What is the Average Business Liability Insurance Cost?

Business liability insurance protects your company from costly lawsuits and claims. But understanding business liability insurance costs can feel overwhelming when you’re comparing quotes and coverage options.

We at Archibald Insurance Agency help Utah business owners navigate these decisions every day. The cost of your policy depends on several factors-and knowing what drives those prices helps you make smarter choices for your company.

What Actually Drives Your Business Liability Insurance Cost

Your industry determines far more about your premium than you might expect. Construction contractors pay roughly $337 per month for general liability coverage, while technology consultants average around $27 monthly-a massive gap that reflects actual risk exposure. Healthcare operations sit somewhere in between at $31 per month on average. The Hartford’s data shows restaurants face $1,352 annually for general liability, photographers pay $421, and accountants average $604.

Insurers calculate premiums based on claim frequency and severity within each industry. A contractor faces higher injury risks and property damage exposure than an accountant working from home, so the pricing reflects that reality.

How Company Size Multiplies Your Costs

Your company’s size matters just as much as your industry type. Solo operators average $65 monthly for general liability, while businesses with five to nine employees jump to over $200 monthly. Companies with twenty to forty-nine employees can pay up to 1,768% more than the average small business. More employees mean more exposure and higher payroll, which increases workers’ compensation obligations in most states. This acceleration happens because risk exposure grows with your workforce.

Location and Local Factors Shape Your Rate

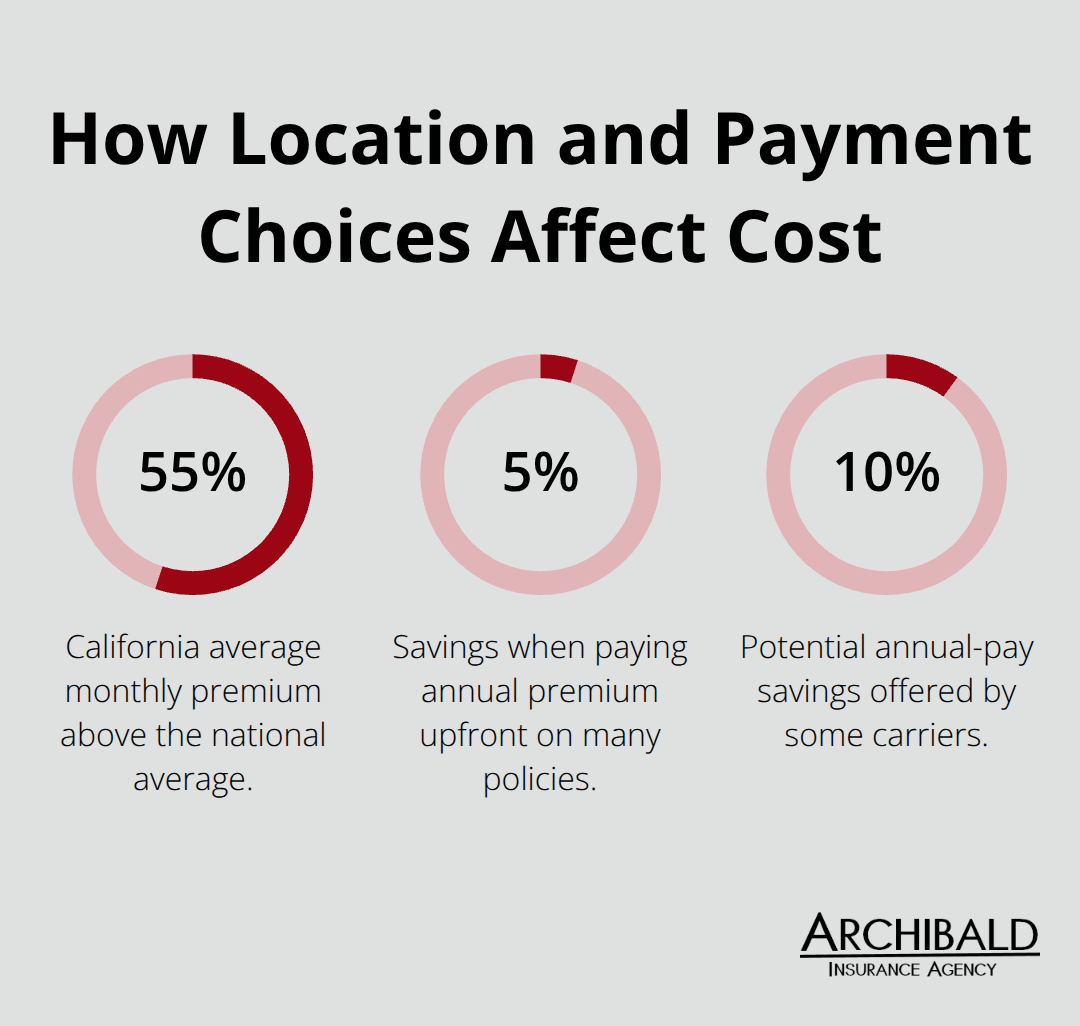

Your location within Utah affects your rate significantly. States like California average $190 monthly-55% above the national average-while lower-cost states like West Virginia average $87 monthly. Utah tends toward the mid-range tier, but specific cities and local factors like medical costs and litigation patterns influence your actual quote.

Regional differences reflect how claim patterns and legal environments vary across the country.

Claims History and Coverage Choices Impact Future Premiums

A clean claims record matters more than most business owners realize. If you file multiple claims, insurers view you as higher risk, and your premiums reflect that perception. Conversely, businesses that demonstrate strong loss-control practices can negotiate better rates over time, typically seeing improvements within one to three renewal cycles. Claims history directly impacts pricing alongside your coverage limits. A $1 million per occurrence/$2 million aggregate policy costs roughly $69 monthly, while upgrading to $2 million per occurrence/$4 million aggregate increases your premium to around $46 monthly-a meaningful difference on annual budgets. Raising your deductible from $500 to $1,000 or higher lowers your monthly premium significantly since you accept more financial responsibility per claim.

Accuracy in Your Application Prevents Rate Surprises

Your annual revenue and operational details matter more than general industry classification. Provide accurate underwriting information about your actual revenue, employee count, and specific work descriptions to avoid rating class surprises at renewal. Incorrect information forces insurers to reclassify your business, sometimes resulting in unexpected rate increases. Your actual cost depends on how your particular operation compares to others in your field, which is why a personalized quote tailored to your specific situation beats relying on industry averages. Understanding these cost drivers positions you to make informed decisions about coverage levels and deductibles that protect your business without overpaying for unnecessary protection.

How Much Does Business Liability Insurance Cost Across Industries

Retail and E-Commerce Operations

Retail and e-commerce businesses face moderate liability exposure compared to high-risk trades. The Hartford data shows retail stores average $1,687 annually, while general liability for this sector typically falls in the $40–$55 monthly range. E-commerce operations often qualify for lower rates since they lack physical storefronts and customer foot traffic, though product liability becomes more relevant if you sell physical goods. The median monthly cost for general liability in retail hovers around $42–$60 depending on your specific operation, inventory value, and location within Utah.

Professional Services and Consulting Firms

Professional services and consulting firms enjoy some of the lowest rates in the insurance market. Accountants average $604 annually according to The Hartford, engineers average $500, and business consultants average $720. Technology consultants sit even lower at $27 monthly on average, reflecting minimal physical risk and claims history. Professional liability (errors and omissions) costs differently than general liability for these firms, running $50–$60 monthly or $600–$720 annually. If your consulting practice operates from home with minimal staff, you’ll land near the bottom of this range.

Contractors and Trades Face Higher Premiums

Contractors and trades face the steepest premiums because injury risk and property damage exposure are genuinely higher. Construction averages $337 monthly for general liability-roughly $4,044 annually-while restaurants hit $1,352 per year. Workers’ compensation for construction trades reflects payroll and injury frequency as key cost drivers. A contractor in Utah should expect general liability premiums well above the national average, especially if your work involves heights, heavy equipment, or subcontractors.

Why the Price Gap Reflects Real Risk

The gap between a consultant paying $27 monthly and a contractor paying $337 monthly isn’t unfair pricing-it reflects actual claim data showing contractors file more frequent and more expensive claims. When you shop for quotes, provide your exact revenue, employee count, and detailed work descriptions to avoid the surprise of reclassification into a higher-risk category at renewal. Vague descriptions tempt insurers to assume worst-case scenarios, which inflates your rate. Your specific operation details matter far more than general industry labels when insurers calculate your actual premium.

How to Lower Your Business Liability Insurance Costs

Implement Safety Programs That Reduce Claims

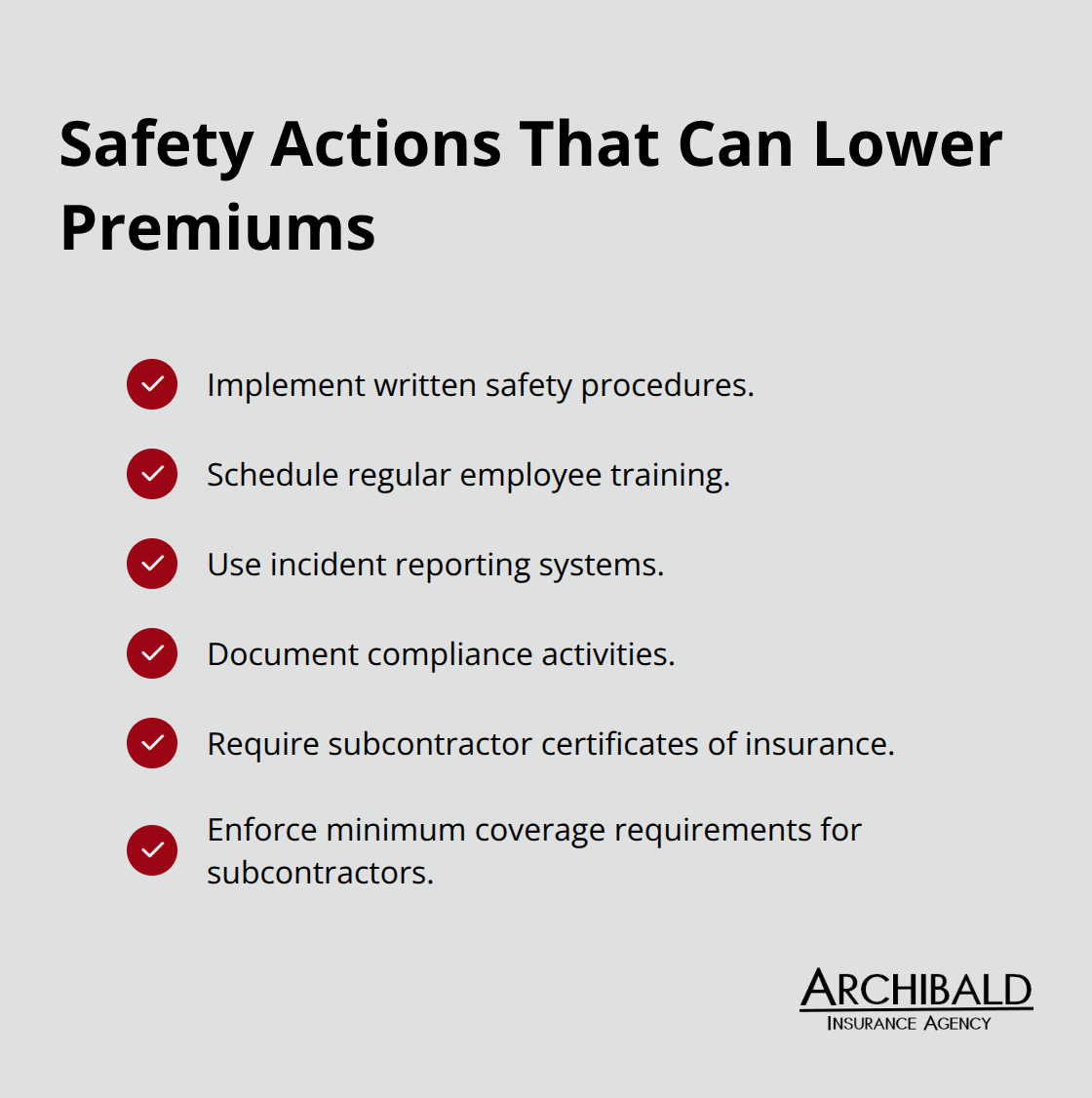

Safety investments and risk management lower your premiums across renewal cycles. Insurers reward businesses that demonstrate loss-control practices with better rates, typically within one to three renewal periods. Written safety procedures, regular training programs, incident reporting systems, and documented compliance reduce your claims likelihood-the metric insurers care about most.

If you operate in construction or trades, require subcontractors to carry minimum coverage and provide certificates of insurance. This signals professional operations to underwriters. A contractor who implements these controls negotiates lower premiums than one with identical revenue and employee count but no formal safety program. The investment pays for itself through premium reductions over time.

Provide Accurate Information on Your Application

Accuracy in your application prevents costly rate surprises at renewal. Vague descriptions of your work tempt insurers to assume worst-case scenarios, which inflates your initial quote or causes reclassification at renewal. Provide exact revenue figures, precise employee counts, and detailed operational descriptions to your insurer. If your actual revenue differs significantly from your application, expect a rating adjustment-sometimes upward. This happens because your exposure directly correlates to revenue volume. Your specific operation details matter far more than general industry labels when insurers calculate your actual premium.

Bundle Policies and Adjust Deductibles Strategically

Bundling policies delivers measurable savings that most Utah business owners overlook. A Business Owner’s Policy bundles general liability with commercial property coverage, with savings available when you bundle multiple coverages together. Adding commercial auto, cyber, or umbrella coverage to your bundle generates additional discounts beyond the BOP savings. Increasing your deductible from $500 to $1,000 or higher lowers your monthly premium significantly since you accept more financial responsibility per claim-this works only if you can actually afford the higher deductible when a claim occurs.

Optimize Payment Methods and Coverage Limits

Paying your annual premium upfront instead of monthly installments saves five to ten percent on most policies. Shopping quotes across multiple carriers with identical coverage details reveals dramatic price differences for the same protection. Your coverage limits directly impact cost-a $1 million per occurrence/$2 million aggregate policy costs roughly $69 monthly, while a $2 million per occurrence/$4 million aggregate policy increases your premium meaningfully. If your contracts don’t require higher limits, lower limits reduce your premium without sacrificing necessary protection.

Review Coverage Annually as Your Business Evolves

Review these details annually because your business changes, your exposure shifts, and your coverage needs evolve. Each renewal presents an opportunity to reassess whether your current limits and deductibles still match your actual operations. Businesses that grow their employee count or expand into new service areas face different risk profiles than they did previously. Conversely, if you’ve reduced operations or implemented stronger safety measures, your premium may decrease at renewal. Annual reviews ensure you maintain adequate protection while capturing savings opportunities.

Final Thoughts

Your business liability insurance cost reflects your industry risk, company size, location, claims history, and coverage choices. A consultant might pay $27 monthly while a contractor pays $337 monthly, but both numbers represent actual exposure and claim patterns in their respective fields. The national average for general liability sits around $69 monthly, though Utah businesses typically fall within the mid-range tier for state pricing.

Adequate coverage protects your business from lawsuits that could otherwise devastate your finances. A single liability claim can exceed your annual revenue, making proper protection non-negotiable regardless of your industry. Your coverage limits should match your actual exposure and contractual requirements, not just the cheapest option available.

We at Archibald Insurance Agency help Utah business owners find coverage that matches their actual needs and budgets. Our team represents multiple carriers, which means we can compare quotes across different insurers to find the best protection at the right price for your situation. Contact Archibald Insurance Agency to discuss your business liability insurance needs and receive a quote tailored to your operation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation