How to Lower Your Car Insurance Rates in Utah

Utah drivers pay an average of $1,456 annually for car insurance, but most people don’t realize how much they could save with the right strategy. Your driving record, vehicle type, and age all play a role in what you pay each month.

At Archibald Insurance Agency, we’ve helped countless Utah residents lower their car insurance rates by identifying savings they didn’t know existed. This guide walks you through the specific factors affecting your premiums and the practical steps you can take right now.

What Really Drives Your Utah Car Insurance Rates

Your Driving Record Sets the Foundation

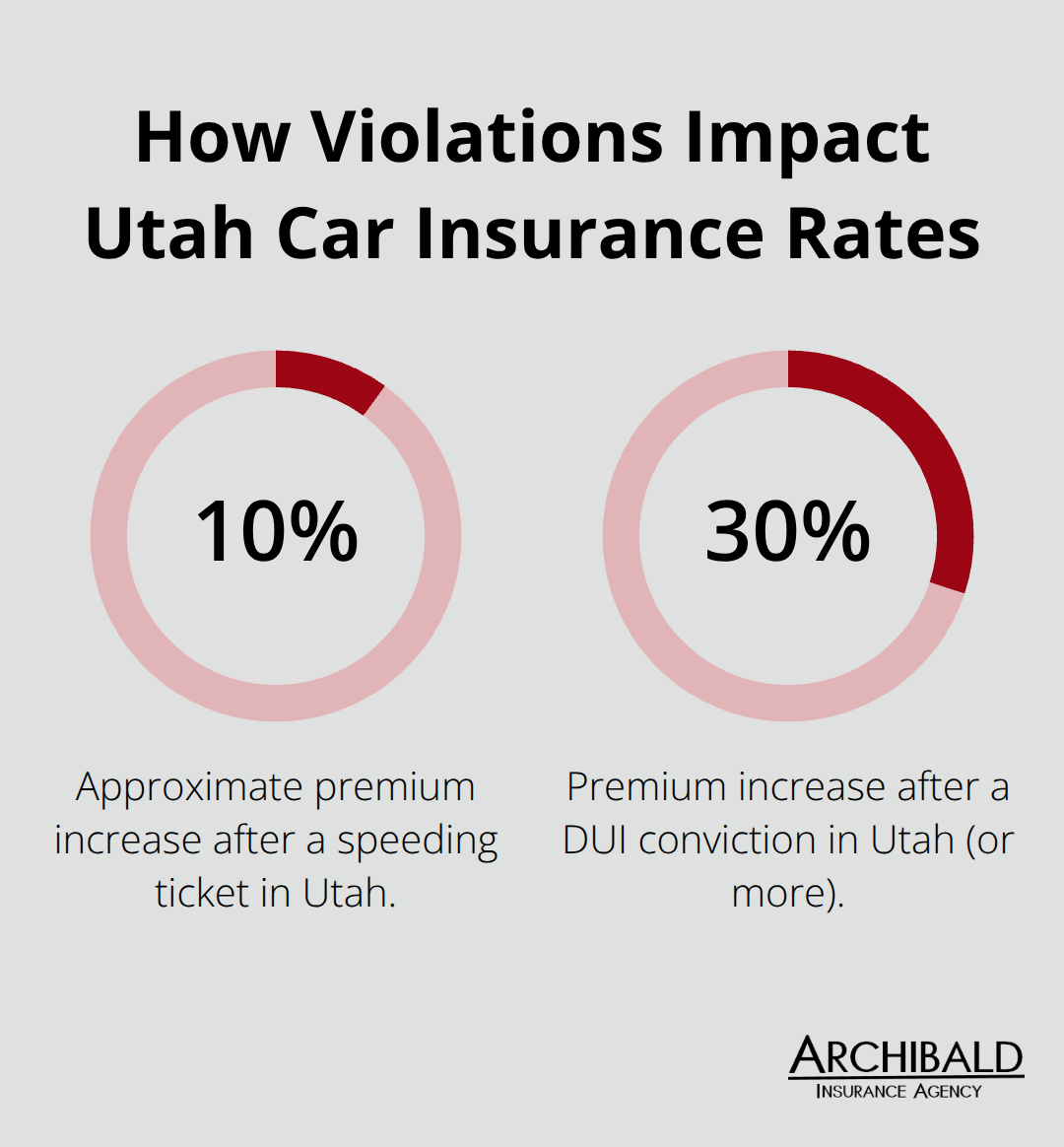

Your driving record stands as the single most important factor determining what you pay for car insurance in Utah. A speeding ticket raises your premium by approximately 10 percent, while a DUI conviction increases rates by 30 percent or more. Utah law requires that rates remain not excessive, inadequate, or unfairly discriminatory, which means insurers must justify every dollar they charge based on documented risk factors.

Accidents and violations within the past three years follow you through renewal cycles. The positive side: clean driving records compound over time. Drivers who avoid claims and violations for three or more years see meaningful reductions at renewal.

Vehicle Type and Claims History

The vehicle you drive matters more than most people realize because insurers review claims data for each make and model to calculate premiums. A Honda Civic typically costs less to insure than a Dodge Charger because the Civic has a lower claims history and cheaper repair costs. Expensive luxury vehicles and high-performance sports cars carry substantially higher premiums due to repair expenses and theft risk. Before purchasing a new vehicle, check the Insurance Institute for Highway Safety ratings-this step can save thousands over the life of your ownership. Safer vehicles with advanced safety features often qualify for discounts that offset some of the higher base premiums.

Age, Experience, and Location

Drivers under 25 pay roughly double what drivers in their 40s pay for identical coverage, according to industry pricing models. A 19-year-old male driver in Utah typically pays $2,800 to $3,200 annually while a 45-year-old pays $1,200 to $1,500 for the same car and coverage. This gap exists because younger drivers have statistically higher accident rates regardless of individual driving habits. Completing an approved defensive driving course reduces premiums for drivers of any age-State Farm and other carriers offer discounts for courses that meet Utah Code Annotated 3/A-19a-211 standards. The discount lasts three years from completion, making a one-time course investment worthwhile.

Gender also influences rates, with male drivers typically paying more than female drivers in the same age bracket. Where you live in Utah affects your rate as well since urban areas with higher accident and theft frequency command higher premiums than rural communities. Salt Lake City residents pay more than someone in a smaller town due to increased exposure to accidents and vehicle theft.

Moving Forward With Your Coverage

Understanding these rate factors helps you recognize which elements you can control and which ones you cannot. Your next step involves examining your current coverage and identifying which discounts apply to your specific situation.

How to Actually Save Money on Your Utah Car Insurance

Bundle Your Policies for Immediate Savings

Bundling your auto policy with homeowners or renters insurance delivers the most straightforward savings available to Utah drivers. Bundle your policies for immediate savings with discounts that reduce your auto premium by approximately 25 percent depending on the insurer and your location. If you carry homeowners insurance with one company and auto with another, you leave money on the table every single month. Consolidating these policies takes roughly 15 minutes to arrange and produces immediate savings at your next renewal. Bundling can save you $847 per year compared to separate policies.

Stack Multiple Discounts Together

Utah insurers stack multiple discounts that compound when applied together. A clean driving record qualifies you for good driver discounts that reduce premiums when no household members have filed claims. Defensive driving courses certified under Utah Code Annotated 3/A-19a-211 generate discounts lasting three years from completion, with courses costing between $20 and $50 online. Vehicles equipped with advanced safety features like automatic emergency braking and lane departure warning systems often receive additional premium reductions. These discounts exist across most major carriers, yet many drivers never inquire about them during renewal conversations. Asking your agent specifically which discounts apply to your situation typically uncovers $200 to $400 in annual savings you weren’t receiving before.

Raise Your Deductible Strategically

Raise your deductible strategically from $500 to $1,000 to typically save 20-25% on your car insurance premiums annually. The trade-off is straightforward: you pay less monthly but more out of pocket if an accident occurs. This strategy only makes sense if you have emergency savings covering your chosen deductible amount without creating financial hardship. A driver with $5,000 in liquid savings can comfortably raise their deductible to $1,000. Someone living paycheck to paycheck should maintain a $500 deductible regardless of premium savings, since a major accident would trigger financial crisis. Utah drivers should calculate their actual break-even point: if raising your deductible saves $300 annually but costs $500 more if you file a claim, you need to avoid accidents for two years just to break even.

Shop Around Before Making Changes

These savings strategies work best when you compare quotes across multiple carriers to see which company offers the lowest rates for your specific situation. Different insurers weight factors differently, meaning one carrier might charge significantly less than another for identical coverage. Getting three to five quotes takes roughly 30 minutes and reveals whether your current insurer remains competitive or whether switching would produce substantial savings. Once you identify the best rates and applicable discounts, you can move forward with confidence knowing you’ve made an informed decision about your coverage and costs.

How a Local Agent Beats Shopping Alone

Access to Rates and Discounts You Won’t Find Online

Local independent agents represent multiple insurance carriers, which means they access rates and discounts that individual shoppers never see when comparing online. When you submit quotes through comparison websites, you’re limited to whatever algorithms those platforms prioritize, often favoring larger national carriers that pay for premium placement. Direct relationships with underwriters at companies like State Farm and Progressive reveal exactly which discounts apply to your specific situation.

A 55-year-old driver in Salt Lake City who completed a defensive driving course within the last three years qualifies for discounts that vary dramatically between carriers-one company might offer 10 percent off while another offers 25 percent. Online quote tools don’t capture these nuances because they rely on standardized rating algorithms rather than actual underwriter discretion.

Understanding Which Carriers Fit Your Risk Profile

Different insurers weight factors differently, meaning one carrier might charge significantly less than another for identical coverage. An independent agent knows which carriers offer the best rates for drivers with recent violations, which companies provide the steepest discounts for bundling, and which insurers have the loosest underwriting criteria for your particular risk profile. This knowledge translates directly into lower premiums. A Utah driver switching from a national carrier to a regional company often saves $400 to $800 annually on identical coverage simply because that carrier prices your risk category more favorably.

Matching Coverage to Your Actual Financial Situation

Finding the right coverage limits requires understanding your actual financial exposure, not following generic recommendations. Many Utah drivers either over-insure and waste money on coverage they don’t need or under-insure and face catastrophic financial risk after a serious accident. An agent analyzes your assets, your vehicle value, your driving patterns, and your financial situation to recommend coverage that protects what matters without padding your premium with unnecessary protection. A 28-year-old with $15,000 in savings and a financed vehicle needs different coverage than a 52-year-old with $300,000 in home equity and paid-off cars.

Monitoring Your Policy Throughout the Year

An independent agent monitors your policy annually rather than waiting until renewal to discuss changes. When you turn 25, you qualify for better rates. When you pay off your vehicle loan, dropping collision coverage becomes an option. When you complete a defensive driving course, that discount applies immediately rather than waiting for your renewal date. This ongoing relationship means your premium stays competitive year after year instead of slowly creeping upward as you miss available savings.

Final Thoughts

Lowering your car insurance rates in Utah requires three core actions: understanding what drives your premiums, claiming available discounts, and working with someone who knows the market. Your driving record, vehicle type, and age establish your baseline costs, but bundling policies, stacking discounts, and adjusting deductibles put real control back in your hands. Most Utah drivers forfeit hundreds of dollars annually simply because they never ask about discounts or compare their current coverage to what’s actually available.

Start by reviewing your current policy to identify which discounts you already receive and which ones you’re missing. If you completed a defensive driving course within the last three years, that discount should be active right now. If your household maintains a clean driving record, you qualify for good driver discounts that many people overlook. These actions compound into meaningful savings when you contact Archibald Insurance Agency to review your coverage and discover how much you could save.

Our team represents multiple insurance carriers, which means we show you exactly which company offers the best rates for your risk profile rather than limiting you to whatever comparison websites prioritize. We understand Utah’s specific insurance landscape and know which carriers offer the steepest discounts for bundling, defensive driving courses, and safety features on your vehicle. Our family-owned team in Salt Lake City monitors your policy throughout the year so you never miss an opportunity to lower how to lower car insurance rates when your circumstances change.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation