How to Get Life Insurance Policy No Medical Exam

Getting a life insurance policy without a medical exam is possible, and it’s faster than you might think. We at Archibald Insurance Agency help Utah residents find coverage that fits their needs, even when they want to skip the traditional medical evaluation.

This guide walks you through your options, what qualifies you, and what trade-offs to expect.

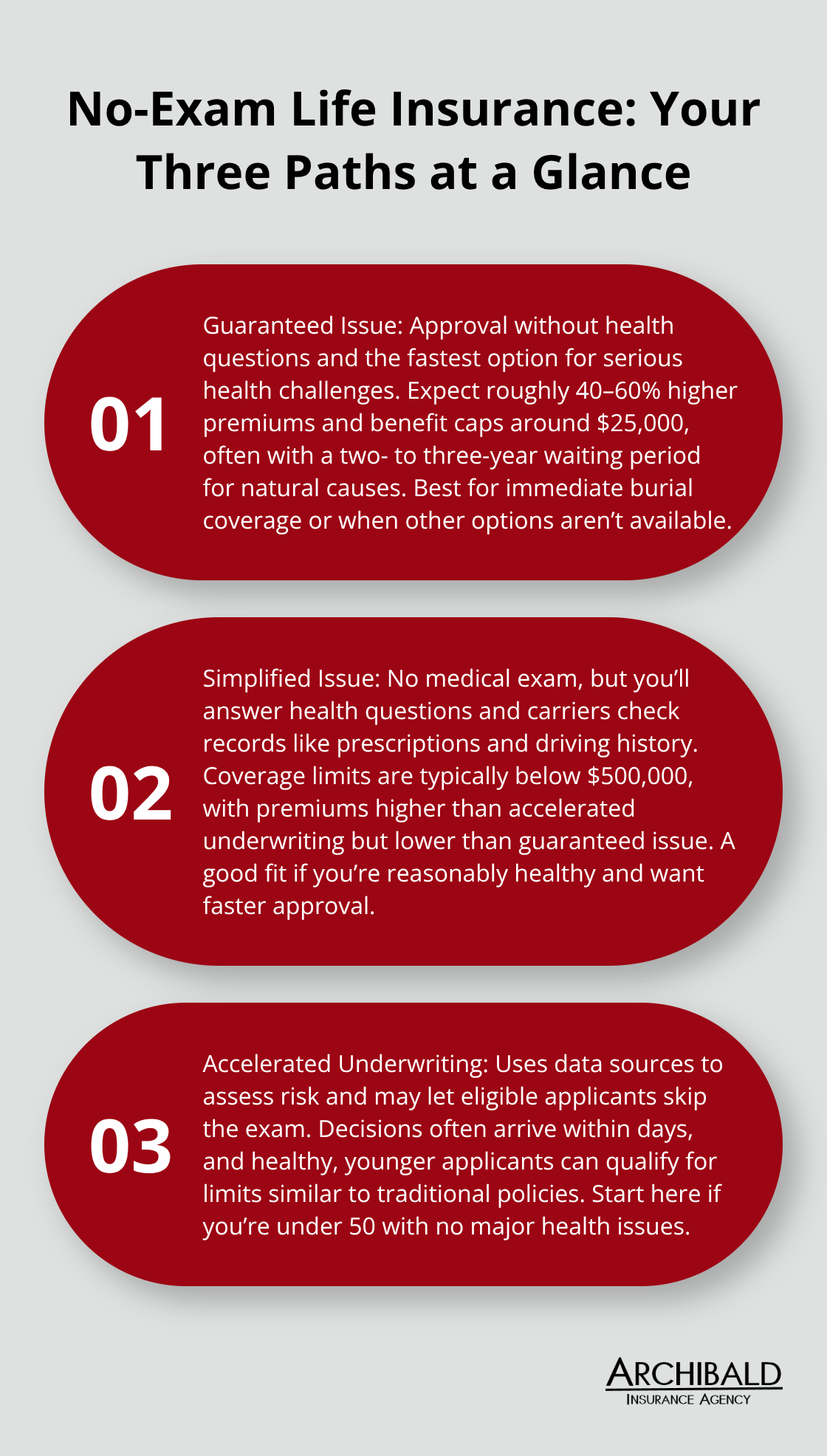

Your Three Main No Medical Exam Options

Guaranteed Issue: The Fastest Approval for Health Challenges

Guaranteed issue life insurance approves nearly everyone without asking health questions, making it the fastest path if you have serious health problems or need coverage immediately. This option comes with a steep price-you’ll pay roughly 40–60% more in premiums than traditional underwriting offers, and death benefits max out around $25,000 according to Experian. Many policies include a waiting period of two to three years, during which your beneficiaries receive only a refund of premiums if you die from natural causes. Use guaranteed issue only if serious health conditions disqualify you from other options or if you need burial expense coverage fast. The higher cost makes it unsuitable as your primary income replacement strategy.

Simplified Issue: The Middle Ground

Simplified issue underwriting removes the medical exam but keeps health questions in place. Insurers review your answers plus prescription records and driving history to assess risk, though they won’t require you to visit a doctor. Coverage limits typically stay under $500,000, and premiums run higher than accelerated underwriting but lower than guaranteed issue. This middle-ground option works well if you’re reasonably healthy but want faster approval than traditional underwriting offers.

Accelerated Underwriting: Best for Young, Healthy Applicants

Accelerated underwriting uses data and technology to assess risk and may allow eligible applicants to skip a medical exam. This approach evaluates health questionnaires, prescription databases, driving records, credit reports, and public records-often delivering approval decisions within days rather than weeks. Younger applicants in good health frequently qualify for coverage limits matching traditional policies while avoiding the medical exam entirely. If you’re under 50 with no major health issues, start here first.

Your choice among these three options depends on your health status, timeline, and budget. Understanding which path fits your situation sets you up to move forward with the right application strategy.

Who Qualifies for No Medical Exam Life Insurance

Age Opens or Closes Your Doors

Age matters more than you’d expect with no-exam policies. Accelerated underwriting works best if you’re under 50 and in decent health-applicants in this range qualify for higher coverage limits and better rates. Once you hit 55 or 60, your options narrow significantly, and guaranteed issue becomes more realistic since traditional carriers tighten their underwriting. If you’re over 65, guaranteed issue policies become your primary choice, though you’ll face the $25,000 benefit cap and 40–60% premium markup that comes with that product type. Starting your application before age 50 gives you substantially better pricing and more flexibility across all three no-exam pathways.

Health History Determines Your Path

Health history directly controls which no-exam track you can take. Accelerated underwriting screens your prescription data, driving records, and public health information-algorithms flag serious conditions like cancer, heart disease, or diabetes, which disqualify you from this fastest path. Simplified issue accepts some health conditions but requires honest answers on the application; lying about your health voids coverage and creates legal exposure. Lincoln Financial specializes in underwriting applicants with pre-existing conditions for no-exam policies, so if you have managed diabetes, controlled hypertension, or similar issues, simplified issue often works. Guaranteed issue asks no health questions at all, making it the only viable option if you’ve been denied traditional coverage.

Coverage Limits and Income Requirements

Coverage limits tie directly to health: a 35-year-old healthy applicant might qualify for $500,000 with accelerated underwriting, but someone with serious health problems maxes out at $25,000 with guaranteed issue. Income requirements vary by carrier and policy type-most no-exam policies don’t require proof of income for coverage under $100,000, but higher limits demand tax returns or recent pay stubs to verify you can afford the premiums and demonstrate insurability.

What the Application Process Actually Involves

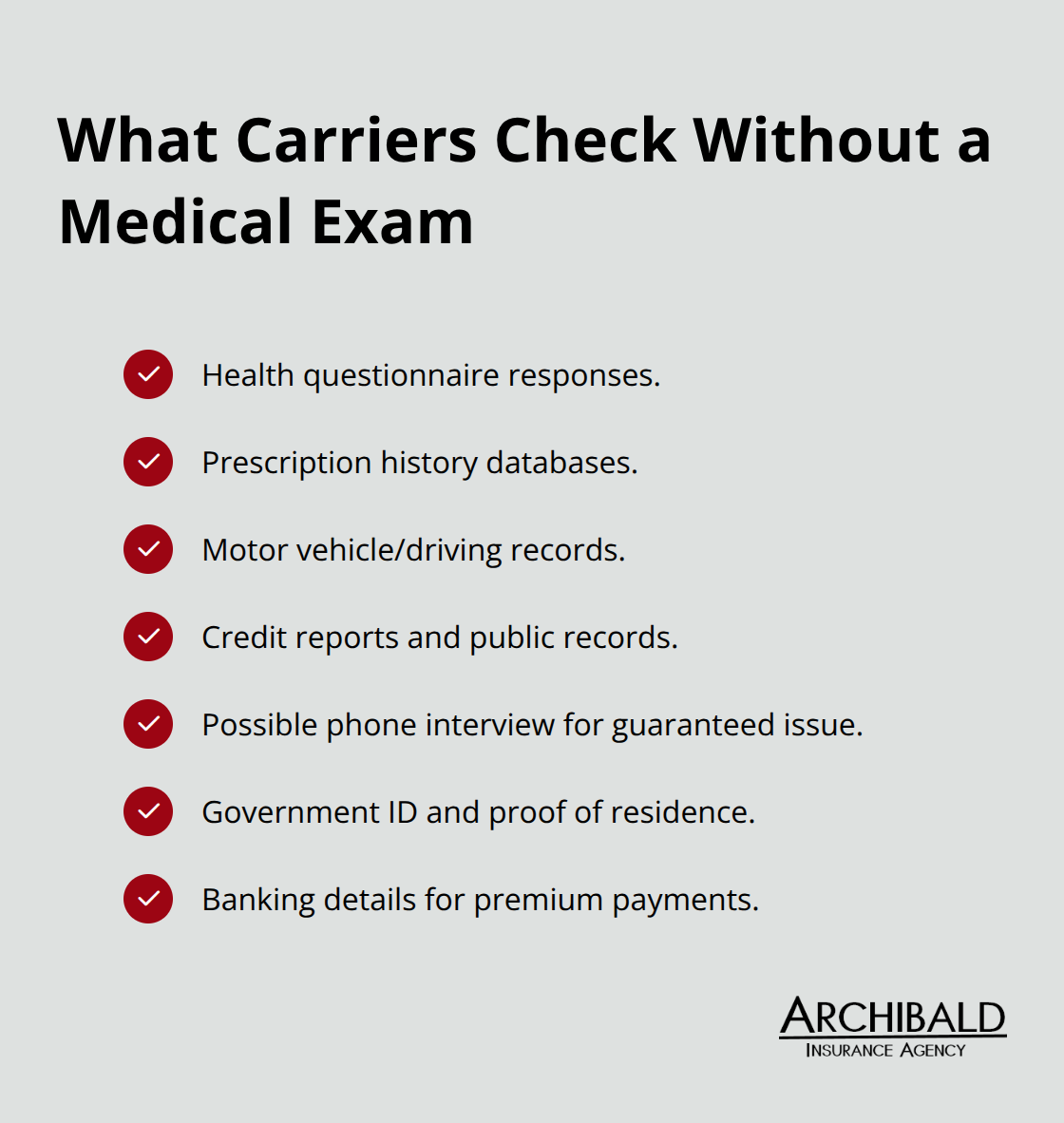

The application process itself takes days for accelerated underwriting versus weeks for traditional policies, but you’ll still answer health questions and authorize prescription checks. Simplified and guaranteed issue applications move faster since they skip the exam, though guaranteed issue may require a phone interview to confirm basic information. Documentation needs stay minimal: government ID, proof of residence, and possibly banking details for premium payments.

Carriers pull data from multiple sources to assess your actual risk, so skipping the medical exam doesn’t mean skipping scrutiny altogether. Understanding these qualification standards helps you identify which no-exam option matches your situation before you apply.

The Real Trade-Offs of Skipping the Medical Exam

Speed Versus Timeline Reality

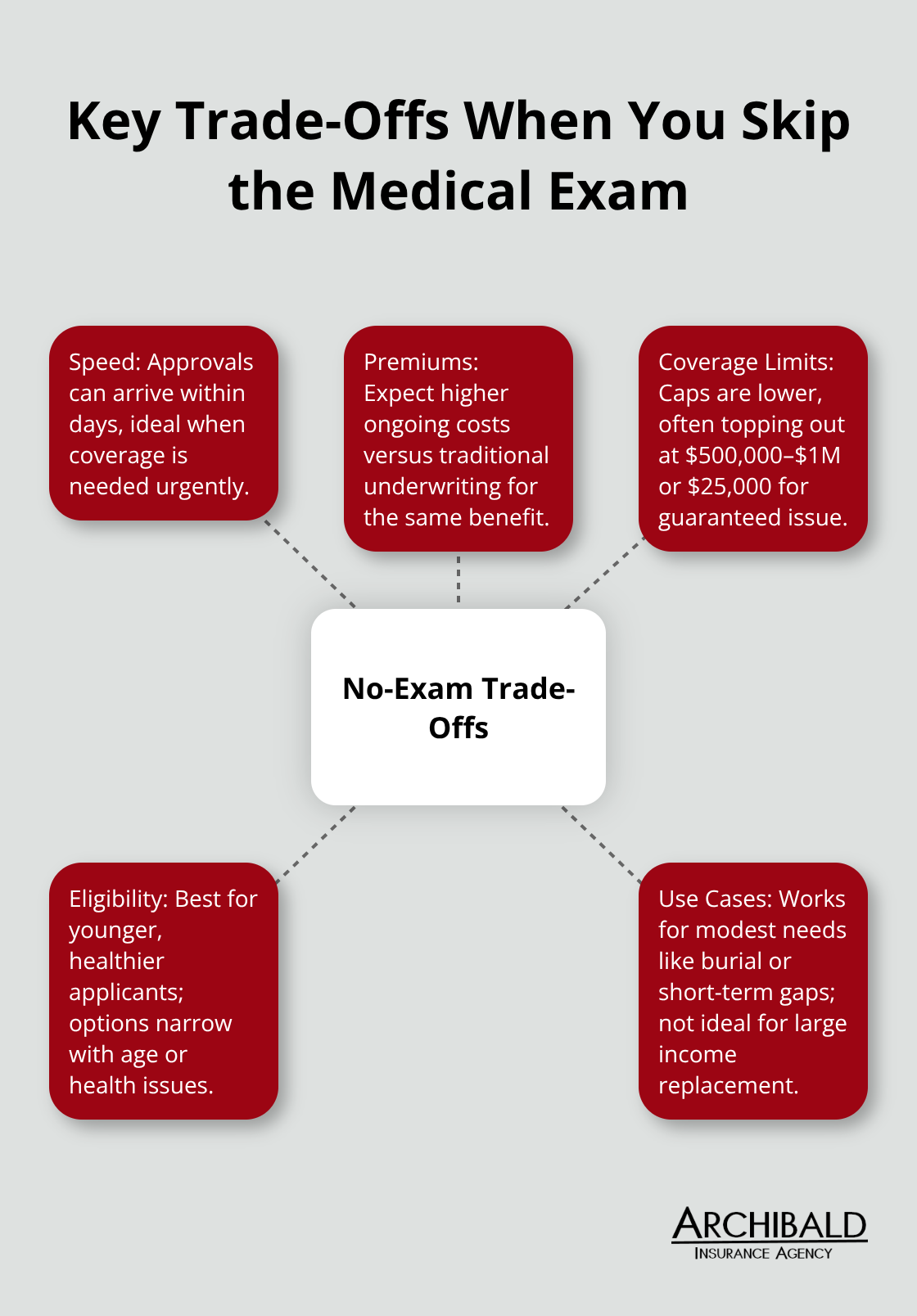

Speed represents the primary advantage of no-exam life insurance, but the actual time savings depend heavily on your age and health status. Accelerated underwriting delivers decisions in days instead of weeks by automating risk assessment through prescription databases, driving records, and public data. A healthy 35-year-old completes the entire process and receives approval within 48 to 72 hours, compared to two to four weeks for traditional underwriting that includes a medical exam. This speed advantage shrinks considerably if you’re over 55 or have health complications-simplified issue and guaranteed issue still move faster than traditional policies, but the gap narrows significantly.

The real benefit surfaces when you need coverage urgently, such as after a major life event or when employer-provided insurance ends unexpectedly.

The Premium Penalty for Convenience

Speed creates a hidden cost that most people underestimate: you’ll pay substantially higher premiums for the convenience. Premiums for no-exam policies run 15 to 40 percent higher than traditional term life for the same death benefit. A healthy 35-year-old male pays $30.79 monthly for a $500,000 traditional term policy over 20 years, but accelerated underwriting typically costs 20 to 30 percent more for identical coverage. Guaranteed issue premiums spike even higher-expect to pay 40 to 60 percent more than traditional rates while receiving only $25,000 in benefits. This premium penalty exists because carriers assume higher risk when they skip the medical exam and rely instead on incomplete health information.

Coverage Limits Create Real Restrictions

Limited coverage amounts compound the premium problem significantly. Accelerated underwriting caps most policies at $500,000 to $1 million, while guaranteed issue maxes out around $25,000. If you need $1.5 million in coverage to replace your income, no-exam options simply won’t work, forcing you back to traditional underwriting despite the longer timeline. The combination of higher premiums and lower limits means no-exam policies work best for modest coverage needs rather than comprehensive income replacement strategies.

Weighing Your Priorities

The choice ultimately depends on whether you value speed enough to accept higher ongoing costs and coverage restrictions, or whether traditional underwriting’s lower premiums and unlimited benefits make more financial sense for your situation. Younger applicants with modest coverage needs often find accelerated underwriting worthwhile, while those requiring substantial death benefits should consider traditional underwriting despite the longer approval window. Your specific circumstances-age, health status, coverage amount needed, and timeline-determine which trade-off makes sense for you.

Final Thoughts

No medical exam life insurance offers three distinct pathways: guaranteed issue for those with serious health challenges, simplified issue as a middle ground, and accelerated underwriting for younger, healthier applicants. Each option trades speed and accessibility against higher premiums and lower coverage limits. Your decision hinges on three factors: your age, your health status, and how much coverage you actually need.

Calculate your real coverage requirement before you apply. If you need $1.5 million to replace your income, no-exam options won’t work, and traditional underwriting becomes necessary despite the longer timeline. If you need $100,000 for burial expenses or modest income replacement, a life insurance policy no medical exam makes financial sense. Age matters significantly too-applicants under 50 in good health should explore accelerated underwriting first, since approval comes within days and premiums stay reasonable.

The premium penalty deserves honest consideration, as you’ll pay 15 to 60 percent more depending on which no-exam option you select. That extra cost compounds over decades, so calculate the total premium difference over your policy’s lifetime before deciding that speed justifies the expense. Contact Archibald Insurance Agency today to discuss your options and receive personalized guidance on finding the right coverage for your situation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation