Guaranteed Issue Life: What It Means For Your Coverage

Getting older or managing health conditions shouldn’t disqualify you from life insurance protection. Guaranteed issue life insurance removes the medical exam barrier, making coverage accessible when traditional policies won’t.

At Archibald Insurance Agency, we help Utah families understand this option and determine if it fits their needs. This guide breaks down how guaranteed issue policies work, their real advantages, and the trade-offs you should know about.

What Guaranteed Issue Life Insurance Actually Is

Guaranteed issue life insurance is a whole life policy that accepts you without medical exams or health questions. The insurer guarantees coverage based solely on your age, typically between 50 and 80 years old depending on the carrier. This permanent coverage lasts your entire life as long as you pay premiums, which remain level and never increase. The trade-off for guaranteed acceptance is a waiting period, usually two to three years, during which death benefits are limited. If you die from natural causes during this period, your beneficiary receives only a return of premiums paid plus interest, not the full death benefit. Accidental death pays the full benefit immediately, even during the waiting period. After the waiting period ends, your beneficiary receives the complete death benefit regardless of cause.

Coverage amounts typically range from $5,000 to $25,000, designed primarily to cover final expenses like funeral costs, which averaged $8,300 in 2023.

How it differs from traditional life insurance

Traditional life insurance requires medical underwriting, meaning the insurer reviews your health history, runs lab tests, and asks detailed health questions before deciding whether to cover you. Many people face denial because of pre-existing conditions like diabetes, heart disease, cancer, or respiratory issues. Guaranteed issue skips all of this. You answer no health questions and take no medical exam. The approval decision happens within days, sometimes hours. Traditional policies offer much higher death benefits, often $250,000 or more, at lower premiums because insurers can assess individual risk. Guaranteed issue policies cap benefits lower because the insurer cannot screen for serious health conditions. Both policies build permanent cash value over time, which you can borrow against, but guaranteed issue policies charge significantly higher premiums relative to the death benefit amount.

Who actually qualifies

If you are between 50 and 80 years old and live in most U.S. states, you likely qualify. Your health history does not matter. Terminal illness, dialysis, organ transplants, HIV/AIDS, dementia, or chronic conditions do not disqualify you. You simply need to be a U.S. citizen or permanent resident and currently reside in the United States. Some states have different age limits; New York residents, for example, can apply up to age 75 rather than 80. Montana does not offer these policies. If you previously applied for standard life insurance and faced rejection due to health issues, guaranteed issue becomes your practical option. Seniors especially benefit because new health conditions often emerge with age, making traditional underwriting increasingly difficult.

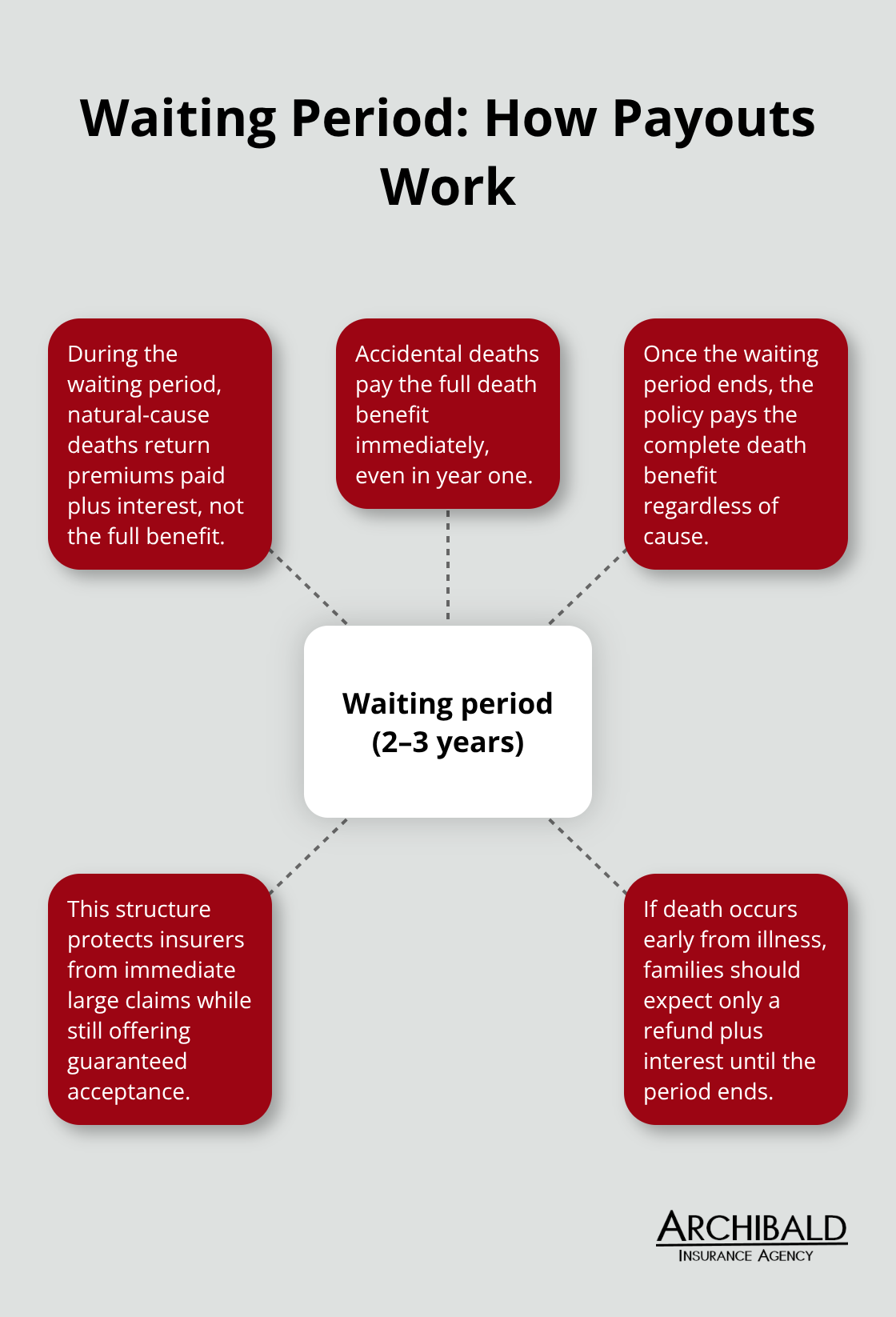

What happens during the waiting period

The waiting period (typically two to three years) fundamentally shapes how your coverage works initially. During this time, natural-cause deaths trigger a reduced payout-your beneficiary receives only the premiums you paid plus interest, not the full death benefit. This structure protects insurers from covering applicants with terminal diagnoses who might otherwise apply specifically to cash out quickly. Accidental deaths, however, pay the full benefit immediately, even in year one. Once you pass the waiting period, the policy operates like standard whole life insurance, paying the complete death benefit regardless of how you die. This distinction matters significantly if you have serious health concerns, as it affects what your family actually receives in the near term.

Cash value and borrowing options

Guaranteed issue policies build cash value as you pay premiums over time. This cash value grows slowly but steadily, and you can borrow against it or withdraw funds if needed. Loans accrue interest, and unpaid loans reduce both your cash value and the death benefit your beneficiary ultimately receives. Withdrawals may trigger tax consequences depending on how much you take out. This flexibility distinguishes whole life policies from term insurance, which builds no cash value. The cash value feature means your policy functions as both protection and a modest financial tool, though the primary purpose remains covering final expenses. Understanding these mechanics helps you decide whether guaranteed issue aligns with your broader financial picture and what role you want this coverage to play in your estate planning.

Why Guaranteed Issue Gets You Covered Fast

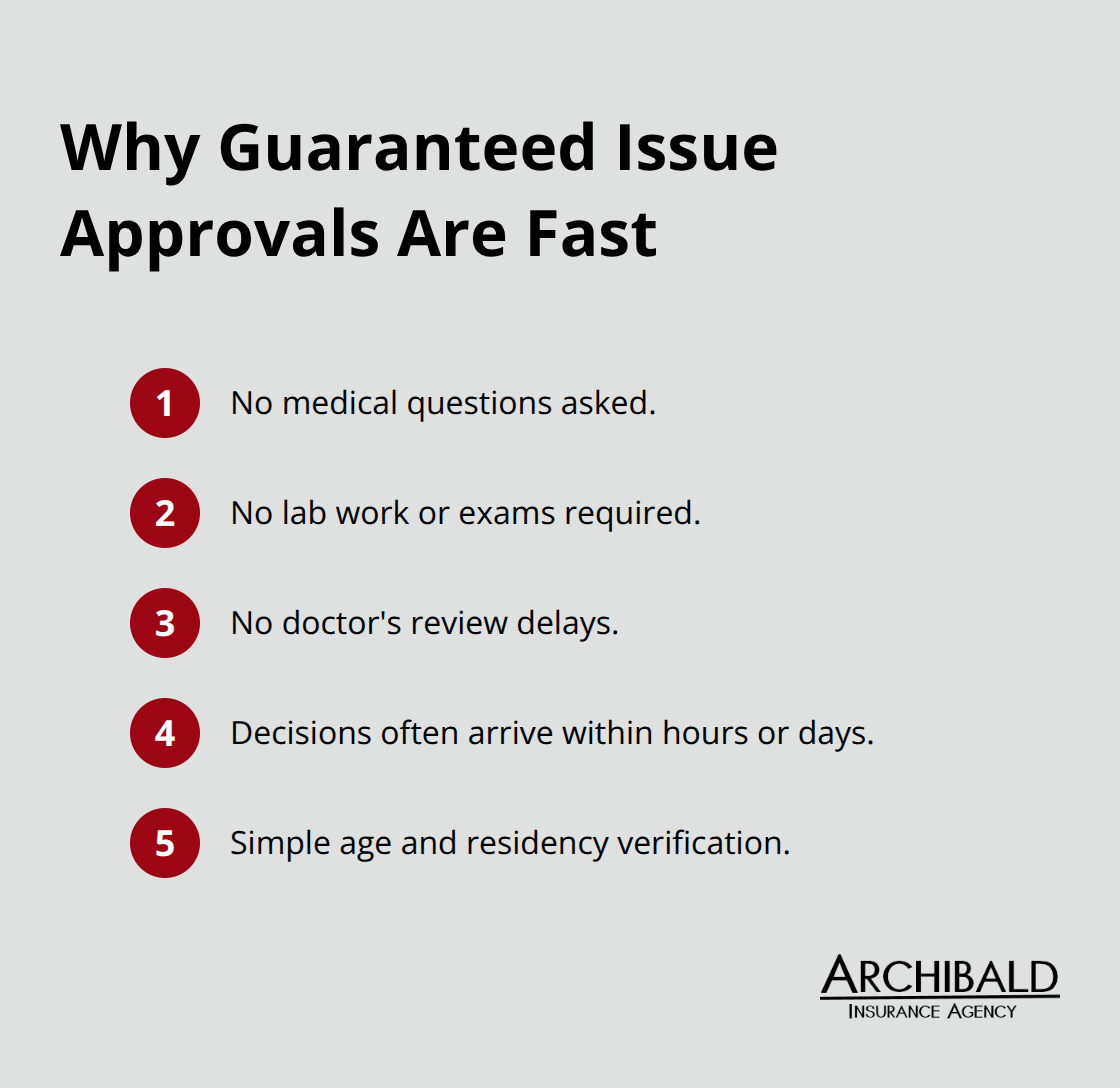

No Medical Questions, No Delays

The speed and simplicity of guaranteed issue life insurance separate it from every other coverage option available to Utah residents. When you apply, the insurer asks nothing about your medical history, medications, surgeries, or current health status. No forms request details about diabetes, heart conditions, cancer, or any other diagnosis. No lab work, no blood tests, no doctor’s review.

Underwriting can take as little as 24 hours but could last 4 to 6 weeks depending on policy complexity. State Farm’s Guaranteed Issue Final Expense Life delivers instant coverage decisions through a simple quote and application process. Progressive Life via eFinancial offers the same speed. For someone managing multiple health conditions or facing a tight timeline, this matters enormously. You submit your application, confirm your age and residency, and coverage begins without the gatekeeping that blocks so many people from traditional policies.

Who Gets Accepted Immediately

This accessibility transforms life insurance from an impossible goal into an achievable one for people whom traditional insurers reject outright. Someone with stage three kidney disease, requiring dialysis three times weekly, qualifies immediately. A 72-year-old who survived a heart attack five years ago faces no questions about cardiac history. A person living with HIV or managing dementia gets accepted without hesitation. Gerber Life Insurance Company’s Guaranteed Life policy exemplifies this approach, requiring only U.S. citizenship or permanent resident status and current U.S. residence. The policy cannot be canceled by the insurer once coverage begins as long as you pay premiums. This guarantee provides certainty that traditional underwriting never offers. You control the relationship going forward.

Speed Solves Real Problems

The speed also matters practically: if you need coverage within weeks rather than months, guaranteed issue delivers what you need. The trade-off of higher premiums and lower death benefits becomes worthwhile when the alternative is remaining uninsured. For Utah families facing health challenges or age-related barriers, guaranteed issue represents genuine protection when no other option exists. Yet speed and accessibility come with real limitations that affect how much protection you actually receive and what your beneficiary collects during the critical first years of your policy.

What Guaranteed Issue Actually Costs You

The speed and accessibility of guaranteed issue life insurance come at a genuine financial cost that affects both your wallet and your family’s protection. Premiums run significantly higher than traditional whole life policies because insurers cannot screen applicants for health conditions. Someone paying $75 monthly for a guaranteed issue policy with a $15,000 death benefit might obtain a traditional whole life policy with $50,000 in coverage for the same premium after medical underwriting. Progressive Life via eFinancial and State Farm’s Guaranteed Issue Final Expense Life both reflect this pricing reality. A 65-year-old purchasing $15,000 in guaranteed issue coverage typically pays $40 to $60 monthly, while a 65-year-old in excellent health might obtain $100,000 in traditional coverage for comparable or lower premiums. The cost-to-benefit ratio worsens as you age. At 75, guaranteed issue premiums jump sharply because mortality risk increases substantially. This expense structure means guaranteed issue works best when traditional underwriting blocks you entirely, not when you simply prefer to avoid medical exams. If you can qualify for standard coverage, the savings often justify the application process and waiting period.

The Waiting Period Limits What Your Family Receives

The two-to-three-year waiting period fundamentally limits what your family actually receives if you die soon after purchasing the policy. During this window, natural-cause deaths pay only your premiums plus interest, not the full death benefit. If you pay $500 monthly for two years, your beneficiary receives roughly $12,000 plus modest interest instead of the promised $15,000 or $20,000 death benefit. This matters intensely for someone with a terminal diagnosis, serious heart disease, or advanced cancer. The waiting period essentially renders the policy nearly worthless during the period when you need it most. Accidental deaths bypass this restriction and pay the full benefit immediately, but you cannot control how you die. After the waiting period expires, the policy works normally, paying the complete death benefit regardless of cause. This timeline shapes whether guaranteed issue makes financial sense for your specific situation. Someone in stable health with years ahead can absorb the waiting period. Someone managing stage three cancer or severe COPD faces a genuine problem that the policy does not solve in the near term.

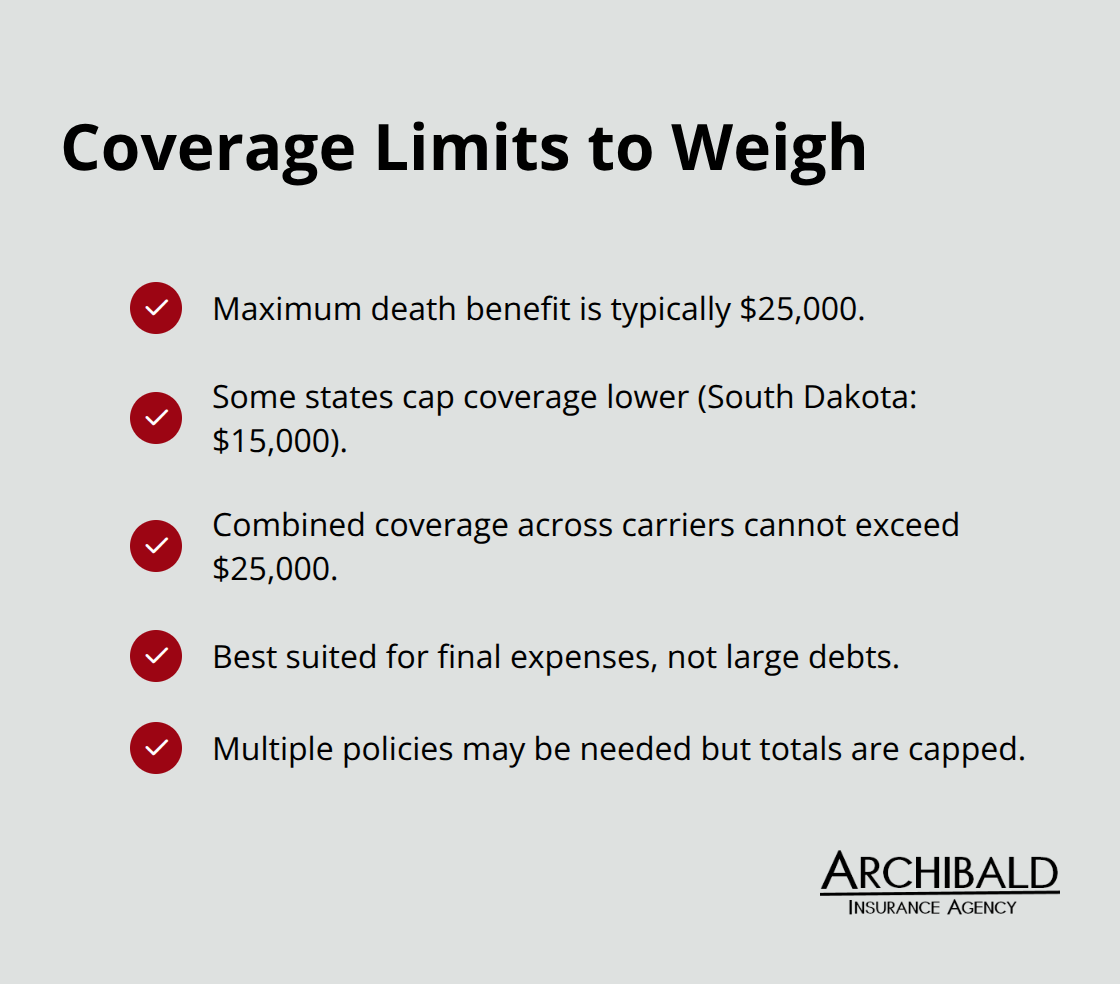

Coverage Limits Force Difficult Decisions

Death benefits max out at $25,000, often lower depending on your state and age. South Dakota caps coverage at $15,000 per person. This limitation reflects the insurer’s inability to assess individual risk through underwriting.

For final expense coverage, $15,000 to $20,000 often suffices since funeral costs average $8,300 for burial and $6,280 for cremation. However, if you have outstanding medical debt, credit card balances, or mortgage payments, $20,000 coverage leaves your family short. Someone with $35,000 in medical bills and funeral costs cannot bridge that gap with a guaranteed issue policy. You might need multiple policies across different carriers, though combined coverage cannot exceed $25,000 total. This ceiling means guaranteed issue addresses only partial final expenses, not comprehensive financial protection. Understanding this limitation prevents the false confidence that a guaranteed issue policy solves all end-of-life financial problems when the actual death benefit falls short of your family’s real obligations.

Final Thoughts

Guaranteed issue life insurance solves a specific problem: it provides coverage when traditional underwriting blocks you due to age or health conditions. The policy delivers speed, guaranteed acceptance, and permanent protection without medical exams or health questions. For Utah residents managing diabetes, heart disease, cancer, or other serious conditions, this accessibility matters enormously.

The trade-offs are real and substantial. Higher premiums, lower death benefits capped at $25,000, and waiting periods that limit payouts during the first two to three years mean guaranteed issue life works best as a targeted solution for final expenses, not comprehensive financial protection. Ask yourself whether you can qualify for traditional life insurance, whether you need coverage within weeks rather than months, and whether your primary goal involves covering funeral costs and outstanding debts rather than leaving a substantial inheritance.

Contact Archibald Insurance Agency to discuss your situation with someone who understands Utah’s insurance landscape and your family’s specific circumstances. Our team represents multiple insurance carriers, so we can show you real quotes and real differences rather than pushing a single product. Getting a quote takes minutes and costs nothing.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation