Term vs Whole Life Insurance Which is Right for You?

Choosing between term and whole life insurance is one of the biggest decisions you’ll make for your family’s financial security. The right policy depends on your budget, timeline, and long-term goals.

At Archibald Insurance Agency, we help Utah families navigate this choice with clarity. Let’s break down what each option offers so you can make an informed decision.

Understanding Term Life Insurance

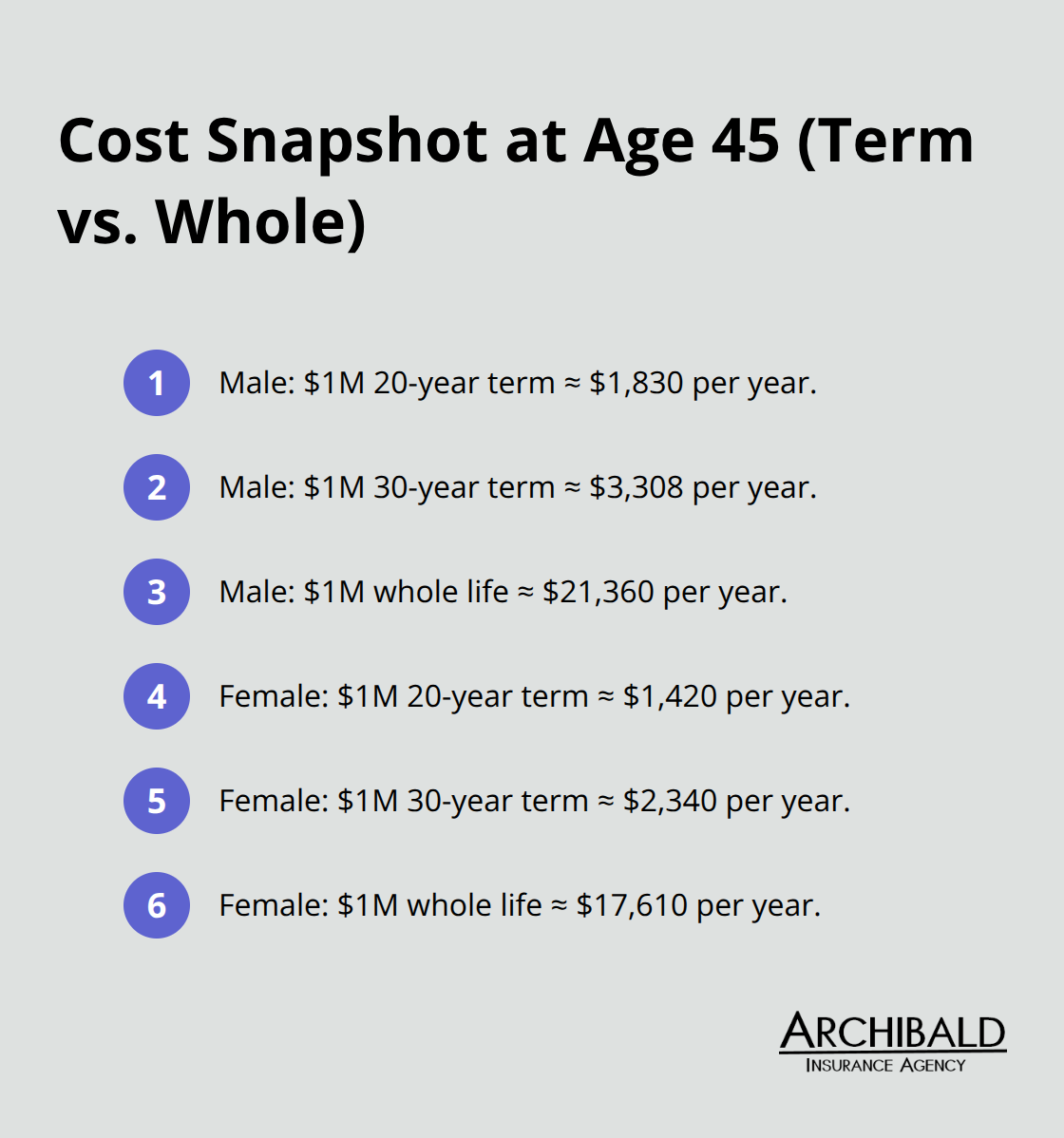

Term life insurance provides straightforward protection: you pay a monthly or annual premium, and if you pass away during the policy term, your beneficiaries receive the death benefit. No cash value exists, no investment component complicates the picture, and no hidden layers obscure what you’re buying. You purchase pure protection for a defined period. In Utah, the average life insurance premium sits around $636 per year, though term policies typically cost significantly less than permanent alternatives. For a 45-year-old man seeking $1 million in coverage, a 20-year term policy costs approximately $1,830 annually, while a 30-year term runs about $3,308 per year. Women in the same age group pay less due to longer life expectancy-20-year terms around $1,420 and 30-year terms near $2,340. These numbers matter because affordability determines whether families actually maintain coverage or let policies lapse.

What Term Life Insurance Covers

Term policies protect your family with a straightforward death benefit. If you pass away during the coverage period, your beneficiaries receive the full amount tax-free. This money helps cover funeral costs, outstanding debts, mortgage payments, and lost income. The policy offers nothing more and nothing less-pure financial protection without the complexity of investment accounts or cash accumulation.

Selecting Your Coverage Window

Term lengths typically range from 10 to 40 years, and the most popular choice among Americans is the 20-year level term, representing about 39% of all term policies purchased according to LIMRA data. A 30-year term captures another 18% of the market, making these two options the dominant choices for families. The 20-year term aligns perfectly with the period when most families face their heaviest financial obligations: young children still at home, mortgages with decades remaining, and earning years ahead.

A mother with two young children might select a 20-year term that expires when her youngest turns 21, providing protection during the critical years when dependents need financial support.

Flexibility Through Conversion

Some term policies offer a return of premium feature, allowing you to recover all paid premiums if you outlive the term, though this option increases your annual cost. Conversion options matter enormously. Many term policies allow you to convert to permanent coverage during a specified conversion window, even if your health changes. This flexibility means you avoid being locked into a decision made years ago when circumstances were different. A single father with a term policy might convert to provide for a new spouse if life circumstances shift unexpectedly.

Affordability That Families Can Maintain

Term life remains the most accessible way to protect your family on a budget. Lower premiums mean families can afford higher death benefits without straining monthly finances. This affordability factor directly impacts whether protection stays in place or lapses when money gets tight. As your situation evolves-children grow older, debts shrink, retirement approaches-you may find that your insurance needs change. Understanding what term life offers sets the stage for comparing it against permanent options that work differently and cost substantially more.

Understanding Whole Life Insurance

Whole life insurance operates on a fundamentally different principle than term: it lasts your entire lifetime, not just a set number of years. You pay a fixed premium each month or year, and that premium never changes regardless of age or health changes down the road. The policy guarantees a death benefit payout whenever you pass away, whether that’s in 5 years or 50 years. For a 45-year-old man seeking $1 million in coverage, whole life costs approximately $21,360 annually according to Wealth Enhancement Group data, compared to $1,830 for a 20-year term. A 45-year-old woman pays around $17,610 yearly for the same whole life coverage versus $1,420 for term. These numbers reveal the real trade-off: permanent protection comes at a steep price.

Lifetime Coverage and Death Benefits

Whole life policies guarantee a death benefit payout whenever you pass away. This permanence distinguishes whole life from term insurance, which expires after a set period. Your beneficiaries receive the full death benefit tax-free, regardless of when you die. The policy never lapses as long as you pay premiums, eliminating the risk that coverage ends before you do.

Cash Value Component

Beyond the death benefit, whole life policies accumulate cash value over time. This cash value grows at a guaranteed rate set by the insurance company, and you can borrow against it tax-free during your lifetime. If you withdraw funds beyond what you’ve paid in premiums, those excess withdrawals get taxed as ordinary income. Some whole life policies pay dividends based on company profits, though dividends aren’t guaranteed. The cash value component creates a secondary benefit beyond pure protection, functioning as a forced savings account that grows regardless of market conditions.

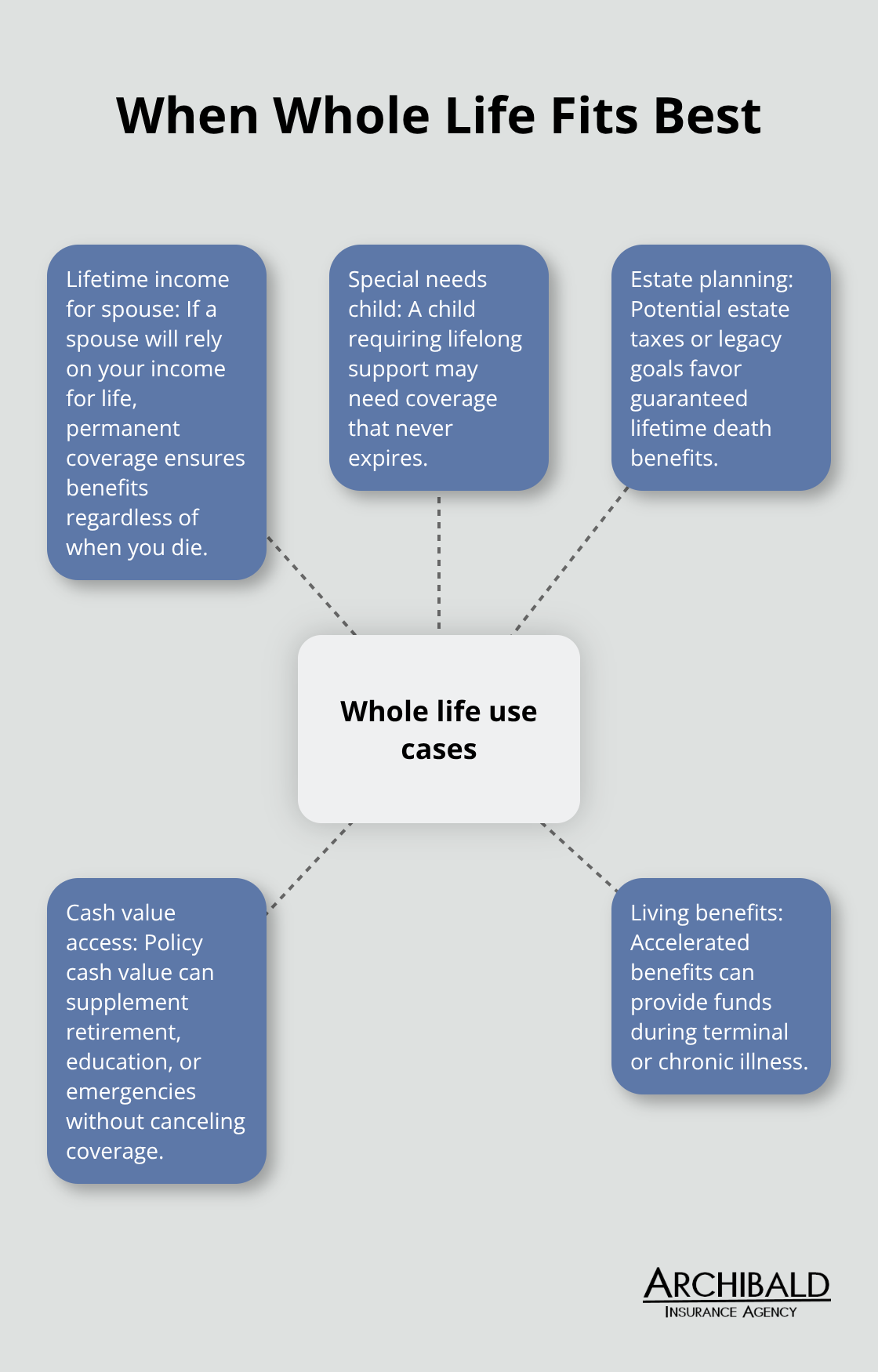

When Whole Life Makes Financial Sense

Whole life works best when you need permanent protection that outlasts your working years and you want predictability in both premiums and benefits. A spouse relying on your income for life, a child with special needs requiring lifelong support, or estate planning objectives like covering potential estate taxes all favor whole life’s permanence. The policy’s cash value provides a genuine advantage here: you can access funds for retirement supplementation, education expenses, or emergency needs without canceling the policy entirely. Accelerated benefits in some whole life policies can also provide funds during your lifetime if you face terminal or chronic illness, turning the policy into a multi-purpose financial tool rather than purely a death benefit vehicle.

The Premium Reality

However, the high premiums mean you’ll likely afford less total coverage than with term insurance. If your primary goal is replacing income for dependents until they become independent, term life delivers far superior value per dollar spent. Whole life shines for long-term obligations and estate planning, not for temporary income replacement needs. The decision hinges on whether your insurance need is permanent or temporary, and whether you value cash value growth enough to justify premiums that can exceed term costs by 1,000 percent.

Understanding these two distinct approaches sets the stage for comparing them directly. The choice between term and whole life depends on your specific situation, timeline, and financial priorities-factors we’ll examine in the next section.

Key Differences and How to Choose

Coverage Duration Reveals Your True Need

Term and whole life diverge sharply in how they work financially, and understanding these differences reveals which policy actually serves your circumstances. The core distinction isn’t philosophical-it’s mathematical. Term life delivers maximum death benefit for your premium dollar in the early years when your family faces the heaviest financial pressure. A 45-year-old man pays $1,830 annually for $1 million in 20-year term coverage; that same $1,830 buys roughly $85,000 in whole life death benefit according to Wealth Enhancement Group data. The gap widens with age and desired coverage amount.

If you’re protecting a family through your peak earning years while children attend school and your mortgage dominates your finances, term life’s affordability allows you to purchase adequate protection without financial strain. Whole life makes sense only when you’ve determined that your insurance need extends beyond a specific timeframe. A surviving spouse who won’t remarry and depends entirely on your income for life, a child with special needs requiring permanent support, or significant estate taxes that will exist whenever you die-these situations favor permanent coverage.

The Conversion Bridge

The conversion feature bridges both worlds effectively. Many term policies allow conversion to permanent coverage during a set window, typically 10 to 15 years. This flexibility means you can lock in today’s health at current rates while maintaining the option to extend protection if circumstances change. If you convert at age 55 after your children finish college, the conversion preserves your insurability even if new health issues emerge, avoiding the higher premiums or denial that comes with applying fresh for permanent coverage.

Cost Compounds Over Decades

Cost compounds dramatically over decades, making this the practical decision point. Maintaining a $1 million whole life policy from age 45 to 85 costs approximately $1.068 million in premiums for a man, versus roughly $36,600 for a 20-year term that expires at 65. If your need actually ends when you retire with paid-off debts and adequate savings, you’ve overpaid substantially for coverage you no longer need. Conversely, if you let a term policy lapse at 65 when you still need protection, you face either paying vastly higher premiums to renew or losing coverage entirely.

Assess Your Timeline Honestly

The solution requires honest assessment of your actual timeline. When will your children become financially independent? When will your mortgage be paid? When will you have accumulated sufficient retirement savings that your family won’t need income replacement? These answers determine whether you need 20, 30, or 40 years of protection. If your analysis shows protection needs persisting beyond a reasonable term length, converting partway through or purchasing whole life for those extended years costs far less than whole life from the start.

The Practical Utah Approach

Utah families balancing mortgages, education costs, and retirement savings typically benefit from term insurance during their working years, then reassessing at 55 or 60 whether permanent coverage makes financial sense for remaining obligations. This practical approach avoids both the trap of underinsurance and the waste of overpaying for permanent protection you’ll never need.

Final Thoughts

Term versus whole life insurance represents a fundamental choice about how you protect your family’s financial future. Term life delivers affordability and straightforward protection during your peak earning years when dependents rely on your income most heavily, while whole life provides permanence and cash value growth for situations where your insurance need extends throughout your lifetime. The correct choice depends entirely on your timeline, financial obligations, and long-term goals-neither option is universally right or wrong.

Start by identifying when your insurance need actually ends. If you’re protecting young children until they finish college, covering a mortgage that will be paid off in 20 years, or replacing income until retirement, term insurance provides the coverage you need at a price your budget can sustain. If you’re concerned about permanent obligations like a spouse’s lifetime income needs, a child with special needs, or estate taxes that will exist whenever you pass away, whole life’s permanence justifies the higher cost. Many Utah families find that a combination approach works best: term insurance for defined obligations paired with whole life for longer-term needs that persist beyond your working years.

Contact Archibald Insurance Agency today to explore term vs whole life insurance options tailored to your specific situation. As an independent agency representing multiple insurance carriers, we compare coverage across different companies to find protection that fits both your needs and your budget. Our team takes time to understand your family’s timeline, financial obligations, and goals before recommending a policy.