How to Calculate Homeowners Insurance Cost

Homeowners insurance costs vary dramatically based on where you live, what your home is worth, and the coverage you choose. Understanding what goes into these calculations helps you make smarter decisions about your policy.

At Archibald Insurance Agency, we work with Utah homeowners every day who want to know exactly how to calculate homeowners insurance costs and find ways to pay less. This guide walks you through the factors that matter most and shows you concrete steps to lower your premium.

What Drives Your Homeowners Insurance Premium

Location Creates the Biggest Price Differences

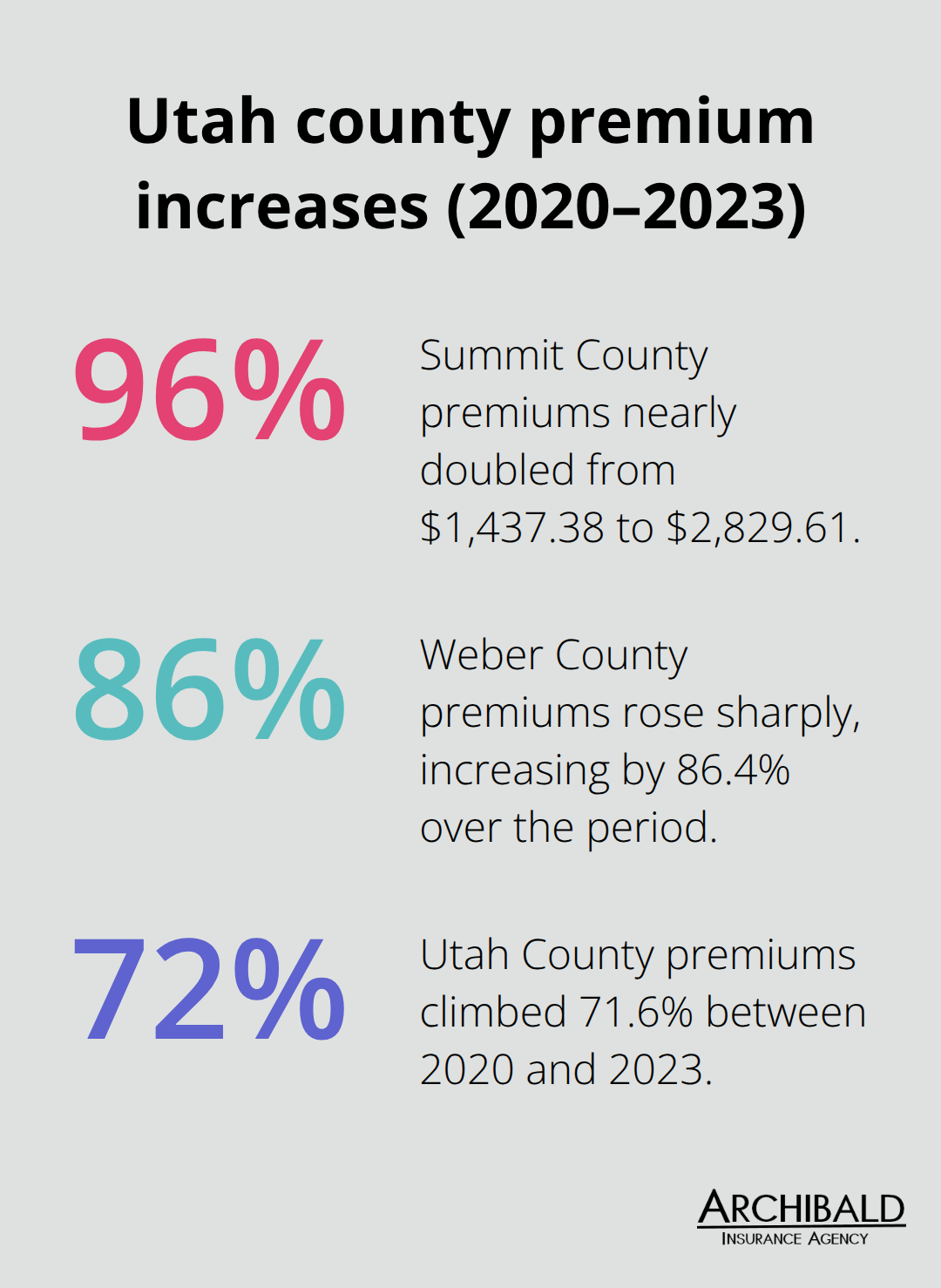

Your location in Utah has the single biggest impact on what you pay for homeowners insurance, and the numbers prove it. Salt Lake County median premiums jumped from $1,045.42 in 2020 to $1,578.57 in 2023, a 51% increase. Summit County saw premiums nearly double from $1,437.38 to $2,829.61 over the same period-a 96.8% jump. Weber County hit an 86.4% increase, while Utah County climbed 71.6%.

Your ZIP code matters because it reflects local disaster history, fire department proximity, and property values in your area. Even within Utah’s more affordable pricing compared to the national average, where you live determines whether you pay $1,272 or well over $6,548 annually. Provo averages about $97 per month, while West Valley City runs closer to $100 per month. These differences stem from how often claims happen in your neighborhood, how quickly emergency services respond, and the cost to rebuild homes in your specific area.

Replacement Cost Sets Your Coverage Foundation

Your home’s replacement cost-not its market value-is what insurers use to calculate your dwelling coverage and your premium. Multiply your square footage by replacement cost per square foot to get an accurate dwelling coverage amount. If you own a 3,000 square foot home in an area where rebuilding costs $180 per square foot, you need $540,000 in dwelling coverage. Underestimating this number is a costly mistake because you’ll face a gap when you file a claim.

Personal Property and Deductible Choices Impact Your Total Cost

Personal property coverage should typically be 50% to 75% of your dwelling coverage, so higher home values automatically push up your total premium. Your deductible choice directly affects what you pay each month. Jumping from a $1,000 deductible to a $5,000 deductible can lower your annual premium significantly, but only if you have emergency funds available to cover that higher out-of-pocket cost when you file a claim. The trade-off between monthly savings and out-of-pocket risk matters more than most homeowners realize, and it shapes how insurance companies calculate your rate.

How Insurance Companies Price Your Policy

Claims History Signals Future Risk

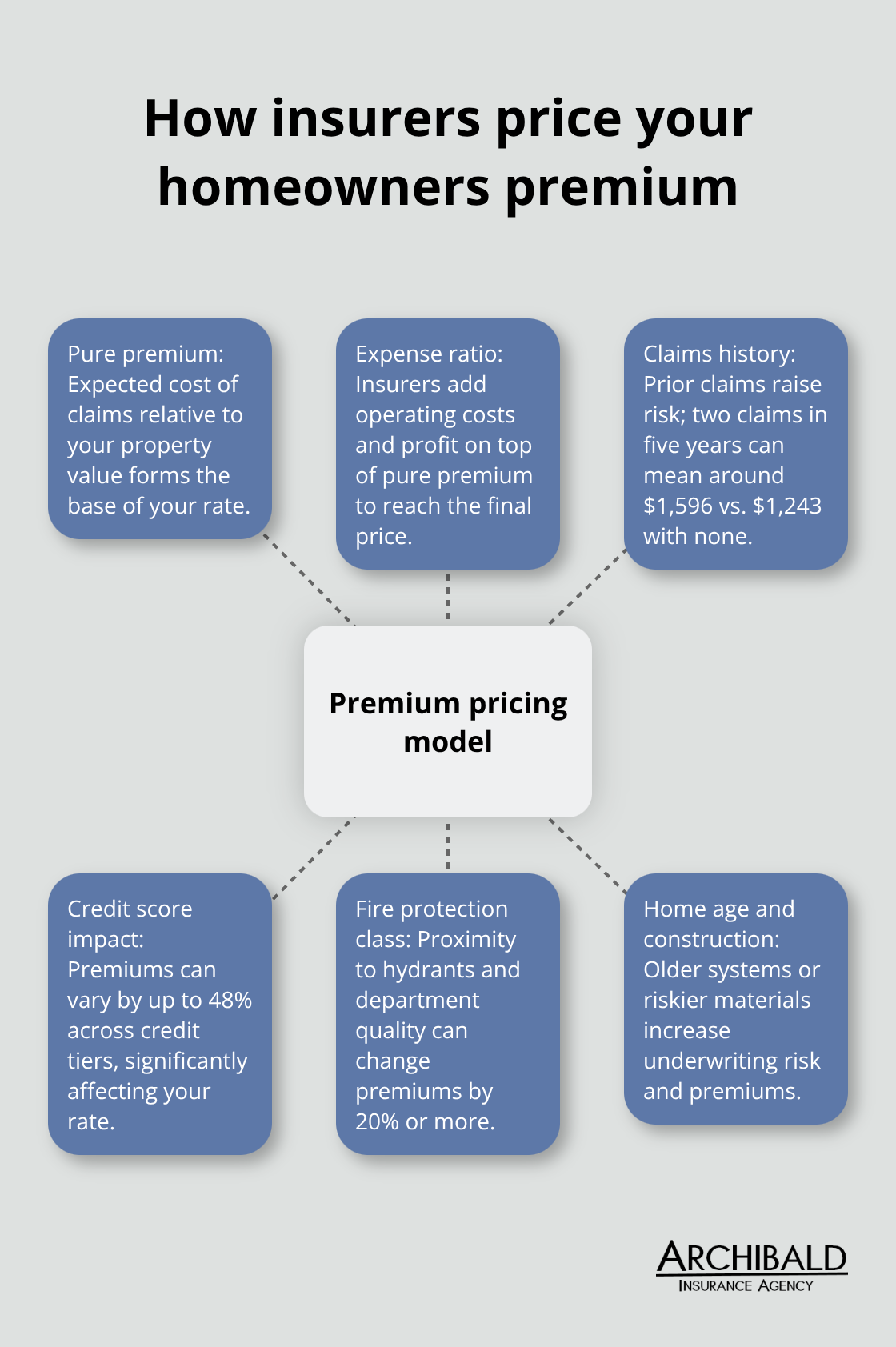

Insurance companies use a two-step calculation to arrive at your premium: they calculate the pure premium (the expected cost of claims relative to your property value) and then add an expense ratio for operating costs and profit. Your claims history as a statistical predictor of future claims feeds directly into that first calculation because insurers view past claims as a key risk factor. If you filed two claims in the past five years, your premium might run around $1,596 annually, compared to $1,243 per year if you’ve had no claims in five years or longer, according to MoneyGeek’s analysis. Even small claims can raise your rate by roughly 12%, so insurance companies treat your filing history as a core risk factor.

Credit Score Creates Dramatic Premium Differences

Your credit score influences premiums just as heavily as claims history, sometimes by up to 48% depending on your credit tier. A homeowner with excellent credit might pay around $1,016 per year while someone in a fair credit range pays roughly $2,396 annually for identical coverage. Insurers use credit scores as a statistical predictor of how likely you are to file a claim and how you manage financial obligations, not as personal judgment about your character.

Home Age and Construction Materials Determine Underwriting Risk

The age of your home matters significantly because older homes typically cost more to insure. A home built in 1950 with original wiring and plumbing represents higher risk than a 2015 home with updated systems, so your construction year directly affects your premium calculation. Frame construction with a shake or treated roof costs substantially more to insure than brick construction with a composition roof, sometimes adding $55 to $111 per month to your premium depending on condition and location. Insurance underwriters assess whether your roof is near the end of its lifespan, whether your electrical system meets current standards, and whether your plumbing is prone to failure-these factors determine your risk profile before you ever discuss coverage limits.

Fire Protection Class Affects Your Rate

The distance from your home to the nearest fire hydrant and the quality of your local fire department feed into your final premium through what insurers call your fire protection class. Homes within 5,000 feet of a fire hydrant and served by well-equipped departments get better rates than rural properties, sometimes creating premium differences of 20% or more for otherwise identical homes. This geographic factor combines with your home’s age and construction type to complete the underwriting picture that shapes what you pay each month.

Understanding these risk factors helps you see why your premium lands where it does. The next step is learning what you can actually control to lower that cost.

How to Reduce Your Homeowners Insurance Premium

Bundle Your Home and Auto Insurance for Immediate Savings

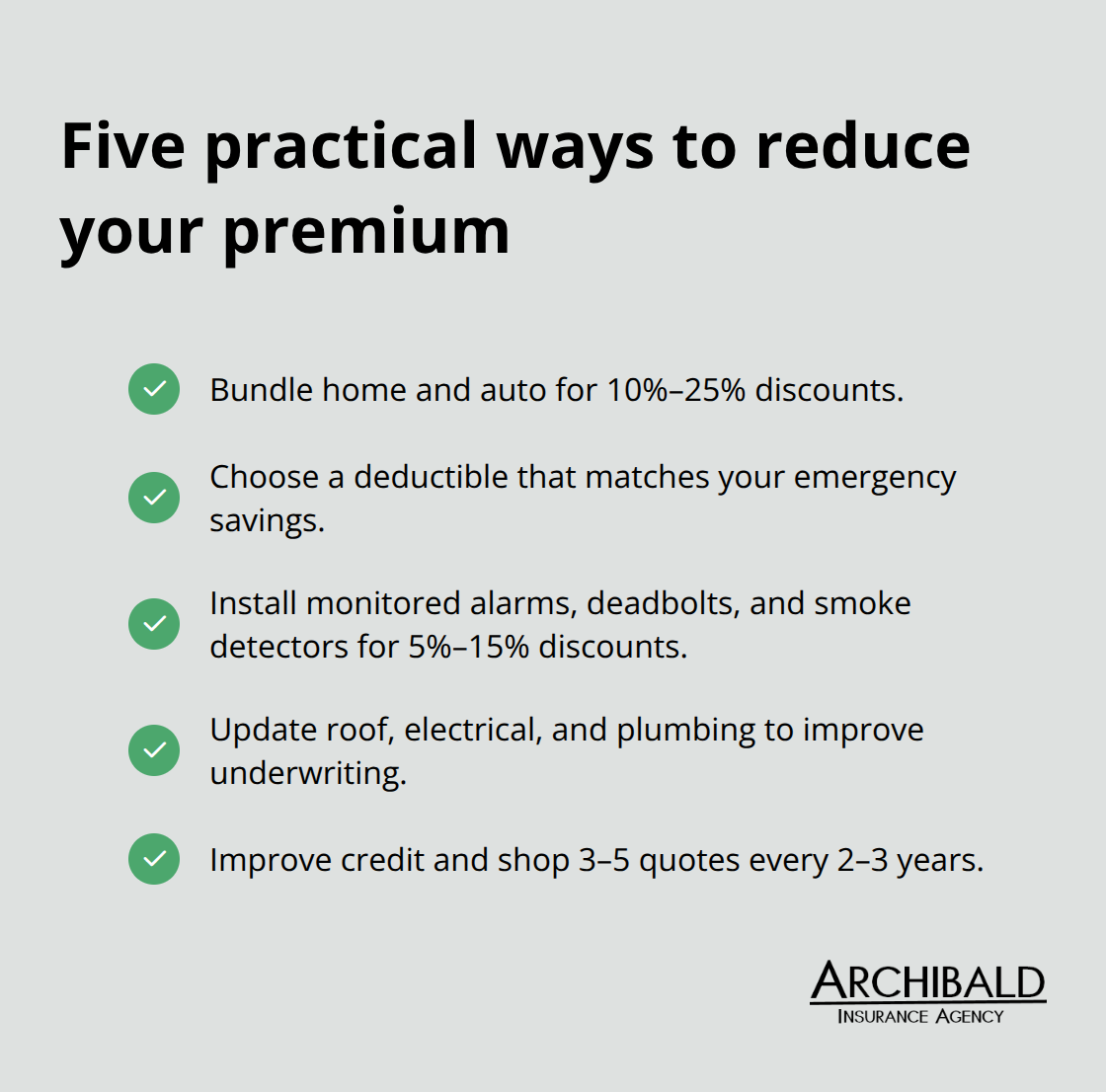

Bundling your home and auto insurance typically delivers a 10% to 25% discount on both policies, making this the easiest immediate action you can take. If you carry auto insurance with one company and homeowners with another, you’re leaving money on the table every single month. Moving both policies to the same carrier takes one phone call and can save you hundreds annually. This single step addresses one of the most straightforward ways insurers reward lower-risk customers.

Adjust Your Deductible to Match Your Emergency Savings

Your deductible choice offers immediate control over your monthly cost. Standard homeowners insurance deductibles often range from $500 to $2,000, although they can be higher or lower depending on your insurance carrier and budget. The mistake most homeowners make is selecting a high deductible without building the cash reserves to support it, which creates financial stress when a covered loss occurs. Match your deductible to what you can actually afford to pay out of pocket.

Install Security Features That Insurers Reward

Installing physical security features like monitored burglar alarms, deadbolt locks, and smoke detectors signals lower risk to insurers and often qualifies you for discounts ranging from 5% to 15% depending on the system and your carrier. A professionally monitored system costs between $20 and $50 monthly but can reduce your annual insurance premium by $100 to $200, making the investment worthwhile within the first year. These upgrades address the underwriting factors that directly influence your premium calculation.

Update Your Home’s Age-Related Systems

Your home’s age and construction condition influence whether you qualify for preferred rates or face higher premiums. If your home was built before 1980, updating your roof, electrical system, or plumbing can improve your underwriting classification and lower costs. Insurers often require roof replacement if it’s within five years of the end of its lifespan, so addressing this proactively prevents coverage denials and rate increases.

Improve Your Credit Score and Shop Regularly

Credit score improvements deliver substantial savings because premiums can vary by up to 48% across credit tiers. If you’ve worked to improve your credit from fair to good range, notify your insurer because they may re-evaluate your rate without requiring a policy change. Shopping your policy every two to three years matters more now than ever because insurers adjust rates differently based on market conditions and claims trends in your area. Utah premiums increased approximately 13% in 2024 alone, so a quote that looked competitive two years ago may no longer reflect current market pricing. Getting three to five quotes from different carriers ensures you’re not overpaying for identical coverage. When comparing quotes, verify that deductibles, coverage limits, and valuation methods match across all quotes so you’re genuinely comparing apples to apples. Some insurers price replacement cost coverage much higher than actual cash value, so understanding which valuation method each quote uses prevents costly surprises when you file a claim.

Final Thoughts

Your homeowners insurance premium reflects three core factors: where you live in Utah, what your home costs to rebuild, and the coverage limits you choose. Location drives the biggest differences, with some counties seeing premiums nearly double between 2020 and 2023. Your replacement cost determines your dwelling coverage foundation, and your deductible choice directly controls your monthly payment.

You have real control over several factors that shape what you pay each month through bundling policies, raising your deductible, installing security features, and improving your credit score. Start by requesting actual quotes from multiple carriers rather than relying on online calculators, and have your home’s square footage, construction year, roof type, and claims history ready so you can compare identical coverage across different insurers. Utah’s market offers competitive options, but rates vary dramatically by provider, so shopping around typically saves hundreds annually.

We at Archibald Insurance Agency understand that navigating how to calculate homeowners insurance cost feels overwhelming when you’re trying to balance protection with affordability. As an independent agency in Salt Lake City, we represent numerous insurance carriers, which means we show you options that fit your specific needs and budget rather than pushing you toward one company’s products. Contact us at archibald-insurance.com to discuss your situation with someone who knows Utah’s insurance market and can help you find the right coverage at a competitive rate.