Replacement Cost on Homeowners Insurance Explained

Most Utah homeowners don’t realize their insurance might not cover the full cost to rebuild their home after a disaster. The difference between what you think your coverage provides and what it actually pays can be devastating.

We at Archibald Insurance Agency see this confusion about replacement cost on homeowners insurance daily. Understanding this coverage type protects your biggest investment and your family’s financial future.

How Does Replacement Cost Coverage Actually Work

Replacement cost coverage pays the full amount needed to rebuild your home or replace your belongings at today’s prices without subtracting for age or wear. When you file a claim, your insurer calculates what it would cost to use similar quality materials and current labor rates to restore everything exactly as it was before the damage occurred.

The Clear Difference Between Coverage Types

This differs dramatically from actual cash value coverage, which deducts depreciation from your payout and leaves most Utah homeowners significantly short of funds needed for repairs. Many homeowners face coverage gaps, primarily because they don’t understand this coverage difference.

If your 10-year-old roof gets damaged in a hailstorm, actual cash value coverage might pay only $12,000 for a roof that originally cost $20,000. Replacement cost coverage pays the full $25,000 needed for today’s materials and labor.

What Items Qualify for This Protection

Your home structure, attached garages, built-in appliances, and personal belongings can all qualify for replacement cost coverage. You must specifically request this protection since many insurers default to actual cash value for personal property (a detail that catches many homeowners off guard).

Utah’s Construction Cost Reality

Replacement cost coverage protects against rising construction costs in Utah, where homeowners have seen premiums rise significantly due to lumber price fluctuations and labor shortages. Standard policies cap coverage at your home limit, which makes it essential to carry adequate limits that reflect current rebuild costs rather than your home’s market value.

Extended replacement cost coverage adds 25-50% above your home limit. Guaranteed replacement cost coverage removes caps entirely, though fewer insurers offer this premium protection in Utah’s high-risk wildfire and earthquake zones.

These coverage limits become even more important when you consider the specific factors that drive up reconstruction costs in Utah’s unique market conditions.

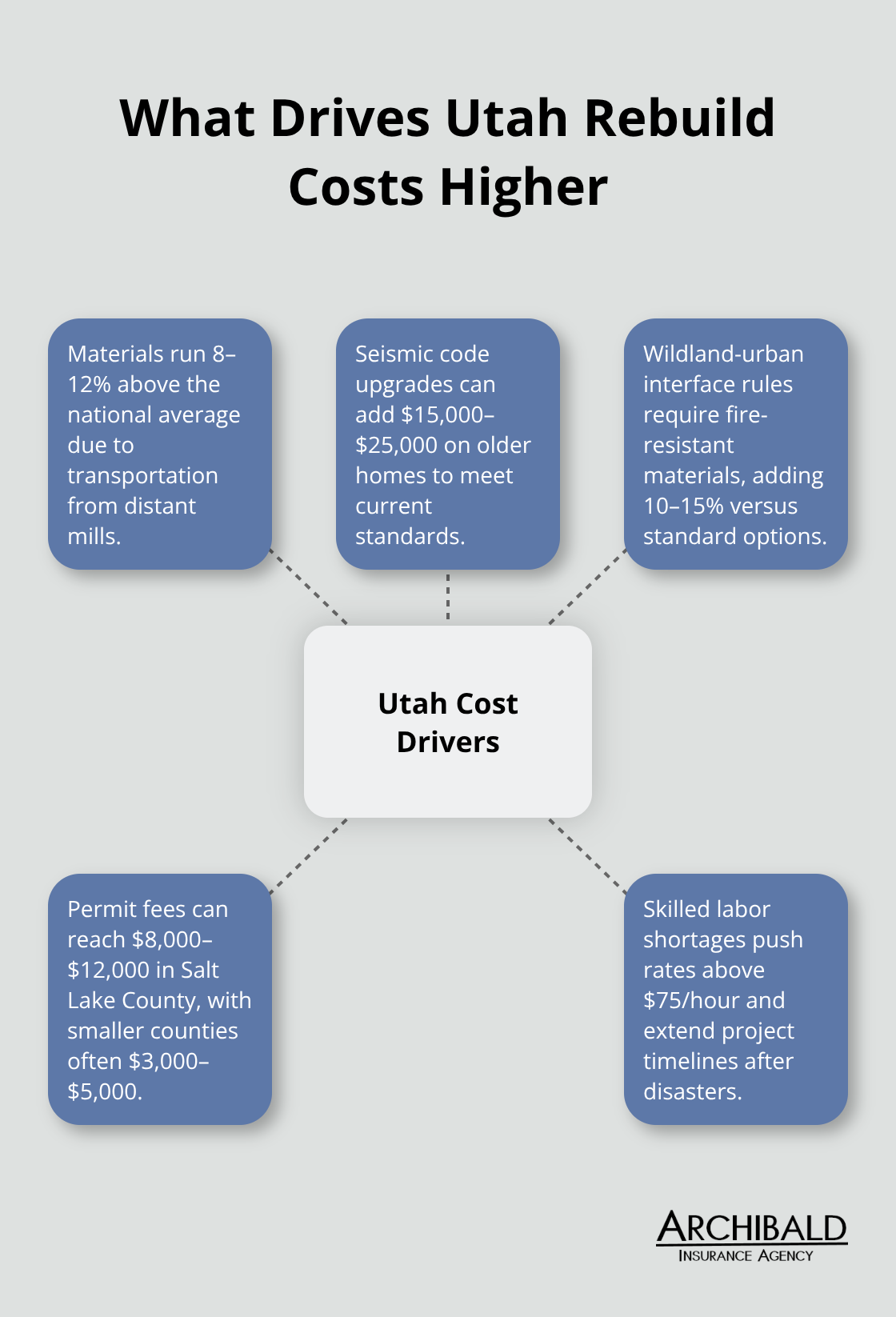

What Drives Your Replacement Cost Up in Utah

Utah’s construction market creates specific challenges that directly impact your replacement cost coverage needs. Lumber prices have shown volatility with recent decreases, while skilled labor shortages push hourly rates for contractors above $75 in the Salt Lake City metro area. These factors mean your replacement cost estimate from three years ago likely falls short of today’s reality by 20-30%.

Material Costs Hit Utah Harder

Utah’s distance from major lumber mills increases transportation costs, which makes materials 8-12% more expensive than the national average. Steel and concrete prices fluctuate based on regional demand from commercial projects along the Wasatch Front. Your home’s square footage matters less than the materials used – a 2,000-square-foot home with custom millwork and high-end finishes costs $200-250 per square foot to rebuild, while standard construction runs $140-170 per square foot. Homes built before 1980 often require specialized materials that cost significantly more due to discontinued products and exact match requirements.

Code Updates Add Hidden Expenses

Utah’s seismic codes require structures to resist earthquakes without significant damage, which add $15,000-25,000 to rebuild costs for older homes. New electrical standards mandate whole-house surge protection and updated panel systems. Fire-resistant materials are now required in wildland-urban interface zones (areas where homes meet wildland vegetation), which increases costs by 10-15% over standard materials. Permit fees in Salt Lake County alone can reach $8,000-12,000 for a complete rebuild, while smaller counties charge $3,000-5,000.

These code upgrades aren’t optional – your insurance won’t cover shortcuts that don’t meet current standards.

Labor Shortage Impact

Utah faces a severe shortage of skilled construction workers, particularly in specialized trades like electrical and plumbing. This shortage drives up hourly rates and extends project timelines (which can increase temporary housing costs covered under your policy). Many contractors now require premium pay for rush jobs after disasters, when multiple homeowners compete for limited workers. The shortage becomes more pronounced during peak construction seasons from April through October.

Despite these cost pressures, many Utah homeowners make critical errors when they estimate their coverage needs or update their policies.

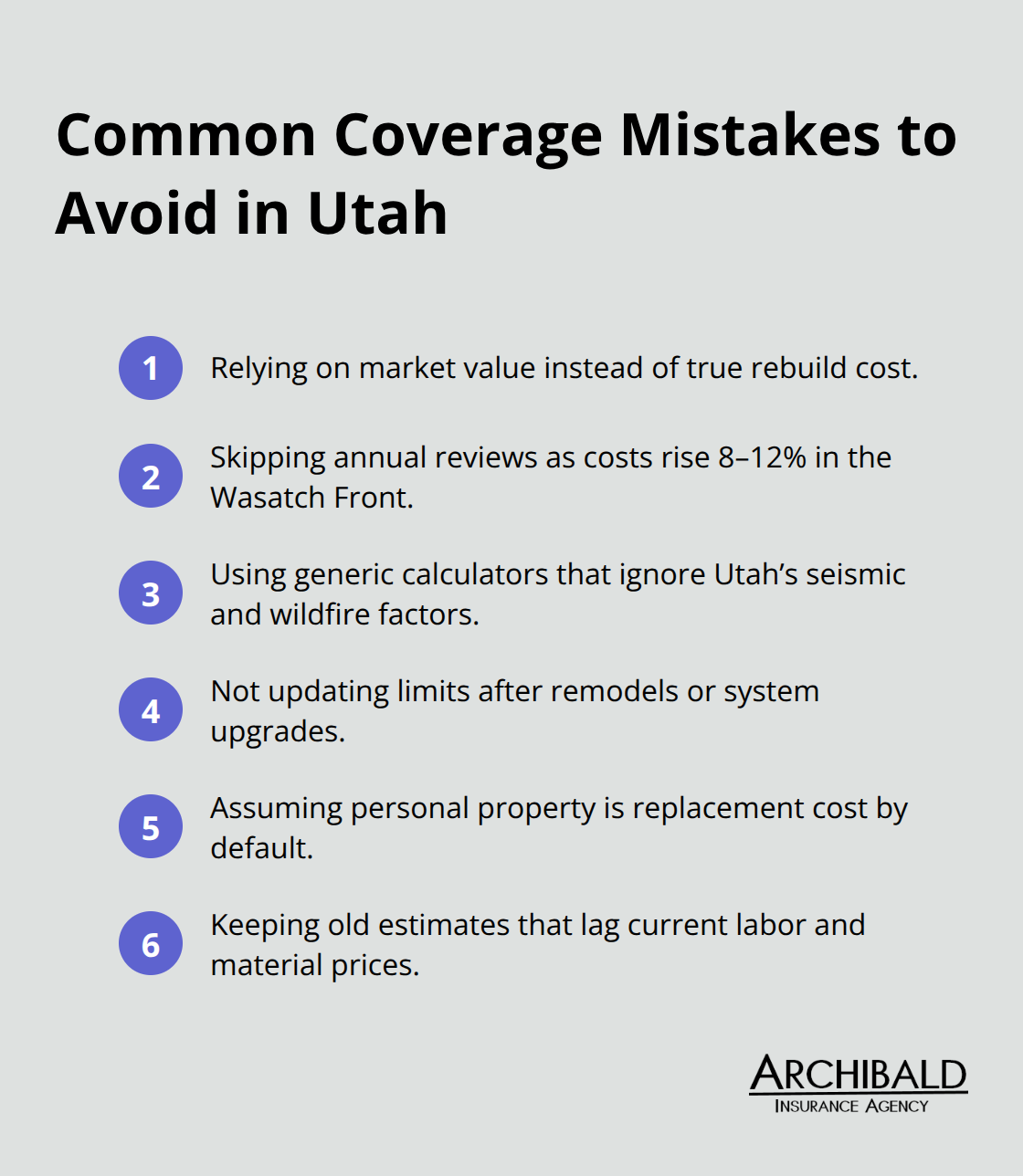

Where Utah Homeowners Go Wrong With Coverage

Utah homeowners make three expensive mistakes that leave them financially exposed when disaster strikes. The most damaging error involves online calculators that underestimate rebuild costs, when actual Utah construction varies significantly based on materials and location. These calculators ignore Utah’s unique factors like seismic requirements, wildfire-resistant materials, and higher transportation costs for building supplies.

The $50,000 Market Value Trap

Market value creates the most dangerous assumption homeowners make about their coverage needs. Your home’s $400,000 market value includes land worth $150,000-200,000 in most Utah markets, which means your actual structure value sits closer to $200,000-250,000. However, rebuilding that same structure costs $300,000-400,000 at current rates due to code upgrades, permit fees, and labor shortages.

Many homeowners across the United States face underinsurance challenges, with 7.4 percent uninsured entirely. This gap between market value and replacement cost catches homeowners off guard when they file claims.

The Annual Review Gap

Most Utah homeowners review their coverage every three to five years, which creates dangerous gaps as construction costs rise 8-12% annually in the Wasatch Front region. Home improvements compound this problem – that $30,000 kitchen remodel increases your replacement cost by $35,000-40,000 due to current material and labor prices.

Homeowners who add solar panels, finish basements, or upgrade HVAC systems often fail to update their coverage limits. These improvements can add $20,000-80,000 to rebuild costs, yet many policies still reflect pre-improvement values from years earlier (sometimes dating back five or more years).

The Calculator Confusion

Generic replacement cost calculators fail Utah homeowners because they use national averages that don’t account for local conditions. Utah’s seismic building requirements add $15,000-25,000 to standard construction costs. Earthquake insurance becomes crucial given these elevated risks and building standards. Wildfire-resistant materials in interface zones increase costs by another 10-15%. Transportation costs for materials run 8-12% higher than national averages due to Utah’s distance from major supply centers.

Final Thoughts

Replacement cost on homeowners insurance protects Utah families from financial devastation when disaster strikes. This coverage pays current rebuild costs without depreciation deductions, which means you receive the full amount needed to restore your home and belongings to their original condition. Annual policy reviews prevent dangerous coverage gaps as construction costs rise 8-12% yearly in Utah.

Document home improvements immediately and update your coverage limits to reflect these changes. Calculate replacement costs with Utah-specific factors like seismic requirements, wildfire-resistant materials, and elevated labor costs rather than generic online tools. Local agents who understand Utah’s unique construction challenges make the difference between adequate protection and financial exposure.

We at Archibald Insurance Agency represent multiple carriers to find coverage that matches your specific needs and budget. Our team knows Utah’s building codes, material costs, and regional risks that affect your replacement cost calculations (factors that generic calculators miss entirely). Contact us today to review your policy and protect your family’s financial future.