Affordable Life Insurance for the Elderly: Your Guide

Finding affordable life insurance for the elderly can feel overwhelming with so many options and varying costs. Many seniors assume coverage will be too expensive or that age makes them ineligible.

We at Archibald Insurance Agency help Utah families navigate these challenges every day. The right policy exists for your situation and budget.

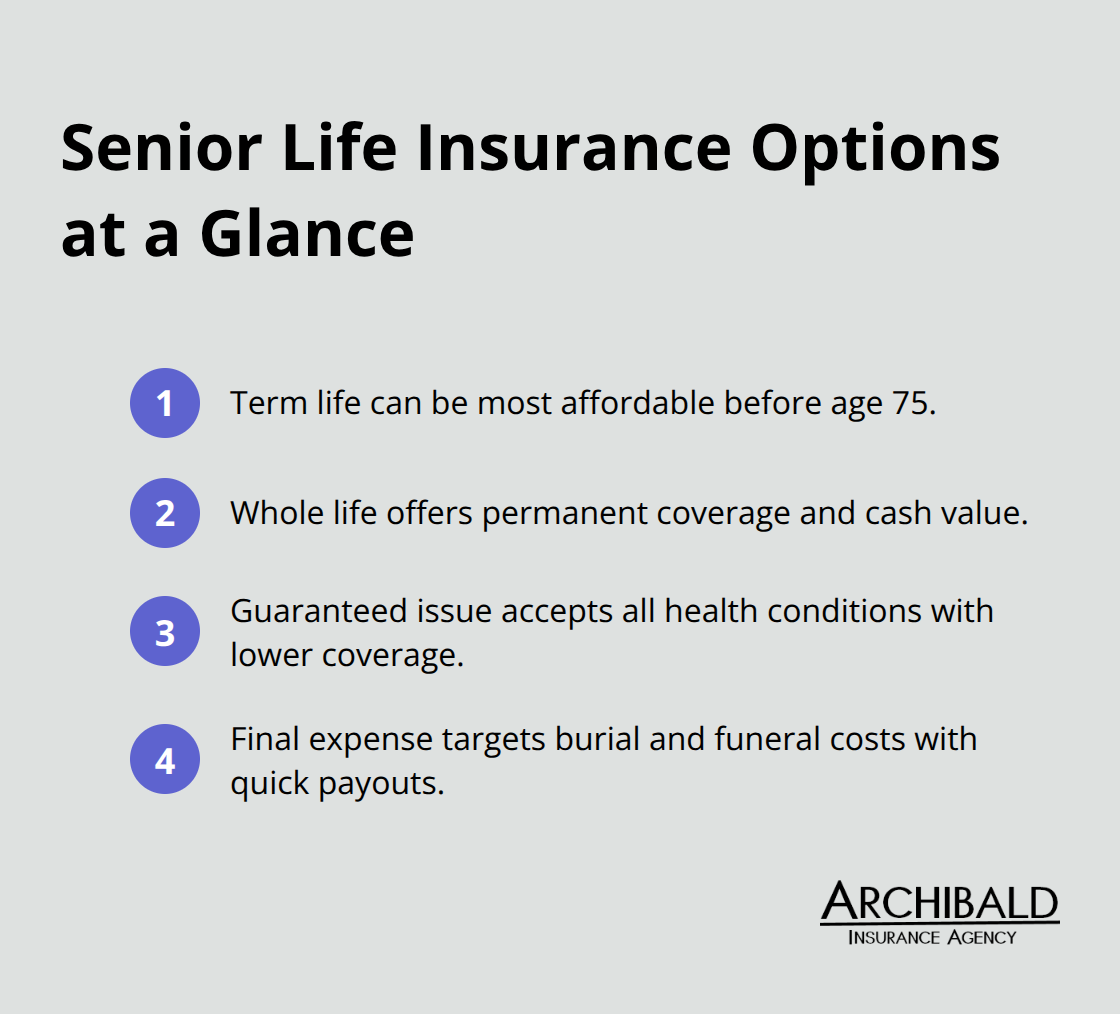

Which Life Insurance Types Work Best for Seniors

Term life insurance remains the most affordable option for seniors, but availability becomes limited after age 75. Legal & General America offers competitive rates for healthy non-smokers (females pay about $23 per month and males pay $27 for a $500,000 20-year term policy). However, seniors in their mid-to-late 70s face increasing difficulty when they seek term coverage, which makes timing essential for this option.

Whole Life Insurance Provides Lifelong Coverage

Whole life insurance costs significantly more than term but offers permanent protection and cash value growth. MassMutual stands out when it offers whole life policies up to age 75 with an A++ financial stability rating from AM Best. The policy builds cash value through dividends, which creates a financial asset while it provides death benefits. Premiums stay level throughout your life, which appeals to seniors on fixed incomes who want predictable costs.

Guaranteed Issue Policies Accept All Applicants

Guaranteed issue life insurance accepts applicants regardless of health conditions, which makes it ideal for seniors with serious medical issues. Mutual of Omaha excels in this area when it offers final expense coverage for ages 80 to 85 without medical exams. These policies typically have two-year waiting periods before full benefits activate, and coverage amounts stay lower than traditional policies. Premiums cost more per dollar of coverage, but approval rates reach nearly 100 percent for eligible ages.

Final Expense Insurance Covers End-of-Life Costs

Final expense insurance targets seniors who need coverage for burial and funeral costs (which average approximately $8,300 as of 2023). This type of policy requires no medical exam and accepts applicants up to age 85. Coverage amounts typically range from $5,000 to $25,000, which makes premiums more affordable for seniors on tight budgets. The application process takes minutes rather than weeks, and benefits pay out quickly to help families during difficult times.

Understanding these options helps you evaluate which type fits your specific situation and budget constraints. Choosing the right life insurance policy requires careful consideration of your health, age, and financial goals.

What Drives Your Life Insurance Premium Costs

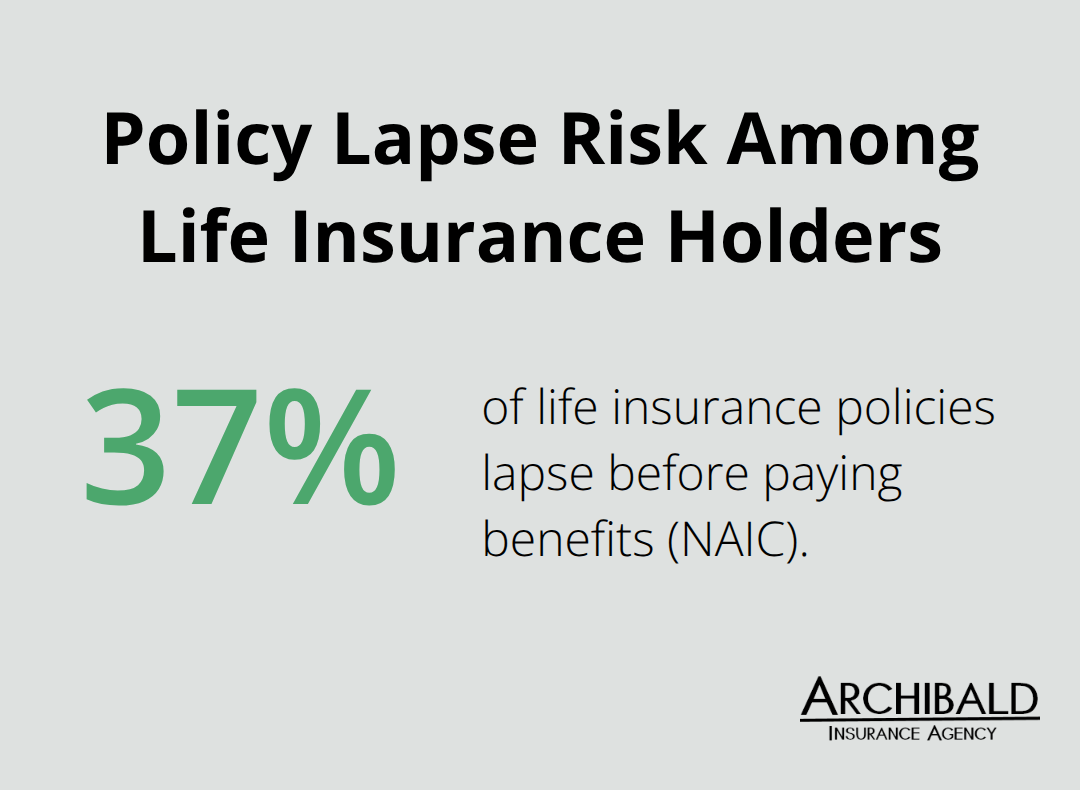

Age stands as the single most powerful factor that determines life insurance premiums for seniors. A 60-year-old pays between $60 to $100 monthly for term life insurance according to industry data, while a 70-year-old faces premiums that can double or triple for identical coverage. Health status creates an equally dramatic impact on costs. Seniors with controlled diabetes or high blood pressure often qualify for standard rates with companies like Legal & General America, but those with heart conditions or cancer history face significantly higher premiums or potential coverage denials. The National Association of Insurance Commissioners reports that 37% of life insurance policies lapse before paying benefits, often leading seniors to purchase insufficient coverage amounts that seem affordable but fail to meet their family’s financial requirements.

Coverage Amount Determines Base Premium Costs

The death benefit amount you select directly correlates with premium costs, but the relationship isn’t always linear. A $250,000 policy doesn’t cost exactly half of a $500,000 policy due to administrative fees and underwriting costs. Most insurers offer better per-dollar rates for higher coverage amounts, which makes $500,000 policies more cost-effective than multiple smaller policies. Policy type creates substantial cost differences too. Term life insurance for a healthy 65-year-old might cost $50 monthly, while whole life insurance for the same person could reach $300 monthly for equivalent death benefits.

Lifestyle Choices Impact Underwriting Decisions

Smoking status dramatically affects premiums, with smokers paying two to three times more than non-smokers for identical coverage. Legal & General America offers reduced rates after one year of cessation, which provides immediate savings for seniors who quit tobacco. Medical history requirements vary significantly between insurers and policy types. Lincoln Financial accepts applicants with pre-existing conditions like depression or controlled heart conditions at competitive rates, while other carriers might decline coverage entirely. Accurate disclosure during the application process prevents claim denials during the two-year contestable period (which Utah law allows insurers to investigate policy applications).

These cost factors work together to create your final premium quote, but smart shopping strategies can help you find affordable coverage despite these variables.

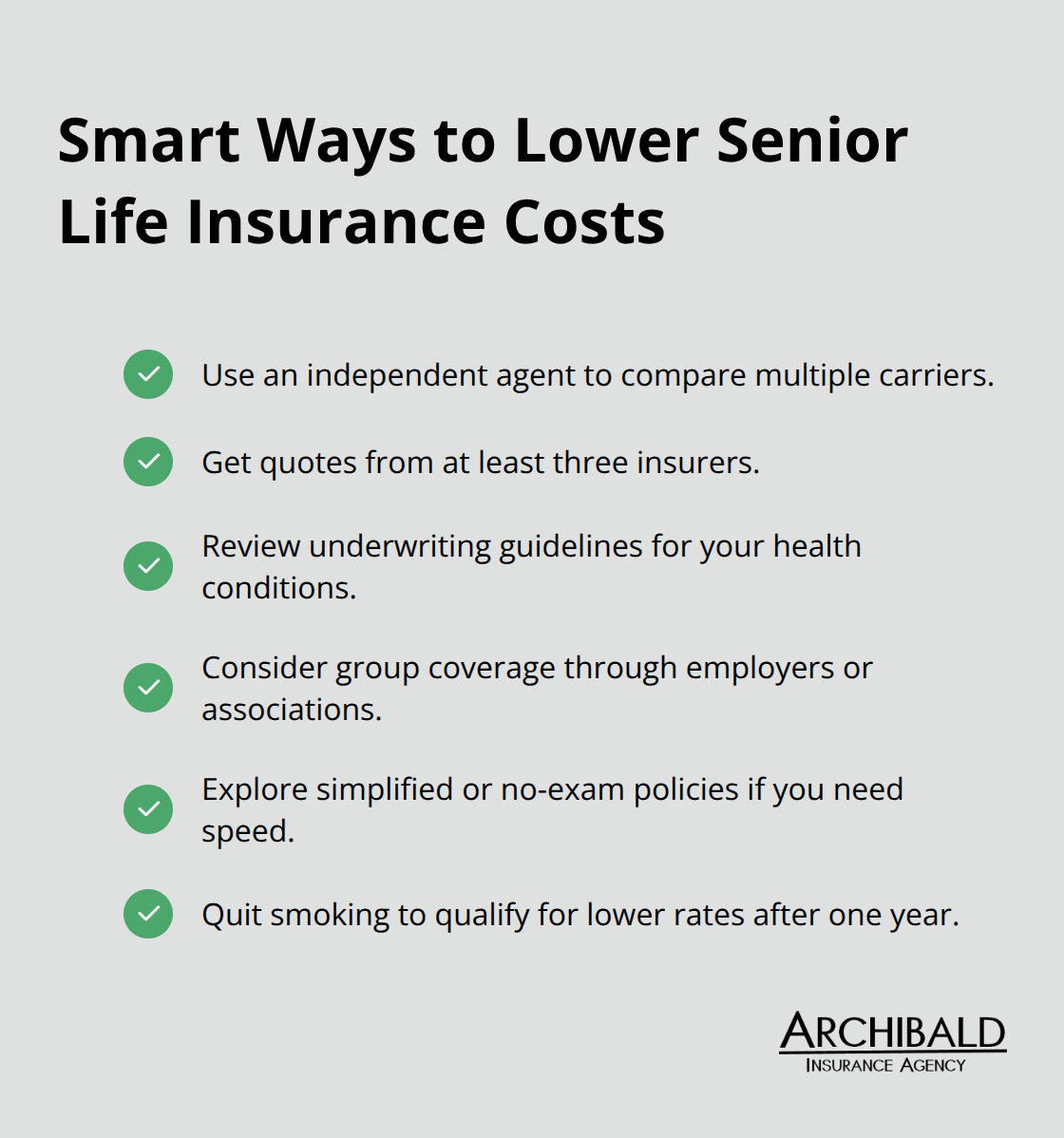

How Can You Find Affordable Coverage

Independent insurance agents represent multiple carriers and access wholesale rates that direct consumers cannot obtain. We at Archibald Insurance Agency work with numerous insurers, which allows us to compare policies from Prudential, Legal & General America, MassMutual, and Pacific Life at once. This approach saves seniors significant time and money compared to contact with each company individually. Independent agents also understand underwriting guidelines for different health conditions. A senior with controlled diabetes might face rejection by one carrier but receive standard rates from another. The Financial Industry Regulatory Authority recommends quote comparison from at least three insurers before purchase, but independent agents can provide five to ten quotes in a single meeting.

Quote Comparison Reveals Dramatic Price Differences

Premium variations between carriers can reach 200 to 300 percent for identical coverage amounts and applicant profiles. A healthy 65-year-old male who seeks $250,000 term coverage might receive quotes that range from $45 monthly to $135 monthly (depending on the insurer). Online comparison tools provide quick estimates, but they often lack accuracy for seniors with health issues or specific coverage needs. Direct contact with carriers or independent agents produces more precise quotes that reflect actual underwriting decisions. The Utah Life and Health Insurance Guaranty Association protects policyholders up to $500,000 in death benefits if an insurer fails, so choice of financially stable companies becomes vital. AM Best financial strength ratings help identify reliable carriers, with A-rated companies that offer better long-term security than lower-rated alternatives.

Group Coverage Through Employers and Organizations

Group life insurance through employers or professional associations costs significantly less than individual policies because risk spreads across many participants. AARP offers its members benefits for affordable permanent and term life insurance from New York Life with coverage options. Former employers sometimes allow retirees to continue group coverage at group rates, which provides substantial savings compared to new individual policies. Veterans qualify for Servicemembers Group Life Insurance conversion options that offer competitive rates regardless of health status.

Medical Exam Alternatives Speed Up Applications

No-medical-exam policies eliminate lengthy underwriting processes but typically cost 15 to 25 percent more than traditional policies. Pacific Life offers universal life insurance options for adults up to age 80 without medical exams, which makes coverage accessible for older customers with health concerns. Simplified issue policies require only health questionnaires rather than full medical exams. These options work well for seniors who need coverage quickly or have minor health issues that complicate traditional underwriting.

Final Thoughts

Affordable life insurance for the elderly demands strategic action and expert advice. Term life insurance provides the lowest premiums for healthy seniors under 75, while whole life insurance delivers permanent coverage with cash value benefits. Guaranteed issue policies accept all applicants regardless of health status, which makes them perfect for seniors with serious medical conditions.

Time works against you when you delay coverage decisions. A 60-year-old pays $60 to $100 monthly for term coverage, but those who wait until 70 face costs that double or triple (according to industry data). Less than 50% of seniors believe their current coverage meets their needs, which shows why regular policy reviews matter.

We at Archibald Insurance Agency represent multiple carriers and provide personalized solutions for Utah families. Our independent approach allows us to compare quotes from numerous insurers and find the best rates for your specific situation. Contact us today to explore your life insurance options and secure the protection your family deserves.