Personal Property Coverage Homeowners Insurance Guide

Your homeowners insurance policy protects your house, but personal property coverage homeowners insurance is what shields your belongings inside it. Most Utah homeowners underestimate what they actually own, which leaves them vulnerable to significant financial loss if theft, fire, or other damage strikes.

We at Archibald Insurance Agency help homeowners understand exactly what their personal property coverage includes and where the gaps might be. This guide walks you through the coverage types, limits, and practical steps to make sure your belongings are truly protected.

What Personal Property Coverage Actually Protects

Personal property coverage may protect your belongings against fire, theft, and other covered perils outlined in your policy. This isn’t about your house itself-dwelling coverage handles that. Personal property coverage protects everything inside: furniture, clothing, electronics, tools, jewelry, art, bicycles, and musical instruments.

In Utah, this coverage typically equals about 50% of your dwelling coverage amount. If your home is insured for $200,000, you’d likely have around $100,000 in personal property coverage unless you’ve adjusted it. This percentage-based approach means coverage automatically adjusts when you increase your dwelling limit, but it also means you might be underinsured if you own significant valuables. Most homeowners never calculate what their belongings actually cost to replace, which is why this coverage frequently falls short when claims happen.

Understanding Your Coverage Limits and What They Mean

Your policy states a maximum dollar amount the insurer will pay for personal property losses, minus your deductible. If you have $100,000 in personal property coverage and a $1,000 deductible, the insurer pays up to $99,000 for a covered loss. However, certain categories face additional sublimits-restrictions on specific items regardless of your total coverage. Cash typically has a $200 sublimit, jewelry often maxes out at $1,500, and firearms might be capped at $2,500. If you own a $15,000 engagement ring, that $1,500 sublimit leaves you exposed to a $13,500 gap. This is where scheduled personal property coverage becomes essential. For high-value items, you add a rider to your policy listing each piece with its appraised value, which removes the sublimit restriction. The process requires a professional appraisal and clear photographs, but it guarantees full coverage for those specific items. Many Utah homeowners skip this step because they assume their standard coverage is enough, then face devastating shortfalls after losses.

Actual Cash Value Versus Replacement Cost

Two settlement methods exist, and your choice between them dramatically affects what you receive after a claim. Replacement cost coverage pays what it costs to replace your item new at today’s prices. If your five-year-old laptop suffers destruction and costs $1,200 to replace with an equivalent model, replacement cost pays $1,200 minus your deductible. Actual cash value (ACV) pays based on its value at the time of loss. That same laptop might be worth only $600 under ACV because of depreciation over five years. The difference compounds across dozens of items in a claim. A living room full of furniture, kitchen appliances, and electronics can result in thousands of dollars less under ACV. Replacement cost premiums cost more-typically 10-15% higher-but they provide actual replacement value rather than a reduced amount. Most Utah homeowners choose replacement cost when they understand the real difference, but some policies default to ACV. Check your declarations page to confirm which method your policy uses, and contact your agent if you need to switch.

Identifying Which Items Face Coverage Gaps

Standard personal property coverage protects most household items, but certain belongings face exclusions or limits that leave you vulnerable. Flood damage requires a separate flood insurance policy-your homeowners coverage won’t pay for water damage from rising water or heavy rainfall. Earthquake and earth movement also fall outside standard coverage. Items used for business purposes (equipment, inventory, or supplies) typically aren’t covered if you operate a home-based business. Pets and automobiles have their own separate insurance policies. Items that belong to non-relatives living with you may not be covered under your policy. High-value collectibles, art, and rare items often exceed standard sublimits and need scheduled coverage to be fully protected. Understanding these gaps now prevents the shock of a denied claim later. The next section walks you through how to document what you own and determine the right coverage limits for your specific situation.

Coverage Types That Actually Matter

Replacement Cost Versus Actual Cash Value

Replacement cost coverage and actual cash value represent fundamentally different approaches to paying your claims, and Utah homeowners who pick the wrong one face serious financial consequences. Replacement cost pays what it costs to buy a new item today. If your eight-year-old refrigerator fails and a new equivalent model costs $1,800, replacement cost covers that $1,800 minus your deductible. Actual cash-value coverage applies depreciation, so that same refrigerator might only be worth $600 because of its age.

Across a full household claim involving furniture, appliances, electronics, and clothing, the gap between these two methods easily reaches $10,000 to $20,000. A homeowner with a $150,000 personal property limit and actual cash value coverage might receive only $75,000 in actual replacement funds after depreciation. Replacement cost costs approximately 10-15% more in premiums, but this modest increase prevents devastating underpayment when you need it most. Utah homeowners should prioritize replacement cost coverage for personal property, especially given rising inflation in construction and replacement costs.

Check your policy declarations page right now to confirm which method your insurer applies, because this choice has already been made for you and many policies default to actual cash value.

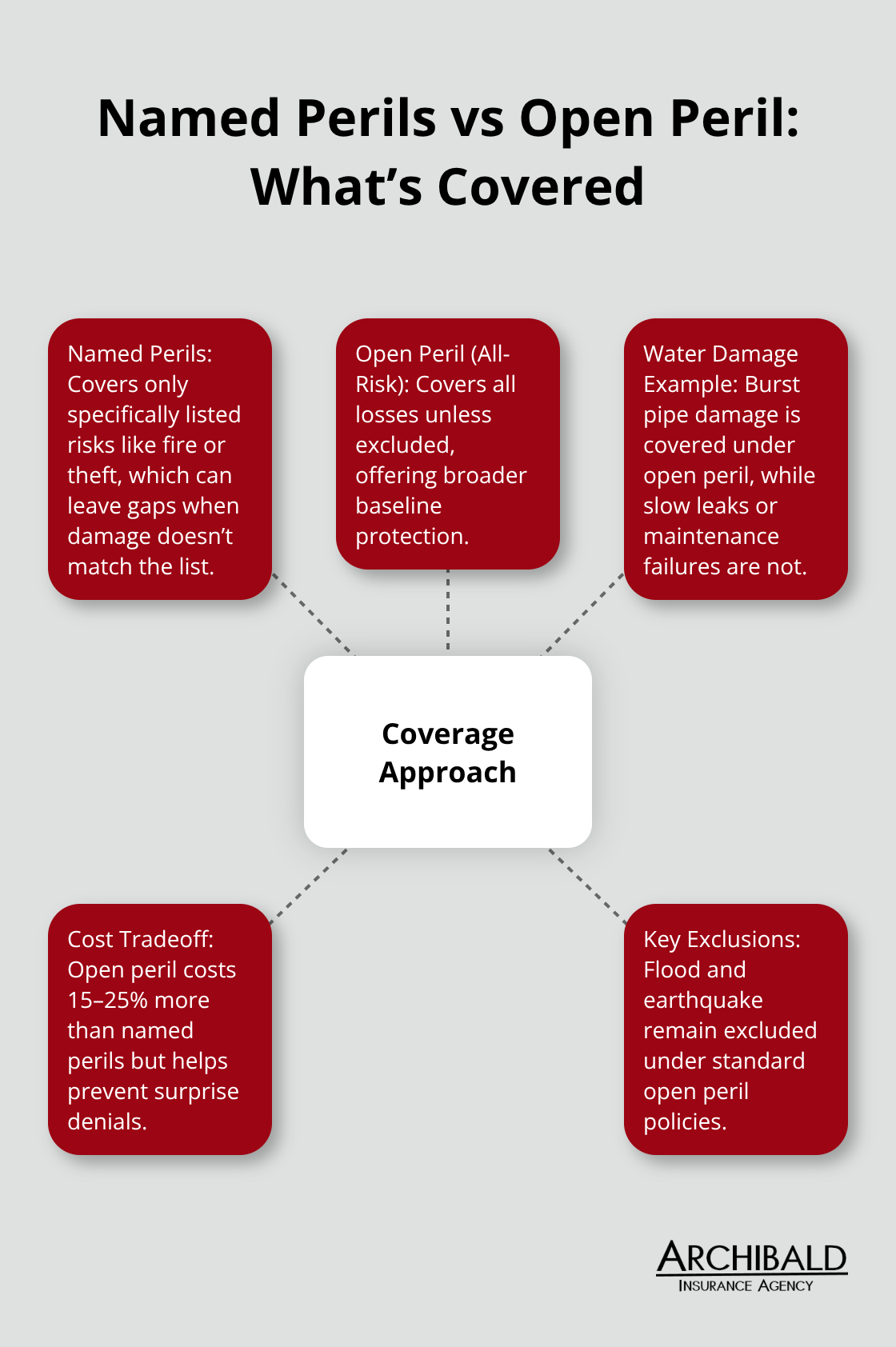

Named Perils Versus Open Peril Coverage

Named perils versus open peril coverage protects against specific listed risks like fire, theft, windstorm, and hail, while open peril coverage (also called all-risk) protects against virtually everything except explicitly excluded perils. Named perils policies cost less upfront but leave dangerous gaps. A water pipe bursts inside your wall and damages electronics and furniture, but the policy only covers sudden and accidental water damage, not slow leaks or maintenance failures.

You file a claim and face denial because the damage doesn’t match the named perils list.

Open peril coverage flips this approach by covering all losses unless your policy specifically excludes them. Flood and earthquake remain excluded under standard open peril policies, but water damage from a burst pipe is covered. Open peril costs 15-25% more than named perils, but the broader protection prevents coverage surprises. Loss of use coverage also protects your family when disaster strikes and you cannot stay in your home.

Scheduled Personal Property Coverage for Valuables

High-value items require scheduled personal property coverage regardless of your peril type. Scheduling means listing specific items like jewelry, art, or collectibles on a rider with their appraised values. A $12,000 engagement ring with a standard $1,500 jewelry sublimit needs scheduling to receive full coverage. The appraisal process takes 1-2 weeks and costs $75-150 per item, but it removes sublimit restrictions entirely.

Utah homeowners with valuables totaling more than $5,000 should seriously consider scheduling because standard sublimits create unacceptable risk for items you truly cannot afford to lose. Once you understand which coverage types fit your situation, the next step involves documenting exactly what you own and calculating the right limits for your household.

How to Actually Protect What You Own

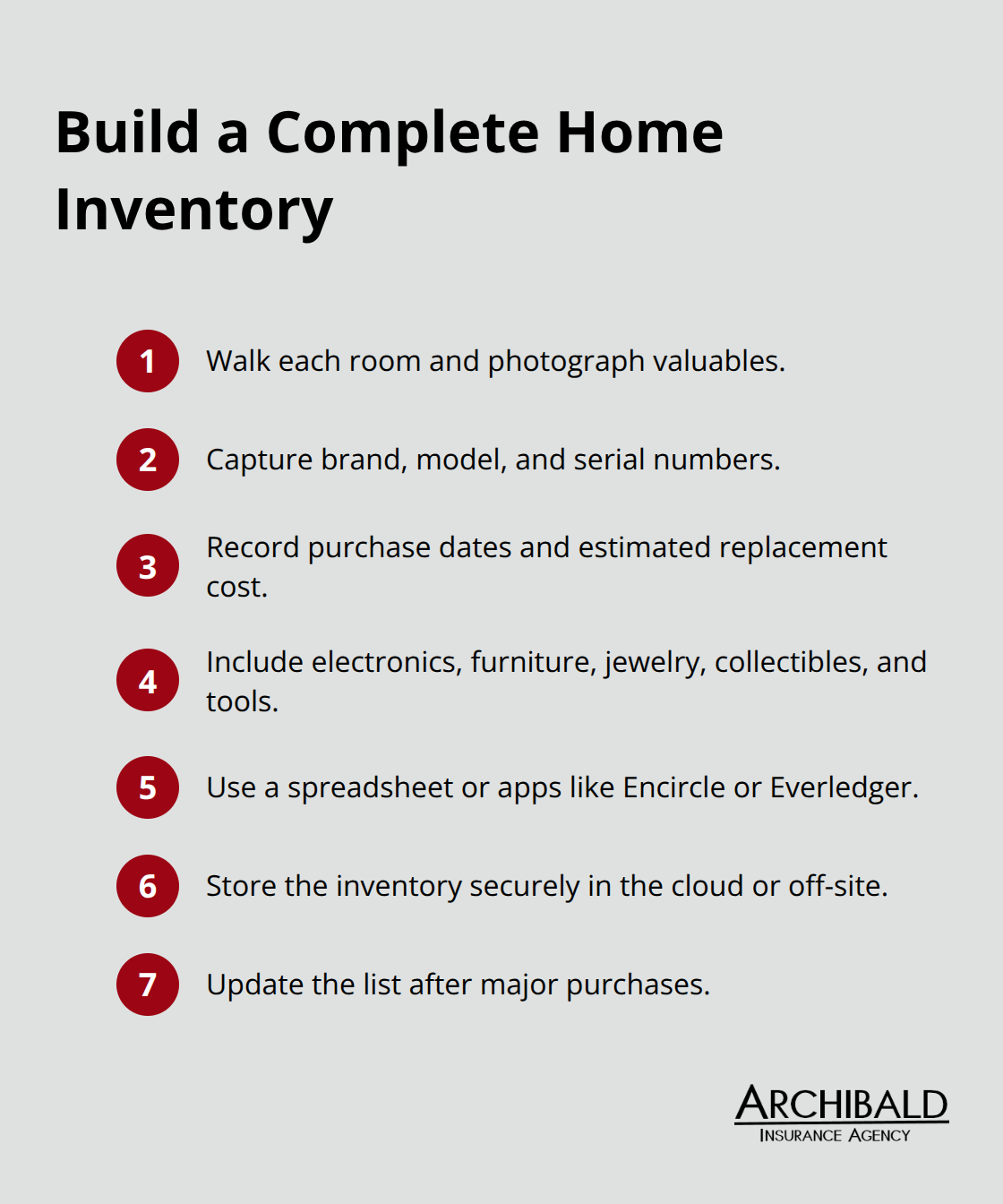

Document Your Belongings with a Complete Home Inventory

Most Utah homeowners skip the hard work of documenting their belongings, then face rejection when filing claims because they cannot prove what they owned. Start your home inventory immediately by walking through each room with your phone camera and photographing items you would struggle to replace. Expensive electronics, furniture, jewelry, collectibles, and tools deserve close-up photos showing brand, model, and serial numbers whenever visible.

The Insurance Information Institute recommends listing make, model, serial number, purchase date, and estimated replacement cost for each significant item. A $3,000 television needs documentation just as much as a $15,000 diamond necklace does. Spreadsheets work fine, but dedicated inventory apps like Encircle or Everledger streamline the process by organizing photos, values, and categories automatically.

Store your completed inventory somewhere safe outside your home-cloud storage, email to yourself, or a safe deposit box all work-because a fire that destroys your belongings will also destroy paper copies kept in your house. This inventory becomes your strongest weapon when a claim adjuster questions what you actually owned and what it cost to replace.

Identify Coverage Gaps Before Disaster Strikes

Your standard personal property coverage protects against sudden, accidental losses rather than predictable aging and deterioration, which means Utah homeowners in flood-prone areas or older homes with aging pipes need separate riders or policies to cover these risks. Business equipment and inventory stored at home fall outside personal property coverage entirely, requiring a separate business policy if you operate a home-based business.

Jewelry and cash face strict sublimits that force you to choose between accepting inadequate coverage or paying for scheduled items coverage with professional appraisals. Understanding these gaps now prevents the painful discovery of exclusions after disaster strikes.

Calculate Your Actual Coverage Needs

Calculate your total personal property value by adding up furniture replacement costs, electronics, clothing, tools, and valuables, then compare that number to your policy limit. Most Utah homeowners discover their limit sits below their actual belongings’ replacement value.

Contact your agent to increase your personal property limit to at least 70% of your dwelling coverage, or higher if you own significant valuables. The premium increase for boosting coverage typically costs $15-30 monthly, a modest investment that prevents tens of thousands in uninsured losses.

Final Thoughts

Personal property coverage homeowners insurance protects your belongings from financial devastation, but only when you understand what your policy actually covers and where gaps exist. You need to document everything you own with photos and values, confirm whether your policy uses replacement cost or actual cash value, and calculate whether your coverage limit matches your actual belongings’ replacement cost. Most Utah homeowners discover their limits fall short only after filing a claim, which is far too late to make adjustments.

Your next step involves scheduling a conversation with an insurance professional who can review your specific situation and discuss whether scheduled personal property coverage makes sense for your valuables, whether your peril type leaves dangerous gaps, and whether your coverage limits align with what you actually own. The modest premium increases for better coverage typically cost $20-40 monthly, a small price for preventing tens of thousands in uninsured losses. We at Archibald Insurance Agency specialize in helping Utah homeowners build personalized insurance solutions that fit their specific needs and budgets, and our team represents numerous insurance carriers so we can compare options and find coverage that actually protects what matters to you.

Contact Archibald Insurance Agency to review your personal property coverage and make sure your belongings are truly protected.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation