General Liability Insurance for Small Businesses Explained

One accident on your business property can cost thousands in medical bills, legal fees, and settlements. General liability insurance for small businesses protects you from these financial disasters.

At Archibald Insurance Agency, we help Utah business owners understand why this coverage matters and how to get the right protection for their specific needs.

What General Liability Insurance Actually Covers

The Core Protection Your Business Needs

One accident on your business property can cost thousands in medical bills, legal fees, and settlements. General liability insurance protects your business when someone gets hurt on your property or your business operations damage someone else’s property. This coverage pays for medical bills if a customer slips and falls in your store, covers legal defense costs if you’re sued, and handles settlement payments if you lose a case. The U.S. Bureau of Labor Statistics reported non-fatal workplace injuries in Utah during 2022, many of which could trigger liability claims against businesses. A typical slip-and-fall claim costs around $20,000, but legal fees can push total costs above $100,000 if the case goes to court.

What Your Policy Actually Covers

Your policy covers bodily injury claims, property damage liability, and personal injury claims like libel or slander related to your business. Medical payments coverage under your policy pays for minor injuries on your premises without requiring the injured person to file a lawsuit, which often prevents small incidents from becoming expensive claims. This coverage is separate from workers’ compensation, which only covers your employees.

The most common GL claims involve slips, trips, and falls, accounting for over 30% of all claims, so premises safety directly impacts your risk profile and potential premiums.

Critical Coverage Gaps You Must Know

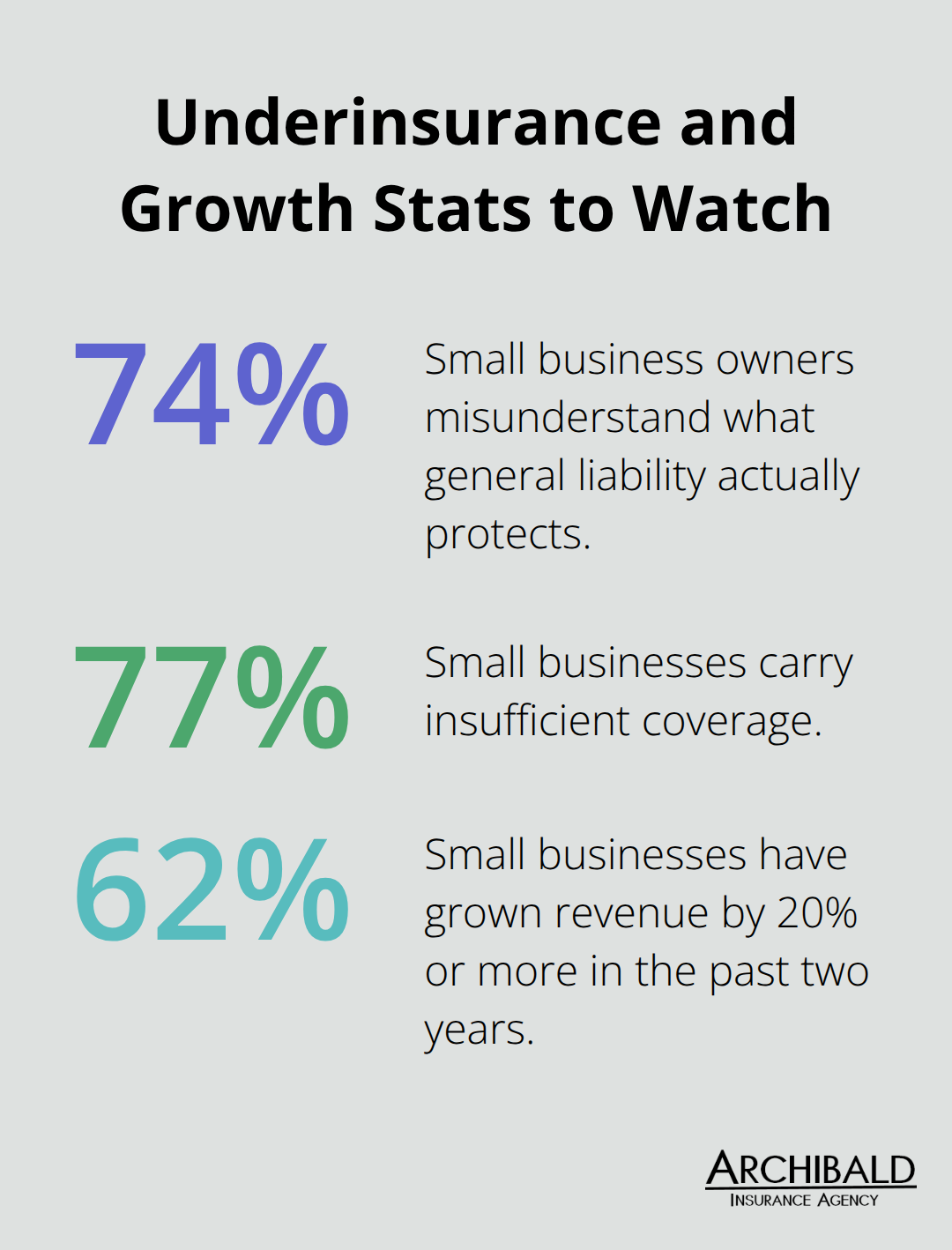

What general liability doesn’t cover matters just as much as what it does. The 2025 Hiscox Underinsurance in Small Business Report found that 74% of small business owners misunderstand what general liability actually protects. Many owners mistakenly believe GL covers fires or floods on their owned property, theft of their own equipment, or professional mistakes like missed deadlines. These gaps require separate policies like commercial property insurance, cyber liability, or professional liability coverage.

Industry and Operation-Specific Risks

If you operate from a home-based office, verify that your coverage extends to those operations. If you use vehicles for business, personal auto insurance won’t cover you, so you need commercial auto coverage or hire and non-owned auto coverage added to your policy. Industry-specific risks demand different limits: a contractor handling heavy equipment faces higher exposure than a consulting firm, so don’t assume standard limits protect you adequately. Understanding your exact business operations helps you identify which coverage gaps pose the greatest threat to your financial stability.

Why Your Business Needs General Liability Coverage

The Real Cost of Operating Without Coverage

General liability insurance isn’t optional for Utah small businesses-it’s the foundation that keeps financial disasters from destroying what you’ve built. Without it, a single incident drains your cash reserves, damages your credit, and forces you to close. A slip-and-fall on your premises can result in significant medical and legal costs that come directly from your pocket if you lack coverage.

Meeting Contract and Lease Requirements

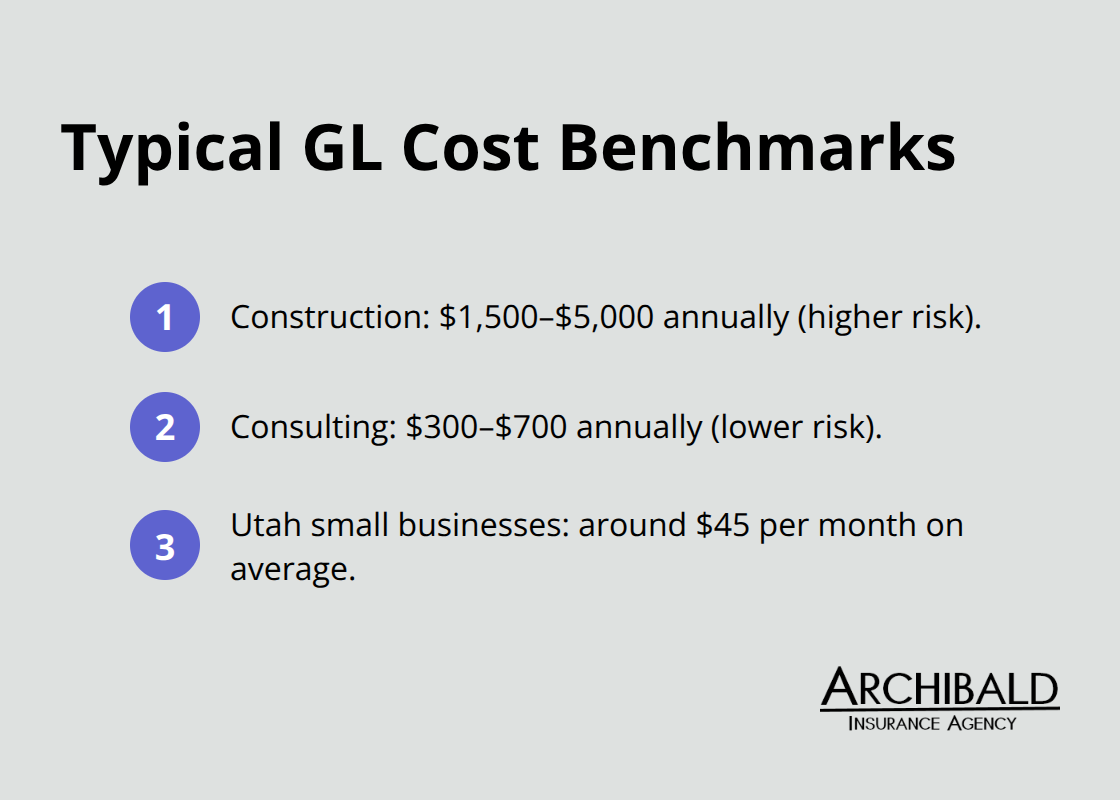

Your clients and landlords won’t wait for you to figure this out. Most commercial leases require proof of general liability before you occupy the space, and clients demand a certificate of insurance before signing contracts. Without it, you simply don’t get the job. Insurance carriers recognize this reality: they’ve priced general liability premiums at around $45 per month for small Utah businesses, making it one of the cheapest protections you can buy relative to the risk it covers.

Building Professional Credibility

General liability coverage signals to customers and partners that you operate professionally and responsibly. When you produce a certificate of insurance on demand, you demonstrate financial stability and accountability that builds trust immediately. This matters especially if you’re competing for larger contracts or working with established companies that vet their vendors carefully. The cost of not having coverage isn’t just the potential claim itself-it’s the lost business opportunities, the damaged reputation when you can’t meet requirements, and the stress of operating without a safety net.

Choosing the Right Coverage Limits

Different industries face different exposures, so your coverage limits should match your actual operations, not just the minimum that sounds affordable. A contractor handling heavy equipment needs higher limits than a consulting firm. A retailer with high foot traffic faces greater slip-and-fall exposure than a home-based service provider. Understanding your specific risk profile helps you select limits that truly protect your business.

Moving Forward with Protection

Once you understand why coverage matters, the next step involves assessing your industry-specific risks and determining the adequate limits for your situation. This process ensures you carry protection that matches your actual exposure rather than guessing at what you need.

How to Choose the Right Coverage for Your Business

Start With Your Actual Risk Profile

Start with your industry’s real risk profile, not generic minimums. A florist operating from a retail location faces different exposures than a contractor using heavy equipment on job sites. The 2025 Hiscox Underinsurance in Small Business Report found that 77% of small businesses carry insufficient coverage, often because owners guess at limits rather than assess real risk. Document what your business does daily: Do customers visit your premises? Do you handle products that could cause injury? Do you operate vehicles for business? Do you work from a home office? Each answer shapes your coverage needs.

Construction businesses typically pay $1,500 to $5,000 annually for general liability, while consulting firms pay $300 to $700, reflecting genuine risk differences. Location matters too-a retail location has different exposure than the same business in another area.

Determine Coverage Limits That Match Your Growth

Once you identify your actual operations, standard limits become obvious. Most contracts require $1 million per occurrence and $2 million aggregate, but your specific assets and revenue growth may demand higher limits. The 2025 Hiscox report shows 62% of small businesses have grown revenue by 20% or more in the past two years. If you fall into that group, your coverage limits from two years ago no longer reflect your real exposure.

Higher revenue means more customers, more transactions, and more potential claims. Assess whether your current limits protect your actual asset value and income level. An umbrella policy provides an extra layer of liability protection by covering costs that go beyond your other liability coverage limits.

Compare Quotes Across Multiple Carriers

Shopping for quotes reveals massive price variations that justify the effort. Carriers charge differently based on industry classification, claims history, safety practices, and risk assessment. Getting quotes from multiple carriers prevents you from overpaying by hundreds of dollars annually.

Some carriers offer bundled policies that combine general liability with commercial property coverage at 10% to 15% savings compared to separate policies, while others focus on specific industries. When comparing quotes, scrutinize what’s actually covered and what’s excluded-an unusually cheap quote often hides exclusions that leave you underinsured for your specific risks.

Leverage Safety Improvements for Lower Premiums

Ask carriers about discounts for safety improvements like better lighting, security upgrades, or formal safety training programs. Many insurers reduce premiums for businesses with documented safety procedures and ongoing training. These investments pay for themselves through lower insurance costs while simultaneously reducing your actual injury risk.

Small businesses can obtain certificates of insurance immediately after purchasing, which you’ll need for contracts and leases. Review your coverage every two years or whenever your business size changes significantly, since static policies don’t account for growth, new equipment, expanded operations, or changed client bases.

Final Thoughts

General liability insurance for small businesses protects your assets, satisfies contract requirements, and keeps your operation running when accidents happen. Without coverage, a single incident drains your cash reserves and forces closure; with it, you transfer that financial risk to an insurer and focus on growth instead of lawsuits. Most Utah small businesses pay around $45 monthly for this protection, making it affordable relative to the catastrophic costs it prevents.

Assess your actual business operations, identify your industry-specific risks, and determine what coverage limits match your real exposure rather than guessing at minimums. Get quotes from multiple carriers to find competitive rates that fit your budget, then obtain your certificate of insurance immediately so you’re ready for contracts and leases. The team at Archibald Insurance Agency understands Utah small businesses and can help you navigate these decisions by comparing options across multiple insurers to find coverage that fits your specific needs.

Review your coverage every two years or whenever your business changes significantly, since growth, new equipment, expanded operations, or different client bases all shift your risk profile. Static policies don’t account for business evolution, so regular attention keeps your protection aligned with reality and prevents the underinsurance problem that affects 77% of small businesses today. This ongoing approach ensures your general liability insurance for small business stays relevant as your operation develops.