Life Insurance for Older People: Complete Guide

Life insurance for older people isn’t a luxury-it’s a practical way to protect those you love most. Whether you’re concerned about final expenses, outstanding debts, or leaving your family with financial security, the right policy makes a real difference.

At Archibald Insurance Agency, we help Utah residents navigate their options and find coverage that fits their needs and budget. This guide walks you through everything you need to know.

Why Life Insurance Matters for Older Adults

Life insurance for older adults solves three specific problems that most people face in their later years. Funeral and burial costs in Utah average between $7,000 and $12,000, according to the National Funeral Directors Association-an expense your family must cover immediately when they’re already grieving. Many older adults carry outstanding debts like mortgages, medical bills, and credit cards that don’t disappear when you pass away, leaving your beneficiaries to face pressure to liquidate assets or lose property to settle what you owe. Life insurance also provides a way to leave money behind for people who depend on you, whether that’s a spouse relying on your income, adult children facing sudden financial strain, or grandchildren you want to support through education.

What Your Family Actually Needs

A 60-year-old in good health who purchases a $500,000 20-year term policy pays roughly $220 per month if male or $157 per month if female, based on current rates. That same coverage protects your family from the financial shock that follows your death. If you’re 70, those same premiums jump significantly-a substantial increase that shows why waiting costs substantially more. The specific amount you need depends on your situation: add up your outstanding debts, estimate final expenses, and consider whether anyone relies on your income. If you own a home with a mortgage, that debt alone justifies substantial coverage. If you have grandchildren or charitable causes you care about, life insurance lets you fund those goals without forcing your family to choose between honoring your wishes and paying their own bills.

Health Status and Your Options

Your age and health determine both whether you qualify and what you’ll pay. Once you reach 70, rates multiply dramatically compared to younger ages. Preexisting conditions like heart disease, diabetes, or cancer don’t automatically disqualify you, but they raise premiums or narrow your options. If you have significant health issues, guaranteed issue policies accept applicants regardless of medical history, though you’ll pay higher premiums and face a two-year waiting period before full benefits apply. Shopping early-ideally before age 70-locks in better rates and gives you more policy choices.

Why Timing Matters More Than You Think

The sooner you act, the less your health changes cost you. A policy purchased at 60 costs far less than the same coverage at 70, even if your health remains stable. Each year you delay, your age alone pushes premiums higher, and any new health condition compounds that increase. This reality makes the decision to shop for coverage urgent rather than something you can postpone indefinitely. Your options expand dramatically when you’re younger and healthier, giving you access to term policies, whole life plans, and simplified underwriting that may not be available later.

Moving Forward With Your Decision

Understanding what life insurance costs and why you need it sets the foundation for choosing the right type of policy. The next section explores the specific types of coverage available to older adults and how each one works differently.

Types of Life Insurance Available for Seniors

Term Life Insurance: Affordable but Temporary

Term life insurance remains the most affordable option for seniors, especially those under 70 who qualify for standard rates. A 60-year-old female in good health pays approximately $168.70 monthly for a $500,000 20-year term policy. At 70, those costs spike dramatically-roughly $447.71 monthly for women-which explains why purchasing before age 70 makes financial sense. Term policies work well if you have specific debts to cover, like a mortgage with 15 years remaining, or if you want to protect a spouse’s income for a defined period.

The major limitation is that term coverage expires. Once your 20-year term ends at age 80, you have no coverage unless you renew at substantially higher rates or convert to a permanent policy, which most people cannot afford. Term life also builds no cash value, so you cannot borrow against it or access funds during your lifetime. This trade-off-lower cost in exchange for temporary coverage-appeals to seniors who prioritize affordability over lifetime protection.

Whole Life and Permanent Coverage Options

Whole life insurance provides permanent coverage that lasts your entire life, regardless of age or health changes after purchase. Premiums stay level and never increase, which appeals to people who want predictability and protection they cannot outlive. The cost difference compared to term life is substantial, but whole life builds cash value over time-money you can borrow against or withdraw if your needs change. Some policies pay dividends that reduce your out-of-pocket costs or increase your death benefit.

The downside is that whole life requires significant monthly commitment. If your budget is tight or you question whether you can sustain these payments for decades, whole life becomes risky because missed payments can lapse your coverage entirely. Universal life offers a middle ground: level premiums like whole life but with minimal cash value, making it cheaper than traditional whole life while still providing lifetime coverage. Survivors life, also called second-to-die insurance, covers two people and pays when the second spouse dies, making it useful for couples concerned about estate taxes or leaving an inheritance. These permanent options suit seniors who want coverage they cannot outlive and have the budget to support higher premiums.

Simplified and Guaranteed Issue Policies

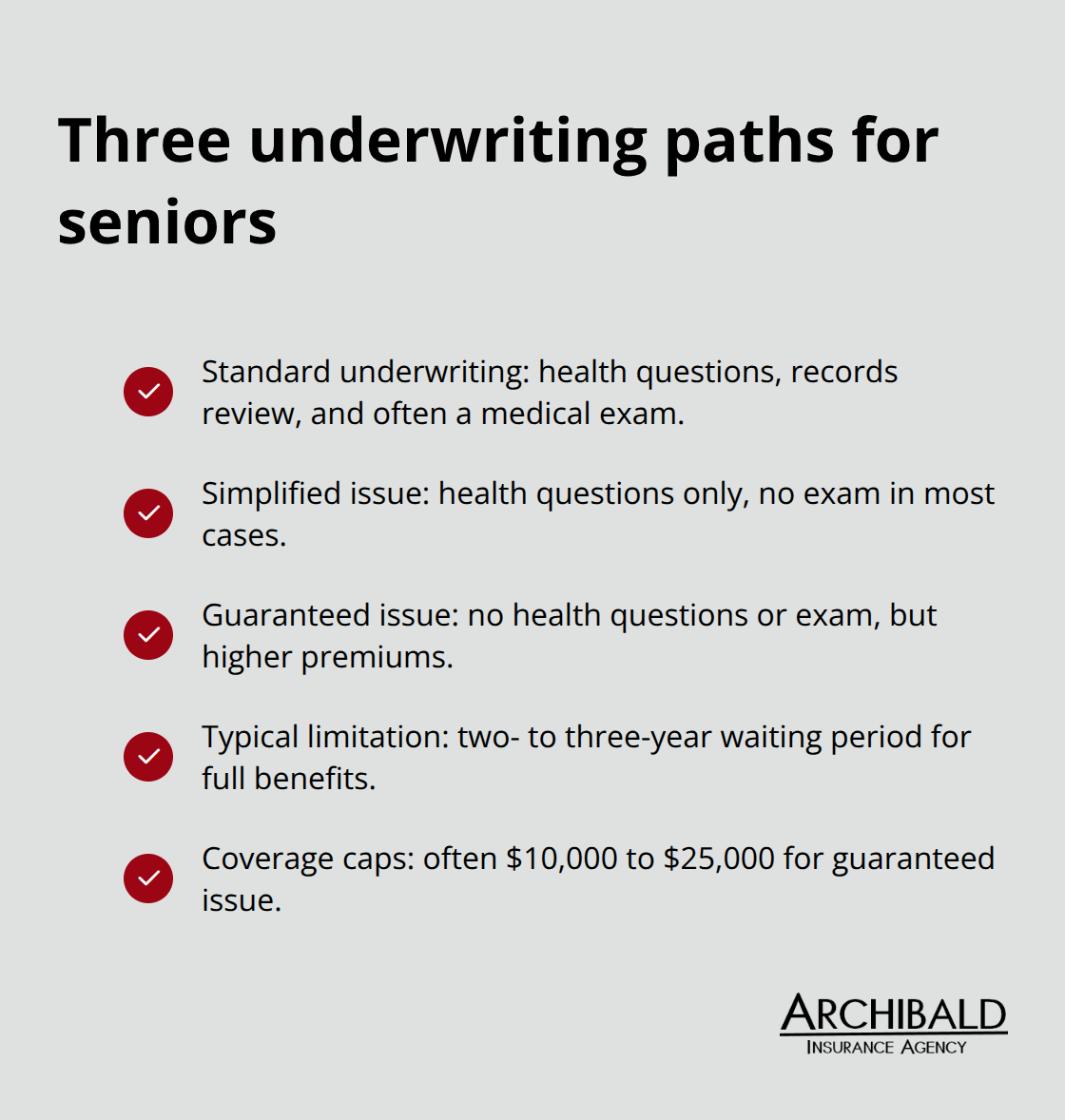

Simplified issue and guaranteed issue policies exist specifically for older adults with health problems or those who have struggled to qualify for standard coverage. Simplified issue requires you to answer health questions but skips the medical exam, making qualification faster and easier than fully underwritten policies. Guaranteed issue asks no health questions and requires no medical exam, accepting applicants regardless of medical history, age, or lifestyle.

The trade-off for this accessibility is steep: guaranteed issue policies carry substantially higher premiums and typically include a two- to three-year waiting period during which the death benefit is limited or unavailable, except in cases of accidental death. A guaranteed issue policy also caps coverage at relatively low amounts, often $10,000 to $25,000, which covers final expenses but not major debts. If you have a serious condition like advanced heart disease, cancer, or kidney failure, guaranteed issue may be your only realistic option, making the higher cost worth accepting. Simplified issue occupies the practical middle ground for many seniors-faster underwriting than standard policies without the extreme cost and limitations of guaranteed issue.

Comparing Carriers and Finding the Best Rates

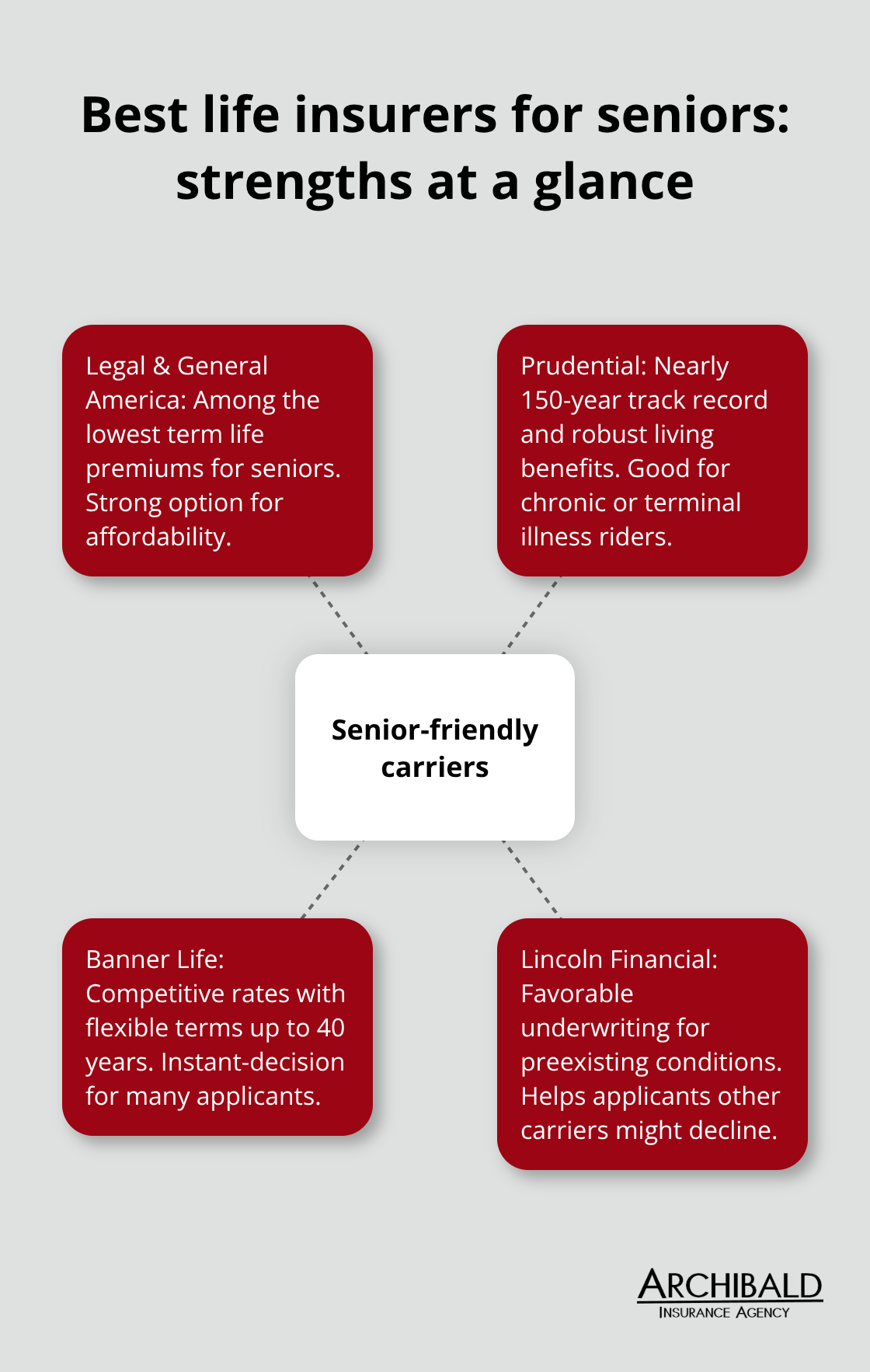

Shopping across carriers matters significantly because rates vary considerably. Legal & General America consistently offers among the lowest term life premiums for seniors, while Prudential stands out for seniors due to its nearly 150-year track record and living benefits like accelerated death benefit for chronic or terminal illness. Banner Life provides competitive rates with flexible terms up to 40 years and instant-decision capabilities for qualifying applicants. Lincoln Financial excels for applicants with preexisting conditions, offering favorable underwriting where other carriers impose restrictions or deny coverage outright.

The right policy depends on your specific situation-your age, health status, budget, and whether you need temporary or permanent protection. Understanding these options positions you to make an informed choice that aligns with your family’s financial security. The next section walks you through the process of assessing your actual coverage needs and comparing quotes to find the policy that works best for your circumstances.

How to Choose the Right Life Insurance as You Age

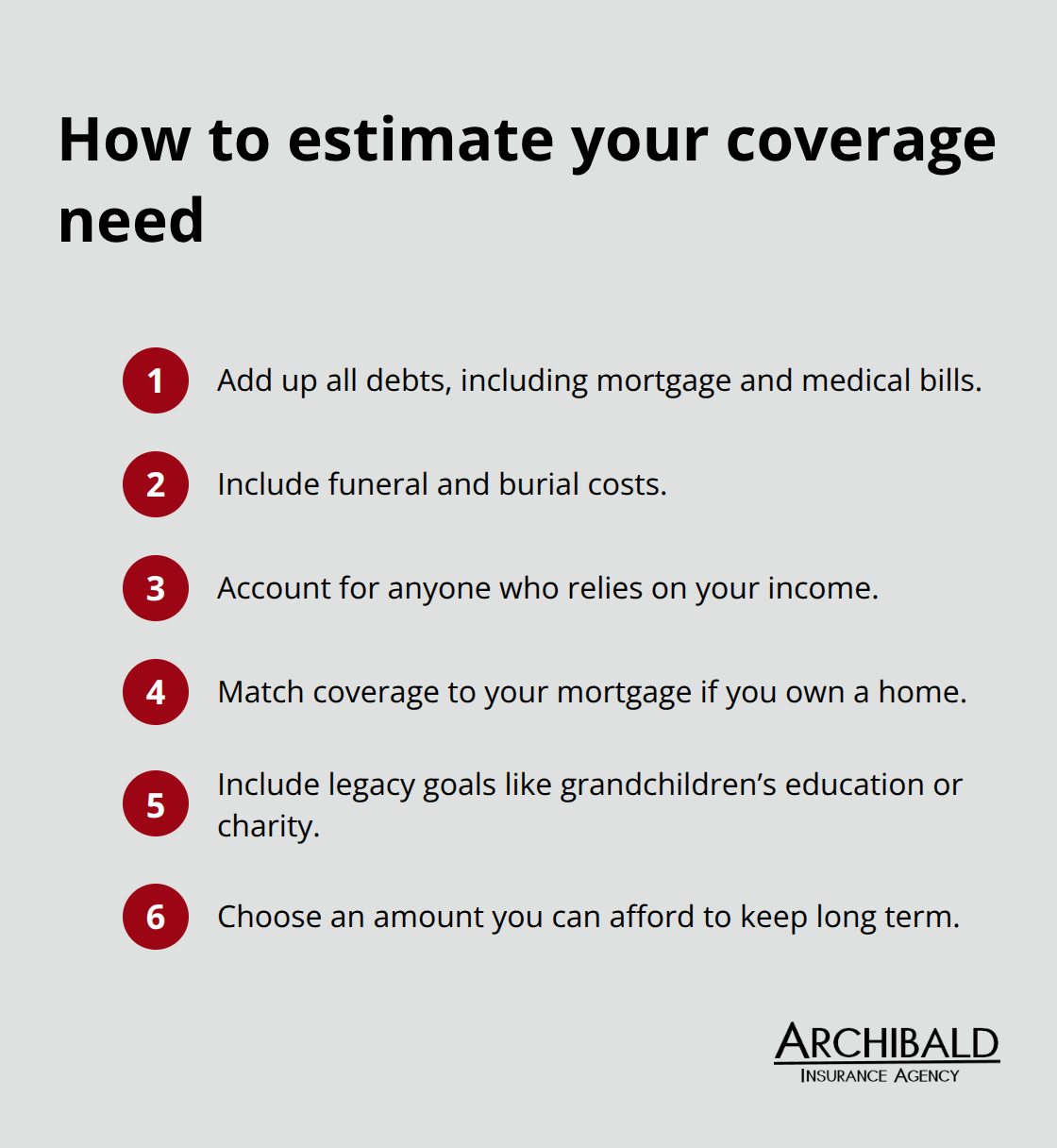

Assessing Your Coverage Needs and Budget

Calculating exactly how much coverage you need forces you to look at your actual finances rather than guessing. Start with your debts: write down your mortgage balance, car loans, credit cards, medical bills, and any other obligations that won’t disappear when you die. Add funeral costs, then consider whether your spouse or dependents lose income when you’re gone. A widow relying on your Social Security benefits faces a gap if those payments don’t cover her living expenses, and life insurance fills that gap for a defined period.

Some people also want to leave money for grandchildren’s education or charitable causes, which increases the coverage amount. Once you total these numbers, you have your target coverage need. Your budget then determines the policy type: if you can afford $200 monthly, term life provides substantial coverage, but if your budget is $50 monthly, you face limits with smaller whole life or guaranteed issue policies. Honesty about what you can sustain matters enormously because a lapsed policy protects nobody.

If you’re uncertain about your numbers, a life insurance calculator helps you model different scenarios and see how your coverage needs change over time based on inflation and investment returns.

Understanding Health Underwriting and Medical Exams

Health underwriting happens differently across policy types, and understanding this process prevents surprises during application. Standard underwriting for term and whole life policies involves health questions, medical records review, and often a phone interview where the insurer asks detailed questions about your medical history, medications, and lifestyle. Some carriers require a medical exam with blood work and urine tests for larger coverage amounts (typically $500,000 or more).

If you have preexisting conditions, the insurer may request records from your doctor, which takes time but gives you the most accurate rate. Simplified issue policies skip the medical exam but require honest answers to health questions, and lying disqualifies your claim later if the insurer discovers the deception. Guaranteed issue eliminates health questions entirely, accepting anyone regardless of condition, but the two-year waiting period means your beneficiaries receive only accidental death benefits if you die from a medical cause during that window.

Comparing Quotes from Multiple Carriers

Shopping across multiple carriers is essential because underwriting standards vary dramatically. Lincoln Financial accepts applicants with heart disease or diabetes that other carriers deny, while Legal & General America offers instant decisions for many applicants without waiting for medical records. Getting quotes from at least three carriers takes roughly an hour online and reveals rate differences of $50 to $200 monthly for identical coverage-a gap worth pursuing.

Different carriers also excel in different areas. Prudential stands out for seniors due to its nearly 150-year track record and living benefits like accelerated death benefit for chronic or terminal illness. Banner Life provides competitive rates with flexible terms up to 40 years and instant-decision capabilities for qualifying applicants. Legal & General America consistently offers among the lowest term life premiums for seniors seeking affordability.

The right policy depends on your specific situation-your age, health status, budget, and whether you need temporary or permanent protection. Understanding these options positions you to make an informed choice that aligns with your family’s financial security.

Final Thoughts

Life insurance for older people solves real problems that affect your family’s financial security after you’re gone. The coverage you choose depends on three factors: how much you need to protect, what you can afford monthly, and whether you want temporary or permanent protection. Term life offers affordability if you have specific debts or income gaps to cover for a defined period, while whole life and universal life provide permanent coverage that lasts your entire life, building cash value or offering level premiums you never outgrow.

Your next step is calculating your actual coverage need by adding your debts, final expenses, and any income gaps your family would face. Once you know that number, get quotes from at least three carriers because rates vary significantly based on age, health, and underwriting standards-shopping takes roughly an hour and often reveals monthly savings of $50 to $200 for identical coverage. If you have preexisting conditions, carriers like Lincoln Financial offer favorable underwriting where others impose restrictions.

We at Archibald Insurance Agency understand that choosing life insurance for older people requires more than generic advice. As an independent agency in Salt Lake City, we represent numerous carriers, which means we match you with the policy and insurer that fit your specific situation rather than pushing one product. Contact Archibald Insurance Agency today to discuss your coverage needs and get personalized quotes.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation