Best Auto Quotes Utah: How to Lock in Top Rates

Auto insurance rates in Utah vary wildly depending on your driving record, vehicle type, and personal factors. Finding the best auto quotes in Utah requires knowing what insurers look for and how to compare options side by side.

We at Archibald Insurance Agency help Utah drivers cut through the confusion and find rates that actually fit their budget. The strategies in this post will show you exactly how to lower your premiums and work with an agent who knows the local market.

What Actually Drives Your Utah Auto Insurance Rate

Your driving record stands as the single biggest factor insurers examine when calculating your premium in Utah. A single speeding ticket raises rates by roughly 11–13%, while an at-fault accident pushes your bill up significantly higher. After an accident, Progressive and American Family charge around $222–224 per month on average in Utah, compared to $147 for clean drivers. The impact compounds: drivers with multiple violations or claims face substantially steeper costs that can persist for three to five years. Past behavior predicts future claims, which is why insurers weight your history so heavily.

Vehicle Type Shapes Your Premiums More Than You’d Think

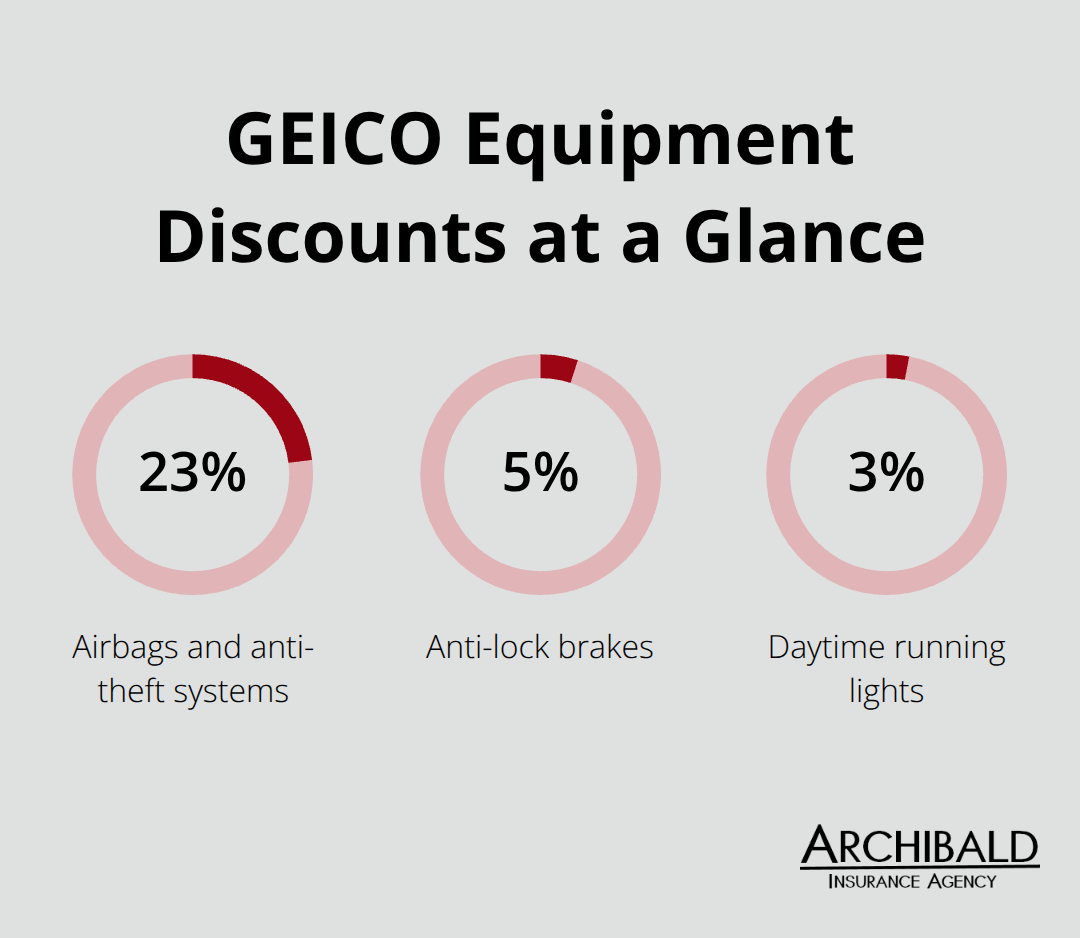

The specific car you drive influences your rate in ways many drivers overlook. Pontiac drivers enjoy the lowest incident rates at about 29.9 per 1,000 drivers, while Infiniti drivers face rates around 78.8 per 1,000-a massive difference that insurers bake into their pricing. Tesla drivers sit at 73.5 incidents per 1,000, another relatively high-risk category. Safety features matter too: GEICO offers equipment discounts of 23% for airbags and anti-theft systems, 5% for anti-lock brakes, and 3% for daytime running lights.

If your vehicle is newer or has strong crash-test ratings from the IIHS, you’ll typically qualify for lower premiums. Conversely, older vehicles or those with poor safety records cost more to insure, though dropping comprehensive and collision coverage on cars worth under $3,000 can offset some costs.

Age and Driving Experience Create Dramatic Rate Swings

Utah drivers aged 18–24 file claims at a rate of 105.7 per 1,000 drivers-nearly 2.5 times higher than Baby Boomers at 39.6 per 1,000 according to QuoteWizard data. This explains why teens on their own policy face liability quotes around $58 per month with the cheapest carriers, while full-coverage policies for teens reach $411 per month with GEICO. Millennials fall in the middle at 43.0 incidents per 1,000. Your zip code within Utah amplifies these age factors: Lehi has the highest incident rate at 66.0 per 1,000 drivers, while Bountiful has the lowest at 41.0 per 1,000. Location, driving history, and age combine to create your baseline rate, which is why a young driver in Lehi pays far more than a middle-aged driver in Bountiful, all else equal.

Where You Live in Utah Matters as Much as Who You Are

Utah’s cheapest cities for auto insurance include Hurricane ($110.18 per month), Vernal ($116.07 per month), and Cedar City ($118.19 per month), while Kearns ($180.35 per month), Lehi ($176.92 per month), and Eagle Mountain ($176.83 per month) rank among the most expensive. These differences reflect local claim patterns, population density, and theft rates specific to each area. A driver with an identical profile pays roughly $70 more per month simply for living in Kearns instead of Hurricane. Insurance companies analyze years of local data to set rates, so your address carries real weight in your final premium.

Now that you understand what drives your rate, the next step involves comparing quotes from multiple carriers to find which insurer offers the best value for your specific situation.

Comparing Quotes Across Carriers Without Wasting Hours

Start with Multiple Carriers to See Real Price Differences

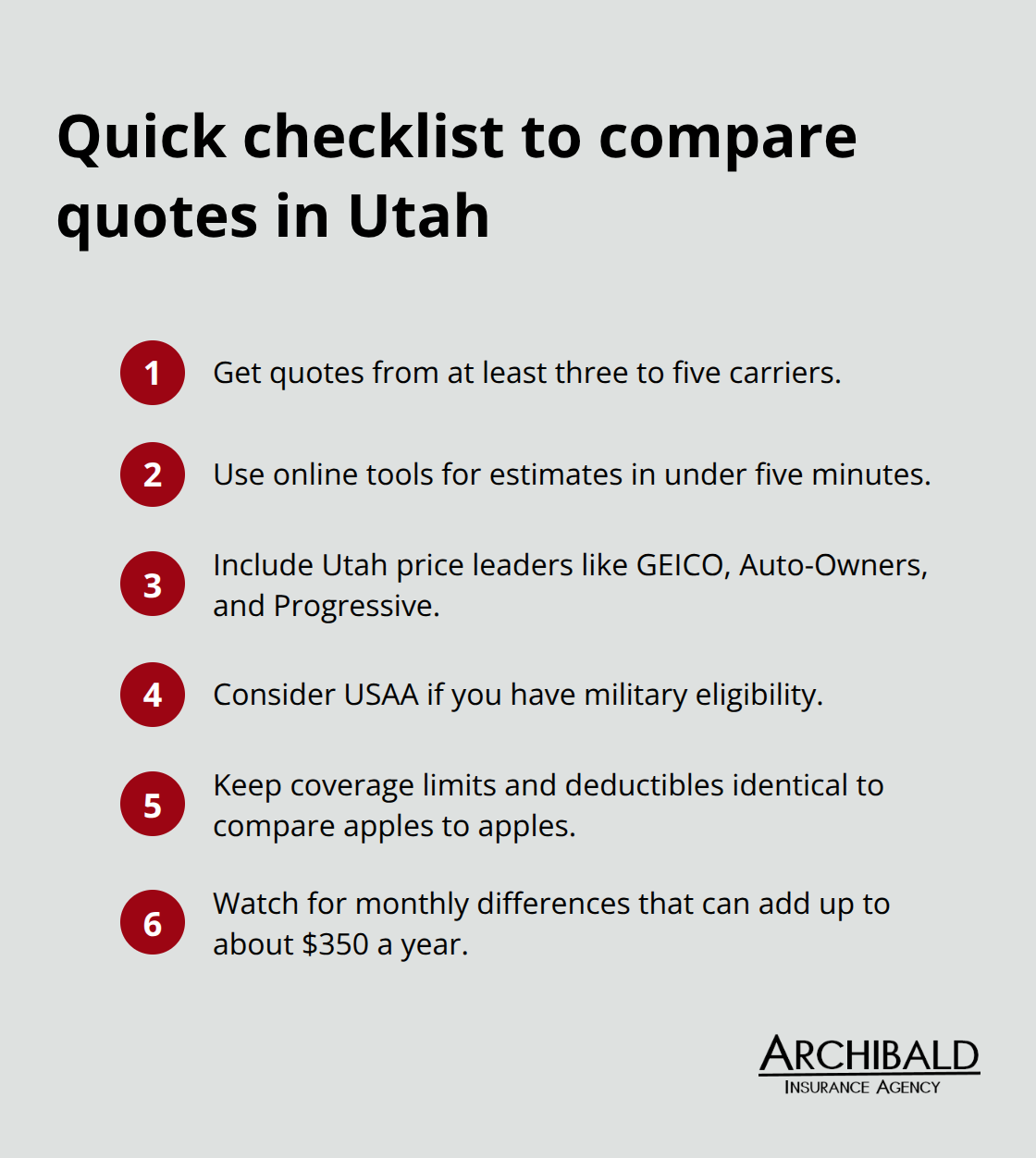

Most drivers stop after one or two quote requests, which means they miss substantial savings. You need quotes from at least three to five carriers to spot meaningful price differences across Utah. Online quote tools generate estimates in under five minutes once you enter your ZIP code, so there’s no reason to skip this step.

Start with carriers that dominate Utah pricing: GEICO offers personalized estimates through their calculator, Auto-Owners typically lands around $1,700 annually, and Progressive sits roughly $1,800 per year according to recent data. If you’re military-connected, USAA often undercuts these at around $1,166 per year, though eligibility is restricted to active and retired service members plus their families. A 40-year-old driver with a clean record and good credit in Utah might pay $147 per month for full coverage with one insurer but only $118 with another-that’s nearly $350 annually for identical protection.

Request Identical Coverage to Make Apples-to-Apples Comparisons

When you request quotes, ensure every company quotes the same liability limits ($25,000 bodily injury per person, $65,000 per accident, $15,000 property damage) plus identical deductibles, typically $500. This approach prevents you from accidentally choosing cheap coverage that leaves gaps. Many drivers overlook that bundling auto with home or renters insurance creates substantial savings, averaging 7–25% depending on the carrier. If you own a home, bundle before comparing quotes so each carrier reflects your actual discount. Utah’s cheapest full-coverage rates come from carriers like Auto-Owners (around $142 per month) and Progressive, but the best choice depends on your specific profile.

Uncover Discounts That Actually Apply to Your Situation

The real power in comparing quotes lies in understanding which discounts each insurer actually applies to your situation, not just reading their advertised rates. GEICO’s equipment discounts-23% for airbags and anti-theft systems, 5% for anti-lock brakes-mean nothing if your 2015 vehicle lacks those features, yet another insurer might offer a 10–15% low-mileage discount that saves you more money. Ask each carrier specifically which discounts you qualify for before accepting their quote. Safe-driver discounts run 5–15% at most carriers if you’ve gone three years without violations or accidents. Defensive driving courses save another 5–15% for up to three years in many cases. Student discounts range 10–15% for full-time students with good grades. If you drive under 7,500 miles yearly, mention this unprompted-low-mileage discounts save 5–15% but insurers won’t volunteer this information.

Test Deductible Changes to Find Your Optimal Premium

When comparing quotes, adjust your deductible to see how much you save: jumping from $500 to $1,000 typically cuts comprehensive and collision premiums by 15–30%, while raising it to $2,000 can save 40% or more. This matters because a lower monthly bill means nothing if you can’t afford your deductible after a claim. After gathering five quotes with identical coverage and deductibles, rank them by price, then call the top three to confirm the quote and ask about additional discounts you might have missed. This final conversation often reveals loyalty discounts, paperless-billing savings (typically 5–10%), or bundling opportunities that weren’t obvious in the online quote.

Finalize Your Selection and Prepare for the Next Step

Once you’ve narrowed your options to the three most competitive carriers, you’re ready to explore specific strategies that lower your premium even further. The discounts you’ve identified form just one piece of the puzzle-your next move involves taking active steps to reduce what you actually pay each month.

Three Moves That Actually Cut Your Utah Auto Insurance Bill

The gap between your current premium and what you could pay sits closer than you think. After gathering quotes, most drivers accept their lowest offer without realizing they can still slash costs through three specific actions.

Raise Your Deductible to Match Your Financial Reality

Increasing your deductible from $500 to $1,000 cuts comprehensive and collision premiums by 10–20%, while jumping to $2,000 saves up to 40% on those coverages alone. The math works only if you can actually afford that deductible after a claim-a $50 monthly savings means nothing when you face a $2,000 repair bill you cannot cover. The real strategy involves finding your deductible sweet spot: high enough to meaningfully lower your monthly bill, low enough that you would not scramble for cash if you needed to file a claim. Most Utah drivers underestimate their financial flexibility here. Test this with your top three quote options before committing to any carrier.

Bundle Auto with Home or Renters Coverage

Bundling auto insurance with homeowners or renters coverage delivers meaningful savings depending on the carrier. This is not theoretical-a Utah driver paying $147 monthly for auto coverage alone could drop to roughly $115–125 by adding home insurance to the same company. The bundling discount often exceeds what you would pay for either policy separately with different carriers. Call each insurer and request a bundled quote before finalizing anything; many drivers miss this savings simply because they never ask.

Activate Low-Mileage and Safety Feature Discounts

Low-mileage discounts apply when you drive under 7,500 miles yearly, saving 5–15% at most carriers, yet insurers rarely mention this without prompting. If you work from home, telecommute several days weekly, or have retired, you almost certainly qualify but will not see the discount unless you specify your annual mileage during the quote process. Safety discounts for features like anti-lock brakes, airbags, and anti-theft systems range from 3–23% depending on your vehicle and insurer. These discounts stack with others-combine low-mileage (10%), bundling (15%), and safety features (10%) and you reach 35% off your quoted rate before any loyalty or paperless billing discounts apply.

Stack Multiple Discounts for Maximum Savings

The difference between accepting your first quote and implementing these three strategies routinely amounts to $300–500 annually for Utah drivers. Each discount compounds with the others, so a driver who raises their deductible, bundles policies, and qualifies for low-mileage savings experiences far greater total reductions than any single action produces. Your specific situation determines which combination works best-a high-mileage commuter cannot access low-mileage discounts but might bundle and raise their deductible, while a retired driver in a safe vehicle could stack all three approaches.

Final Thoughts

You now understand what drives your Utah auto insurance rate, how to compare quotes effectively, and which strategies cut your premium the most. Working with a local Utah insurance agent transforms the quote-gathering process from a frustrating solo effort into a streamlined partnership where you access rates and discounts individual drivers simply cannot find online. We at Archibald Insurance Agency represent numerous insurance carriers, which means we shop your coverage across multiple providers simultaneously and save you hours of repetitive form-filling and phone calls.

Our team knows which carriers offer the best auto quotes Utah for your specific situation, whether you’re a young driver in Lehi facing higher incident rates, a retiree in Hurricane with low mileage, or someone recovering from a recent accident. We ask about your driving patterns, your financial situation, and your risk tolerance to recommend deductible levels and coverage limits that make sense for you. If bundling your auto policy with home or renters insurance saves you money, we structure that immediately, and if you qualify for low-mileage or safety discounts, we ensure every applicable discount appears on your final quote before you commit to anything.

The real value emerges when life changes and your rates shift after an accident, a ticket, or a move to a different Utah city. Rather than wondering whether you still receive a fair deal, you contact us and we re-shop your coverage across our carrier network without any hassle on your end. Contact Archibald Insurance Agency today to discover how much you could save on your next auto insurance policy.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation

As summer approaches, camping enthusiasts eagerly anticipate venturing into the great outdoors and making the most of nature. If you own a camper or trailer, it’s essential to complete a quick tune-up to ensure your vehicle is ready for summer use. While some campers opt for professional servicing, it is entirely possible to perform the maintenance yourself. Here are six crucial areas to check when prepping your camper for summer adventures:

As summer approaches, camping enthusiasts eagerly anticipate venturing into the great outdoors and making the most of nature. If you own a camper or trailer, it’s essential to complete a quick tune-up to ensure your vehicle is ready for summer use. While some campers opt for professional servicing, it is entirely possible to perform the maintenance yourself. Here are six crucial areas to check when prepping your camper for summer adventures: