Homeowners Insurance for Fire Damage Protection

Fire damage costs Utah homeowners an average of $76,000 per incident, making proper coverage essential for protecting your investment.

We at Archibald Insurance Agency see too many families struggle with inadequate homeowners insurance for fire damage when disaster strikes. Understanding your policy’s fire protection details can mean the difference between full recovery and financial hardship.

Understanding Fire Damage Coverage in Homeowners Insurance

Your homeowners insurance covers far more fire-related damage than most Utah homeowners realize. Standard policies protect against fire from cooking accidents, electrical faults, lightning strikes, and even wildfires. The Insurance Information Institute provides comprehensive data on homeowners insurance claims and trends.

Your dwelling coverage rebuilds your home’s structure, while personal property coverage replaces damaged items at replacement cost. Additional expenses pay for hotels and increased costs when your home becomes uninhabitable during repairs.

Coverage Exclusions That Surprise Homeowners

Fire damage from arson or intentional acts faces exclusion from every policy. Older homes with knob-and-tube wiring encounter potential coverage gaps if the wiring caused the fire and wasn’t properly maintained. Outdoor structures like detached garages need separate other structures coverage (often 10% of your dwelling coverage). Business equipment stored at home requires additional endorsements for full protection.

How Insurance Companies Handle Fire Claims

Fire claims trigger immediate action from your insurer’s adjuster team. Document everything with photos before cleanup begins, save receipts for temporary repairs, and maintain detailed records of damaged items. The U.S. Fire Administration reports that fire departments responded to an estimated 170,000 home cooking fires in 2021, making kitchen incidents the most common claims.

Your adjuster evaluates structural damage, personal property losses, and additional expenses separately. Most insurers advance funds for immediate needs while they investigate the full extent of damage.

Average Costs and Payout Expectations

Fire damage costs vary dramatically based on the fire’s source and extent. Kitchen fires average $15,000 in damage, while whole-house fires can exceed $200,000. Utah homeowners face unique wildfire risks that can destroy entire neighborhoods, making adequate coverage limits essential for complete protection.

Understanding these coverage basics prepares you for Utah’s specific fire risks and the prevention strategies that can protect your home.

Fire Risk Factors and Prevention Strategies for Utah Homeowners

Utah homeowners face extreme wildfire danger due to the state’s arid climate and mountainous terrain. The Wasatch Front experiences severe fire weather conditions with sustained winds exceeding 40 mph and humidity levels below 15 percent during peak fire season from July through September. These conditions create the perfect storm for rapid fire spread, with flames advancing at speeds of 14 miles per hour across dry vegetation.

Wildfire Zones Demand Immediate Action

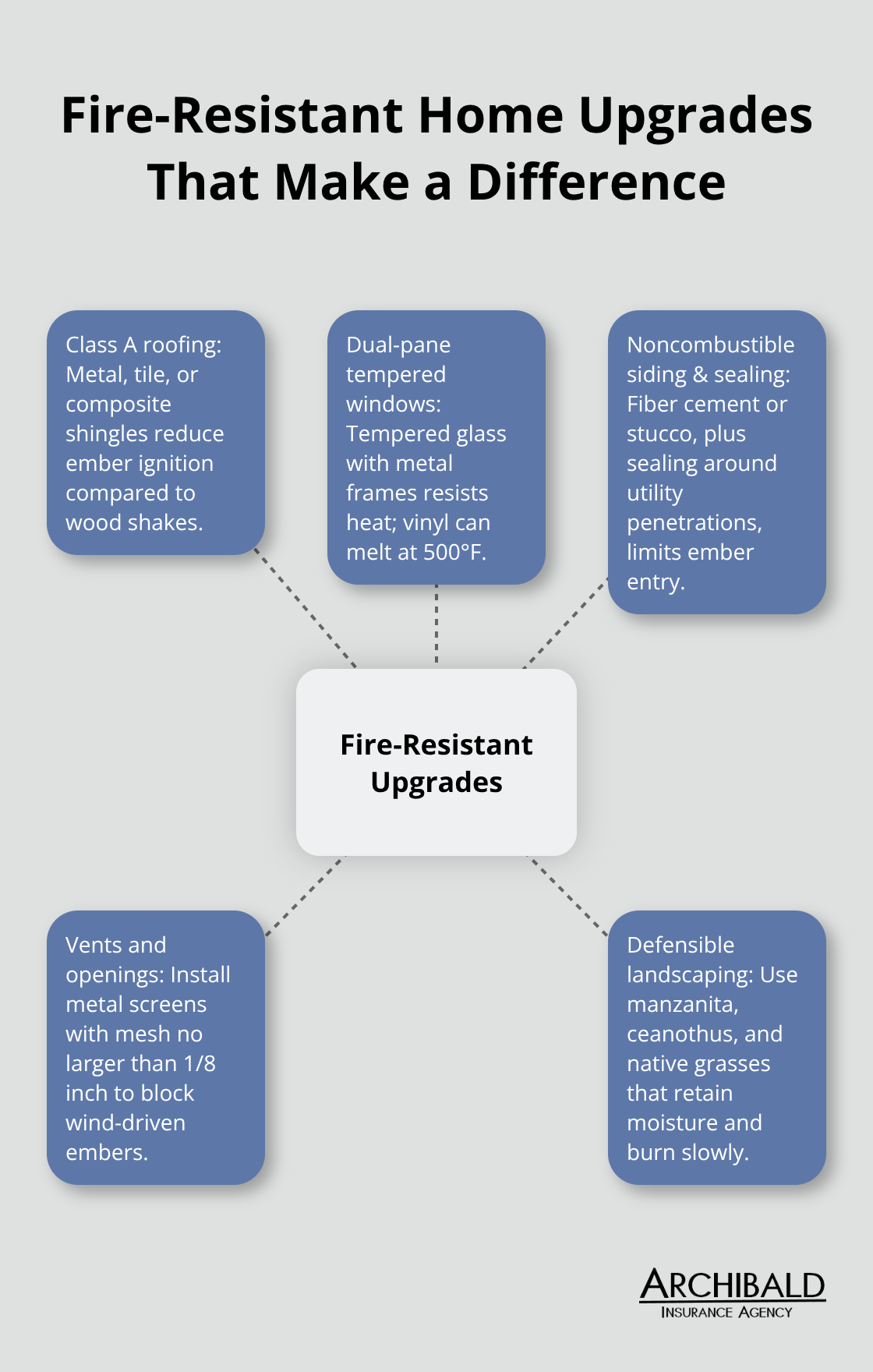

Properties within the Wildland-Urban Interface face the highest risk, particularly homes in foothill areas of Salt Lake, Utah, and Weber counties. The National Interagency Fire Center data shows Utah experiences significant wildfire activity annually. Homes located within one mile of natural vegetation need defensible space that extends 100 feet from all structures. Remove dead vegetation, trim tree branches within 10 feet of your roof, and replace wood mulch with gravel or rock within 30 feet of your home. Install metal screens with mesh no larger than 1/8 inch on all vents and openings.

Kitchen Safety Prevents Most Home Fires

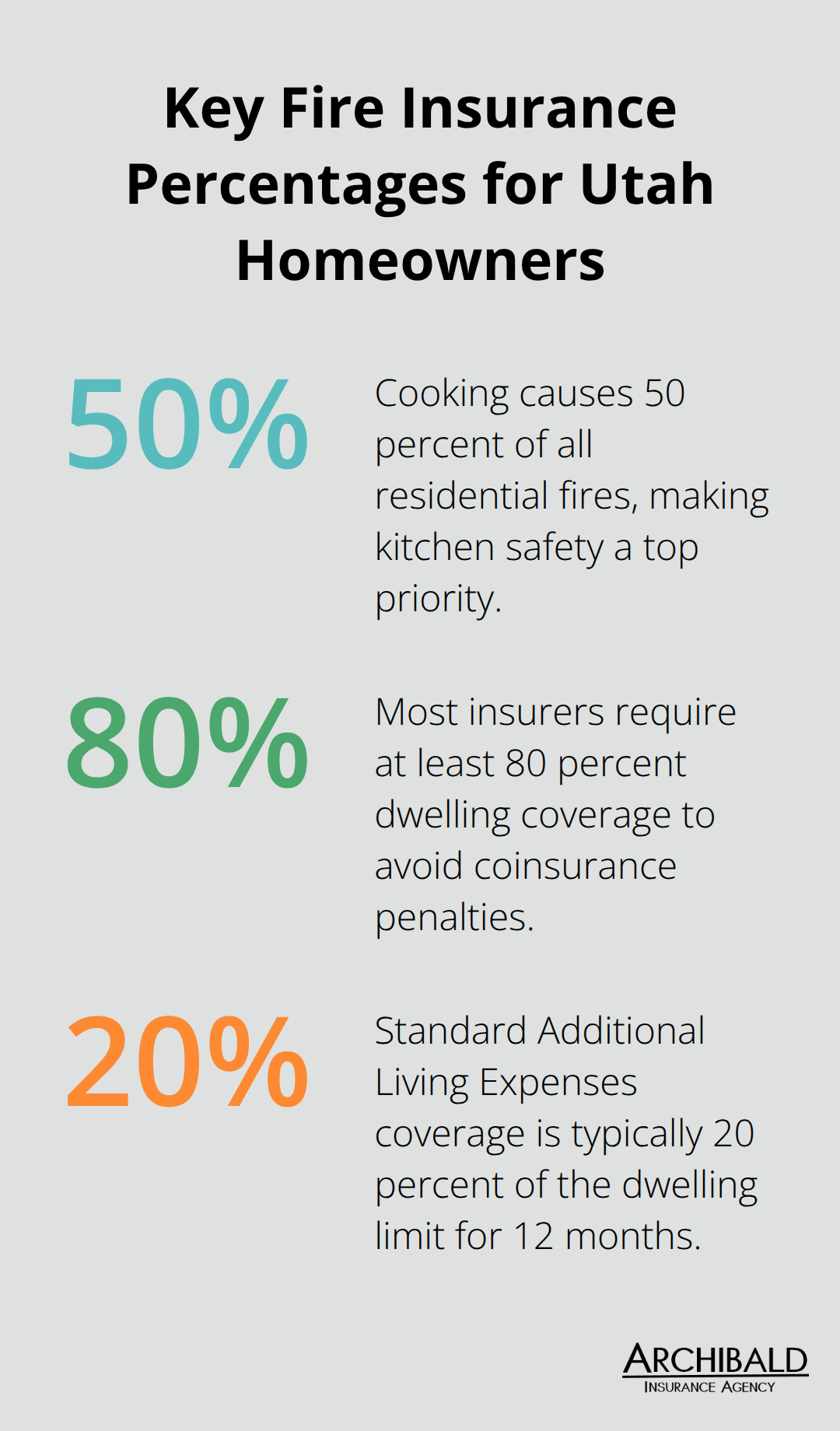

Cooking causes 50 percent of all residential fires, with unattended stovetops accounting for the majority of incidents. Never leave cooking food unattended, keep pot handles turned inward, and maintain a three-foot clear zone around your stove. Electrical fires rank second, often starting from overloaded circuits and damaged extension cords. Replace any cord that shows wear, avoid daisy-chaining power strips, and install arc-fault circuit interrupters in bedrooms and living areas.

Fire-Resistant Materials Save Homes

Class A fire-rated roofing materials like metal, tile, or composite shingles significantly reduce ember ignition risk compared to wood shakes. Install dual-pane windows with tempered glass and metal frames rather than vinyl, which melts at 500 degrees. Choose fiber cement or stucco siding over wood, and seal gaps around utility penetrations with fire-resistant caulk. Plant fire-resistant landscaping like manzanita, ceanothus, and native grasses that retain moisture and burn slowly (creating natural firebreaks around your property).

These prevention strategies work hand-in-hand with proper insurance coverage limits to protect your investment. Understanding how to maximize your fire damage protection requires careful attention to coverage amounts and policy details.

How Much Fire Coverage Do You Actually Need

Utah homeowners consistently underestimate their fire damage coverage needs and create dangerous gaps when reconstruction costs surge after major fires. Dwelling coverage must equal 100 percent of your home’s replacement cost, not its market value. Construction costs in Utah continue to fluctuate based on market conditions, which means a home valued at $400,000 might cost significantly more to rebuild.

Most insurers require 80 percent coverage minimum to avoid coinsurance penalties, but this leaves you severely underprotected. Calculate replacement costs with current construction rates of $150 to $200 per square foot for standard Utah homes. Personal property coverage should equal 50 to 70 percent of your dwelling amount and cover everything from furniture to electronics at replacement cost rather than actual cash value.

Additional Living Expenses Coverage Prevents Financial Stress

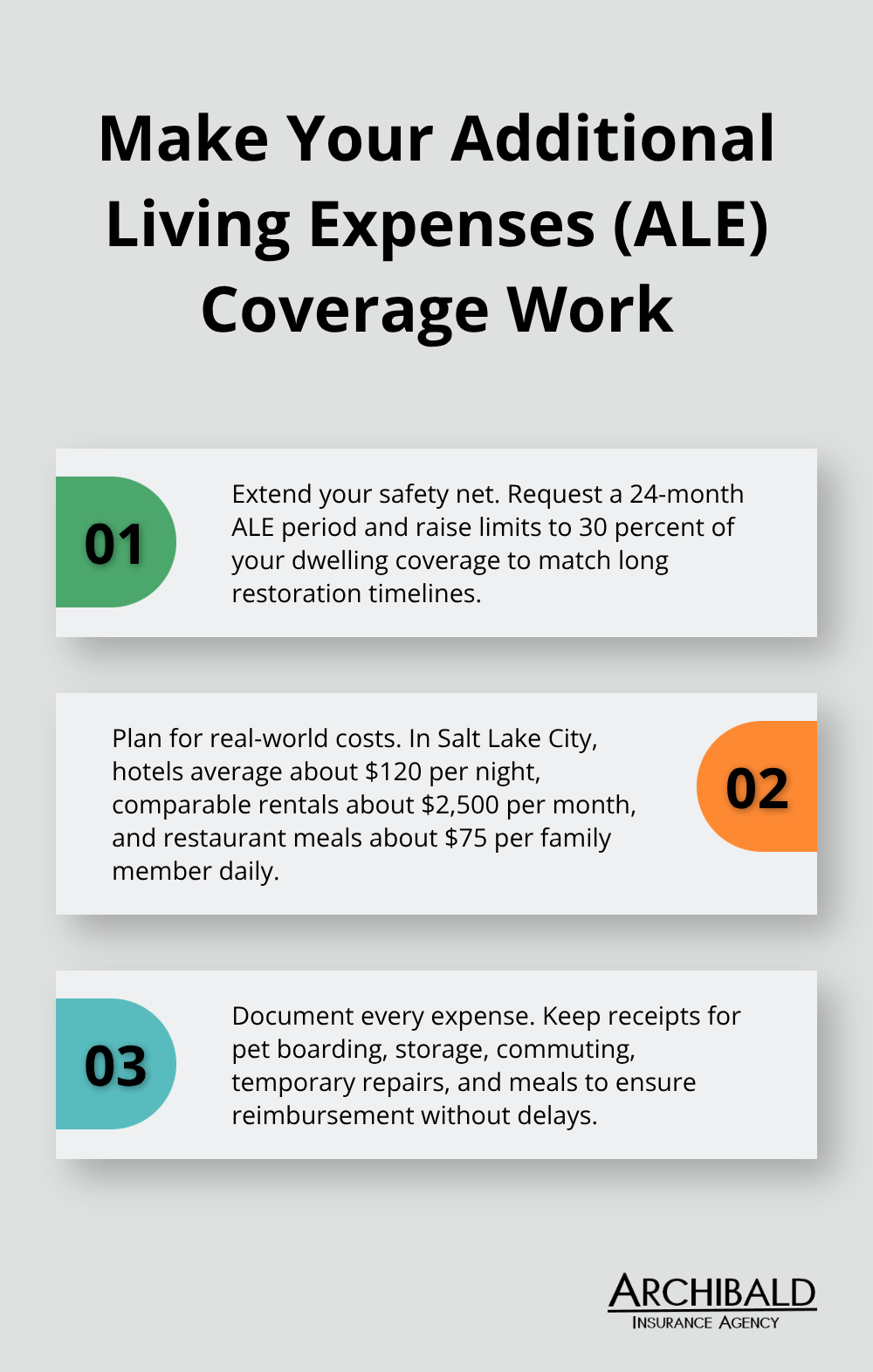

Fire damage repairs take four to eight months for major incidents, which makes Additional Living Expenses coverage essential for maintaining your lifestyle. Standard policies provide 12 months of coverage at 20 percent of your dwelling limit, but complex fire restoration often exceeds this timeframe.

Request extended coverage periods of 24 months and increase limits to 30 percent of dwelling coverage. Hotel costs in Salt Lake City average $120 nightly, while temporary rentals cost $2,500 monthly for comparable housing. Restaurant meals add $75 daily per family member when you cannot cook at home. Document every expense with receipts (including pet boarding, storage units, and commuting costs to temporary housing).

Digital Documentation Accelerates Claims Processing

The National Association of Insurance Commissioners reports that homeowners with detailed inventories receive claim settlements 40 percent faster than those without proper documentation. Photograph every room from multiple angles quarterly and focus on serial numbers for electronics and appliances.

Store digital copies in cloud storage separate from your home, including purchase receipts and appraisal documents for valuable items. Video walkthroughs work better than photos for capturing room contents comprehensively. Update your inventory immediately after major purchases, home improvements, or seasonal decoration changes.

Professional appraisals for jewelry, art, and collectibles worth over $2,500 provide concrete values that adjusters cannot dispute during settlement negotiations (making the claims process smoother and more accurate).

Final Thoughts

Fire damage protection requires three essential elements: adequate coverage limits, comprehensive documentation, and proactive risk reduction. Utah homeowners need dwelling coverage at 100 percent replacement cost, extended additional living expenses protection, and detailed home inventories that they update quarterly. Prevention strategies like defensible space creation and fire-resistant materials work alongside proper insurance to minimize both risk and financial exposure.

Local Utah agents provide distinct advantages over national carriers or online platforms when you need homeowners insurance for fire damage coverage. We at Archibald Insurance Agency understand Utah’s unique wildfire risks, construction costs, and seasonal weather patterns that affect coverage needs. Our agency represents multiple carriers, which allows us to compare options and find policies that match your specific property location and risk profile.

Review your current policy immediately by checking dwelling coverage amounts against current construction costs and verifying additional living expenses limits exceed 20 percent of dwelling coverage. Confirm your personal property inventory reflects recent purchases (including any valuable items acquired in the past year). Schedule annual policy reviews after major home improvements or market changes, and contact your agent within 30 days of any home modifications that could affect replacement costs or fire risk factors.