How to Get Term Life Insurance for Elderly Adults

Getting term life insurance for elderly adults doesn’t have to be complicated. Many seniors assume their age automatically disqualifies them, but that’s simply not true.

At Archibald Insurance Agency, we help Utah residents over 60 find affordable coverage that fits their needs. This guide walks you through the real options available to you.

What Term Life Insurance Actually Covers for Seniors

The Basic Death Benefit

Term life insurance provides a straightforward death benefit paid to your beneficiary when you pass away during the policy term. That’s it-no cash value, no investment component, no complexity. If you die during a 20-year term, your beneficiary receives the full amount you selected, tax-free. If you outlive the term, the coverage ends and you owe nothing further. This simplicity attracts seniors who want protection without ongoing financial obligations.

Why Term Life Costs Far Less Than Whole Life

A healthy 60-year-old nonsmoking man can secure a $500,000 death benefit with a 20-year term for roughly $2,644 per year, according to LifeStein data. A woman in the same scenario pays about $1,885 annually. Term life is almost always less expensive than whole life, making it the practical choice when you need protection without a lifelong financial commitment. The coverage pays out regardless of how you die, with one exception: suicide within the first two years triggers a contestability period where the insurer can investigate or deny the claim.

How Age Shapes Your Options and Costs

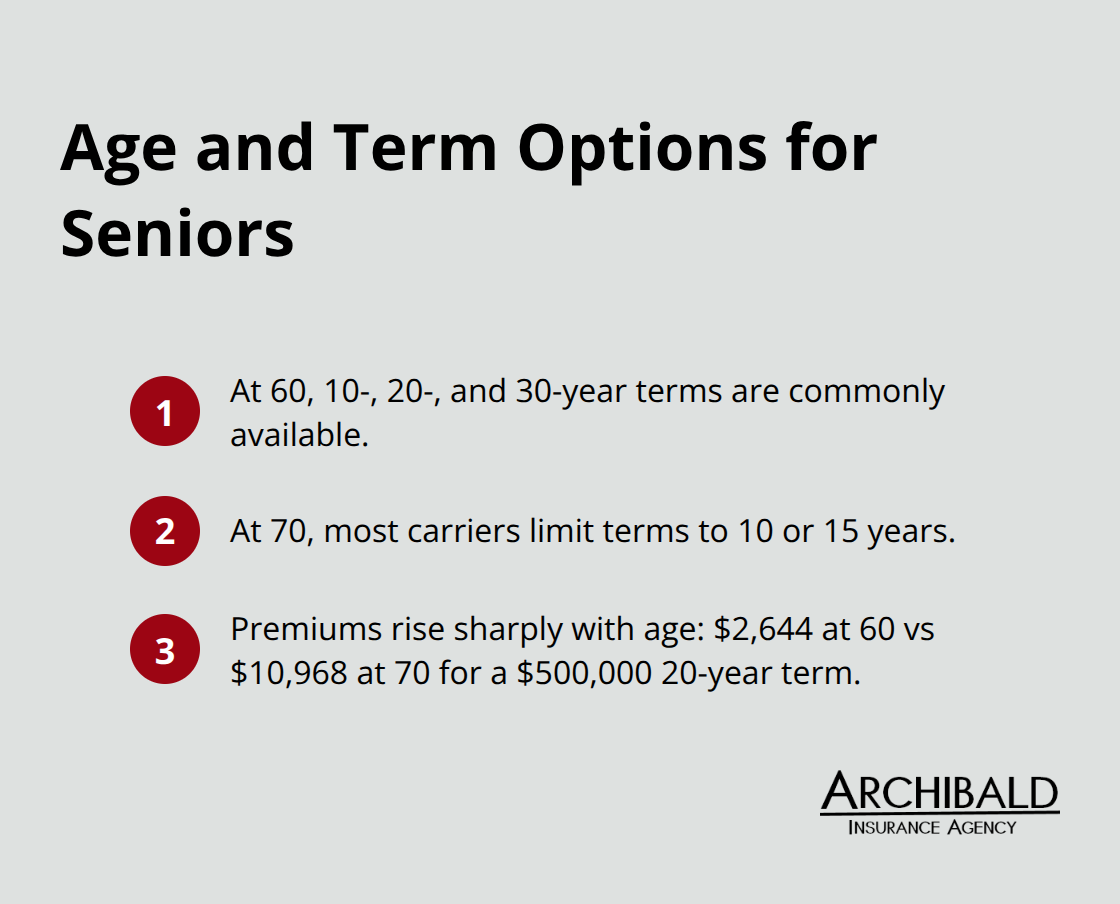

Age directly impacts what you pay and what options exist. At 60, you’ll find 10, 20, or 30-year terms readily available from most carriers. At 70, your choices narrow considerably-most insurers cap term lengths at 10 or 15 years, and some stop writing new policies altogether after age 75 or 80. Premiums climb sharply with each passing year.

That same 60-year-old man paying $2,644 annually could pay around $10,968 yearly at age 70 for identical coverage, according to LifeStein data.

Smoking Status and Health Conditions

Smoking status matters enormously. A 60-year-old smoker pays roughly double what a nonsmoking peer pays for the same policy. Health conditions like heart disease, diabetes, stroke, or cancer raise rates significantly or result in outright denial. The underwriting process for seniors takes longer than for younger applicants because insurers scrutinize medical history more carefully.

Finding Carriers That Accept Seniors with Health Issues

If you have pre-existing conditions, Lincoln Financial stands out for favorable underwriting and offers competitive rates for daily marijuana users, distinguishing itself from peers on this front. No-medical-exam options exist through carriers like Pacific Life, which offers simplified underwriting up to age 70 for coverage amounts in the low millions, but these policies carry higher premiums and lower benefit caps as the trade-off for skipping extensive health screening. Understanding which carriers actively write policies for seniors with health challenges becomes your next critical step in the application process.

How to Apply for Term Life Insurance as a Senior

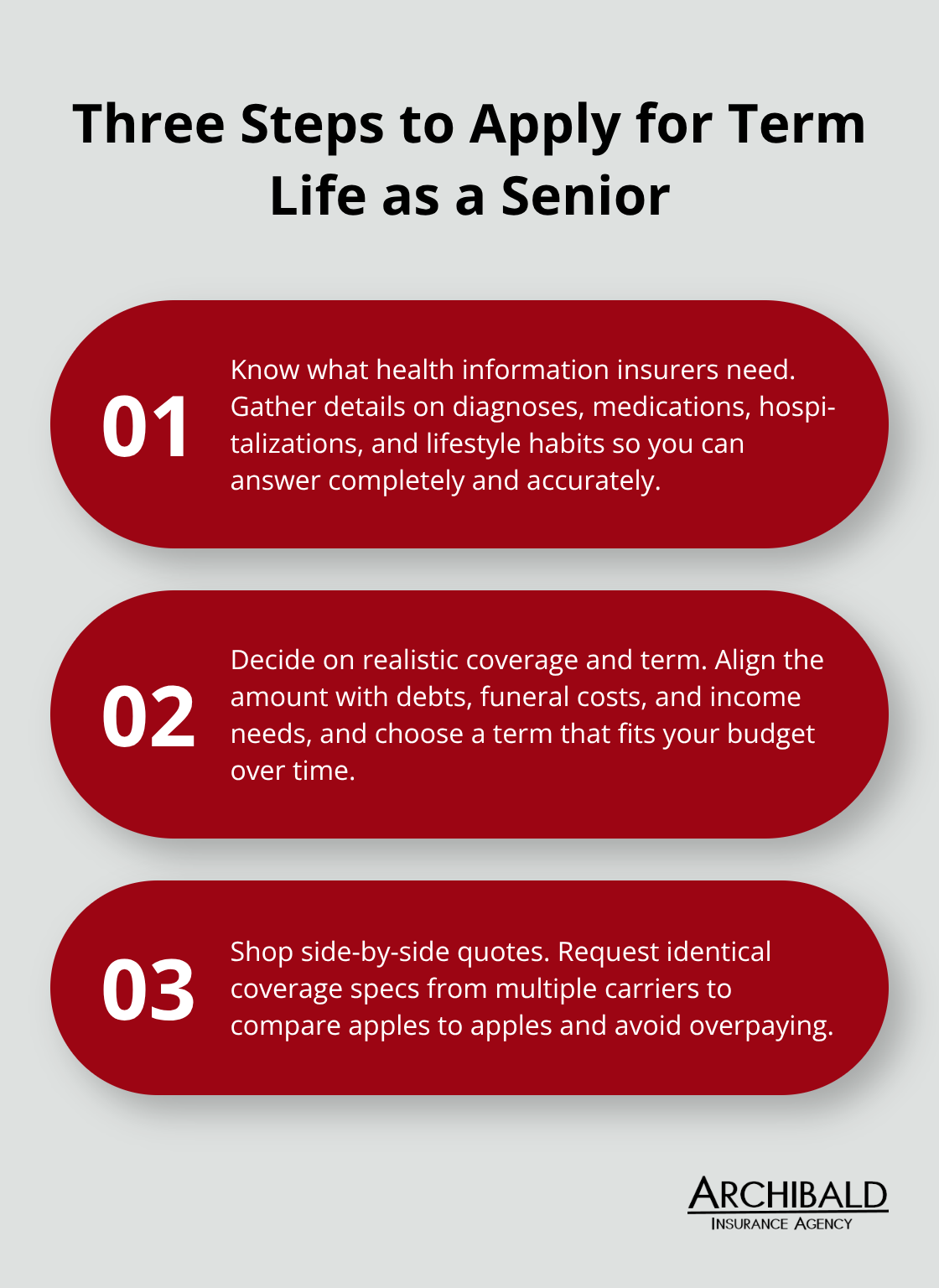

Getting through the application process for term life as a senior involves three straightforward steps: understanding what health information insurers need, deciding on a realistic coverage amount and term length, and shopping quotes side-by-side to find the best rate. None of this requires special skills or technical knowledge. What it does require is honesty about your health and clarity about what you actually need to protect.

Health Information Insurers Will Request

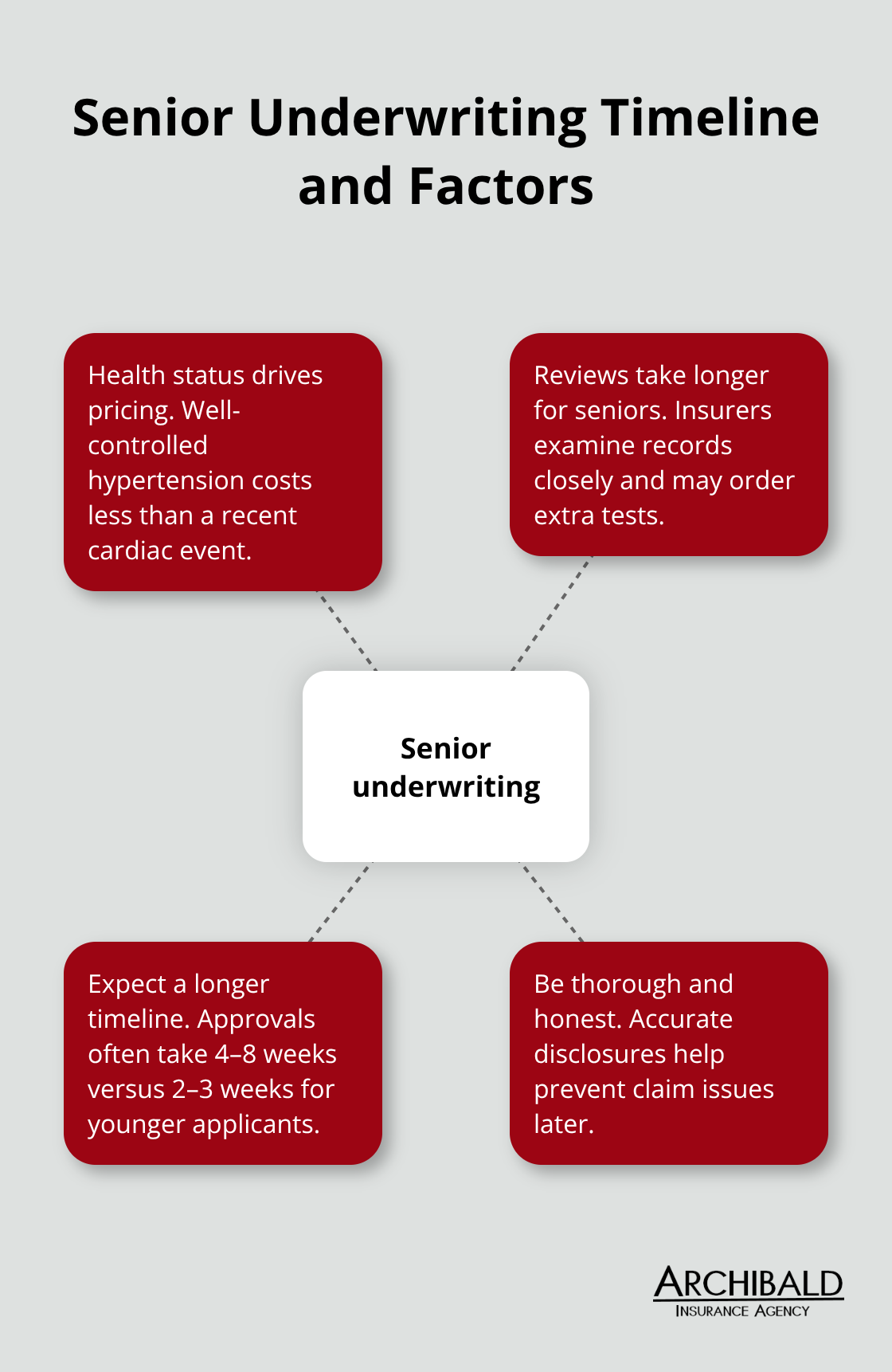

Insurers ask detailed questions about your medical history, current medications, and lifestyle habits. They want to know about hospitalizations, diagnoses like heart disease or diabetes, surgeries, and whether you’ve ever received treatment for mental health conditions. This isn’t intrusive for the sake of it-they’re calculating risk. A 60-year-old with well-controlled high blood pressure pays less than one with uncontrolled hypertension or a recent stroke. Answer these questions completely and honestly. Misrepresenting your health can lead to claim denial years later when your beneficiary needs the money most.

Some insurers offer no-medical-exam policies through Pacific Life and Legal & General America, available up to age 70 for certain coverage amounts. These policies skip extensive health screening but charge higher premiums as compensation. If you have significant health issues, this route can speed up approval, though you’ll pay more for the convenience. The underwriting timeline for seniors typically runs 4–8 weeks because insurers take longer reviewing older applicants’ medical records. Start the application process well before you need the coverage in place.

Matching Your Coverage Amount to Real Expenses

Most seniors need coverage between $100,000 and $500,000, depending on what they’re trying to accomplish. If your goal is funeral costs, expect $10,000–$20,000 in expenses, so a $50,000 policy covers that with room for final medical bills. If you’re leaving money to adult children or paying off a mortgage, you need substantially more. Calculate your actual debts: mortgage balance, car loans, credit cards, and medical debt. Add funeral costs and any ongoing expenses you want your surviving spouse to manage for a year or two.

Don’t purchase coverage you can’t afford to keep for the full term. If premiums rise and you stop paying, the policy lapses and your beneficiary receives nothing. A healthy 60-year-old woman paying $1,885 yearly for a $500,000 20-year term can afford that premium at 70 and 75, but a $1 million policy might cost $3,500+ annually and become unaffordable later. Try an amount that protects your real obligations without stretching your retirement budget too thin. Term lengths of 10, 15, or 20 years work best for most seniors because they align with typical financial obligations and keep premiums manageable. A 30-year term at age 60 means coverage extending to age 90-possible but rare and expensive.

Gathering and Comparing Real Quotes

Contact at least three insurers directly or work with an independent agent who represents multiple carriers. Request quotes for the same coverage amount and term length across all three so you’re genuinely comparing apples to apples. A 60-year-old nonsmoking man might receive quotes ranging from $2,400 to $3,200 yearly for a $500,000 20-year term depending on the carrier-that’s an $800 annual difference or $16,000 over the full term. Don’t accept the first quote.

When you receive quotes, read the fine print for guaranteed versus non-guaranteed elements. Some policies lock in rates for the entire term; others allow the insurer to raise rates at renewal if you renew after the initial term ends. Ask each agent whether the policy is renewable and at what age it stops renewing. Many policies become non-renewable after age 80 or 85, which matters if you think you might need coverage beyond that point. Request a year-by-year illustration showing how premiums and benefits perform across the term so you understand exactly what you’re buying. Once you’ve compared your options and selected a policy, the next phase involves understanding the specific challenges that seniors commonly encounter during underwriting and approval.

What Makes Getting Term Life Insurance Harder as You Age

Age Creates Immediate Barriers to Coverage

Securing term life insurance as a senior means confronting real obstacles that younger applicants never face. Age itself becomes a barrier. Most carriers stop writing new policies after age 75 or 80, and some have cutoffs at 70. If you’re 73, your options shrink dramatically compared to someone at 60. Legal & General America and Pacific Life remain among the few carriers actively underwriting seniors into their 70s, but even they have limits. The practical reality is that waiting costs you thousands of dollars in premiums and potentially eliminates entire carriers from consideration.

A 60-year-old pays roughly $2,644 yearly for a $500,000 20-year term, but that same person at 70 pays $10,968 annually according to LifeStein data. The difference compounds over time. A 75-year-old applicant may find no carriers willing to issue a new policy at any price.

Pre-existing Conditions Raise Rates and Trigger Denials

Pre-existing health conditions compound this problem significantly. Heart disease, stroke, diabetes, and cancer don’t automatically disqualify you, but they raise rates substantially or trigger denials from carriers with strict underwriting guidelines. Lincoln Financial has built a reputation for accepting applicants with health conditions that other insurers reject outright, making them a logical choice when your medical history is complicated.

However, even with Lincoln Financial’s flexibility, your premiums will reflect your health status. An applicant with well-controlled hypertension pays less than one with a recent cardiac event. Underwriting for seniors takes considerably longer than for younger applicants because insurers spend more time reviewing medical records and may order additional testing. Expect 4–8 weeks from application to approval, not the 2–3 weeks younger applicants often experience.

Term Lengths Narrow and Force Difficult Trade-offs

The availability of term lengths narrows sharply with age, forcing difficult trade-offs between affordability and protection duration. At 60, you’ll find 10, 20, and 30-year terms readily available. At 70, most carriers offer only 10 or 15-year terms. At 75 and beyond, finding any term length becomes extremely challenging.

This means a 70-year-old needing protection until age 90 cannot secure a 20-year term and must instead cobble together shorter-term policies or accept coverage that expires before they need it. The shorter available terms keep premiums lower but leave gaps in your protection timeline.

Smoking Status and No-Medical-Exam Trade-offs

Smoking status magnifies your challenges significantly. A 60-year-old smoker pays roughly double what a nonsmoking peer pays for identical coverage, and some carriers decline smokers entirely regardless of age. If you’ve quit within the past year, disclose that truthfully because some carriers offer rate reductions after one year of cessation.

No-medical-exam policies through Pacific Life and other carriers can bypass extensive health screening but charge substantially higher premiums and cap coverage amounts lower than medically underwritten policies. Guaranteed issue policies, which accept all applicants regardless of health, often include a two-year graded benefit period where the death benefit remains limited during the initial years. This design protects insurers but means your beneficiary might not receive the full death benefit if you die in year one or two.

Finding the Right Carrier for Your Situation

Multiple carriers exist specifically to match seniors with underwriters who accept their health profile and age. This matters because applying to the wrong carrier wastes time and can result in a denial that makes subsequent applications harder. An independent insurance agency can represent numerous carriers and help you identify which ones actively write policies for your specific age and health situation, saving you months of frustration and rejected applications.

Final Thoughts

Waiting to act on term life insurance for elderly adults costs you thousands in premiums and eliminates carrier options with each passing year. A 60-year-old who applies today pays roughly one-quarter what that same person pays at 70 for identical coverage, and many insurers stop writing new policies after age 75 or 80. Your health conditions demand careful matching with carriers who actively accept your profile, which means shopping with the right agency matters far more than shopping alone.

We at Archibald Insurance Agency represent numerous insurance carriers, allowing us to match you with underwriters actively writing policies for your age and health situation. Our team knows which carriers offer favorable underwriting for pre-existing conditions, which ones provide no-medical-exam options, and which ones deliver competitive rates for smokers or daily marijuana users. We handle the comparison work so you avoid weeks of contacting multiple insurers only to receive rejections.

Calculate what you actually need to protect: funeral costs, outstanding debts, a mortgage balance, or money for your surviving spouse. Then contact Archibald Insurance Agency to discuss your situation with someone who represents multiple carriers and can provide honest guidance about what’s realistic for your age and health profile. The sooner you start this conversation, the more options remain available to you and the lower your premiums will be.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation