Life Insurance Policies Without Medical Exams

Getting approved for life insurance doesn’t always require a medical exam. At Archibald Insurance Agency, we help Utah residents understand how life insurance policies without medical exams work and whether they fit your situation.

No-exam policies offer speed and simplicity, but they come with trade-offs you should know about. This guide walks you through your options so you can make an informed decision.

How No-Exam Life Insurance Actually Gets Approved

Underwriting Without Medical Tests

No-exam life insurance skips the doctor’s visit, but underwriters still evaluate your health-they just do it differently. Instead of ordering blood work and EKGs, insurers pull information from prescription databases, medical records they can access with your permission, and your answers to a health questionnaire. This approach works because most people applying for no-exam coverage fall into lower risk categories or seek smaller benefit amounts. The underwriting relies on third-party data like your prescription history and answers to health questions rather than medical lab results.

For example, a 35-year-old applying for $500,000 in term coverage receives a decision within days. The insurer reviews whether you take medications for serious conditions, checks your driving history for risky behavior, and confirms basic health facts through your application. Banner Life offers no-exam options across all 50 states and approves qualifying applicants quickly using this streamlined approach. The speed matters because some people need coverage urgently-whether for mortgage protection, income replacement, or to cover final expenses-and waiting weeks for medical test results isn’t realistic.

Speed Varies by Product Type

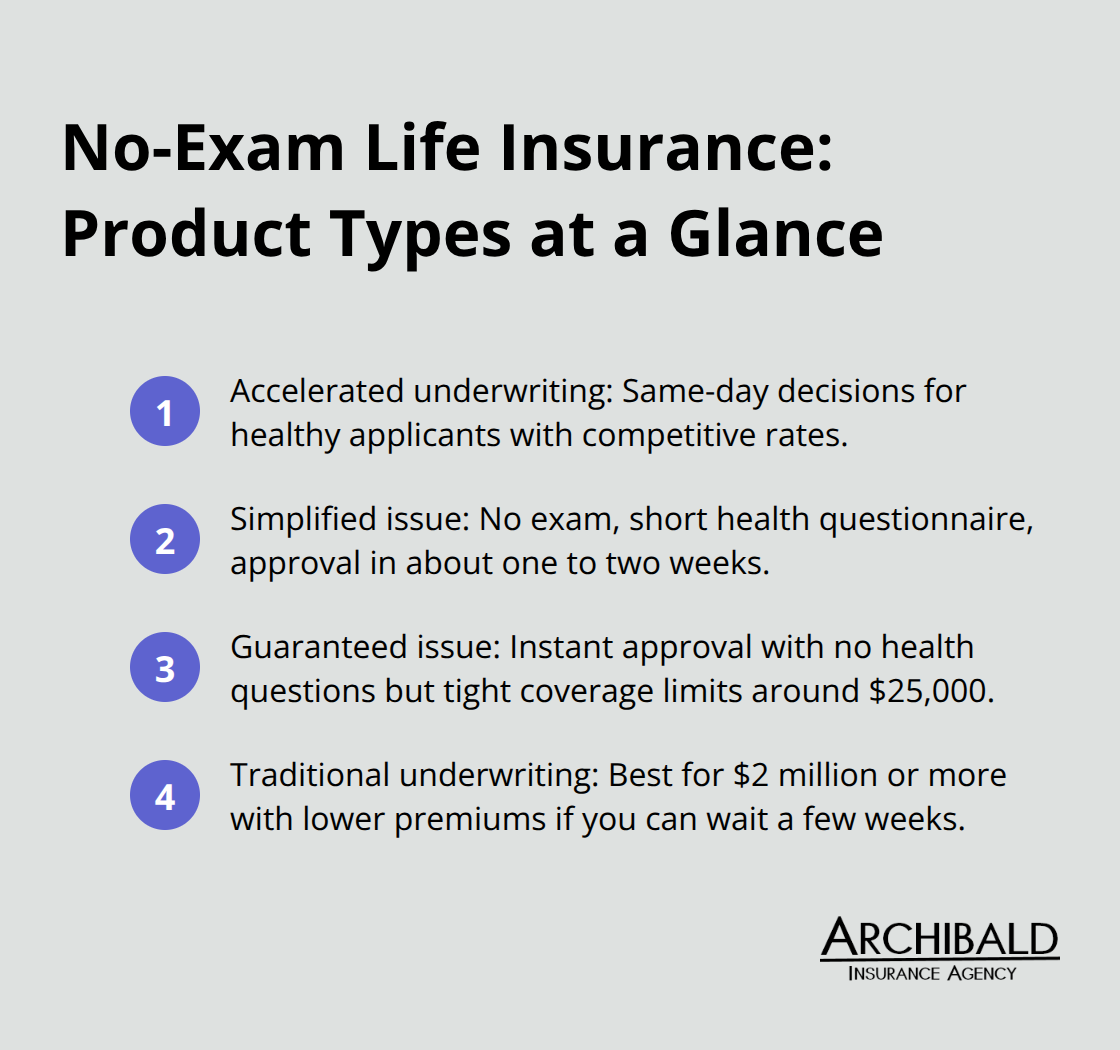

The approval timeline for no-exam policies ranges from same-day decisions to one or two weeks, depending on the product type. Accelerated underwriting streamlines the life insurance application by using data to assess risk, often removing the need for a medical exam. Legal & General America offers instant-decision options for people in their 20s and 30s, making this approach particularly attractive for younger buyers. Simplified issue policies take slightly longer because they collect less health information upfront, so underwriters need more time to assess risk.

Guaranteed issue policies approve everyone regardless of health, but they come with tight coverage limits-usually around $25,000-making them suitable only for funeral expenses rather than income replacement. The real trade-off isn’t speed versus safety; it’s speed versus lower premiums and higher coverage limits.

Pricing and Coverage Trade-Offs

A healthy 35-year-old nonsmoker pays roughly $25.76 monthly for a $500,000 20-year term policy, according to Policygenius data. Simplified issue policies typically cost more because insurers collect less data and set lower maximum coverage amounts. If you’re in good health and willing to answer detailed health questions, accelerated underwriting gives you speed without sacrificing rates.

If you have pre-existing conditions or prefer not to share extensive medical history, simplified or guaranteed issue becomes your option (though expect higher premiums and lower coverage ceilings). The choice depends on your health status, urgency, and how much coverage you actually need. Understanding these three product types helps you identify which one aligns with your situation before you move forward with an application.

Which No-Exam Product Fits Your Situation

Three Products, Three Different Approaches

No-exam life insurance comes in three distinct types, and selecting the wrong one wastes money or leaves you underinsured. Guaranteed issue policies accept everyone but cap coverage around $25,000, making them suitable only for funeral costs. Simplified issue skips the medical exam but asks shorter health questions and typically limits coverage to $1 million or less, with premiums running higher than fully underwritten policies because insurers have less data to assess risk. Accelerated underwriting uses algorithms and third-party data to speed decisions for healthier applicants, often delivering same-day approvals and competitive rates that rival traditional underwriting.

Who Qualifies for Each Type

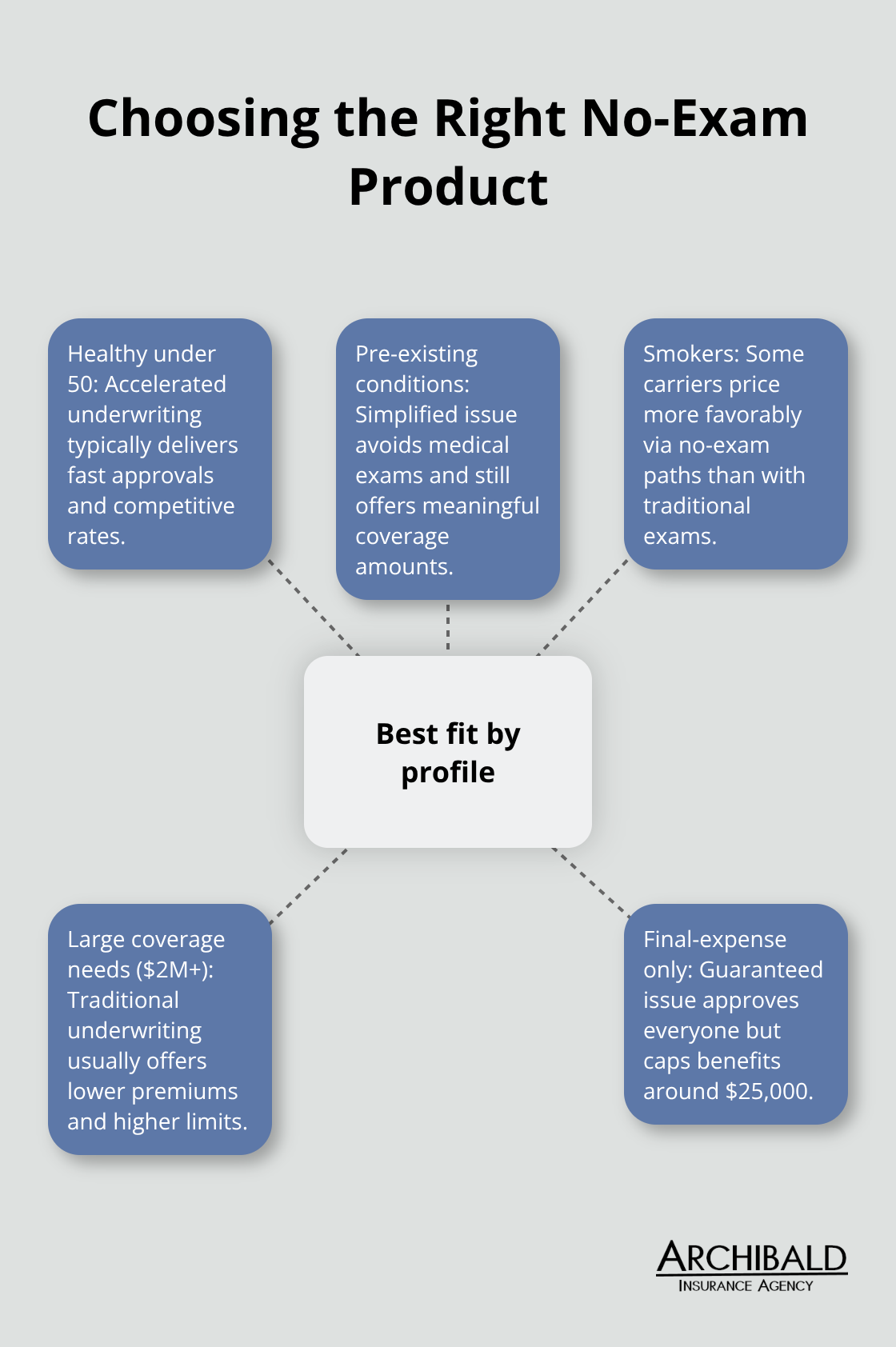

The real difference lies in who qualifies and what you’ll actually pay. If you’re under 50 and in decent health, accelerated underwriting delivers the best combination of speed and cost. If you have pre-existing conditions like controlled diabetes or depression, simplified issue becomes practical because you avoid the medical exam entirely while still accessing meaningful coverage amounts. Lincoln Financial stands out for underwriting people with pre-existing conditions and offers no-exam options for conditions that would normally trigger closer scrutiny. Guaranteed issue makes sense only if you’ve exhausted other paths or need quick coverage for final expenses.

Pricing Differences Between Products

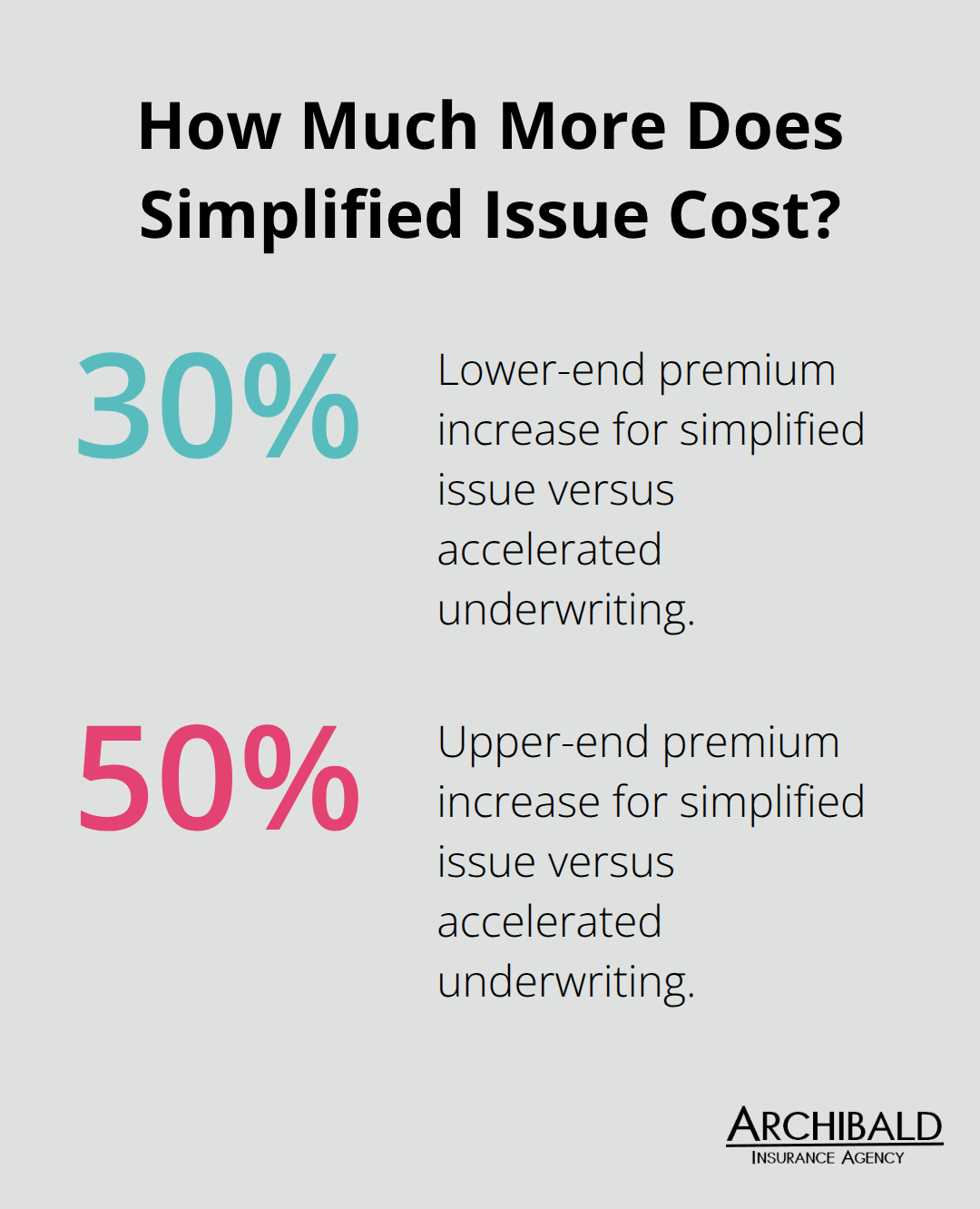

A healthy 35-year-old nonsmoker pays roughly $25.76 monthly for a $500,000 20-year term policy through accelerated underwriting, but simplified issue policies for the same person typically run 30 to 50 percent higher. Guaranteed issue at $25,000 coverage starts around $9.95 monthly, but that low price reflects the tiny benefit amount.

Pacific Life offers up to $3 million without medical exams for ages 18-60, which matters if you’re in decent health. Nationwide Life Essentials provides instant approval up to $1.5 million for qualified applicants using accelerated underwriting.

Speed and Your Decision Factors

The timing question matters too: guaranteed issue approves instantly with zero health questions, simplified issue takes one to two weeks, and accelerated underwriting usually completes within days. Your choice depends on three factors: your current health status, how much coverage you actually need, and whether you can wait a week or two for approval. If you’re healthy, accelerated underwriting wins every time. If you have health concerns or limited funds for premiums, simplified issue beats guaranteed issue because you access real coverage amounts instead of funeral-only limits.

Once you identify which product type matches your situation, the next step involves evaluating specific carriers and comparing quotes to lock in the best rate for your circumstances.

Who Really Benefits from No-Exam Life Insurance

Young Adults Get the Best Rates

No-exam policies work best for specific situations, and applying for one when traditional underwriting makes more sense costs you money. If you’re under 50, in good health, and need coverage within days rather than weeks, accelerated underwriting delivers the strongest outcome. You’ll access competitive rates comparable to fully underwritten policies while avoiding medical exams and lab work. Young adults in their 20s and 30s particularly benefit here-a 30-year-old nonsmoker in Utah pays around $9 to $12 monthly for a $250,000 term policy through no-exam programs, according to pricing data from Insuranceopedia. That’s dramatically cheaper than other life stages and makes accelerated underwriting the obvious choice for this demographic.

Pre-Existing Conditions and Smokers Find Relief

If you have pre-existing conditions like controlled diabetes, depression, or heart disease, simplified issue or guaranteed issue policies remove the barrier of extensive medical scrutiny. Lincoln Financial specifically underwriters people with these conditions favorably and offers no-exam options for situations that would normally trigger additional investigation. Smokers also benefit from no-exam paths because some carriers avoid charging smoker rates when they skip medical exams entirely. Mutual of Omaha’s guaranteed-issue and simplified-issue policies require no medical exam or only limited health questions, making them practical for smokers who face higher premiums through traditional underwriting.

When No-Exam Policies Fall Short

The real weakness of no-exam policies emerges when you need substantial coverage or have limited budget flexibility. Guaranteed issue caps out around $25,000, which only covers funeral costs and final medical bills-not income replacement for a family depending on your paycheck. If you earn $75,000 annually, financial experts recommend carrying 10 to 20 times your salary in coverage, meaning $750,000 to $1.5 million. Simplified issue policies max out around $1 million and cost 30 to 50 percent more than accelerated underwriting for the same person. A healthy 35-year-old nonsmoker pays $25.76 monthly through accelerated underwriting but significantly more through simplified issue, making the premium difference substantial over a 20 or 30-year term.

Traditional Underwriting Wins for Large Coverage Amounts

Traditional underwriting becomes the better choice when you need $2 million or more in coverage, have stable health history, and can wait two to four weeks for approval. You’ll lock in lower rates and access unlimited coverage amounts that actually protect your family’s financial security rather than just cover final expenses. Evaluate your actual coverage need first, then select the policy type that delivers that amount at the lowest cost-not simply choosing no-exam because it sounds faster.

Final Thoughts

No-exam life insurance policies without medical exams work best when you match the product type to your actual situation rather than choosing based on speed alone. Accelerated underwriting delivers competitive rates and quick approvals for healthy applicants under 50, while simplified issue serves people with pre-existing conditions who want to avoid extensive medical scrutiny. Guaranteed issue removes all health barriers but limits coverage to funeral expenses around $25,000, leaving your family severely underprotected if you’re the primary earner.

Start by calculating your real coverage need-financial experts recommend carrying 10 to 20 times your annual salary in life insurance. A healthy 35-year-old nonsmoker pays roughly $25.76 monthly for $500,000 in 20-year term coverage through accelerated underwriting, which provides meaningful protection at an affordable rate. Compare what you actually need against what each product type delivers, then evaluate whether the premium difference justifies choosing a more expensive option with lower coverage limits.

We at Archibald Insurance Agency help Utah residents navigate these decisions by representing multiple carriers and comparing quotes across different product types. Our team assesses your health status, coverage goals, and budget to identify whether accelerated underwriting, simplified issue, or guaranteed issue makes sense for your situation. Contact Archibald Insurance Agency to discuss your options and receive personalized recommendations based on your specific needs.