Independent Agents Salt Lake: Your Local Insurance Advantage

Insurance decisions in Salt Lake City shouldn’t feel overwhelming. Whether you’re protecting your family’s home, your business, or your vehicles, independent agents in Salt Lake offer something direct insurers simply can’t match: genuine local expertise combined with access to multiple carriers.

At Archibald Insurance Agency, we’ve built our reputation on understanding Utah’s unique insurance landscape and matching families and businesses with coverage that actually fits their lives.

What Makes Independent Agents Stand Out in Salt Lake

Access to Multiple Carriers and Better Rates

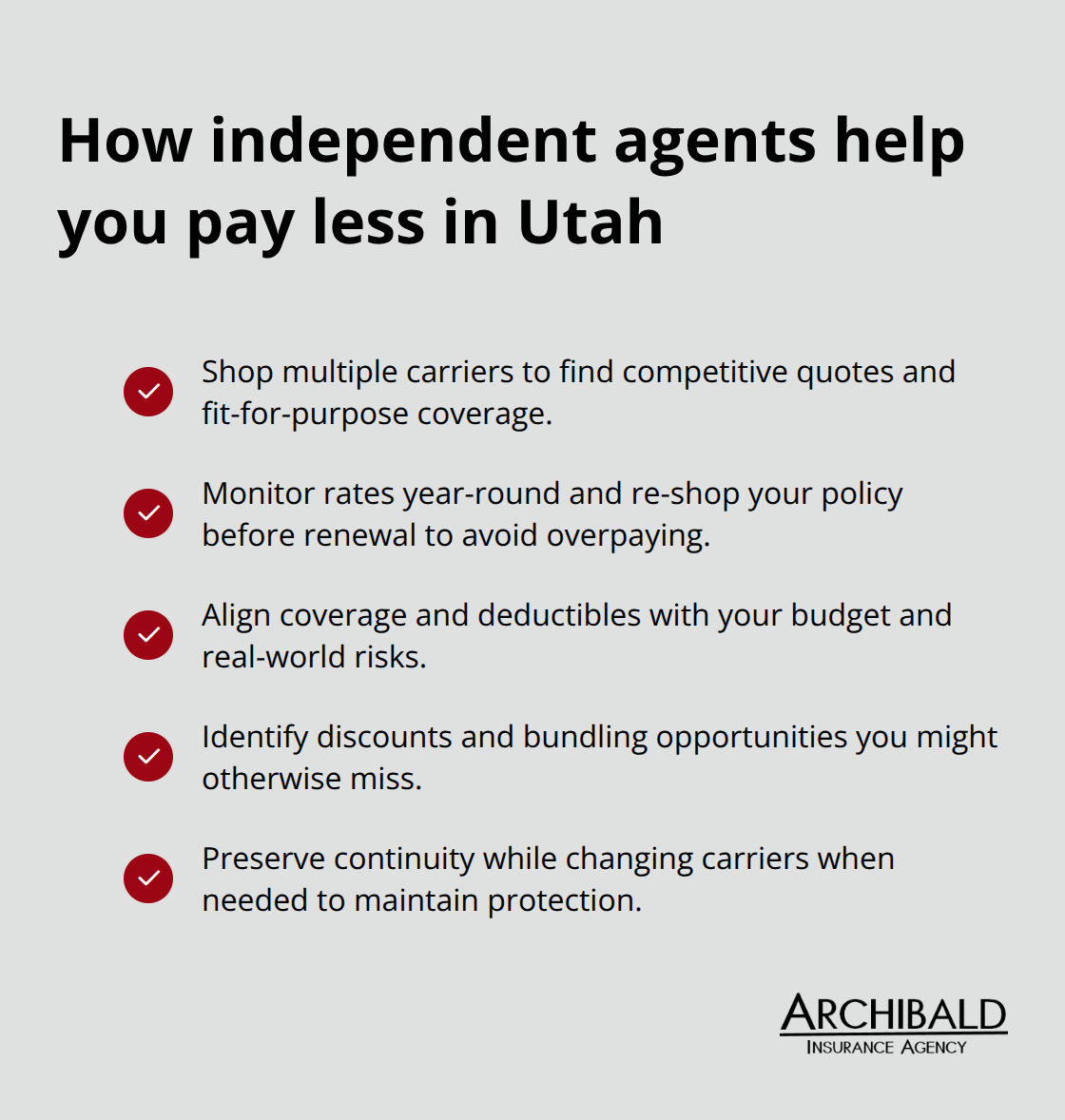

Independent agents work with multiple insurance carriers, which gives us access to rates and coverage options that captive agents cannot match. When you work with an agent tied to a single insurer, you’re limited to what that one company provides. We shop across carriers like Chubb, Travelers, and Safeco, comparing quotes to find the best combination of price and protection for your situation.

Independent agents monitor rate changes year-round, and when your rate jumps, we shop your policy with other carriers before your renewal arrives. A family paying $1,200 annually for auto insurance might save $200 to $400 per year through competitive shopping alone-that adds up to thousands over a decade.

Understanding Local Risks and Weather Patterns

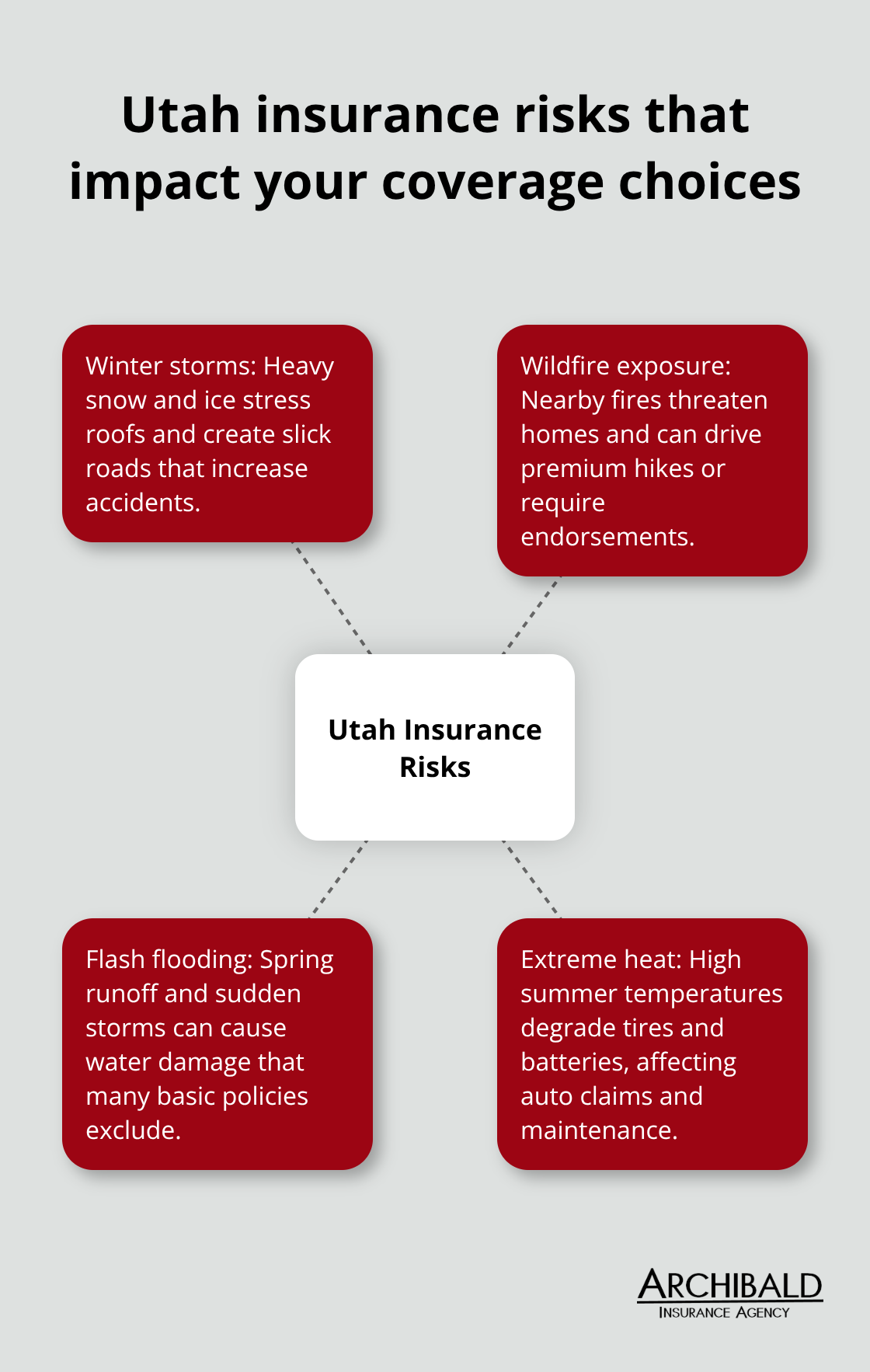

Salt Lake’s winter snow, wildfire risks, and flash flooding create specific insurance needs that national call centers don’t understand. These weather patterns raise claim rates and affect how insurers price coverage. We assess whether your homeowners policy adequately covers these local risks or if you need additional protection.

For businesses, this local insight proves even more valuable. A contractor working in Utah’s varied elevations faces different liability exposures than one in a flat region. We tailor commercial policies to match what you actually do, not generic templates that miss critical details.

Continuity and Advocacy When Claims Happen

Independent agents build relationships with clients over years, not transactions. When claims occur, you contact someone who knows your situation, not a claims center number. That continuity means faster resolution and someone actively advocating for fair treatment from the insurer. This local connection transforms how you experience insurance-from a distant transaction into a partnership with someone invested in your protection.

How Direct Insurers Fall Short for Utah Residents

The Coverage Gap When You Shop Alone

Direct insurers operate on a simple model: they sell you their policies through websites, phone lines, and apps. No agent involved. No local expertise. No one to call when something goes wrong. For Utah residents facing complex insurance decisions, this approach creates real gaps in coverage and protection. When you buy directly from an insurer, you make coverage decisions alone. Most people don’t know what homeowners insurance actually covers or what liability limits they need for their specific situation. Direct insurers won’t tell you that Utah’s wildfire risk has increased significantly in recent years, affecting how much coverage you truly need. They won’t identify that your business liability exposure differs based on your industry and customer base. You receive generic recommendations designed to fit everyone and protect no one specifically.

Customization That Direct Insurers Cannot Provide

An independent agent asks detailed questions about your life, your business, and your risks. We then match you with carriers that specialize in your specific situation. A contractor in Utah needs different commercial auto coverage than a retail business owner. A family with teenage drivers needs different auto insurance strategies than empty nesters. Direct insurers can’t customize this way because they only sell one company’s products. When your circumstances change, direct insurers don’t proactively shop your coverage. Your rate increases at renewal, and you either accept it or switch companies entirely, losing continuity and your claims history.

Year-Round Rate Monitoring and Shopping

Independent agents monitor rate changes continuously and shop your policy with competitors before renewal arrives. This year-round attention typically saves clients 10 to 20 percent compared to staying with a direct insurer that raised rates. A family paying $1,200 annually for auto insurance might save $200 to $400 per year through competitive shopping alone-that adds up to thousands over a decade. Direct insurers have no incentive to shop your business elsewhere; they profit when you stay and accept higher premiums.

Claims Handling: Where the Real Difference Emerges

Direct insurers employ claims adjusters who process thousands of cases. You’re a claim number, not a person. If the insurer denies your claim or offers a low settlement, you negotiate with a faceless system. Independent agents advocate directly with insurers on your behalf. We know the adjusters, understand their processes, and can push back when settlements seem unfair. This personal connection accelerates claim resolution and often results in better outcomes for clients. When a water damage claim or liability dispute arises, having someone in your corner who speaks the insurer’s language makes all the difference.

Local Expertise Meets Carrier Access

Utah’s weather patterns, wildfire risks, and flash flooding create specific insurance needs that national call centers don’t understand. These conditions raise claim rates and affect how insurers price coverage. An independent agent assesses whether your homeowners policy adequately covers these local risks or if you need additional protection. For businesses, this local insight proves even more valuable. A contractor working in Utah’s varied elevations faces different liability exposures than one in a flat region. Independent agents tailor commercial policies to match what you actually do, not generic templates that miss critical details. This combination of local knowledge and access to multiple carriers positions independent agents to serve Utah residents far better than direct insurers can-and it’s why the next step involves understanding exactly which coverage types matter most for your specific situation.

What Coverage Matters Most for Utah Families and Businesses

Utah’s climate and geography demand insurance choices that go beyond standard templates. Winter storms bring heavy snow that stresses roofs and gutters, while summers expose vehicles to extreme heat that degrades tires and battery performance. Wildfires in nearby areas threaten homes even in suburban neighborhoods, and flash flooding during spring runoff creates water damage risks that many homeowners think their policies cover when they actually don’t.

Auto Insurance for Utah Winter Driving

Auto insurance in Utah must account for winter driving conditions that significantly increase accident risk. The National Highway Traffic Safety Administration reports that winter weather contributes to crash fatalities annually across the United States, with snow and ice accounting for a substantial portion. Utah drivers face icy mountain passes, sudden whiteout conditions, and roads that freeze before appearing wet.

Your liability limits matter here because a serious winter accident involving multiple vehicles or pedestrians can generate medical bills exceeding $100,000 quickly. Collision and comprehensive coverage protect your vehicle when weather causes damage, but many Utah drivers carry minimums that don’t reflect replacement costs for newer vehicles. A 2023 vehicle costs $35,000 to $45,000 on average, yet drivers often carry $500 or $1,000 deductibles that made sense when cars cost half that amount.

Homeowners Coverage for Wildfire and Water Damage

Homeowners insurance in Utah requires understanding local wildfire exposure and water damage separately. The state experienced significant wildfire activity in recent years, with some areas seeing insurance premiums jump over 40 percent. Standard homeowners policies exclude wildfire damage in high-risk zones or require separate endorsements that cost extra.

Most homeowners don’t realize that water damage from snow melt, ice dams, or heavy rain requires specific coverage that basic policies may not include. Utah’s spring runoff and winter precipitation patterns create water damage exposure that national insurers often underestimate. Your policy needs to address these local threats rather than hypothetical scenarios that don’t apply to your region.

Commercial Coverage for Utah Contractors and Service Businesses

A contractor or service business operating across Utah faces exposure that varies dramatically by location and industry type. A landscaping company working in the Wasatch Mountains encounters different liability risks than one in the Salt Lake Valley. Commercial auto policies for contractors must cover both owned vehicles and hired or non-owned vehicles used for business purposes, a distinction that direct insurers often oversimplify.

Workers compensation requirements vary based on how many employees you have and what work they perform, and missteps here create serious penalties. Utah law requires employers with employees to carry coverage, and violations result in substantial fines plus potential criminal liability. The right commercial policy addresses your specific operations rather than applying generic templates that miss critical details about your business.

Final Thoughts

Utah’s insurance landscape demands more than generic policies and distant customer service. Independent agents in Salt Lake understand state-specific requirements like the Insure-Rite verification system, local wildfire exposure, and winter driving risks that national insurers overlook. When you work with us, you gain access to professionals who know how to keep you compliant while protecting what matters most without overpaying for unnecessary coverage.

Local independent agents invest in their communities in ways national insurers cannot. We build relationships with families and business owners across Utah, understanding how wildfire exposure affects your home, how winter conditions impact your auto insurance needs, and how your specific business operations require tailored commercial coverage. This community investment means your agent has real accountability-your success and protection directly affect our reputation and our business.

When you’re ready to experience the difference that local expertise and carrier access make, contact Archibald Insurance Agency to discuss your coverage needs. We’ll shop your situation across multiple carriers, identify gaps in your current protection, and build a plan that reflects your life in Utah.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation