Combined Home and Auto Insurance Quotes Benefits

Most Utah homeowners and drivers pay too much for insurance because they’re shopping for home and auto coverage separately. We at Archibald Insurance Agency see this mistake constantly, and it costs families hundreds of dollars every year.

Combining your home and auto insurance quotes changes everything. You’ll unlock real savings, simplify your life, and get coverage that actually fits your situation.

How Much Can You Actually Save by Bundling

Real Savings Numbers from Utah Data

Utah residents who bundle home and auto insurance see real savings that go far beyond marketing hype. According to Insure.com’s 2024 analysis using Quadrant Data Services, State Farm offers the largest discount in Utah at 23 percent. Nationwide delivers the lowest bundled rate at $1,972 per year after discount, down from $2,279 before bundling. Farmers saves customers around $708 annually with a 20 percent discount, while Auto-Owners and American Family offer 14 and 10 percent discounts respectively. These aren’t theoretical numbers-they represent what actual Utah ZIP codes pay.

The study examined 4,686 ZIP codes across 48 insurers, so the data reflects your neighborhood specifically.

How Your ZIP Code Affects Your Savings

Bundling typically saves between 5 and 30 percent depending on the carrier, but your location matters enormously. ZIP code 84180 averages about $2,717 after discount, while 84737 sits around $2,184 after discount. This means your exact address determines whether bundling saves you $300 or $700 annually. Two homes with identical coverage can pay vastly different premiums based on local risk factors, claims history, and carrier pricing strategies in that area.

When Bundling Beats Separate Policies

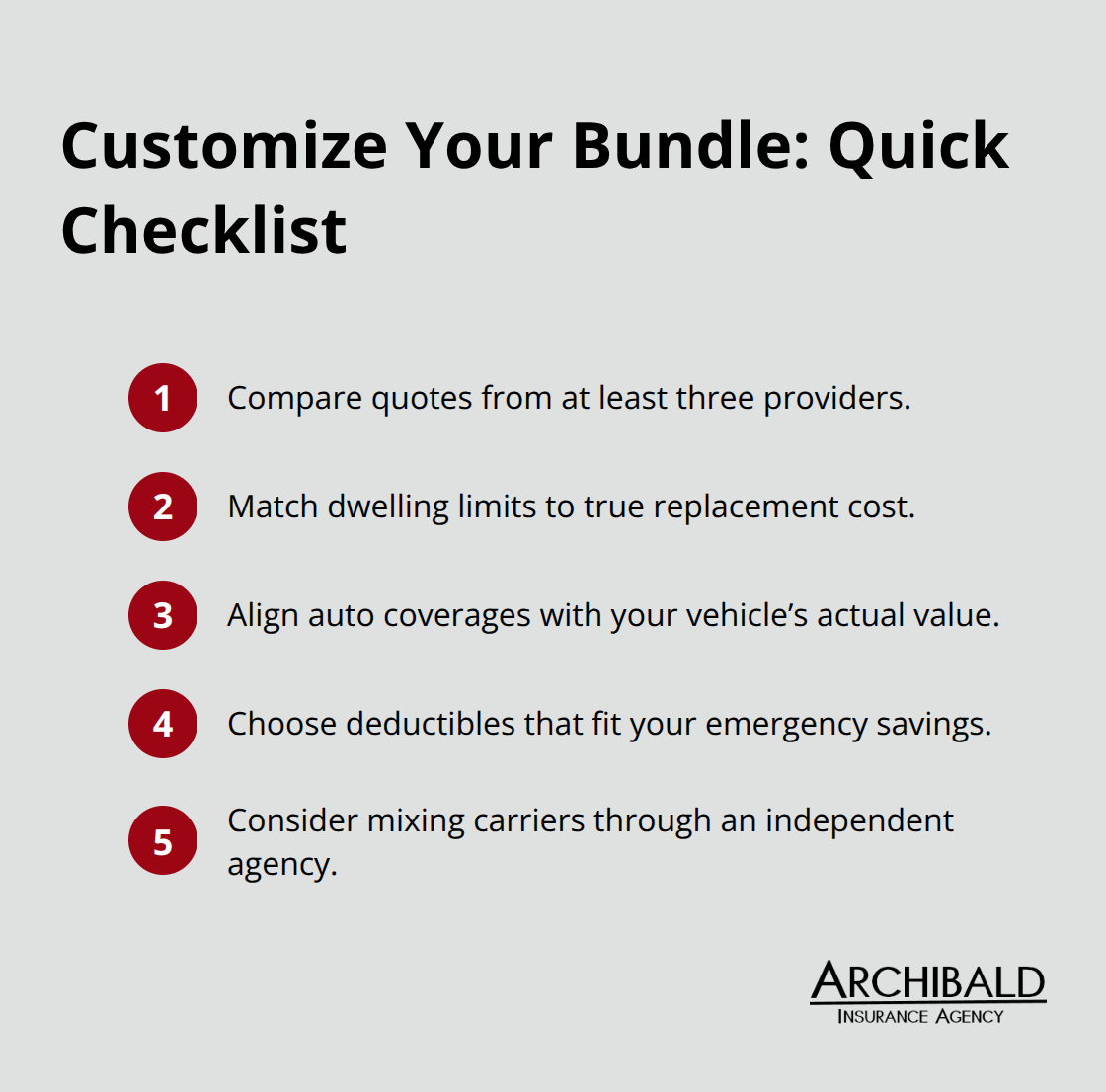

Bundling wins financially in most situations, but not all. If your homeowners coverage costs significantly more with one carrier, you might save more by splitting policies across two companies. Progressive customers report average bundle savings of $1,086 annually for new customers, compared to $946 for auto-only coverage. The key is comparing actual quotes from at least three providers before deciding. Don’t assume the cheapest bundled option is best-verify that coverage limits match your home’s value and your vehicle’s risk level.

Hidden Value in Bundled Policies

Some carriers throw in additional perks when you bundle, like disappearing deductibles where a single incident affecting both policies triggers only one deductible instead of two. Progressive and other carriers offer this benefit, which adds real value beyond the discount percentage. Your situation is unique, so quote multiple combinations: bundled with Carrier A, bundled with Carrier B, and separate policies across different companies. The savings difference often surprises people-sometimes splitting policies saves more than bundling, which is why comparing quotes from multiple carriers matters so much before you make your final decision.

Simplified Management and Convenience

One Bill, One Renewal Date

Separate home and auto policies create administrative chaos. You track two renewal dates, two billing cycles, and two customer portals that operate on different schedules. When you bundle with one carrier, everything consolidates into a single bill that arrives on one date each year. This eliminates the friction that costs you time and mental energy throughout the year. After you move, you make one address change instead of updating two separate accounts.

One phone call handles both your home claim and your auto claim rather than navigating two different claims departments with separate processes and timelines.

One Agent Who Understands Your Complete Picture

When you work with a single agent for both policies, that person understands your entire risk profile. They know your home’s replacement cost and your vehicle’s value, so they spot coverage gaps that slip through when policies live in different places. They identify additional discounts you qualify for across both policies because they review your complete insurance profile at once. This integrated approach prevents costly mistakes like selecting deductibles that don’t align with your actual financial situation.

Faster Claims and Easier Updates

Annual policy reviews take half the time when you discuss two policies with one agent instead of coordinating between multiple providers. Claims settlements move faster because one insurer has complete information about what happened rather than requiring separate investigations. When you need to adjust deductibles or coverage limits, you work with someone who understands how changes to your home policy affect your auto strategy and vice versa.

Independent Agencies Offer the Best of Both Worlds

An independent agency like ours represents multiple carriers while maintaining that single-point-of-contact advantage. You get the bundling benefits of simplified management combined with the flexibility to mix carriers if one company offers better rates on home coverage while another excels at auto pricing in your ZIP code. This approach (combining convenience with competitive pricing) delivers what most bundled policies cannot: personalized solutions that actually fit your situation rather than forcing you into one carrier’s standard package.

The efficiency gains compound over time, and the real advantage emerges when you need to adjust your coverage or file a claim. This foundation of simplified management sets the stage for the customization options that truly make bundled policies work for your specific circumstances.

Customizing Your Bundle to Match Your Reality

Standard Packages Don’t Fit Your Specific Situation

Your home and your vehicles aren’t generic, so your insurance shouldn’t be either. Standard bundled packages often leave you underprotected or overpaying for unnecessary coverage. If your home is worth $450,000 but a bundled package defaults to $400,000 in coverage, you’re underinsured. If your vehicle is a 2015 Honda Civic worth $8,000 but the bundle assumes comprehensive and collision coverage for newer cars, you’re overpaying for protection you don’t need.

This is where independent agencies outperform captive agents who represent only one company. You can mix and match carriers to fit your actual circumstances. Some families find that State Farm’s 23 percent bundle discount works perfectly, while others discover that bundling auto with State Farm and home with Farmers actually saves more money because Farmers’ homeowners rates run lower in their specific ZIP code. You won’t know which combination works best until you test multiple scenarios against your actual needs.

Deductibles Require Real Financial Analysis

Deductibles deserve serious attention when customizing your bundle. Progressive’s single-deductible benefit for bundled policies means if a tree falls on your car and damages your home simultaneously, you pay one deductible instead of two. That’s valuable, but only if you understand what deductible makes sense for your financial situation.

A family with six months of emergency savings can comfortably handle a $2,500 deductible and save significantly on premiums. A family with minimal savings needs the security of a $500 deductible even if it costs more monthly. Your agent should help you stress-test these numbers against your real financial picture, not push you toward whatever generates the biggest discount.

Coverage Limits Must Match Your Assets

Your home’s replacement cost (what it actually costs to rebuild, not what you paid for it) determines your dwelling limit. In Utah, construction costs vary dramatically by location and home age. A 1970s home in Ogden requires different replacement cost estimates than a 2020 home in Park City. Your agent needs to know these specifics to recommend appropriate coverage.

Similarly, your vehicle’s actual value determines whether you need comprehensive and collision coverage. If you’re driving a paid-off 2012 vehicle worth $6,000, carrying $500 deductible collision coverage costs more than the potential payout makes sense. These decisions require actual information about your assets, not assumptions about what you should carry.

Independent Agencies Deliver Customized Solutions

An independent agency represents multiple carriers while maintaining flexibility that captive agents cannot match. You get the bundling benefits of simplified management combined with the ability to mix carriers if one company offers better rates on home coverage while another excels at auto pricing in your ZIP code. This approach delivers what most bundled policies cannot: personalized solutions that actually fit your situation rather than forcing you into one carrier’s standard package.

Final Thoughts

Bundling your home and auto insurance delivers three concrete advantages that matter to Utah families: you save hundreds of dollars annually through multi-policy discounts that range from 10 to 23 percent depending on your carrier and ZIP code, you eliminate administrative friction by consolidating billing and renewals into a single relationship, and you gain the ability to customize coverage that matches your home’s replacement cost and your vehicle’s real value. The combined home and auto insurance quotes you receive should reflect your specific situation, not a one-size-fits-all approach, which is where independent agencies create real value. We at Archibald Insurance Agency represent numerous insurance carriers, allowing us to compare bundled options across multiple companies and find the combination that saves you the most money while protecting your assets properly.

Our team understands Utah’s insurance landscape because we work within it every day. We know how ZIP code affects your rates, which carriers offer the best coverage options for your specific needs, and how to structure deductibles that match your financial reality rather than chase the lowest premium. We build relationships based on trust and reliability, which means we’re here when you need to adjust coverage after a life change or when you file a claim.

Contact Archibald Insurance Agency in Salt Lake City to discuss your home and auto insurance needs. We’ll gather information about your home’s value, your vehicles, and your financial situation, then present options that fit your life. No pressure, no generic packages, just personalized solutions from an agency that serves Utah families.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation