot in 2025, though Utah’s costs vary by region and home type. A 2,500-square-foot home would cost roughly $415,000 to rebuild at that rate before accounting for site-specific factors (foundation type, materials, and local labor rates). Many homeowners base coverage limits on their home’s market value instead, which is a costly mistake. Market value includes land and reflects what a buyer would pay today; replacement cost ignores land and focuses purely on reconstruction expense. Your $600,000 home might cost only $450,000 to rebuild, or it might cost $500,000 depending on construction complexity and local conditions. Getting this right prevents underinsurance, which leaves you personally responsible for costs your policy doesn’t cover.

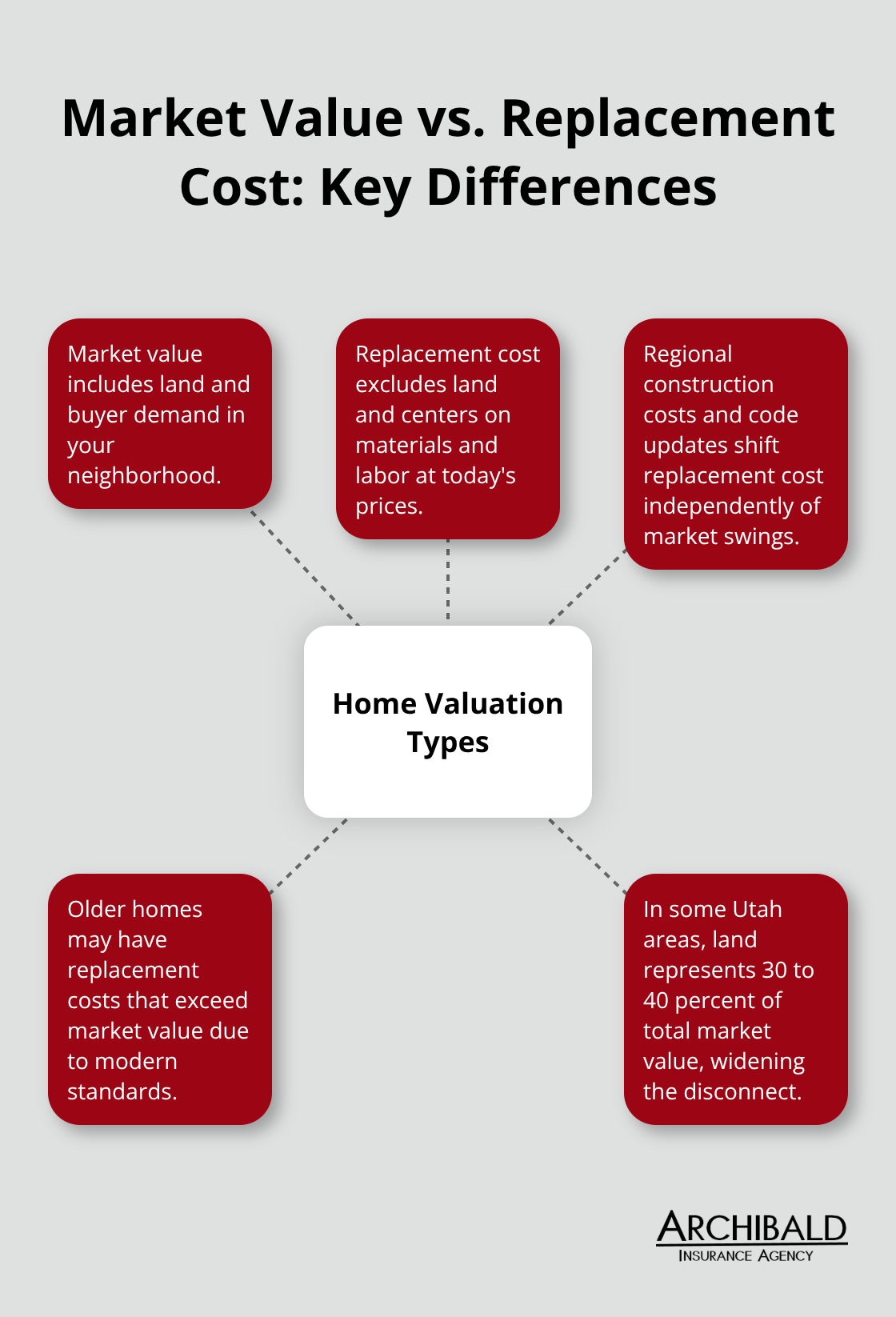

The Gap Between Market Value and Reconstruction Expense

Market value and replacement cost operate on completely different principles. A property’s market value includes the land beneath your home, current real estate trends, and what buyers will pay in your neighborhood. Replacement cost strips away land value and focuses only on what it takes to reconstruct the structure itself.

In some Utah markets, land represents 30 to 40 percent of your home’s total market value, meaning your replacement cost could be significantly lower than what your home would sell for. In other cases, older homes with valuable land might have replacement costs that exceed their market value due to modern construction standards and material expenses. This mismatch explains why many homeowners carry insufficient coverage-they anchor their limits to what their home is worth on the market rather than what it costs to rebuild. Your next step involves calculating your actual replacement cost with precision, which requires understanding the specific factors that drive up or down your reconstruction expense.

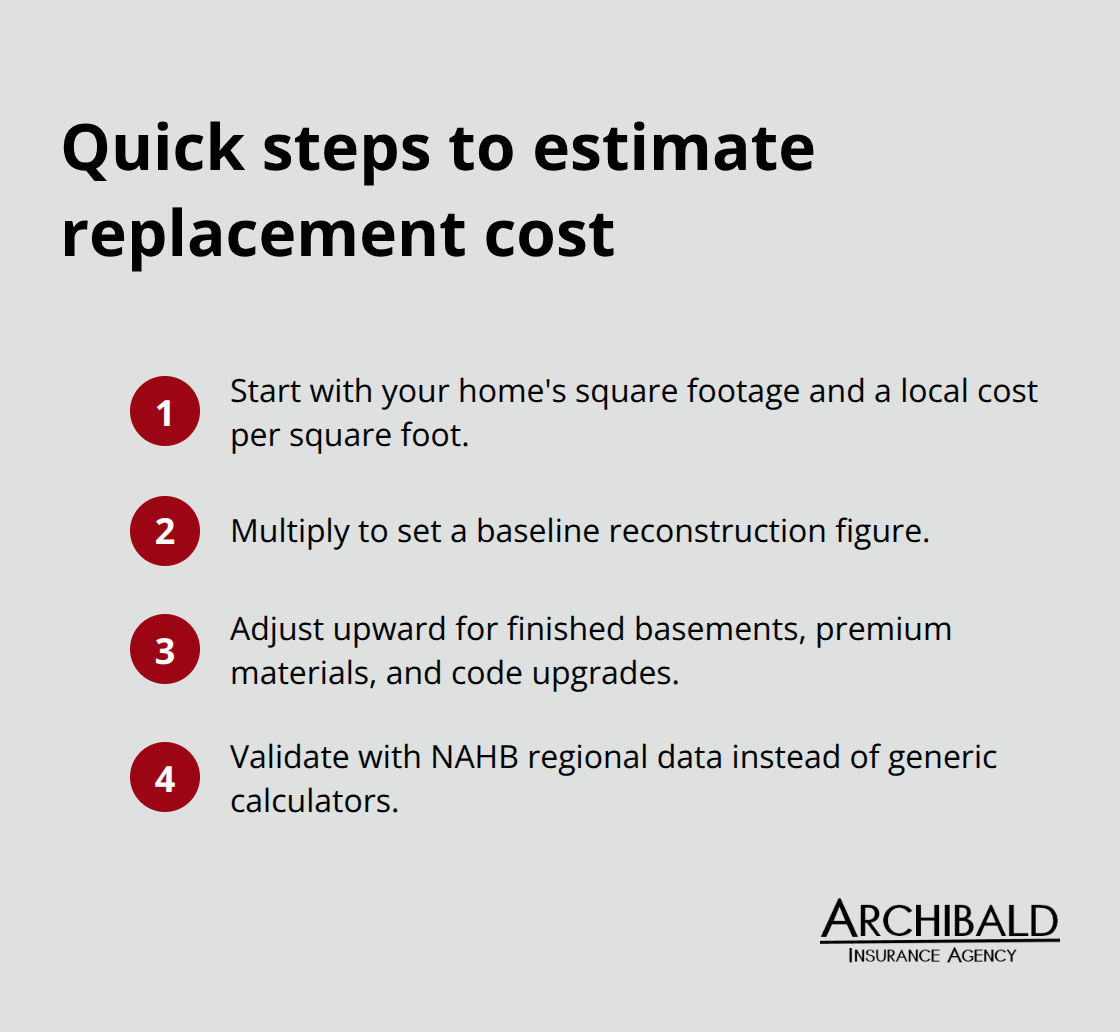

How to Calculate Your Home’s Replacement Value Accurately

The single biggest mistake Utah homeowners make is using their home’s market value as a proxy for replacement cost. Your $500,000 home might cost only $380,000 to rebuild, or it might cost $520,000-market value tells you nothing about actual reconstruction expense. Start with square footage and local construction costs. The National Association of Home Builders data from 2025 shows construction at roughly $166 per square foot nationally, but Utah varies significantly by county and home type. A 2,500-square-foot home in Salt Lake City will cost less to rebuild than an equivalent home in Park City, where labor and material costs run higher.

Multiply your square footage by your local cost per square foot as a rough baseline, then adjust upward for factors that increase complexity: finished basements add 15 to 25 percent to costs, high-end materials and custom finishes push costs higher, and older homes requiring code compliance upgrades during reconstruction often exceed simple square-footage math. The National Association of Home Builders provides regional cost data that beats generic online calculators, which frequently underestimate Utah properties.

Why Professional Appraisers Get Numbers Right

A contractor’s estimate or replacement cost calculator used by a licensed appraiser beats guesswork every single time. These professionals account for your specific home’s foundation type (slab versus basement), roof pitch and material, electrical and plumbing systems, and local permit requirements that affect final cost. Many homeowners skip this step and regret it during claims. When you work with an independent insurance agent-someone who represents multiple carriers rather than just one company-that agent can often connect you with appraisers who specialize in replacement cost calculations for insurance purposes. This differs from a real estate appraisal done for mortgage purposes; insurance appraisals focus purely on reconstruction expense. The cost of a professional replacement cost appraisal typically ranges from $300 to $600 and pays for itself many times over if it prevents underinsurance. Your lender likely requires dwelling coverage at least 80 percent of replacement cost anyway, which means you need an accurate number to satisfy that requirement and protect yourself.

Common Mistakes That Leave You Exposed

Homeowners frequently anchor their coverage limits to what they paid for the home years ago, ignoring that construction costs have climbed steadily. If you bought your home in 2015 for $350,000, that doesn’t mean it costs $350,000 to rebuild today-costs have risen substantially. Another trap involves ignoring recent renovations when updating coverage.

You added a $75,000 kitchen remodel and a new master suite last year, but you didn’t increase your dwelling limit to reflect that improvement. Your policy still shows the old limit, leaving you underinsured for the value you actually own. Some homeowners also fail to account for inflation guard endorsements, which automatically increase coverage limits annually. Without inflation protection, your limits fall further behind rising costs each year, and by the time you file a claim five years later, you’re significantly underinsured. The fix is straightforward: have a professional calculate your replacement cost now, review it every two to three years or after any major renovation, and ensure your dwelling limit matches that number. This precision in your coverage limits determines whether you recover fully or face a financial shortfall when disaster strikes-which is exactly why the next section examines what those coverage limits actually mean when you file a claim.

How Replacement Value Protects Your Finances

Your dwelling coverage limit is the maximum your insurer will pay to rebuild your home after a covered loss. This number must align precisely with your replacement cost, not fall short of it. If your home costs $420,000 to rebuild and your dwelling limit is only $380,000, you face a $40,000 gap your insurance won’t cover-that gap comes directly from your pocket.

The deductible reduces your payout regardless of coverage type, so a $1,000 deductible on a $10,000 claim means your insurer pays $9,000 maximum. Utah lenders require dwelling coverage at least 80 percent of replacement cost before they’ll approve a mortgage, which means most homeowners already know they need substantial limits. The problem is that many set limits based on outdated appraisals or market value rather than current reconstruction costs.

What Happens When You File a Claim

When you file a claim, your insurer hires an adjuster who calculates actual repair or replacement costs. If those costs exceed your limit, you absorb the overage-this isn’t negotiable or flexible. The adjuster’s job is to verify your claim meets policy terms and that repairs fall within your coverage limit, not to advocate for paying you more than your limit allows.

Real Utah Homeowners and Their Coverage Outcomes

A Salt Lake City homeowner with a $380,000 dwelling limit suffered a kitchen fire in 2024 that destroyed cabinets, appliances, flooring, and walls. The adjuster’s repair estimate came to $45,000. The homeowner’s $1,000 deductible reduced the payout to $44,000, which the insurer paid in full because it stayed within the dwelling limit.

A second homeowner in Park City faced a roof failure that caused water damage throughout a 3,200-square-foot home. Repairs totaled $78,000. His dwelling limit was $520,000, so the insurer paid $77,000 after the deductible. Both recovered fully because their limits matched or exceeded actual reconstruction costs.

A third homeowner in Ogden had a $350,000 dwelling limit when her home cost $425,000 to rebuild according to a professional appraisal. After a significant fire, reconstruction estimates reached $185,000. She received $184,000 after her deductible, which covered only about half the actual rebuilding needed. She faced a $91,000 shortfall because her coverage limit was too low.

The Cost of Being Underinsured

Being underinsured in Utah’s current market creates genuine hardship. Construction costs have climbed steadily, and if your coverage limits haven’t kept pace, you’ll discover this gap precisely when you need the money most. The solution is straightforward: obtain a current replacement cost calculation, ensure your dwelling limit matches that number, and review it every two to three years to account for inflation and construction cost increases.

An independent insurance agent can help you navigate this process and connect you with professionals who calculate replacement costs accurately for insurance purposes. This precision in your coverage limits determines whether you recover fully or face a financial shortfall when disaster strikes.

Final Thoughts

Replacement value for homeowners insurance forms the foundation of genuine financial protection. Your dwelling limit must match what it actually costs to rebuild your home with new materials at current prices, not what your home would sell for or what you paid for it years ago. This alignment between your coverage limit and your replacement cost prevents the financial gaps that leave homeowners scrambling after a loss.

Pull out your current homeowners policy and check your dwelling limit on the declarations page. Compare that number to a professional replacement cost calculation for your home ($300 to $600 for an accurate appraisal pays for itself many times over by preventing underinsurance). After you have that number, review your policy every two to three years or whenever you complete a major renovation, since construction costs climb steadily and inflation guard endorsements help but don’t eliminate the need for periodic review.

At Archibald Insurance Agency, we represent multiple carriers rather than pushing one company’s products, which means we can find coverage that matches your specific replacement value for homeowners insurance needs and budget. When you’re ready to review your replacement value coverage or discuss whether your current limits are adequate, reach out to Archibald Insurance Agency in Salt Lake City.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation

Getting involved in a car accident can be an incredibly distressing experience. However, being prepared and knowing how to handle the situation can help you navigate the shock and ensure that you have the necessary documentation to support your claim. While accidents can happen to any driver, whether their vehicle is parked or in motion, understanding and following these essential steps will assist you in dealing with such an unfortunate event.

Getting involved in a car accident can be an incredibly distressing experience. However, being prepared and knowing how to handle the situation can help you navigate the shock and ensure that you have the necessary documentation to support your claim. While accidents can happen to any driver, whether their vehicle is parked or in motion, understanding and following these essential steps will assist you in dealing with such an unfortunate event.