How to Choose Universal and Variable Life Insurance

Universal and variable life insurance offer very different approaches to permanent coverage. One emphasizes flexibility and control over your premiums, while the other ties your cash value to market performance.

At Archibald Insurance Agency, we help Utah residents understand which option matches their financial situation and risk tolerance. The right choice depends on your income stability, investment comfort, and long-term goals.

Understanding Universal Life Insurance

Universal life insurance strips away the rigid structure of traditional whole life policies and replaces it with genuine flexibility. You control how much you pay each month and when you pay it, within policy guidelines. The death benefit stays in place as long as you fund the policy adequately, but the amount can be adjusted upward or downward depending on your changing circumstances. This flexibility appeals to people whose income fluctuates or whose life situation shifts unexpectedly. The cash value grows at a guaranteed minimum interest rate set by the insurer, typically at least 2% annually. Unlike variable life insurance, which ties cash value to market performance, universal life offers predictable growth. You can borrow against the accumulated cash value tax-free up to your cost basis, or make partial withdrawals to cover expenses. Loans accrue interest and reduce your death benefit if not repaid, so they require careful planning. The National Association of Insurance Commissioners notes that premiums for universal life have become increasingly competitive over the past decade, making this option more accessible for Utah families seeking permanent coverage without the commitment of fixed payments.

How Cash Value Accumulates Over Time

The cash value in a universal life policy grows through credited interest rates, but internal costs chip away at that growth. Policy charges for insurance, administrative fees, and cost-of-insurance deductions reduce your cash value each month. If you underfund the policy-paying less than what the insurer’s calculations suggest you need-the cash value shrinks faster than it grows, potentially causing the policy to lapse. A well-funded policy with consistent premiums will see cash value compound steadily over 10, 20, or 30 years.

Some policies allow you to lock in higher credited rates during favorable interest-rate environments, though this varies by carrier. The key is understanding your year-by-year illustration before you commit, so you know exactly how quickly cash value builds and whether the guarantees meet your expectations.

Premium Flexibility and Death Benefit Control

Universal life lets you skip a payment if your cash value is sufficient to cover that month’s charges, a feature that term and whole life policies do not offer. You can also increase or decrease your death benefit, subject to underwriting approval for increases. This adaptability makes universal life attractive for people managing variable income, such as self-employed professionals or business owners. However, flexibility can become a liability if you treat it casually. Missing payments when cash value is low can cause unexpected policy lapse. We recommend reviewing your illustration annually and adjusting premiums when income changes, rather than relying on the option to skip payments. This disciplined approach protects your coverage and ensures your policy remains active when you need it most.

Why Variable Life Insurance Demands Your Attention

Universal life’s predictable growth appeals to many, but it may not satisfy those seeking higher returns or greater control over investments. Variable life insurance introduces market-linked growth potential that universal life cannot match. The next section explores how variable life works and whether its investment flexibility aligns with your financial goals and risk tolerance.

Variable Life Insurance and Market-Linked Growth

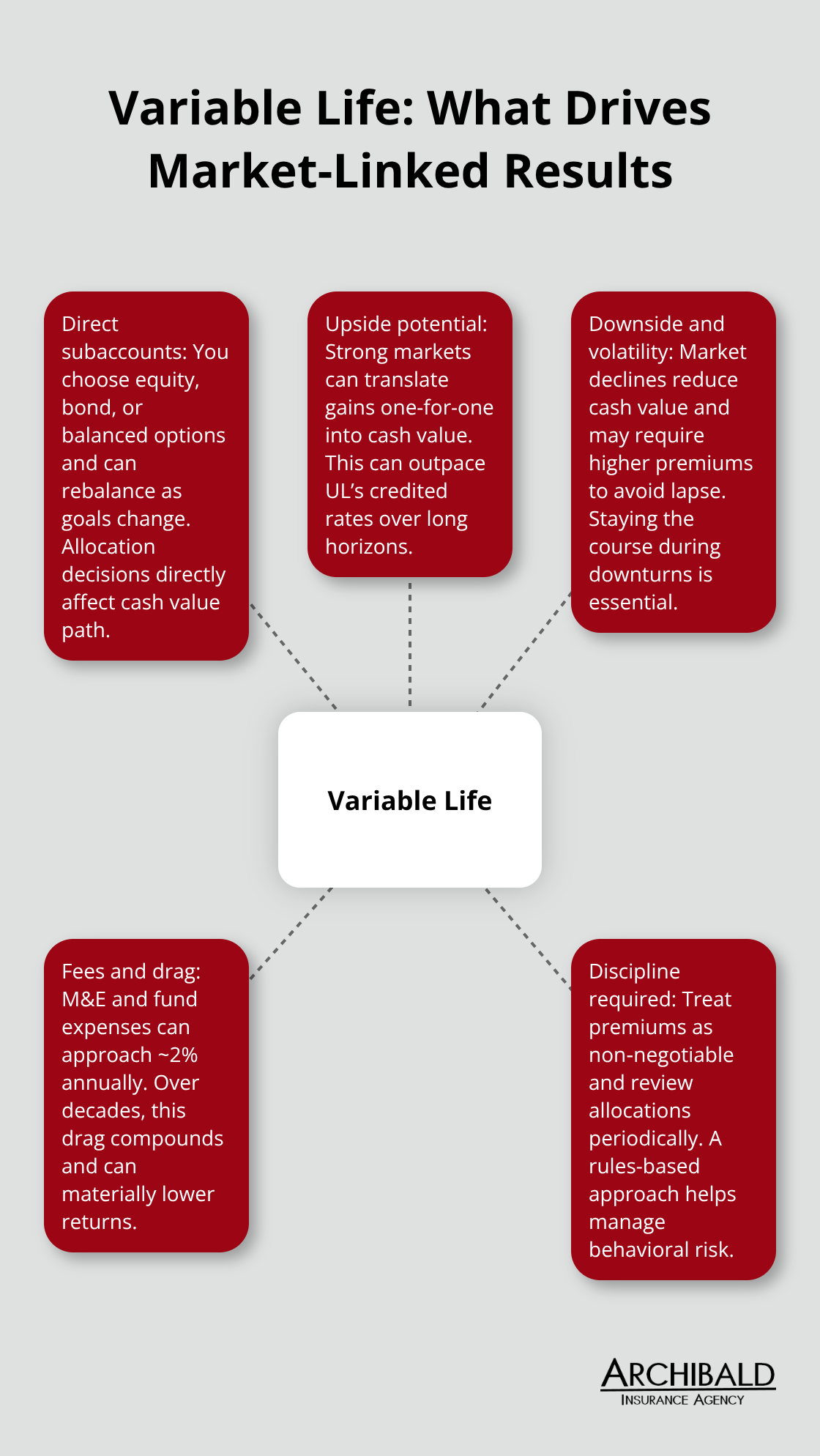

Variable life insurance invests your cash value directly into subaccounts you select, much like choosing mutual funds within your policy. The S&P 500 stock fund, international equity funds, bond portfolios, and balanced options are typical choices available through most carriers. Your cash value rises and falls with the performance of those investments, which means upside potential far exceeds what universal life delivers in strong market years. A 20% gain in your chosen stock subaccount translates directly to a 20% gain in your cash value that year, whereas universal life’s credited rate typically caps around 2–3% annually.

Direct Market Exposure and Growth Potential

This direct market exposure appeals to investors comfortable with volatility and seeking growth that outpaces inflation over decades. However, the tradeoff is real: when markets decline, your cash value declines too. The 2022 stock market downturn reduced many VUL policies’ cash values by 15–25%, forcing some policyholders to increase premiums to prevent lapse. Variable life requires you to monitor your subaccount allocation, rebalance periodically, and understand that poor market timing or concentration in declining sectors can slow your progress significantly.

The Cost Structure of Variable Life

Internal costs matter more in variable life than universal life because fees compound on a larger, market-exposed base. Typical VUL policies charge 0.75–1.5% annually in mortality and expense fees, plus underlying fund expenses ranging from 0.25–0.75% per subaccount, meaning your total drag can reach 2% or higher each year. That 2% annual cost compounds, reducing your 20-year return substantially compared to a policy with lower fees.

Who Controls Investment Risk

The core difference between variable and universal life comes down to who controls investment direction and who bears market risk. In universal life, the insurance company credits a guaranteed minimum rate and absorbs market risk through its own investment portfolio. In variable life, you direct the investments and bear the market risk directly through your subaccount choices. This distinction reshapes how you approach premium funding and cash value projections.

A universal life illustration shows stable, predictable numbers year after year. A variable life illustration shows multiple scenarios based on historical market performance. Those scenarios reveal that VUL cash value could grow to $500,000 in a favorable market but stall at $200,000 in a poor one over the same 20-year period. This uncertainty demands disciplined premium contributions regardless of market performance; skipping payments when markets are down can trigger policy lapse precisely when you need coverage most.

Matching Variable Life to Your Financial Profile

Variable life suits people with 20+ year time horizons, stable income to support consistent premiums, and genuine comfort with market volatility. If you check your investment portfolio daily and lose sleep during market corrections, variable life’s emotional demands may outweigh its growth potential. Conversely, if you view market downturns as buying opportunities and maintain a long-term perspective, variable life’s uncapped upside can build substantial cash value for retirement income, education funding, or legacy planning. The decision hinges not on which product is objectively better, but on whether your financial discipline and risk tolerance align with market-linked growth.

Understanding your own investment temperament matters as much as understanding the mechanics of either product. The next section compares universal and variable life side by side, helping you weigh cost, flexibility, and risk in concrete terms.

Comparing Universal and Variable Life Insurance

Cost Structures That Shape Long-Term Outcomes

Universal life and variable life operate on fundamentally different cost structures, and understanding those differences prevents costly mistakes down the road. Universal life policies typically charge 0.5–1% annually in mortality and expense fees, with cost-of-insurance deductions that increase as you age. Variable life adds a second layer: underlying mutual fund expenses ranging from 0.25–0.75% per subaccount, meaning your total annual drag often reaches 1.5–2% or higher. Over 20 years, that extra 1% compounds significantly. A policy with $300,000 in cash value losing 2% annually to fees versus 1% annually leaves you roughly $60,000 behind, assuming identical investment performance.

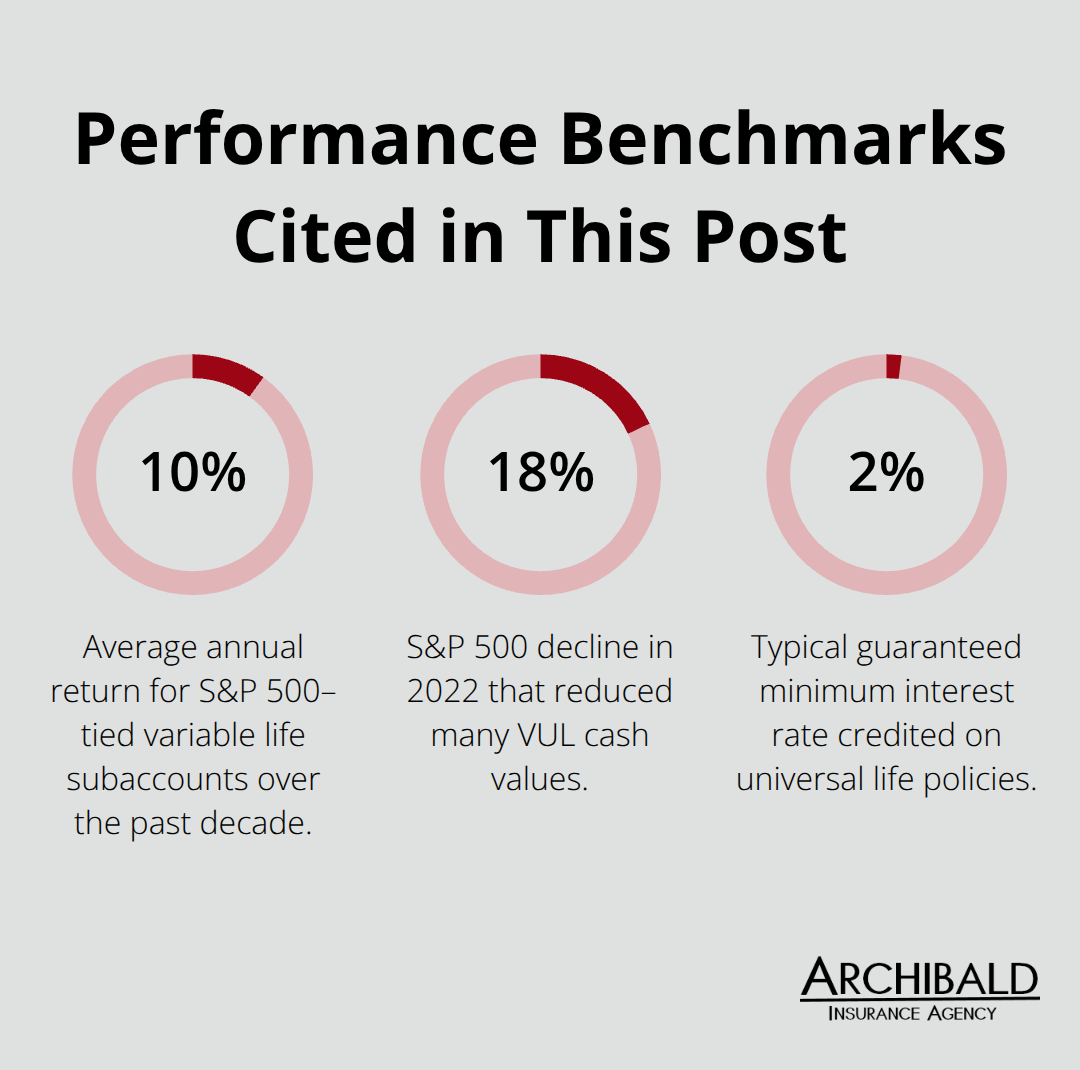

However, this comparison assumes variable life outperforms universal life’s credited rates, which is not guaranteed. The National Association of Insurance Commissioners found that credited rates on universal life policies averaged 2–3% annually over the past decade, while variable life subaccounts tied to the S&P 500 returned 10% annually on average. The math favors variable life in strong markets, but that average masks volatility. In 2022, the S&P 500 fell 18%, meaning variable life policyholders saw their cash value decline while universal life continued crediting positive returns.

Premium Flexibility and Discipline Requirements

Premium flexibility differs sharply between the two. Universal life lets you adjust your payment amount month to month and even skip payments if cash value covers charges, a feature that appeals to self-employed workers or anyone with irregular income. Variable life demands more discipline because market downturns erode cash value precisely when you might be tempted to reduce premiums. Skipping or reducing premiums during a market correction forces the policy to consume cash value faster, increasing lapse risk when markets recover slowly.

Treat variable life premiums as non-negotiable, regardless of market conditions. Universal life offers greater flexibility, but that flexibility becomes dangerous without self-control. Many policyholders skip payments during good income years, then face lapse when income drops and cash value has been depleted.

Investment Control and Behavioral Risk

Variable life gives you direct control over investment allocation and rebalancing, allowing you to shift between stock, bond, and balanced subaccounts as your goals change. You can concentrate in growth-focused equity funds during your 40s and shift toward bonds as you approach retirement, all within the same policy. Universal life removes this granular control; the insurer manages your cash value through its own investment portfolio and credits a rate based on broader market conditions and the company’s investment performance.

This difference matters more than many realize. A variable life policyholder who rebalanced aggressively in early 2020 before markets crashed, then reinvested in stocks as they recovered, captured significantly more upside than someone who remained static. Conversely, a variable life policyholder who panicked and moved everything to money market funds during the 2008 financial crisis locked in losses and missed the subsequent 400% S&P 500 gain. Universal life eliminates this behavioral risk because you cannot make poor timing decisions with money you do not directly control.

Matching Cost and Control to Your Financial Profile

Your risk tolerance and financial goals should drive the decision, not abstract notions of which product is objectively superior. Universal life suits people who value simplicity, guaranteed minimums, and protection against their own investment mistakes. Variable life suits people with genuine long-term discipline, investment experience, and willingness to monitor their subaccount performance quarterly or annually (or who work with a financial professional to handle this task). Neither approach is wrong; both can build substantial cash value over time if properly funded and aligned with your actual behavior, not your aspirational self.

Final Thoughts

Universal and variable life insurance represent two distinct paths to permanent coverage, each with clear tradeoffs that align with different financial situations and temperaments. Universal life prioritizes stability and simplicity, offering guaranteed minimum interest rates and protection from market volatility at the cost of lower growth potential. Variable life prioritizes growth and control, allowing you to direct investments into subaccounts and capture market upside, but demanding discipline and comfort with fluctuating cash values.

The choice between universal and variable life insurance hinges on three concrete factors: your income stability, your investment temperament, and your time horizon. If your earnings fluctuate significantly, universal life’s premium flexibility may prevent lapse during lean years, while steady income makes variable life’s consistent premium requirement manageable. Variable life suits people who understand market cycles and maintain conviction during downturns; universal life suits people who prefer to avoid investment decisions entirely and accept lower returns for predictability.

We at Archibald Insurance Agency help Utah residents navigate this decision by reviewing your specific circumstances, income stability, and risk tolerance. Contact us for a personalized quote and illustration comparing both options side by side, and our independent agency represents multiple carriers to ensure you see options tailored to your actual needs.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation