Homeowners Insurance Loss of Use Coverage Benefits

Your home is your biggest investment, and homeowners insurance protects it. But standard coverage has gaps that many Utah homeowners overlook.

Loss of use coverage fills one of those critical gaps. When a disaster forces you out of your home, this protection covers your temporary living expenses while repairs happen. We at Archibald Insurance Agency see firsthand how this coverage saves families thousands of dollars during their most stressful moments.

What Loss of Use Coverage Actually Covers

Understanding Additional Living Expenses

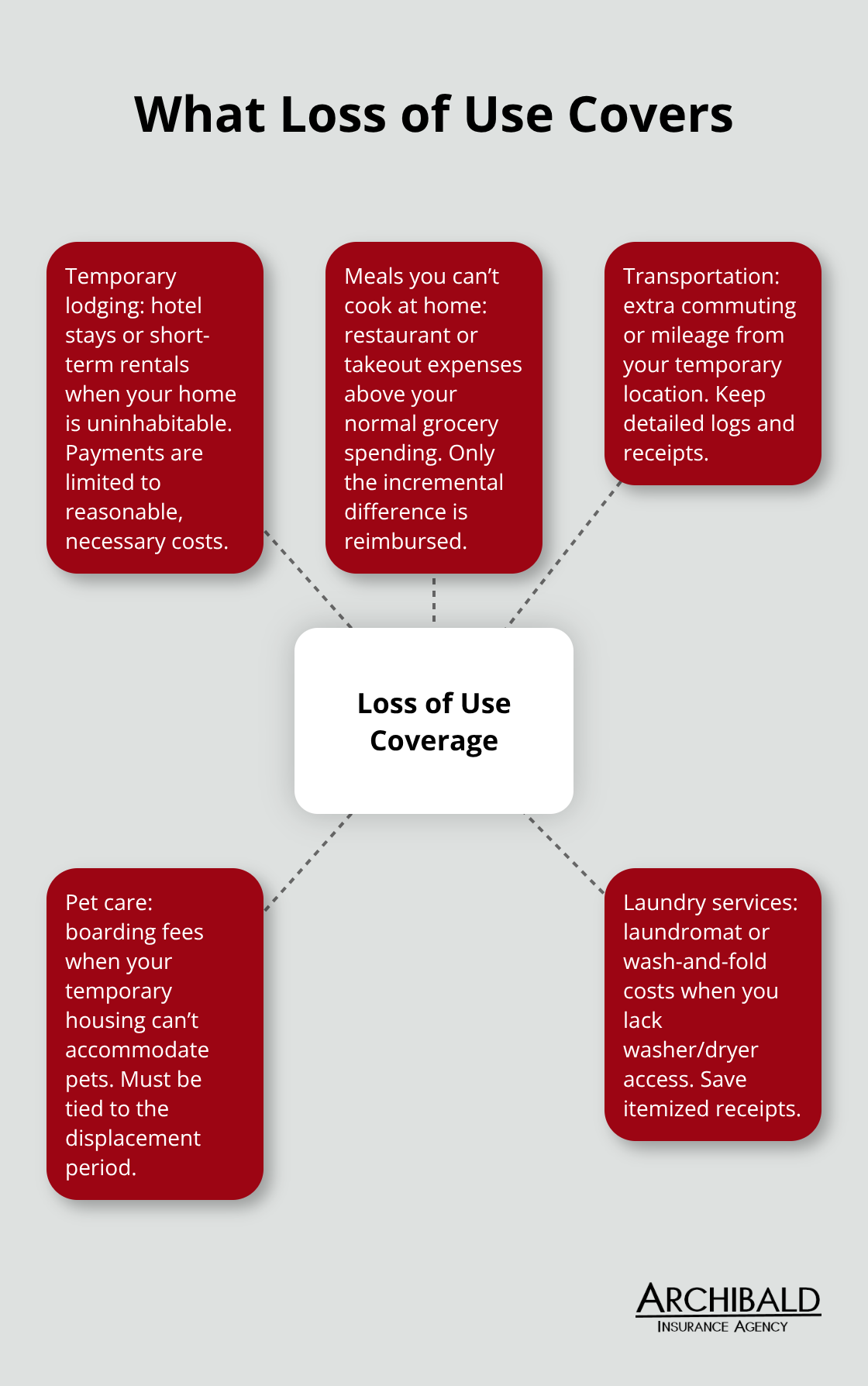

Loss of use coverage, formally called Additional Living Expenses or Coverage D, reimburses the extra costs you pay when a covered disaster makes your home uninhabitable. This protection addresses the gap between what you normally spend to live and what you must spend while displaced. When a fire, severe hail damage, or other covered peril forces you out, this coverage pays for hotel rooms, temporary rentals, meals you cannot prepare at home, pet boarding, extra transportation costs, and laundry services.

How Much Coverage You Need

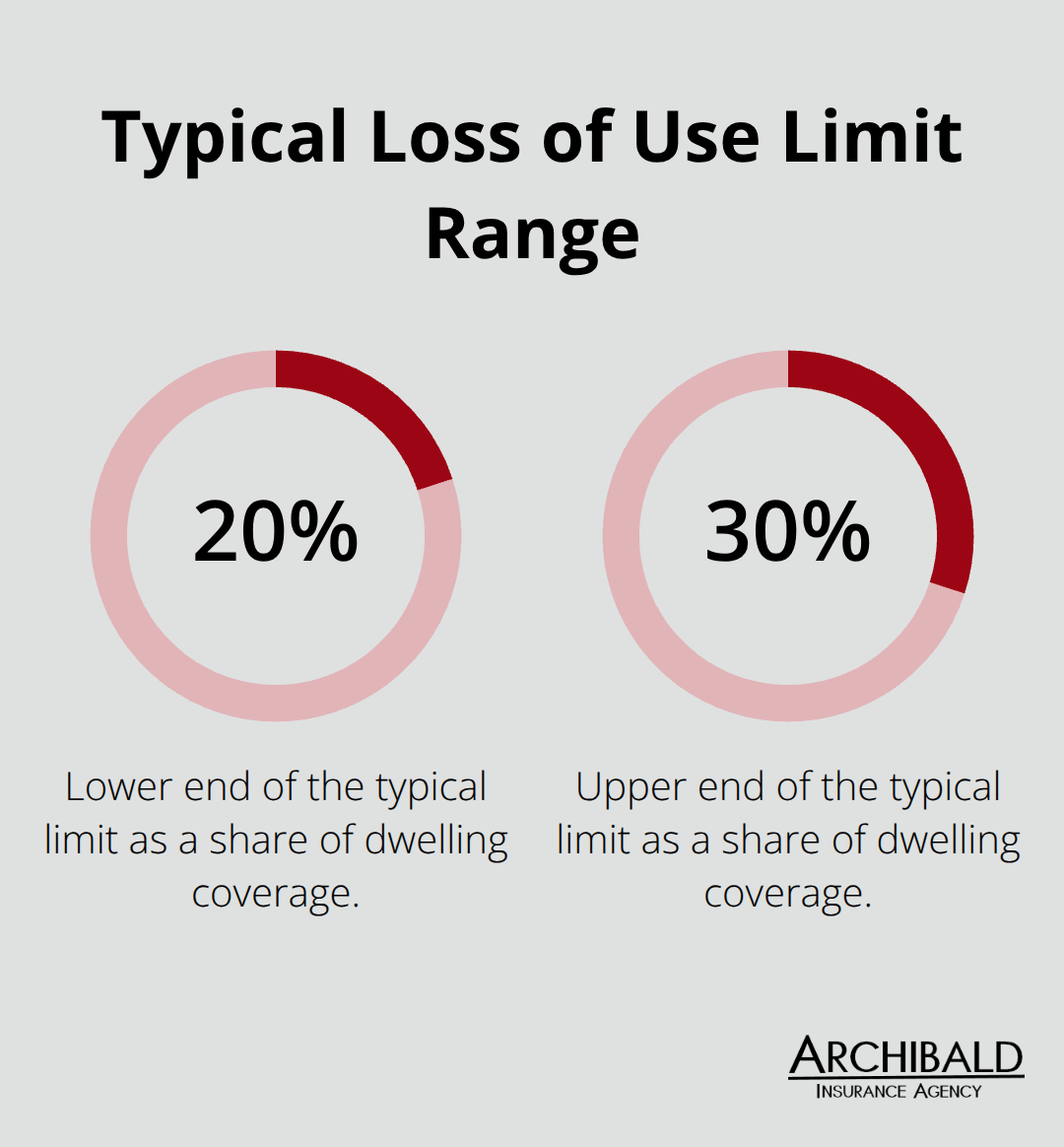

The typical limit runs 20 to 30 percent of your dwelling coverage, so a home insured for $300,000 might carry $60,000 to $90,000 in loss of use protection. Utah homeowners should understand that this coverage only applies to perils named in your policy-flood damage, for example, requires separate flood insurance to trigger loss of use benefits. Most policies cap loss of use reimbursements for 12 to 24 months, though some carriers offer longer periods depending on the claim circumstances.

What Loss of Use Actually Reimburses

The coverage pays actual incremental expenses, not upgrades or luxuries. If you normally spend $200 weekly on groceries and temporarily spend $400 because you eat restaurant meals, you recover the $200 difference, not the full restaurant bill. Similarly, the coverage will not reimburse your mortgage, property taxes, or utilities you would owe regardless of displacement. This distinction matters because many homeowners mistakenly assume loss of use covers all temporary living costs without limits.

Documentation Makes the Difference

To file successfully, keep itemized receipts for every cost-hotels, meals, gas, parking, pet care-and document your baseline living expenses before the loss. The claims process moves faster when you report the incident promptly and provide clear documentation early. Utah’s rising construction costs and housing market volatility make adequate loss of use limits more important than ever, since temporary lodging and meal costs climb when repairs stretch longer than expected. Your insurance agent can help you understand what documentation the carrier requires and how to organize your records for a smooth claims experience.

When Disaster Strikes Your Home

Fire and Storm Damage Force Immediate Displacement

A structure fire in Salt Lake City forces your family to evacuate in the middle of the night. Within hours, your home is uninhabitable, and you stand in a hotel lobby at 11 PM trying to figure out how to afford a room for the next month while contractors assess the damage. Loss of use coverage transforms this nightmare into a manageable situation by paying your hotel costs, restaurant meals because your kitchen no longer exists, and even pet boarding if you had to leave your dog with a friend temporarily. The National Association of Home Builders estimates that tariffs and rising material costs could add nearly $11,000 to new home construction, meaning roof repairs and fire damage repairs stretch longer than they did five years ago. When repairs take weeks or months instead of days, loss of use coverage becomes the difference between financial stability and depleting your savings account.

A severe hail storm that damages your roof and makes your home unsafe for occupancy triggers the same protection. Your coverage pays for your temporary apartment rental, the difference between your normal grocery budget and restaurant meals while displaced, extra mileage to drive to work from a temporary location, and even laundry services since you lack access to your home’s washer and dryer. Theft or vandalism that forces you out while repairs happen also qualifies, though you must verify your specific policy includes coverage for these perils since some carriers exclude certain types of loss. The key distinction is that loss of use only activates when a covered peril makes your home genuinely uninhabitable, not when you choose to leave or when damage is minor.

Documentation Determines Your Full Recovery

Documentation determines whether you recover every dollar owed to you. You must keep receipts for hotel bills, restaurant charges, gas purchases for extra commuting, pet boarding invoices, and any other incremental costs you incur while displaced. Utah’s housing market volatility means temporary rentals in Salt Lake City or Park City can easily cost $2,500 to $4,500 monthly for a short-term lease, far exceeding what you would normally spend on housing if you were not displaced. A single month of displacement without adequate loss of use coverage could cost your family $5,000 to $8,000 in out-of-pocket expenses when you factor in lodging, meals, transportation, and other necessities.

Speed Up Your Claim with Prompt Reporting

You should report the loss to your insurance carrier immediately after evacuation or displacement occurs, because early reporting often triggers faster claim processing and sometimes allows the carrier to provide partial advance payments while you accumulate receipts. Utah’s rising construction costs and housing market volatility make adequate loss of use limits more important than ever, since temporary lodging and meal costs climb when repairs stretch longer than expected. The standard 20 to 30 percent of dwelling coverage may fall short if repairs extend beyond three months or if you live in a high-cost area where short-term rentals command premium prices. Your insurance agent can help you understand what documentation the carrier requires and how to organize your records for a smooth claims experience.

Setting Your Loss of Use Limit to Match Your Real Costs

Calculate Your True Monthly Displacement Costs

Most Utah homeowners accept the default 20 to 30 percent loss of use limit without calculating what they actually need, which often leaves them underinsured when displacement happens. Start with your baseline monthly expenses-not what you wish you spent, but what you actually spend on housing, food, transportation, and other necessities. Add up twelve months of bank and credit card statements to find your true average, then multiply by the number of months you estimate repairs might take. A roof replacement in Utah typically takes three to six months depending on weather and contractor availability, while major structural damage from fire or severe hail can stretch to nine or twelve months. If your normal monthly expenses run $5,000 and repairs take six months, you need at least $30,000 in loss of use coverage just to maintain your current lifestyle during displacement-yet many Utah homeowners carry only $20,000 or $25,000 because they never performed this calculation.

Account for Utah’s Temporary Housing Premium

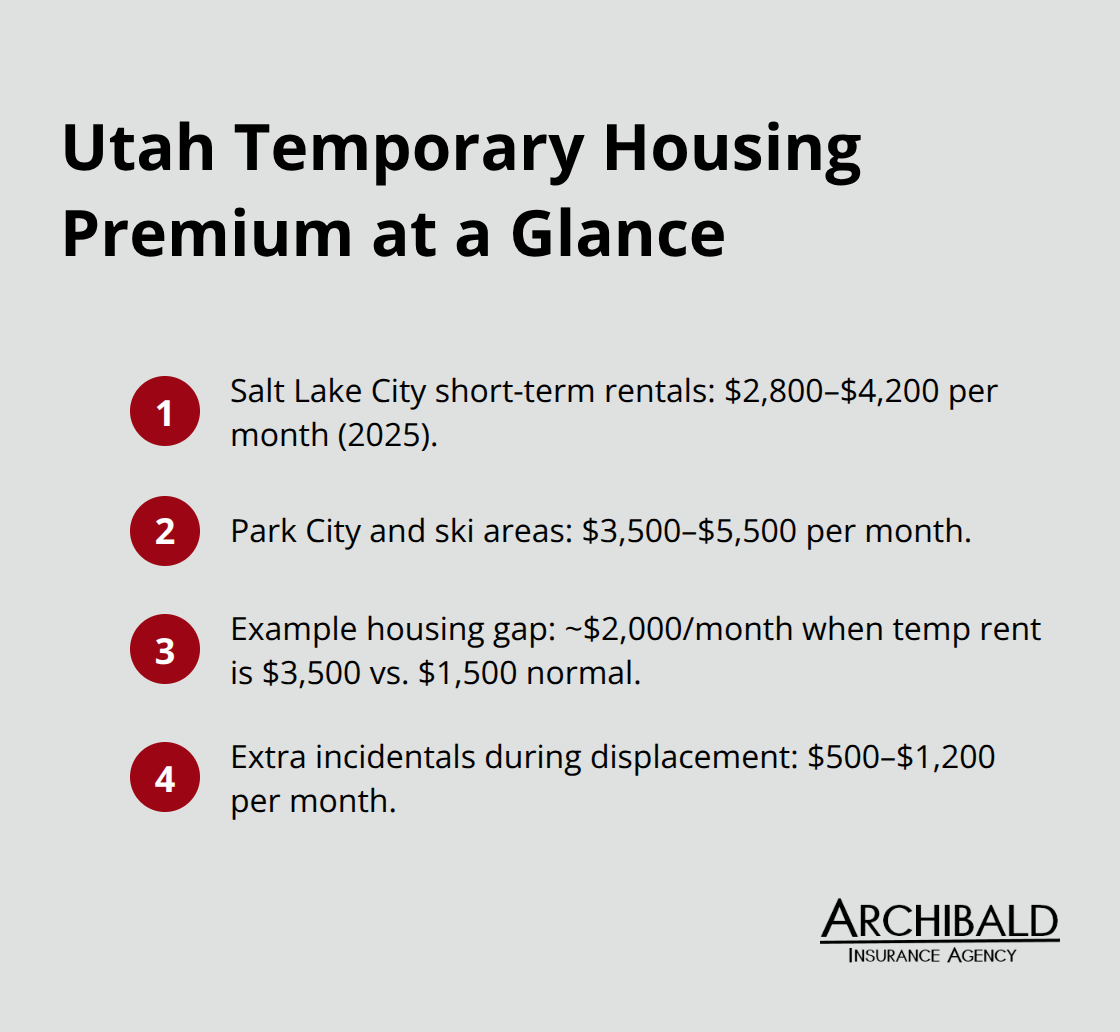

Utah’s housing market creates a second problem: temporary rental costs far exceed your normal housing expense. Salt Lake City short-term rentals averaged $2,800 to $4,200 monthly in 2025, while Park City and ski resort areas command $3,500 to $5,500 for comparable units.

If your mortgage or normal rent is $1,500 monthly but temporary housing costs $3,500, you face a $2,000 monthly gap that loss of use coverage must fill. Add restaurant meals because your displaced kitchen limits cooking, pet boarding if you cannot keep your dog in a temporary apartment, extra transportation costs to commute from a rental across town, and laundry service fees since your temporary housing lacks washer and dryer access. These incremental costs easily reach $500 to $1,200 monthly on top of the housing difference.

Determine Your Adequate Coverage Amount

A family with $5,000 monthly baseline expenses facing a six-month displacement in a high-cost Utah market should carry $45,000 to $50,000 in loss of use coverage, not the $30,000 that 20 percent of a typical $150,000 dwelling limit provides. Underestimating this coverage leaves you paying thousands out-of-pocket during the worst time. Your specific situation depends on your family’s actual displacement expenses and local Utah housing costs, which vary significantly between Salt Lake City, Park City, and rural areas. An independent insurance agent who understands your community’s market conditions can help you set limits that match your real needs rather than accepting a percentage-based default that may fall short when you need protection most.

Final Thoughts

Loss of use coverage protects your family when disaster forces you from your home, and without it, you face thousands in out-of-pocket expenses for temporary housing, meals, and transportation while repairs happen. Utah homeowners often underestimate what they need because they accept default coverage limits without calculating their actual displacement costs-a six-month repair period in a high-cost Utah market can easily cost $30,000 to $50,000 when you factor in temporary rental premiums, restaurant meals, and extra commuting expenses. The 20 to 30 percent default limit frequently falls short, leaving families vulnerable to significant financial strain.

Your homeowners insurance loss of use coverage only activates when a covered peril makes your home genuinely uninhabitable, and fire, severe hail damage, theft, and vandalism all trigger this protection (though flood damage requires separate flood insurance). Check your current homeowners insurance loss of use coverage limit against your actual monthly expenses and local Utah housing costs right now, before disaster strikes. If you carry only $20,000 or $25,000 in coverage but face potential displacement in Salt Lake City or Park City, you are almost certainly underinsured.

We at Archibald Insurance Agency help Utah families set loss of use limits that match their real needs rather than accepting percentage-based defaults, and our team understands Utah’s housing market volatility and can guide you through calculating adequate coverage for your specific situation. Contact us today to review your homeowners policy and ensure your family has the protection you need when displacement happens.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation