How to Find the Top Rated Life Insurance Policy

Finding a top rated life insurance policy requires more than just comparing premiums. The financial strength of the insurance company and the specific features of each policy matter just as much.

We at Archibald Insurance Agency help Utah families navigate these complex decisions every day. This guide breaks down the rating systems, policy features, and comparison strategies you need to make an informed choice.

What Do Life Insurance Rating Systems Actually Tell You

AM Best, Standard & Poor’s, Moody’s, and Fitch rate insurance companies based on their ability to pay claims when you need them most. These agencies assign letter grades from A++ down to D, with anything below B+ signaling serious financial concerns. These rating systems provide extensive databases of life/health and property/casualty insurance companies worldwide, offering comprehensive financial analysis that helps consumers evaluate insurer stability.

Financial Strength Ratings Matter More Than Marketing Claims

A company’s financial strength rating reflects its claims-paying ability over decades, not just current year profits. Legal & General America maintains an A rating from AM Best, while companies with lower ratings may offer cheaper premiums but higher risk of future payment issues. The rating agencies analyze debt ratios, reserve adequacy, and management quality with data unavailable to consumers.

Companies rated A- or higher by multiple agencies demonstrate consistent financial performance across different economic cycles, while those with single-agency ratings or B-level grades often face operational challenges that could affect your beneficiaries.

Company Ratings vs Policy Performance Are Completely Different Metrics

Company ratings measure financial stability, while policy performance depends on underwriting practices, claims processing speed, and customer service quality. A highly-rated company might still deny valid claims through aggressive underwriting or delay payments beyond required settlement periods. Within 15 days of receiving notice of loss, insurers must provide necessary claim forms and reasonable assistance to claimants. Lincoln Financial earns strong financial ratings but specializes in coverage for pre-existing conditions (showing how company strength and policy features serve different purposes). Smart buyers examine both the insurer’s AM Best rating and their actual claims payment history, complaint ratios with state regulators, and customer satisfaction scores from J.D. Power studies rather than rely solely on financial strength grades.

How Rating Changes Signal Real Problems

Rating downgrades often precede major company problems by 12-18 months. When agencies lower a company’s rating from A to A-, they typically cite concerns about reserve adequacy or management decisions that could affect future stability. These downgrades matter because they can trigger policy cancellations (as institutional investors often require A-rated or higher carriers) and force companies to raise premiums to maintain profitability. The specific features that make policies truly valuable go beyond these basic financial metrics.

What Makes Life Insurance Policies Worth Your Premium

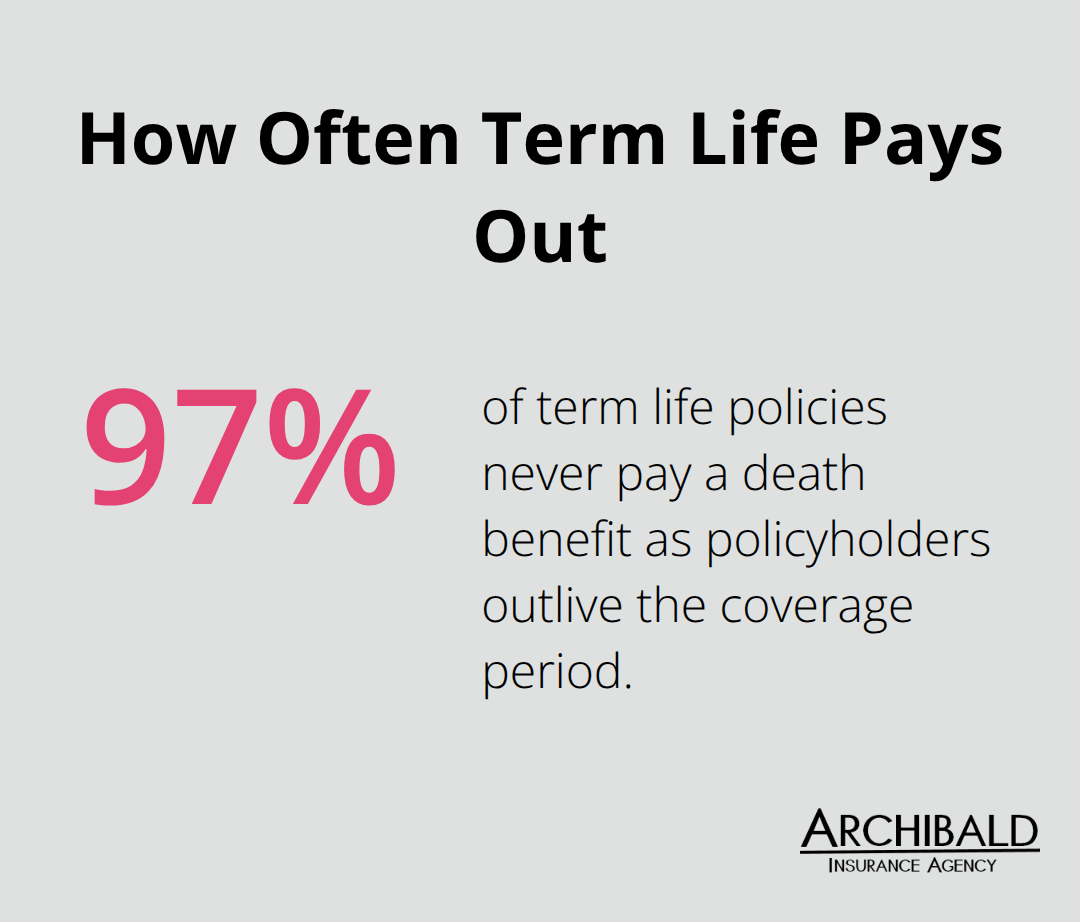

Coverage amounts mean nothing without affordable premiums that fit your actual budget. A healthy 35-year-old female pays around $25.76 monthly for $500,000 in term coverage through Legal & General America, while whole life policies cost 5 to 15 times more for the same death benefit. Term life makes financial sense for temporary needs like mortgage protection or income replacement during child-rearing years, since 97% of term policies never pay death benefits as policyholders outlive their coverage periods. MassMutual leads whole life options for those who need permanent coverage with cash value growth, though these policies require long-term commitment and higher premiums that many families cannot sustain.

Policy Flexibility Separates Good from Great Coverage

Universal life policies from carriers like Lincoln Financial allow premium payment flexibility for those with fluctuating incomes, while guaranteed universal life provides low-cost permanent coverage without complex cash value features. Conversion options in term policies let you switch to permanent coverage without new medical exams as health changes, though this feature expires at specific ages that vary by carrier. Return of premium riders refund all payments if you outlive term coverage but increase costs by 20-30% annually. Pacific Life offers no-medical-exam coverage up to $3 million for those who cannot qualify through traditional underwriting (though premiums reflect the additional risk these policies represent).

Claims Processing Speed Reveals Company Priorities

Utah law requires insurers to timely pay every valid insurance claim, yet some companies consistently exceed reasonable timelines while others pay within 7-10 days. The Utah Life and Health Insurance Guaranty Association protects policyholders up to $500,000 in death benefits if insurers become insolvent (though this safety net cannot replace the need to choose financially stable companies from the start). Customer service quality shows in claim denial rates, appeals processing times, and complaint ratios filed with state regulators rather than marketing promises about support.

Premium Stability Protects Your Long-Term Investment

Term life premiums can increase dramatically at renewal periods, especially for policies without level premium guarantees. Some carriers offer 20-year level term policies that maintain the same premium throughout the entire term, while others provide only 10-year guarantees before rates adjust based on your age and health status. Whole life policies lock in premiums for life but require higher initial payments that strain many family budgets. The key lies in understanding exactly when and how much your premiums might change before you commit to any policy.

These policy features matter most when you need to compare actual options from multiple carriers and evaluate which combination of benefits fits your specific situation.

How Do You Actually Compare Life Insurance Companies

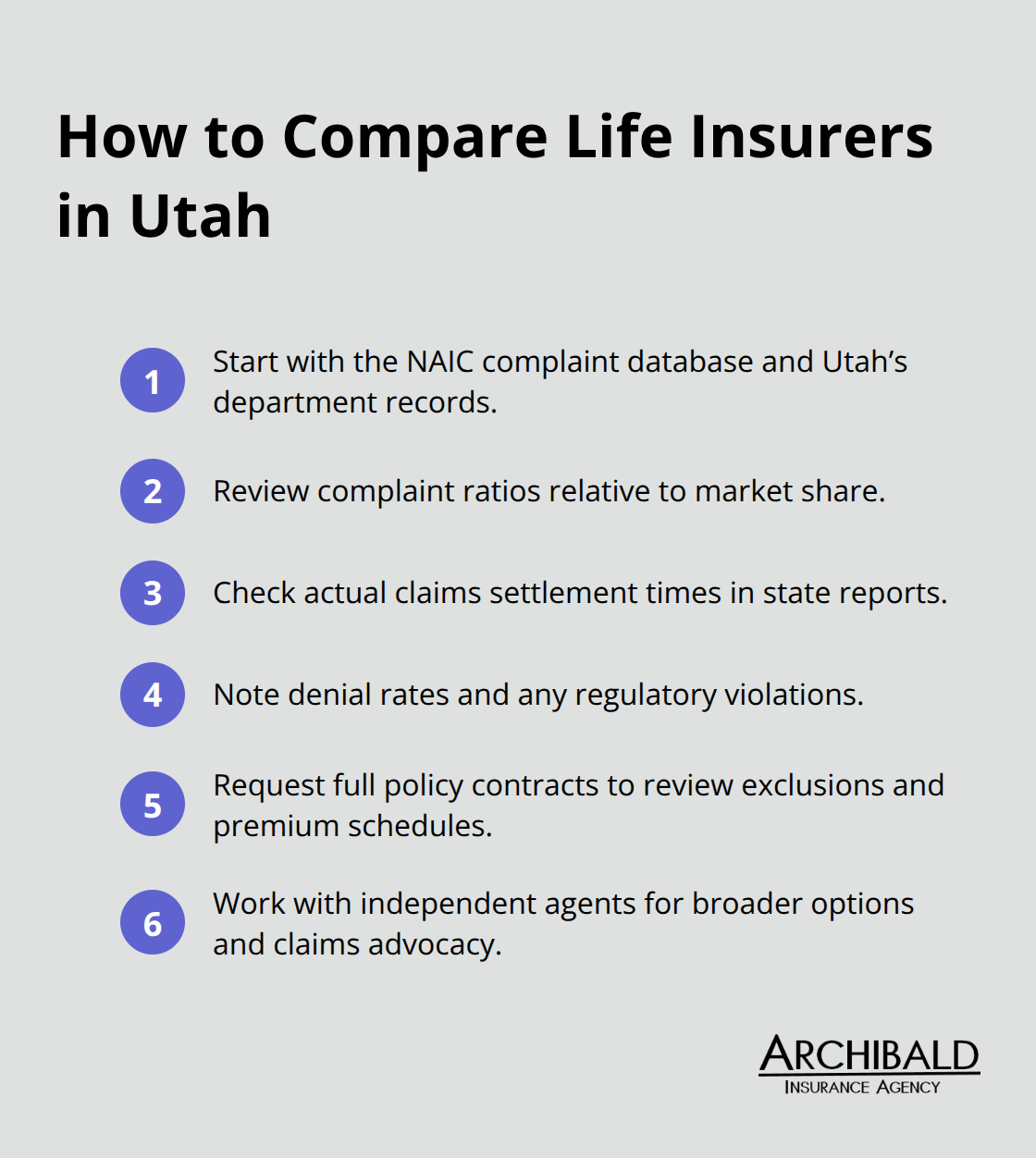

Start with the NAIC’s company complaint database and state insurance department records before you look at marketing materials. Utah’s insurance department publishes complaint ratios that show how often each company faces regulatory action compared to their market share. Legal & General America maintains low complaint ratios while they offer competitive rates that start at $23 monthly for healthy females who seek $500,000 in 20-year term coverage. Pacific Life shows strong performance metrics for no-exam policies up to $3 million, though their complaint data reveals longer processing times for complex underwriting cases.

State Records Reveal Real Company Performance

Check each company’s claims payment speed through state insurance department annual reports rather than rely on company websites that highlight best-case scenarios. These reports show actual settlement times, denial rates, and regulatory violations that marketing materials never mention. Companies with consistent regulatory problems often face higher complaint ratios and slower claims processing (which directly affects your beneficiaries when they need payments most).

Online Tools Miss Critical Policy Details

Comparison websites show premium quotes but hide policy restrictions, medical exam requirements, and renewal terms that affect long-term costs. The NAIC Life Insurance Policy Locator reveals how often companies actually pay claims versus deny them through technicalities, since millions in benefits go unclaimed annually due to poor company communication with beneficiaries. Request actual policy contracts from each carrier to review exclusions, suicide clauses, and premium increase schedules that online calculators cannot capture.

Independent Agents Access Better Options

Lincoln Financial’s pre-existing condition expertise shows in their underwriting guidelines, not their quoted premiums, which makes direct company contact necessary for accurate pricing. Independent agents access wholesale pricing and underwriting flexibility unavailable through direct-to-consumer channels. They handle claims advocacy when companies delay or dispute payments during your family’s most difficult moments, plus they represent multiple carriers to find coverage that fits your specific health and financial situation.

Final Thoughts

You need systematic evaluation of company financial strength ratings, policy features, and actual claims performance data to find a top rated life insurance policy. Start with AM Best ratings of A- or higher, then examine complaint ratios through state insurance departments and premium stability guarantees that protect your investment. These steps help you avoid companies that offer attractive premiums but lack the financial strength to pay claims when your family needs them most.

Your coverage needs change as your financial situation evolves. Marriage, children, mortgage payments, and income growth all affect how much protection you require. Utah residents receive a 10-day free look period and 30-day grace period for missed payments, but these protections cannot replace active policy management (which prevents coverage gaps during life transitions).

Experienced professionals who understand Utah’s insurance landscape can access multiple carriers for comparison and help you navigate complex policy terms. We at Archibald Insurance Agency represent numerous insurance carriers and provide personalized solutions that fit your specific needs and budget. Contact us today to review your life insurance options and secure the protection your family deserves.