Life Insurance Guidance Utah: Smart Steps to Secure Your Family’s Future

Life insurance is one of the most important financial decisions you’ll make, yet many Utah families put it off or choose coverage without fully understanding their options.

At Archibald Insurance Agency, we’ve helped countless residents navigate life insurance guidance in Utah by breaking down the complexity and focusing on what actually matters for your situation. This guide walks you through the types of coverage available, the mistakes to avoid, and how to select a policy that genuinely protects your family’s future.

Life Insurance Types and What Fits Your Situation

Term life insurance and permanent life insurance serve fundamentally different purposes, and the right choice depends on your timeline and budget. Term life covers you for a set period-typically 10, 20, or 30 years-and pays a death benefit only if you die during that term. It’s the most affordable option upfront, making it ideal for families with a mortgage, young children, or specific financial obligations that won’t last forever.

Permanent life insurance, which includes whole life and universal life policies, lasts your entire life and builds cash value you can borrow against. The trade-off is clear: permanent policies cost significantly more each month. For most Utah families, term life offers the best value per premium dollar, especially when you have dependents relying on your income. Permanent life makes sense if you’re older, in excellent health, want lifetime protection, or have estate planning concerns. The key is matching your policy type to how long you actually need coverage-not purchasing more than necessary or settling for less protection than your family requires.

Calculate the coverage amount your family actually needs

Most Utah families underestimate what they need, which is why a Life Needs Analysis matters. Start by adding your mortgage balance, outstanding debts, final expenses (typically $10,000 to $15,000), and income replacement for your dependents. If you earn $60,000 annually and have two children, your family needs roughly 10 years of that income replaced, which means at least $600,000 in coverage. Don’t forget childcare costs-if a non-working spouse dies, the surviving parent must pay for childcare while working, so insure both spouses. Include anticipated college costs if your children are young. Then subtract what your family already has: Social Security survivor benefits, pension plans, and any group life insurance through your employer. This gap is what you actually need to cover with a personal policy. Most Utah families need between $500,000 and $1 million in coverage, but your specific number depends entirely on your obligations and income.

Add riders and additional benefits that protect you

Policy riders allow you to customize coverage without purchasing a separate policy. A conversion rider on a term policy allows you to switch to permanent coverage later without a medical exam, which protects your insurability if your health changes. An accelerated death benefit rider lets you access part of your death benefit early if you’re diagnosed with a terminal illness. A disability waiver of premium means your premiums pause if you become disabled and can’t work, so your coverage stays intact during hardship. These riders add cost, but a few provide real protection. Skip riders that duplicate coverage you already have or address risks unlikely to affect you. Your agent can explain which riders make sense for your situation rather than adding them automatically.

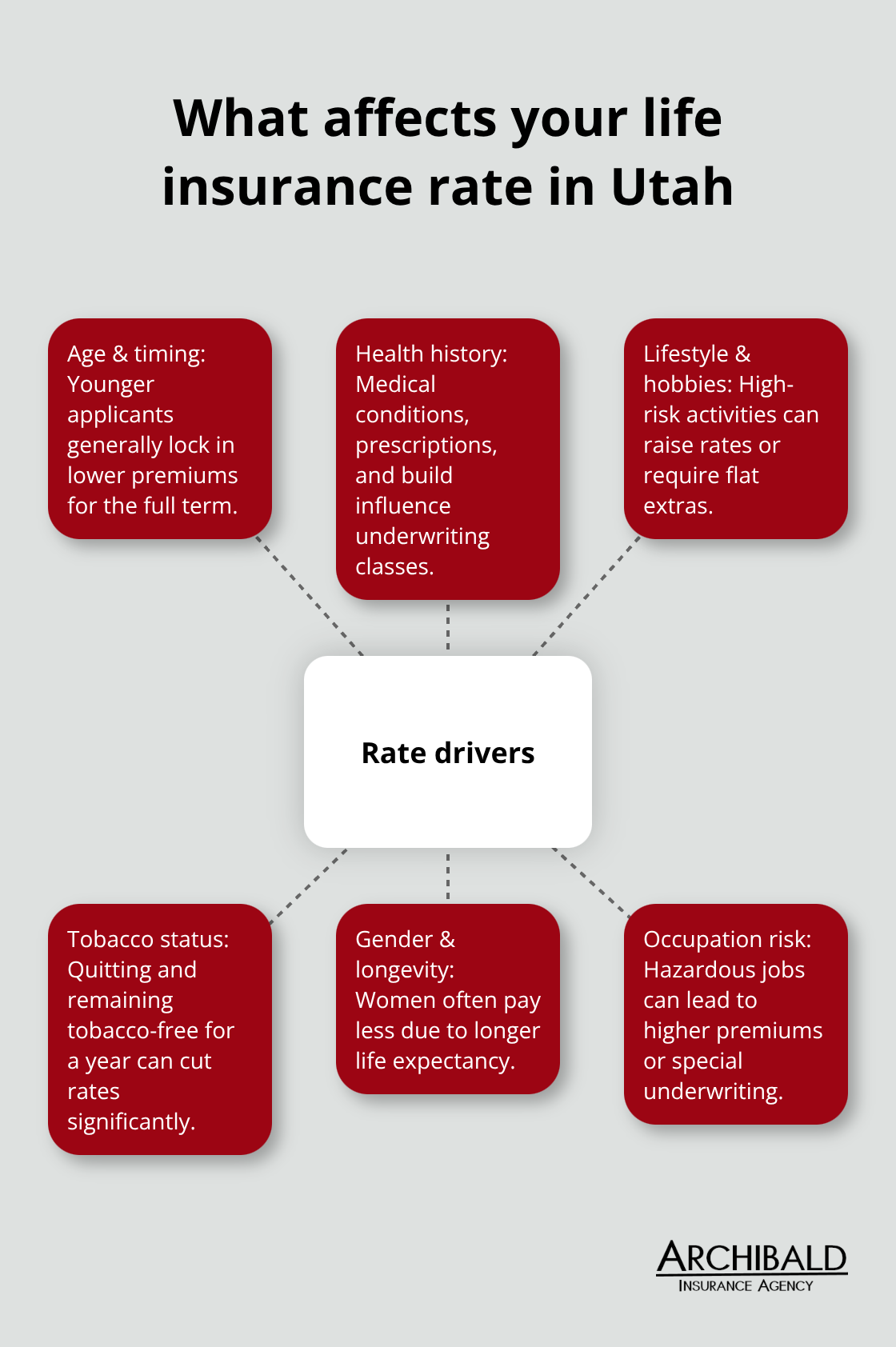

Compare quotes across multiple carriers to find your best rate

Utah families often accept the first quote they receive, missing opportunities to save hundreds annually. Term life premiums vary significantly across carriers based on age, health, and lifestyle factors. Younger applicants lock in lower rates, so purchasing earlier can reduce your costs for years to come. Women typically pay slightly lower rates due to longer life expectancy. High-risk activities (skydiving, mountain climbing, motorcycle racing) can significantly increase life insurance rates. Smokers usually pay more due to higher health risks; quitting can reduce costs over time. Request quotes from multiple carriers to see how your health profile and situation affect pricing. An independent insurance agency can compare options across numerous carriers quickly, saving you time and revealing the best rates available for your specific circumstances. This comparison step often uncovers savings that make a real difference in your family’s budget.

The mistakes you make during this selection process can cost your family thousands of dollars over time, which is why the next section walks you through the most common errors Utah families encounter.

Common Mistakes People Make When Choosing Life Insurance

Underestimating coverage needs leaves families vulnerable

Most Utah families make one critical error when buying life insurance: they purchase coverage based on what they can afford monthly rather than what they actually need. The National Association of Insurance Commissioners found that only about 35% of young singles have life insurance at all, and many who do carry insufficient amounts. A family earning $75,000 annually with a mortgage, two children, and $30,000 in car loans might buy a $250,000 policy because the premium fits their budget, then feel protected. In reality, they need closer to $800,000 to replace ten years of income, cover the mortgage, fund college, and handle final expenses. When the primary earner dies, that $250,000 depletes rapidly-the mortgage alone consumes half, leaving the surviving spouse scrambling to cover childcare, property taxes, and living expenses.

This gap between perceived and actual needs explains why most life insurance claims fall short of what families require.

Ignoring policy reviews and updates creates coverage gaps

Utah families rarely review their policies after purchase, which compounds the problem significantly. Life changes-you pay off the car, your income increases, you have another child, your mortgage balance drops-but your coverage stays frozen in time. A 20-year term policy purchased at age 35 becomes inadequate by age 45 when your income has doubled and you’ve accumulated more assets. You should review your coverage every three to five years, especially after major life events like marriage, children, a promotion, or significant debt changes. Many people also fail to understand their renewal terms. When a 20-year term expires, premiums can jump 50% to 300% depending on your age and health, making coverage unaffordable when you might still need it. Knowing these terms upfront prevents nasty surprises later.

Comparing quotes from only one or two carriers costs you thousands

The third mistake undermines your ability to find the best rate: comparing quotes from only one or two carriers. Someone in excellent health might pay $40 monthly with one company and $65 with another for identical 20-year, $500,000 term coverage-that’s a $300 annual difference, or $6,000 over twenty years. Health history, age, occupation, and lifestyle heavily influence pricing, yet most people accept the first quote they receive. Smokers typically pay two to four times more than non-smokers, but some carriers offer better rates for smokers than others. High-risk activities like skydiving or professional racing increase premiums significantly, though the penalty varies across insurers. An independent insurance agency can request quotes across numerous carriers simultaneously, showing you exactly how different companies price your specific situation. This comparison reveals not just the lowest price but also which carriers offer the best value for your health profile. Shopping with only captive agents (those representing a single company) leaves you paying more than necessary while believing you’ve done your due diligence.

The families who avoid these three mistakes end up with appropriate coverage at competitive rates. Understanding how to select the right policy type and customize it to your situation separates those who truly protect their families from those who simply feel protected.

How to Choose the Right Life Insurance Policy for Your Situation

Assess your family’s actual financial obligations

Selecting the right life insurance policy means working backward from your actual obligations, not forward from what feels affordable. List every financial responsibility your family would face without your income: the mortgage balance, car loans, credit card debt, property taxes for the next ten years, childcare costs until your youngest finishes school, and college funding if applicable. Add $12,000 to $15,000 for final expenses. This total becomes your baseline coverage need. If you have a $300,000 mortgage, $50,000 in car loans, $100,000 in anticipated college costs, and $100,000 to replace five years of income while your spouse transitions back to work, you need roughly $550,000 in coverage minimum.

Utah families typically require between $500,000 and $1 million based on these calculations, though some need significantly more. The mistake most people make is starting with budget instead of need-they ask what premium they can afford monthly, then work backward to find a policy that fits. This approach leaves your family underprotected. Calculate your actual need first, then find coverage that meets it within your budget. If the gap seems too large, a term policy with a 20 or 30-year term keeps premiums manageable while protecting your family through their most vulnerable years.

Match your policy type to your timeline and budget

Matching your policy type to your timeline determines whether you overpay or undershoot coverage. If you have a mortgage and young children, term life covers you through the period when your family depends entirely on your income-typically 20 or 30 years. Once that term expires, your mortgage may be paid off, your children self-sufficient, and your retirement savings substantial. Permanent life insurance makes sense if you’re in your 50s or 60s and want lifetime protection for estate planning or tax purposes, or if you have ongoing financial obligations that won’t end.

Term is usually much cheaper upfront than whole life, which costs more but adds lifelong protection and a cash value feature. Utah life insurance premiums vary based on age, health, and lifestyle. A healthy 35-year-old in Utah pays significantly less for a $500,000 20-year term policy than a 55-year-old with the same coverage. Locking in coverage earlier always costs less over time.

Understand how your health and lifestyle affect your rates

High-risk hobbies like skydiving or professional racing can double or triple your premiums, while quitting smoking can reduce rates by 50% or more once you’ve been tobacco-free for a year. Women typically pay 10% to 15% less than men for identical coverage due to longer life expectancy. Your occupation, medical history, and current health status all influence what insurers charge you.

An independent insurance agency representing multiple carriers can show you how your specific health profile and circumstances affect pricing across different companies, revealing which insurers offer the best rates for your situation rather than relying on a single company’s quote.

Final Thoughts

Securing your family’s financial future through life insurance comes down to three core actions: calculate what you actually need rather than what feels affordable, select a policy type that matches your timeline and budget, and compare quotes across multiple carriers to find the best rate for your situation. Most Utah families who follow these steps end up with appropriate coverage at competitive rates, while those who skip any step leave themselves vulnerable to underinsurance or overpaying. The mistakes outlined earlier-underestimating needs, ignoring policy reviews, and accepting the first quote-cost families thousands of dollars over time, yet they’re entirely preventable with the right approach.

Your next step is straightforward: gather your financial obligations, determine your coverage gap by subtracting existing benefits like Social Security survivor coverage, and request quotes from multiple carriers. Don’t settle for a single quote or limit yourself to one company’s options. An independent insurance agency can handle this comparison quickly, showing you how different insurers price your specific health profile and circumstances.

Life insurance guidance in Utah works best when you have a trusted local partner who understands your family’s needs and can access numerous carriers. We at Archibald Insurance Agency specialize in helping Utah families find personalized life insurance solutions that fit their specific circumstances and budgets. Contact us today to discuss your coverage needs and get quotes that reflect your actual situation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation