Young Driver Auto Insurance: Tips for Safer, More Affordable Coverage

Young drivers face significantly higher insurance premiums than their older counterparts, often paying two to three times more for the same coverage. At Archibald Insurance Agency, we’ve helped countless young drivers in Utah find ways to reduce these costs without sacrificing protection.

The good news is that your age and driving record don’t have to define your insurance expenses forever. This guide walks you through proven strategies to lower your young driver auto insurance rates while building safer driving habits.

Why Young Drivers Cost More to Insure

Insurance companies view drivers under 25 as statistically riskier, and the numbers back up this position. According to the American Academy of Pediatrics, motor-vehicle accidents account for a significant portion of deaths among people aged 16 to 20. The CDC reports that in 2022, 17% of teen drivers aged 15 to 20 who died in crashes had a blood alcohol content of 0.08% or higher. These statistics directly influence how insurers price your policy.

Experience Gaps Create Real Risk

Young drivers lack the experience to anticipate hazards, react quickly to sudden changes, and make split-second decisions that prevent collisions. A 16-year-old simply hasn’t logged enough hours behind the wheel to develop the instinctive responses that older drivers take for granted. Post-pandemic trends show that teen driving risks have intensified, with increases in speeding, seatbelt non-use, and smartphone distractions creating an even riskier environment than before.

How Insurers Calculate Your Premium

Insurance companies use actuarial data to assign risk. They factor in your age, driving history, the type of vehicle you drive, where you live in Utah, and the coverage limits you select. A 16-year-old adding themselves to a parent’s policy typically increases the annual premium by around $5,327 in the first year, according to Bankrate. This figure reflects the genuine cost of insuring higher-risk drivers.

Utah’s Legal Requirements

When you obtain your license, Utah law requires you to notify your insurer immediately. Failure to do so can result in denied claims if you cause an accident, leaving you personally liable for damages and medical bills. The calculation isn’t punitive; it’s actuarial reality. Insurers know that young drivers will file more claims, so they price accordingly.

Understanding this framework explains why your premium feels steep-and why the cost-reduction strategies ahead can meaningfully lower what you pay each month.

How to Cut Your Young Driver Insurance Costs

Good Student Discounts Pay Real Money

A strong GPA directly translates to savings. Insurers like GEICO and State Farm offer good student discounts for teens maintaining a 3.0 GPA or ranking in the top 20% of their class. This discount doesn’t disappear after high school either. If you’re homeschooled, you can qualify by providing evidence of strong performance on national standardized tests. Keeping your grades up ranks as one of the easiest ways to reduce what you pay each month.

Defensive Driving Courses Deliver Measurable Results

Completing an approved driver education program qualifies you for discounts with most major carriers. If all drivers under 21 in your household complete the course, some insurers apply additional reductions. These courses teach hazard recognition and emergency braking techniques that actually prevent accidents, so the discount reflects real risk reduction rather than marketing gimmick.

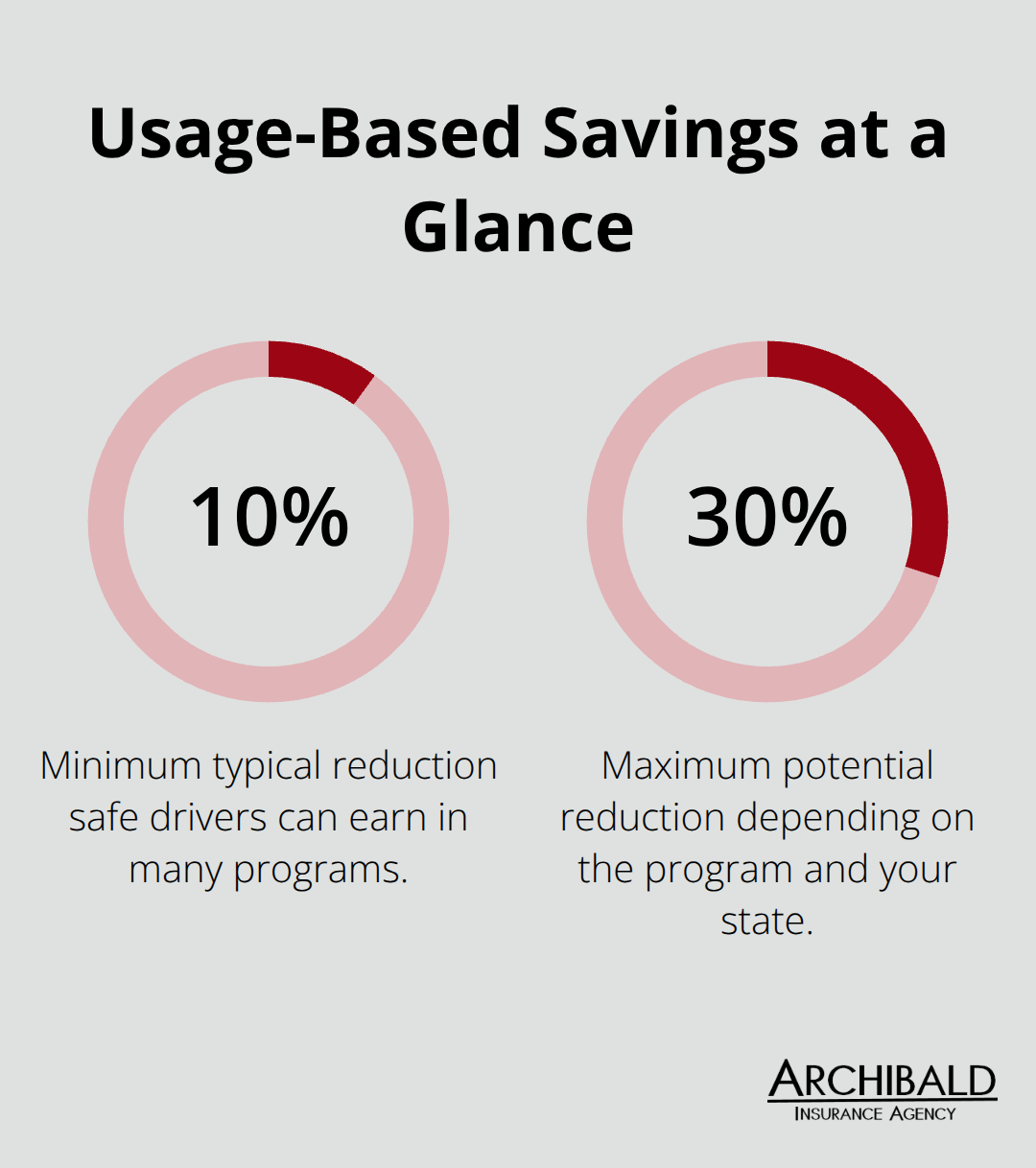

Usage-Based Insurance Rewards Safe Driving Habits

Usage-based insurance programs flip the traditional model on its head by rewarding actual driving behavior rather than penalizing age. Programs like Steer Clear from State Farm and Drive Safe & Save from Progressive use a small device or smartphone app to monitor your acceleration, braking, cornering, and nighttime driving. Safe drivers see premium reductions of 10% to 30% depending on the program and your state. This approach matters especially for young drivers because it proves your competence through data rather than assumptions about your age.

Bundling and Family Policies Cut Costs Significantly

Bundling your auto policy with your parent’s homeowners or renters policy generates immediate savings that compound monthly. Most insurers offer 10% to 25% multi-policy discounts simply for consolidating coverage under one carrier. If your family adds you to an existing policy rather than purchasing separate coverage, you’ll pay considerably less than striking out independently. A 16-year-old on a parent’s policy costs roughly $5,327 more annually according to Bankrate, but that’s still substantially cheaper than a standalone policy for a young driver.

Vehicle Selection and Shopping Strategy Matter

Shop multiple quotes before committing because rates vary dramatically between insurers even for identical coverage. A vehicle’s make, model, and year dramatically influence your premium, so selecting an economical car with strong safety ratings and lower theft risk reduces your insurable risk profile. Newer vehicles with forward collision warning and lane departure warning systems appeal to insurers because those features prevent collisions. The specific details you provide when requesting quotes-including the exact make, model, and year-directly affect the premium you receive, so accuracy matters when comparing options across carriers.

These cost-reduction strategies work best when combined, but they only address half the equation. Your actual driving behavior determines whether you’ll keep these discounts or watch your rates climb after your first accident.

How to Actually Prevent Accidents as a Young Driver

Your insurance discounts mean nothing if you wrap your car around a telephone pole in the first month. The hard truth is that young drivers cause accidents at rates that justify those premium increases, and no discount reverses the damage of a collision. The CDC reports that motor vehicle crashes are the leading cause of death for U.S. teens, accounting for more than one in three deaths in this age group. Post-pandemic trends show the problem has worsened, with increases in speeding, seatbelt non-use, and smartphone distractions creating deadlier conditions than before the pandemic.

Eliminate Phone Distractions Before They Kill You

Smartphones represent the most destructive force in your vehicle. NHTSA’s Put the Phone Away or Pay campaign exists because distracted driving kills. When your phone buzzes, the instinct to check it overrides judgment, and young drivers lack the experience to recognize how quickly a distraction becomes fatal. Place your phone in the trunk, glove compartment, or passenger seat where you cannot reach it while driving. This single action eliminates the temptation that causes most crashes among your age group.

Control Your Speed in All Conditions

Speed kills with mathematical certainty. Driving 10 mph faster than conditions allow eliminates your reaction time and increases stopping distance exponentially. Rain, snow, and darkness amplify these dangers, yet young drivers consistently underestimate how much they need to slow down. Reduce your speed by 25% when weather deteriorates or visibility drops. This adjustment costs you minutes on your commute but saves your life.

Develop Hazard Recognition Skills

Defensive driving courses teach hazard recognition and emergency braking, but the real skill comes from constant practice recognizing threats before they develop. Scan the road three to five seconds ahead of your vehicle, watch for brake lights signaling sudden stops, and assume every driver around you will make a dangerous decision. This habit transforms you from a reactive driver into a proactive one who anticipates collisions before they happen.

Use Telematics Feedback to Improve Your Habits

Usage-based insurance programs like State Farm’s Steer Clear provide real-time feedback on your driving, showing acceleration patterns, braking force, and nighttime driving frequency. This data reveals habits you would not otherwise notice. If the app shows harsh braking events, you are following too closely or failing to anticipate stops. If nighttime driving triggers warnings, you are developing fatigue or overconfidence in darkness. Young drivers who engage with this feedback actively improve their crash avoidance skills.

Choose a Vehicle That Protects You

Newer cars with forward collision warning systems and automatic emergency braking reduce collision risk substantially because they compensate for human error. IIHS crash-test ratings reveal which vehicles protect occupants in actual collisions, and selecting a car with good ratings directly reduces injury severity if an accident occurs. Try a modest, economical vehicle without excessive power that could tempt aggressive acceleration. Your parent’s or guardian’s example shapes your behavior more than any lecture. If they drive distracted, speed in residential areas, or text behind the wheel, you will internalize those behaviors. Safe, sober, distraction-free driving from adults in your household creates the environment where young drivers develop competence rather than confidence masquerading as skill.

Final Thoughts

Lowering your young driver auto insurance costs requires action on two fronts: you must reduce your risk profile through discounts while simultaneously preventing accidents through safer driving habits. Good student discounts, defensive driving courses, usage-based insurance programs, and bundling all signal to insurers that you represent lower risk than the statistical average for your age group. Vehicle selection and shopping multiple quotes amplify these savings further, but discounts vanish the moment you file a collision claim.

Young drivers cause accidents at rates that justify higher premiums, and no discount survives a crash. Eliminating phone distractions, controlling your speed in poor conditions, developing hazard recognition skills, and choosing a safer vehicle directly prevent the crashes that would erase your savings and spike your rates. Your parents or guardians set the tone through their own driving behavior, so safe, sober, distraction-free driving from adults in your household creates the foundation for your competence.

Utah law requires you to notify your insurer when you obtain your license, and failing to do so leaves you personally liable for accident damages. Contact an independent insurance agent who represents multiple carriers and can compare quotes across different insurers to find young driver auto insurance that fits both your budget and your risk profile. Archibald Insurance Agency specializes in helping young drivers in Utah find personalized coverage that matches your specific situation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation