Why Life Insurance for Young Adults is a Smart Move

Life insurance for young adults often feels like something to worry about later. But the truth is, your twenties and thirties are the best time to get coverage.

At Archibald Insurance Agency, we’ve seen how affordable premiums are when you’re young and healthy. Waiting even a few years can cost you thousands more in the long run.

The Real Cost of Waiting

Your age right now determines how much you’ll pay for life insurance for the next two or three decades. The average cost of life insurance is $26 a month in your twenties, and waiting until your thirties means paying more per month. Waiting until your fifties significantly increases your monthly premium. Waiting just ten years can triple your monthly premium. This isn’t a minor difference you can absorb later. Lock in coverage today, and you protect yourself against rate increases that compound over time.

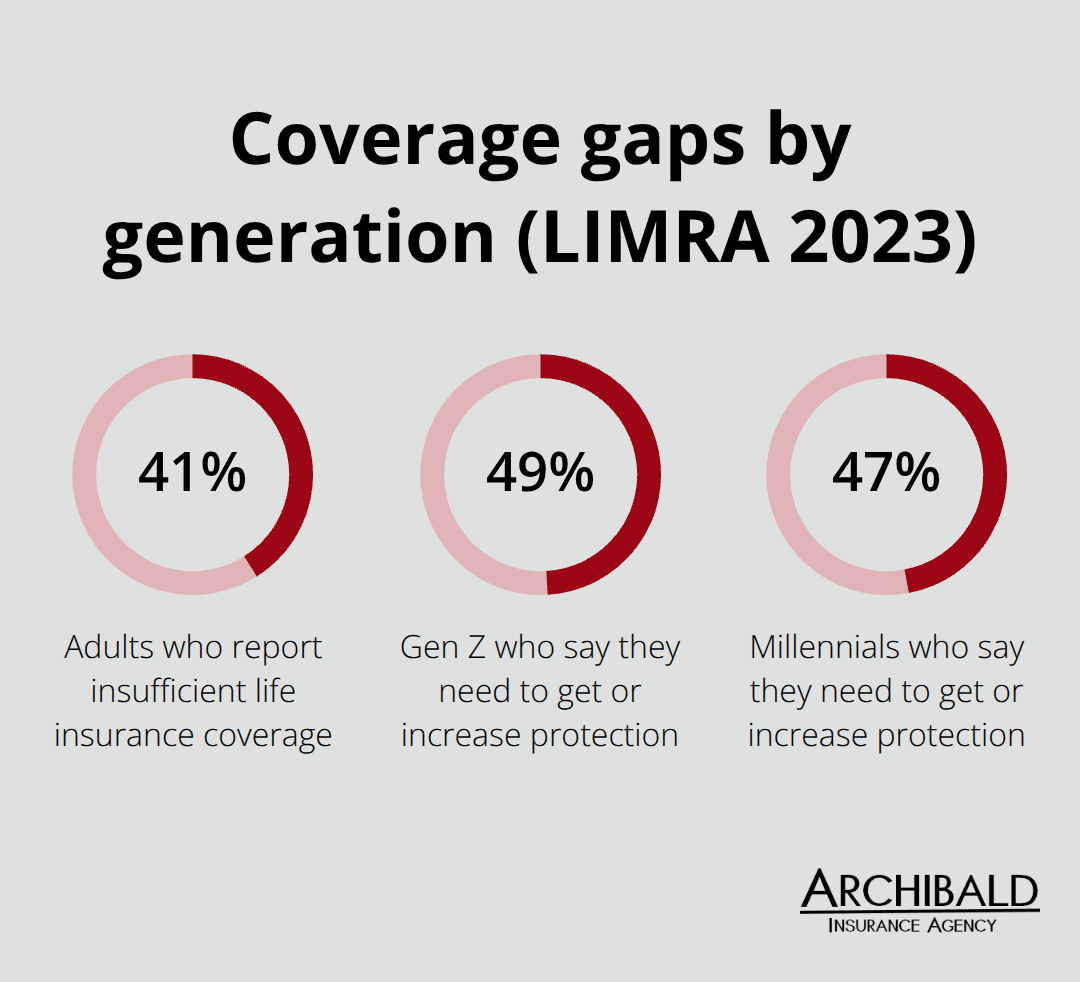

Health changes drive most of this cost difference. Insurance companies view younger applicants as lower risk because they typically have fewer pre-existing conditions and longer life expectancies. Once you develop high blood pressure, diabetes, or any chronic condition, insurers either deny you coverage outright or charge significantly more. The LIMRA and Life Happens 2023 Insurance Barometer found that 41% of people report having insufficient life insurance coverage, with 49% of Gen Z and 47% of millennials saying they need to get or increase protection. This gap exists partly because people assume they can purchase coverage whenever they want. That assumption costs money.

Why Your Twenties Matter Most

Getting approved for favorable rates becomes harder as you age and your health profile changes. A healthy 25-year-old qualifies for standard rates; a 35-year-old with the same health might face higher premiums or additional scrutiny. Young people also carry real financial obligations that need protection. The average federal student loan debt is $39,075, with private student loan debt also representing a significant burden. If you co-signed those loans, your family inherits that debt if something happens to you. Life insurance covers this gap.

Calculating Coverage That Fits Your Life

A practical coverage target is five to ten times your annual income, adjusted for your debts and any dependents you plan to have. Someone earning $50,000 annually with $30,000 in student loans should consider at least $250,000 to $500,000 in coverage. That protection costs significantly less now than it will later. Starting early also means you build flexibility into your financial plan. You’re not locked into permanent decisions. Term policies last ten, twenty, or thirty years, giving you time to evaluate whether whole life makes sense as you accumulate assets and wealth.

The younger you start, the more options remain available to you. This flexibility becomes important as your life evolves and your financial priorities shift. Understanding what coverage amount actually protects your situation sets the foundation for choosing the right policy type.

What’s Holding Young Adults Back From Life Insurance

Many young adults convince themselves that life insurance is something to handle after they’ve built their career or started a family. This delay costs money and creates unnecessary risk. The reality is simpler than most people think. You don’t need to wait for a specific life milestone to benefit from coverage. You need coverage now because your current health and age are your greatest assets in the insurance market. The LIMRA and Life Happens 2023 Insurance Barometer shows that 49% of Gen Z and 47% of millennials acknowledge they need life insurance but haven’t acted yet. The reasons they cite reveal common misconceptions that cost them thousands in premiums over time.

Debt Protection Matters Right Now

Many young adults believe life insurance only matters once they have dependents. This ignores the real financial obligations you carry right now. Student loans, car payments, credit card debt, and co-signed loans don’t disappear if something happens to you. They transfer to whoever co-signed or to your estate. If your parents co-signed your student loans, they become responsible for repayment. Life insurance covers this gap and protects the people who helped you. Someone earning $45,000 annually with $35,000 in student debt has genuine financial obligations that require protection. The cost to cover those obligations runs roughly $30 to $50 per month in your twenties. Waiting ten years means paying $80 to $150 per month for the same coverage. That’s not a small difference. The math favors action now, not later.

Complexity Disappears When You Focus on Basics

Life insurance feels complicated because the industry uses technical language. Strip away the terminology, and the core choice is straightforward. Term life insurance covers you for a set period at a fixed monthly cost. If you die during that term, your beneficiaries receive the payout. If the term expires and you’re still living, coverage ends. Whole life insurance lasts your entire life, costs significantly more monthly, and includes a cash value component you can access. For someone in their twenties, term life solves the actual problem at a price you can afford. You’re not choosing between 47 different policy structures. You’re choosing between temporary affordable coverage and permanent expensive coverage. Most young adults benefit from term life because it protects their obligations during their earning years when they’re most financially vulnerable. That’s the decision. Everything else is details your insurance agent can explain in five minutes.

Why Your Health Status Matters More Than You Think

Insurance companies view younger applicants as lower risk because they typically have fewer pre-existing conditions and longer life expectancies. Once you develop high blood pressure, diabetes, or any chronic condition, insurers either deny you coverage outright or charge significantly more. A healthy 25-year-old qualifies for standard rates; a 35-year-old with the same health might face higher premiums or additional scrutiny. Getting approved for favorable rates becomes harder as you age and your health profile changes. Young people also carry real financial obligations that need protection. The average federal student loan debt sits at $39,075, with private student loan debt also representing a significant burden. Your twenties and thirties represent a window of opportunity that closes as you age. Understanding what coverage amount actually protects your situation sets the foundation for choosing the right policy type and moving forward with confidence.

Picking the Right Policy for Your Situation

The choice between term and permanent life insurance determines how much you pay and what protection you actually get. Term life covers you for a specific period-typically ten, twenty, or thirty years-at a fixed monthly cost. If you die during that term, your beneficiaries receive the full payout. Permanent life insurance, which includes whole life and universal life policies, lasts your entire lifetime and builds cash value over time. For someone in their twenties earning $45,000 to $60,000 annually, term life solves the actual problem. A twenty-year term policy costs roughly $165 per year according to Policygenius data, while whole life for the same person runs closer to $2,400 annually. That’s a difference of $195 per month. Whole life makes sense once you’ve built substantial assets and want lifelong protection with a savings component. Right now, term life protects your student loans, car payments, and future family obligations without consuming your monthly budget. The math is straightforward: term life gives you the coverage you need at a price that doesn’t force trade-offs with other financial goals.

How Much Coverage Actually Protects You

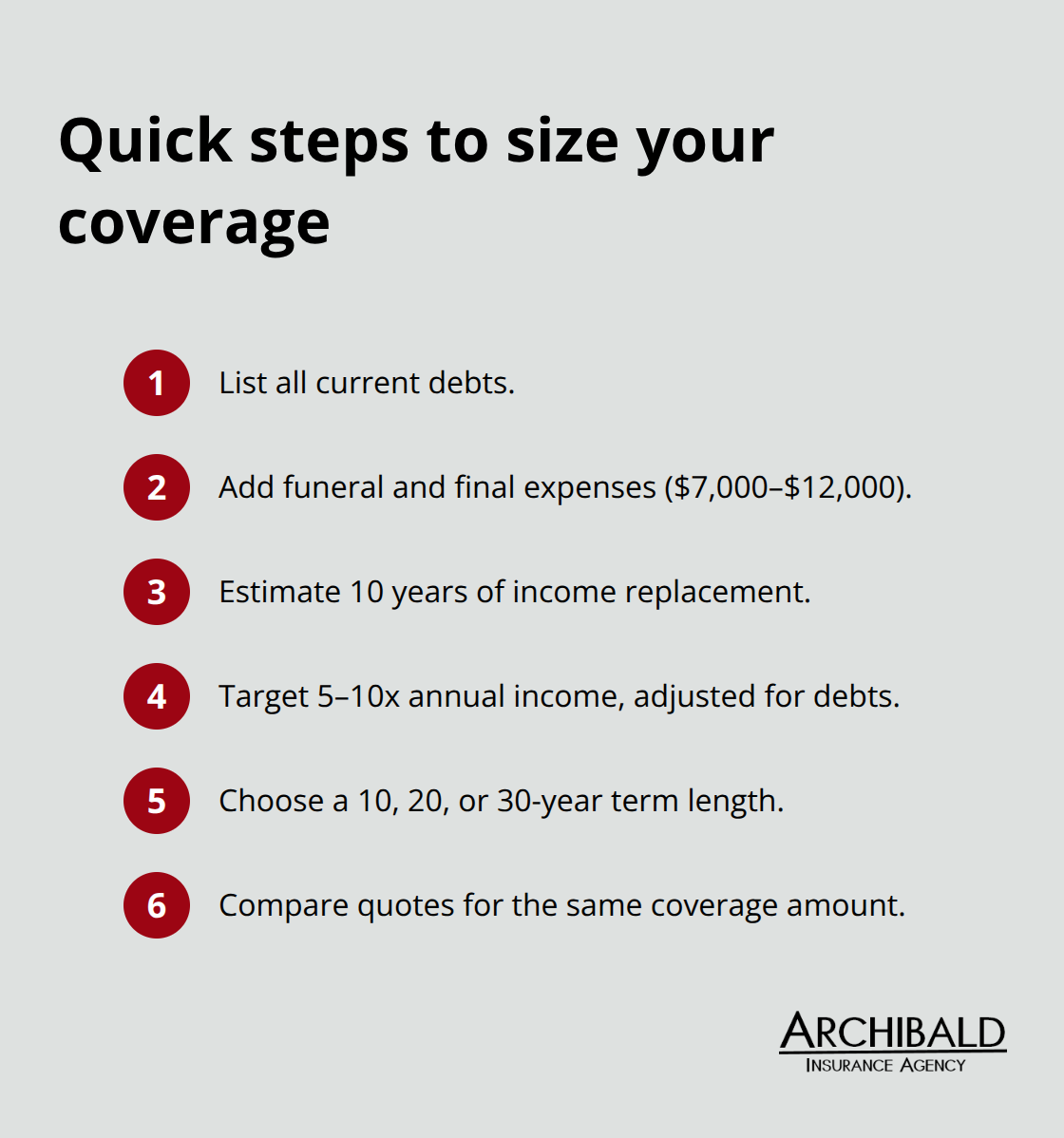

The five to ten times annual income rule works as a starting point, but your actual number depends on what you’re protecting. Someone with $35,000 in student debt, a $25,000 car loan, and plans to marry and have children within five years needs different coverage than someone with minimal debt and no dependents. List your current debts first. Add the cost of your funeral and final expenses, roughly $7,000 to $12,000. Then estimate ten years of income replacement for any dependents you plan to have.

Someone earning $55,000 with $40,000 in debt and planning a family should target $400,000 to $500,000 in coverage. That amount costs roughly $35 to $50 monthly at age twenty-five. The coverage amount matters because underinsurance leaves your family vulnerable while overinsurance wastes money on premiums you don’t need. Work backwards from your actual obligations rather than picking an arbitrary number. This approach also simplifies comparing quotes across carriers-you’re shopping for the same coverage amount, so price differences become clear.

Comparing Carriers and Getting Real Quotes

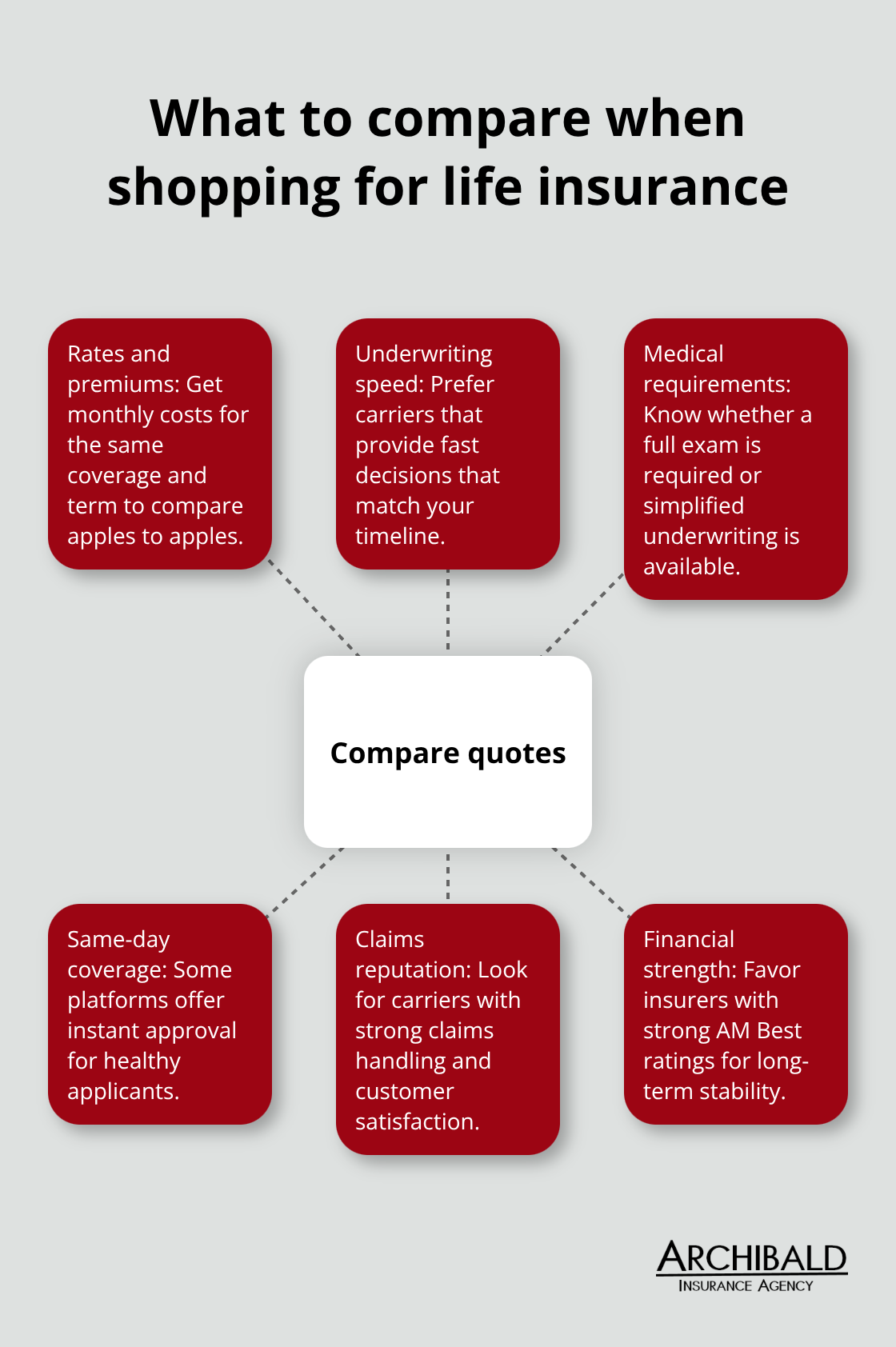

Shopping for life insurance in Utah means evaluating carriers based on their rates, underwriting speed, and claims reputation. Some insurers require full medical exams while others offer simplified underwriting with just health questions, delivering quotes and approval within days. Platforms like Ethos provide same-day coverage for healthy applicants, eliminating the weeks-long underwriting process traditional carriers require.

Try getting quotes from at least three carriers for the same coverage amount and term length. A $350,000 twenty-year term policy might cost $32 per month with one carrier and $41 with another-that’s $2,700 in difference over the full term. When you evaluate quotes, verify that the rate is guaranteed for the full term and check whether the carrier has a strong AM Best financial rating. You’re not choosing based on brand recognition. You’re choosing based on the actual monthly cost for the coverage you need, combined with carrier stability and underwriting speed that fits your timeline. A life insurance agent can help you compare options and find the right policy for your situation.

Final Thoughts

Life insurance for young adults protects the financial obligations you carry right now at a price that fits your budget. A $350,000 policy costs roughly $35 monthly in your twenties but $100 or more in your forties-that difference compounds over decades and costs you thousands in unnecessary premiums simply because you waited. The real advantage of acting now isn’t just the lower monthly cost; it’s the certainty that you’ll qualify for coverage at standard rates while your health remains stable.

Once you develop a chronic condition, insurers either deny you or charge premiums that make protection unaffordable. Your twenties and thirties represent a window that doesn’t stay open forever, and locking in coverage today means you won’t scramble to find affordable options later when your health situation has changed. A twenty-year term policy purchased at twenty-five expires when you’re forty-five, giving you time to reassess whether permanent coverage makes sense once you’ve built substantial assets.

Determine what you’re actually protecting, obtain quotes from multiple carriers for that specific coverage amount, and select the policy that offers the best rate with a financially stable insurer. We at Archibald Insurance Agency work with numerous carriers to find personalized solutions that fit your specific needs and budget, and our team can walk you through the comparison process and answer questions about coverage amounts, policy types, and underwriting timelines. Contact us today to get real quotes and move forward with the protection your financial future deserves.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation