How to Choose Term Life Insurance Policy for Seniors

Choosing a term life insurance policy for seniors requires understanding what coverage actually protects your family and how to avoid overpaying for protection you don’t need.

At Archibald Insurance Agency, we help Utah seniors navigate this decision by focusing on the factors that matter most: your health, your financial obligations, and realistic premium costs based on your age.

What Term Life Insurance Actually Covers

Term life insurance provides a straightforward death benefit paid to your beneficiaries if you pass away during the policy term. Unlike whole life policies that build cash value over time, term insurance focuses solely on protection at an affordable price. When you die during the coverage period-whether that’s 10, 15, or 20 years-your beneficiaries receive the full death benefit tax-free, with no waiting period or medical exam delays. This is why term life appeals to seniors who want to cover specific financial obligations without paying for features they won’t use. The death benefit can be used to pay off a mortgage, cover funeral expenses, settle outstanding medical bills, or leave a small inheritance. Term insurance does not include a savings component, investment options, or cash surrender value, which keeps premiums significantly lower than permanent policies.

Why term life costs less than whole life

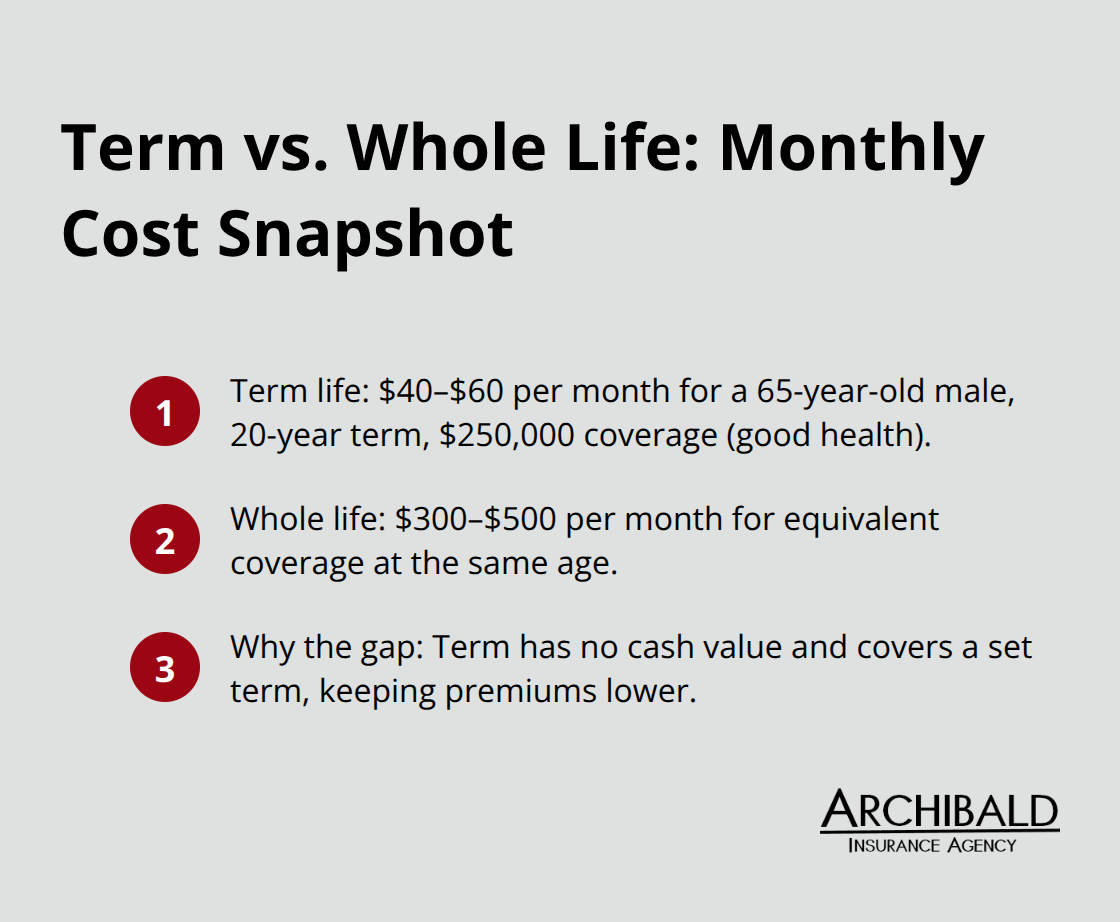

Seniors over 60 who choose term life over whole life make a financially sound decision in most cases. Term life represents the most affordable senior option, with premiums increasing notably from age 60 to 70. A 65-year-old male in good health pays $40 to $60 monthly for a 20-year term policy with $250,000 in coverage, whereas the same person pays $300 to $500 monthly for equivalent whole life coverage. Whole life policies charge higher premiums because they include lifetime coverage and build cash value that takes a decade or more to accumulate, especially at older ages.

If you live on a fixed retirement income, this premium difference matters substantially over time. Term policies become non-renewable or prohibitively expensive after a certain age, so most seniors select terms that align with their actual coverage needs rather than commit to lifetime protection they may not require.

How policy length impacts what you’ll pay

The term length you select directly determines your monthly premium. A 10-year term costs less per month than a 20-year term because the insurance company accepts less risk. If you’re 70 years old and need coverage to pay off a remaining mortgage balance, a 10-year term makes sense financially and practically. However, if you’re 65 with a 15-year mortgage still outstanding, a 20-year term provides better protection without forcing you to reapply at age 85, when coverage becomes difficult or impossible to obtain. Premiums lock in at your current age when you purchase, so delaying your application increases your baseline cost permanently. A 62-year-old who waits two years to apply will pay higher premiums at age 64 than they would have at 62, even for the same coverage amount and term length. Many seniors fail to account for this age-based cost escalation, which makes early shopping critical.

What happens when your term ends

Your term policy expires after the selected period ends, and you lose coverage unless you take action. Some policies offer a conversion option that allows you to switch to a permanent policy without a medical exam, though premiums will increase significantly. Other policies include a renewal option, which means you can extend coverage for another term, but the new premium reflects your current age and health status. If you’re 80 years old when your 20-year term expires, you may find that renewal costs triple or that insurers decline to renew altogether. This reality makes it essential to select a term length that covers your actual financial obligations, not one that extends indefinitely into your later years. Understanding these options before you purchase helps you avoid coverage gaps or unexpected expenses down the road.

Key Factors to Consider When Selecting a Policy

How Your Health Status Shapes Your Options

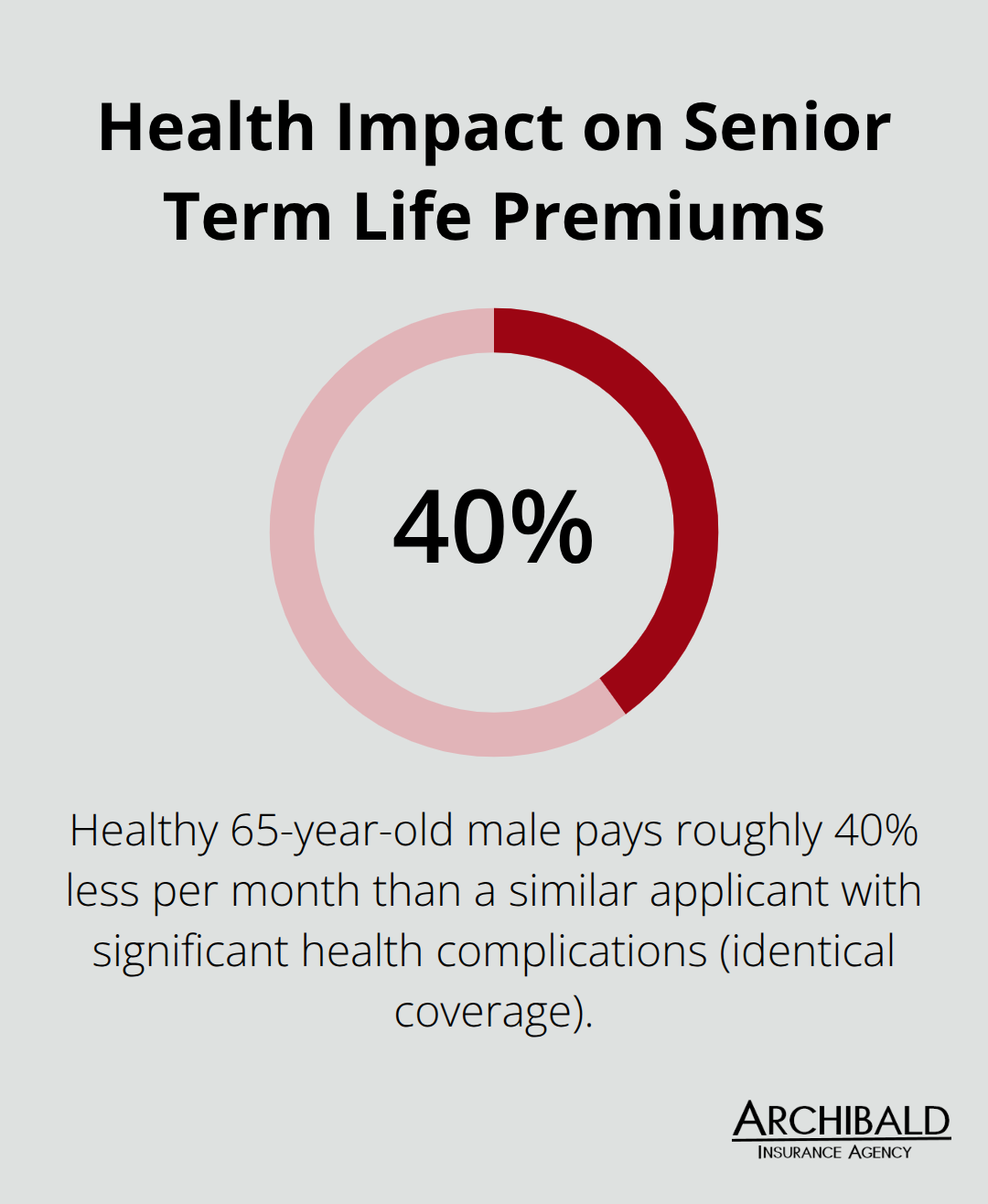

Your health status determines which policies you qualify for and what you’ll actually pay each month. Seniors with controlled diabetes, hypertension, or past heart surgery can still qualify for standard or preferred rates depending on how well-managed their conditions are. If you have a terminal diagnosis or severe untreated health issues, guaranteed issue policies become your only option, though they cost significantly more and cover far less. You must disclose your complete medical history during the application process, including medications, surgeries, and lifestyle habits like smoking. Insurers verify this information through medical records, so omitting details only delays approval or leads to claim denials later. NerdWallet data from November 2025 shows that a healthy 65-year-old male pays roughly 40 percent less monthly than someone with significant health complications for identical coverage. This makes accurate quotes impossible without honesty about your actual health.

If one insurer declines you, other carriers may still approve you at different rates, which is why shopping across multiple companies matters.

Calculating the Coverage Amount You Actually Need

Your financial obligations should drive the coverage amount, not an arbitrary number someone suggests. Calculate what your family would face if you died tomorrow: remaining mortgage balance, final expenses, unpaid medical bills, credit card debt, and property taxes. Most Utah seniors try $10,000 to $20,000 in coverage to handle these obligations without overextending their budget. If your home is paid off and your children are financially independent, you genuinely need less coverage than someone still carrying a mortgage. The Utah Insurance Department’s Life Insurance Buyer’s Guide recommends matching your coverage amount to these specific debts rather than purchasing more than you need. Overbuying creates unnecessary monthly expenses that drain your fixed retirement income.

Comparing Quotes Across Multiple Carriers

Comparing quotes from different carriers is non-negotiable because premium variation is substantial. A 70-year-old male in good health might pay $45 monthly with one insurer and $75 monthly with another for the same 20-year, $250,000 term policy. That $30 monthly difference equals $7,200 over twenty years on a single policy, and most seniors carry multiple financial obligations requiring coverage. You should obtain quotes from at least three different carriers before deciding, and ensure each quote reflects your actual health history and the exact coverage amount you need. Online quote tools provide estimates, but speaking directly with an agent who understands Utah’s local market produces more accurate pricing. An independent agent can access multiple carriers simultaneously, saving you hours of individual applications while identifying which company offers the best rate for your specific health profile. Avoid choosing based solely on the lowest premium, as financial strength matters equally. You can check your chosen insurer’s ratings through AM Best or the National Association of Insurance Commissioners to confirm they’ll be solvent when your beneficiaries file a claim decades from now. Utah’s guaranty association, ULHIGA, protects death benefits up to $500,000 if an insurer fails, but relying on this safety net should never be your strategy. Premium cost, health approval odds, and company reliability must all factor into your final decision. With these three elements aligned, you’re ready to identify the mistakes that derail most seniors during the purchasing process.

Three Costly Mistakes Seniors Make When Buying Term Life Insurance

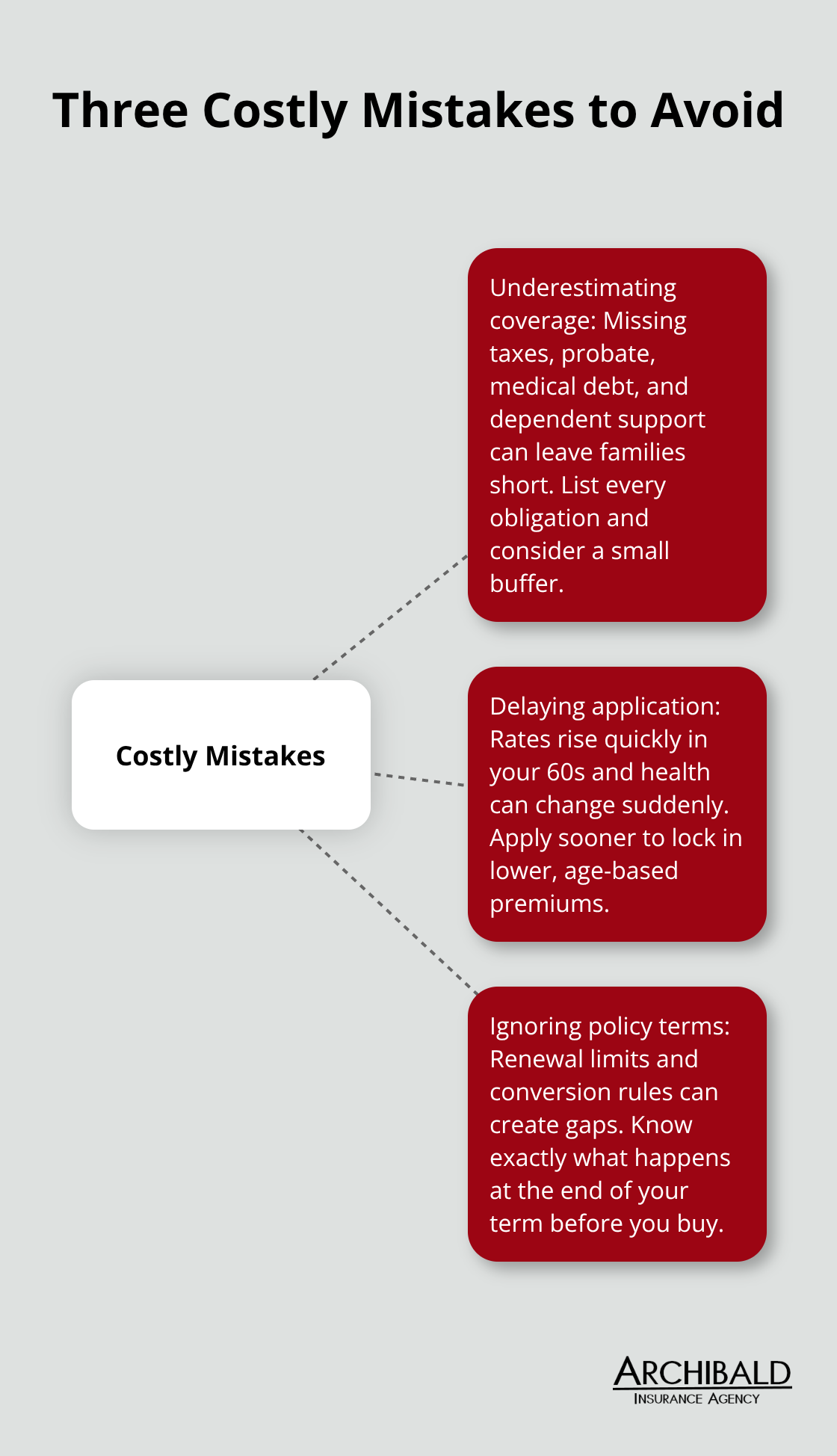

Underestimating Coverage Needs Leaves Families Short

Seniors routinely underestimate how much coverage they actually need, and this mistake costs their families dearly. Most people add up their mortgage balance, funeral costs, and a small buffer, then stop calculating. What they miss are property taxes owed at death, probate fees, outstanding medical bills from their final illness, credit card balances, and any support their spouse or dependents still require. A 68-year-old in Utah with a $150,000 mortgage remaining, $10,000 in funeral costs, $8,000 in property taxes, and $6,000 in medical debt actually needs $174,000 in coverage, not the $160,000 they initially thought. They purchase the lower amount to save on premiums, then leave their family $14,000 short when they pass.

The Utah Insurance Department’s Life Insurance Buyer’s Guide recommends listing every financial obligation line by line rather than guessing at a round number. If you’re uncertain, purchasing slightly more coverage costs far less than the financial strain your family faces when coverage falls short.

Delaying Your Application Locks in Higher Premiums Permanently

The second mistake seniors make involves waiting to apply based on the false belief that a few more years won’t significantly impact their premiums. This thinking is backwards. A 62-year-old who applies today for a 20-year term policy locks in rates based on their current age and health. That same person waiting three years to apply at age 65 pays permanently higher premiums for identical coverage because the baseline age has shifted upward.

Premiums increase notably from age 60 to 70, with some increases exceeding 15 percent annually in that range. Waiting doesn’t save money; it costs thousands over the life of your policy. Health can also change unexpectedly, meaning a manageable health profile today might become a pre-existing condition that increases costs or limits your options tomorrow.

Ignoring Renewal and Conversion Terms Creates Coverage Gaps

The third mistake is purchasing a policy without carefully reviewing the renewal and conversion terms buried in the fine print. Many seniors buy a 20-year term at age 70, believing they’ll be covered until age 90, then discover the policy becomes non-renewable after age 85 or that renewal premiums triple. Some policies include a conversion option allowing you to switch to permanent coverage without a medical exam if your term expires, while others don’t.

Understanding these provisions before you buy prevents the shock of learning your coverage ends precisely when you might need it most. Read the actual policy document, not just the marketing summary, and ask your agent to explain what happens when your term expires. These three errors-underestimating coverage, delaying application, and ignoring policy terms-account for the majority of senior regrets when discussing their protection needs.

Final Thoughts

Selecting a term life insurance policy for seniors requires matching your coverage amount to actual financial obligations, locking in rates while you qualify at reasonable costs, and understanding what happens when your term expires. We at Archibald Insurance Agency have seen countless Utah seniors regret waiting too long to apply or purchasing coverage that falls short of their family’s real needs. The good news is that term life remains the most affordable protection available to you.

An independent insurance agent makes this process substantially easier because we represent multiple carriers rather than pushing a single company’s products. We can compare quotes across different insurers simultaneously, identify which company approves your specific health profile at the best rate, and explain the fine print that most seniors overlook. We understand Utah’s local market and know which carriers work best for seniors with various health conditions.

Contact Archibald Insurance Agency to request quotes for a term life insurance policy that matches your actual needs. Bring a list of your financial obligations, your current medications and health conditions, and your preferred term length. We’ll gather quotes from multiple carriers, explain the differences in coverage and cost, and help you select a policy that protects your family without draining your retirement budget.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation