Family Life Insurance Utah: Planning With a Reliable Guide

Life insurance is one of the most important financial decisions you’ll make as a parent in Utah. Without it, your family faces serious financial hardship if something happens to you.

We at Archibald Insurance Agency help Utah families understand family life insurance options and find coverage that actually fits their situation. The right policy protects your loved ones from mortgage debt, replaces your income, and covers everyday expenses they’d struggle to pay on their own.

Why Family Life Insurance Matters in Utah

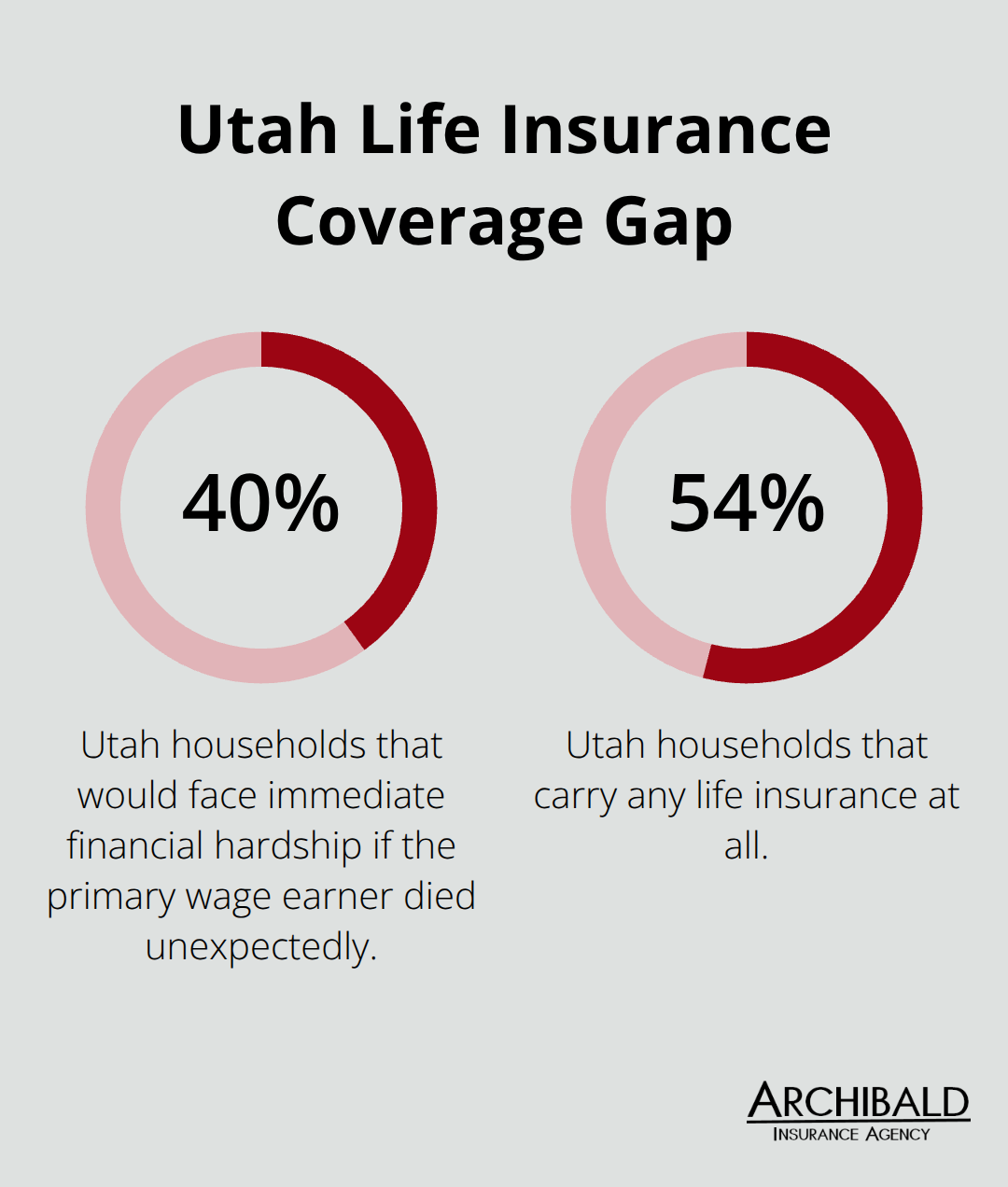

The numbers tell a stark story about Utah families. According to data from the National Association of Insurance Commissioners, 40% of Utah households would face immediate financial hardship if the primary wage earner died unexpectedly. Yet only about 54% of Utah households carry any life insurance at all, leaving a massive protection gap.

In Bountiful alone, median home prices have surpassed $500,000, which means most families carry substantial mortgage debt that would devastate their household if left unpaid. Life insurance isn’t abstract protection-it’s the difference between your family keeping their home and losing it, between your kids staying in their school or moving away, between your spouse managing alone or drowning in debt.

Your mortgage represents your family’s largest financial obligation

A $500,000 home in Utah means a mortgage payment that consumes thousands of dollars annually. If you die without life insurance, that obligation doesn’t disappear. Your family faces a choice: sell the home in a difficult situation, refinance with a single income that may not qualify, or exhaust savings trying to keep up with payments. Life insurance with a death benefit large enough to pay off or significantly reduce your mortgage removes this crushing pressure. The same applies to car loans, credit cards, and personal loans-these debts don’t vanish, and your family shouldn’t inherit them alongside their grief.

Your paycheck funds everything your family depends on

Your income covers rent or mortgage, groceries, utilities, school expenses, childcare, and healthcare. A healthy 30-year-old in Utah can secure $500,000 in term life coverage for roughly $25 to $30 per month, making this protection far more affordable than most people assume.

Employer coverage leaves dangerous gaps

Many families rely solely on employer-provided coverage, which typically caps out at 1 to 2 times annual salary and vanishes the moment you change jobs. That gap leaves your family exposed during the exact years when they depend most heavily on your income. Supplementing employer coverage with a personal policy ensures your family stays protected, even if you switch positions or start your own business.

Understanding these three realities-mortgage obligations, income replacement needs, and employer coverage limits-shapes how much protection your family actually needs. The next step involves evaluating which type of life insurance policy delivers that protection most effectively for your situation.

Types of Life Insurance and Which Fits Your Family

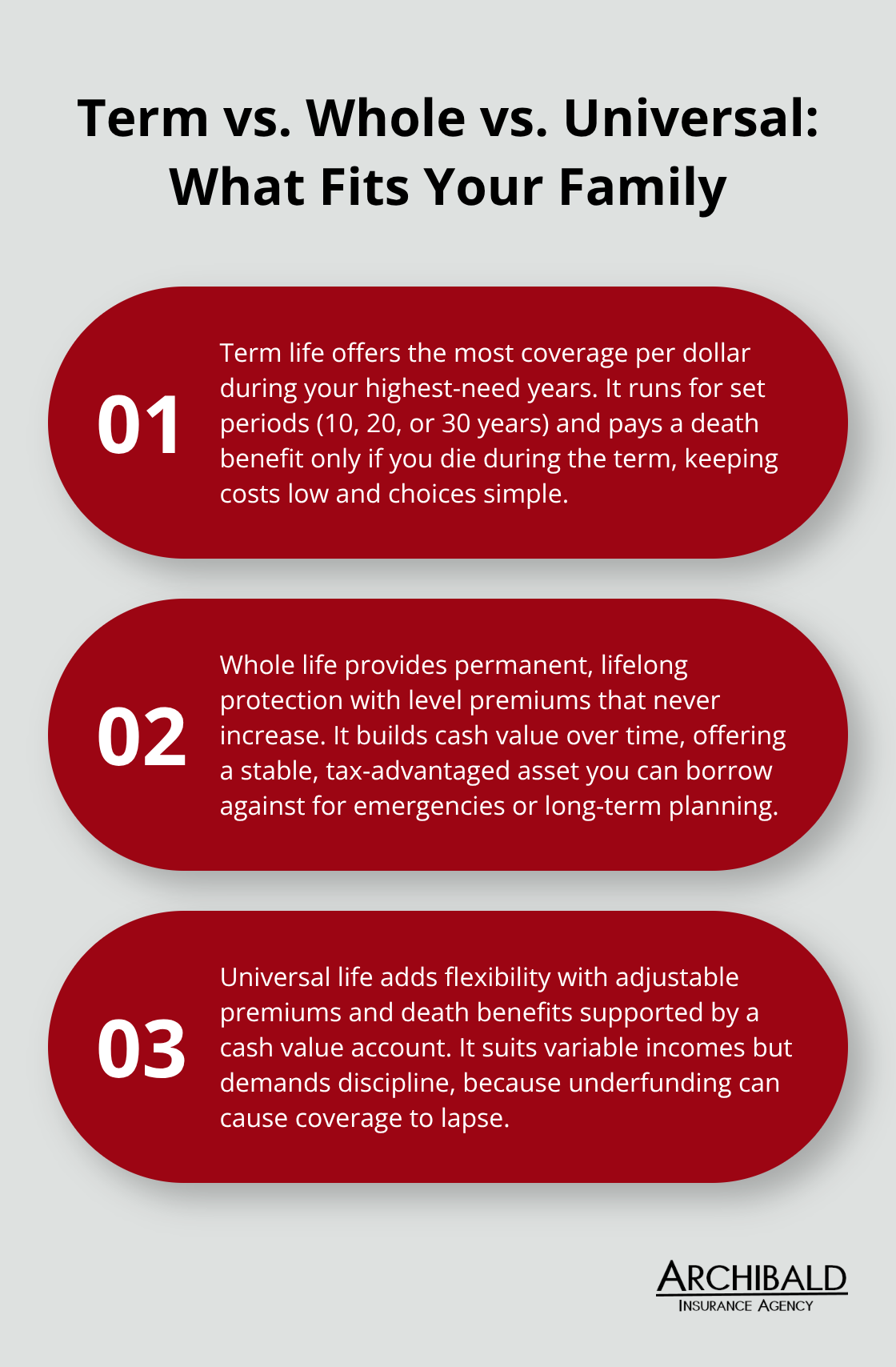

Term life insurance dominates the market for Utah families with good reason: it delivers maximum protection per premium dollar during your highest-risk years. A 30-year-old can purchase substantial coverage for roughly $20 to $25 monthly, making it the most affordable option when you need protection. Term policies run for fixed periods, typically 10, 20, or 30 years, and pay a death benefit only if you die during that term. This simplicity appeals to young families protecting dependents through college years and peak mortgage debt. The tradeoff is straightforward: once your term expires, the policy ends.

You can renew at a higher premium reflecting your age, or convert to permanent coverage, but neither option preserves your original low rate.

Term Life Insurance for Temporary Coverage

Financial advisors widely recommend term coverage for families in their 20s through 40s because the math works. You protect your family during decades when your income replacement needs are highest and your mortgage balance is largest. Term policies offer the lowest entry cost, allowing you to secure substantial death benefits without straining your monthly budget. The fixed term structure means you know exactly when coverage ends, making it easy to plan ahead and evaluate whether you need to renew or adjust your strategy.

Whole Life Insurance for Permanent Protection

Whole life insurance takes the opposite approach by providing lifetime coverage with level premiums that never increase. You pay substantially more upfront-typically three to five times the term rate for equivalent death benefits-but your policy remains active as long as premiums are paid. Whole life builds cash value over time, meaning a portion of your premium accumulates in a tax-deferred account you can borrow against during emergencies or retirement. Academic research found whole life insurance outperformed bonds as the safe-money allocation, appealing to families wanting permanent protection plus a savings component.

Universal Life Insurance for Flexibility

Universal life insurance splits the difference by offering adjustable premiums and flexible death benefits tied to an underlying cash value account. You can pay more in some years and less in others, provided the account maintains sufficient value to cover mortality costs. This flexibility attracts families with unpredictable income, but it requires discipline. If you underfund the account, your coverage can lapse without warning, leaving your family unprotected.

Finding Your Optimal Strategy

Most Utah families benefit most from term coverage during their peak earning and family-raising years, then evaluate permanent options in their 50s when estate planning and tax efficiency become relevant. A mixed strategy combining affordable 20-year term protection with a smaller permanent policy for final expenses and legacy goals often outperforms choosing one type exclusively. The decision hinges on your specific timeline, budget, and whether you value simplicity or maximum flexibility in your coverage structure. Once you understand which policy type aligns with your family’s needs, the next critical step involves calculating exactly how much coverage protects your household from financial collapse.

How to Choose the Right Coverage Amount for Your Situation

Determining your coverage amount requires honest math, not guesswork. Financial advisors recommend securing 10 to 12 times your annual household income in death benefits, which for a Utah family earning $75,000 annually means $750,000 to $900,000 in coverage. This range accounts for income replacement during your family’s working years while acknowledging that your needs decline as children graduate, mortgages shrink, and retirement savings grow.

Calculate Your Family’s Expenses and Goals

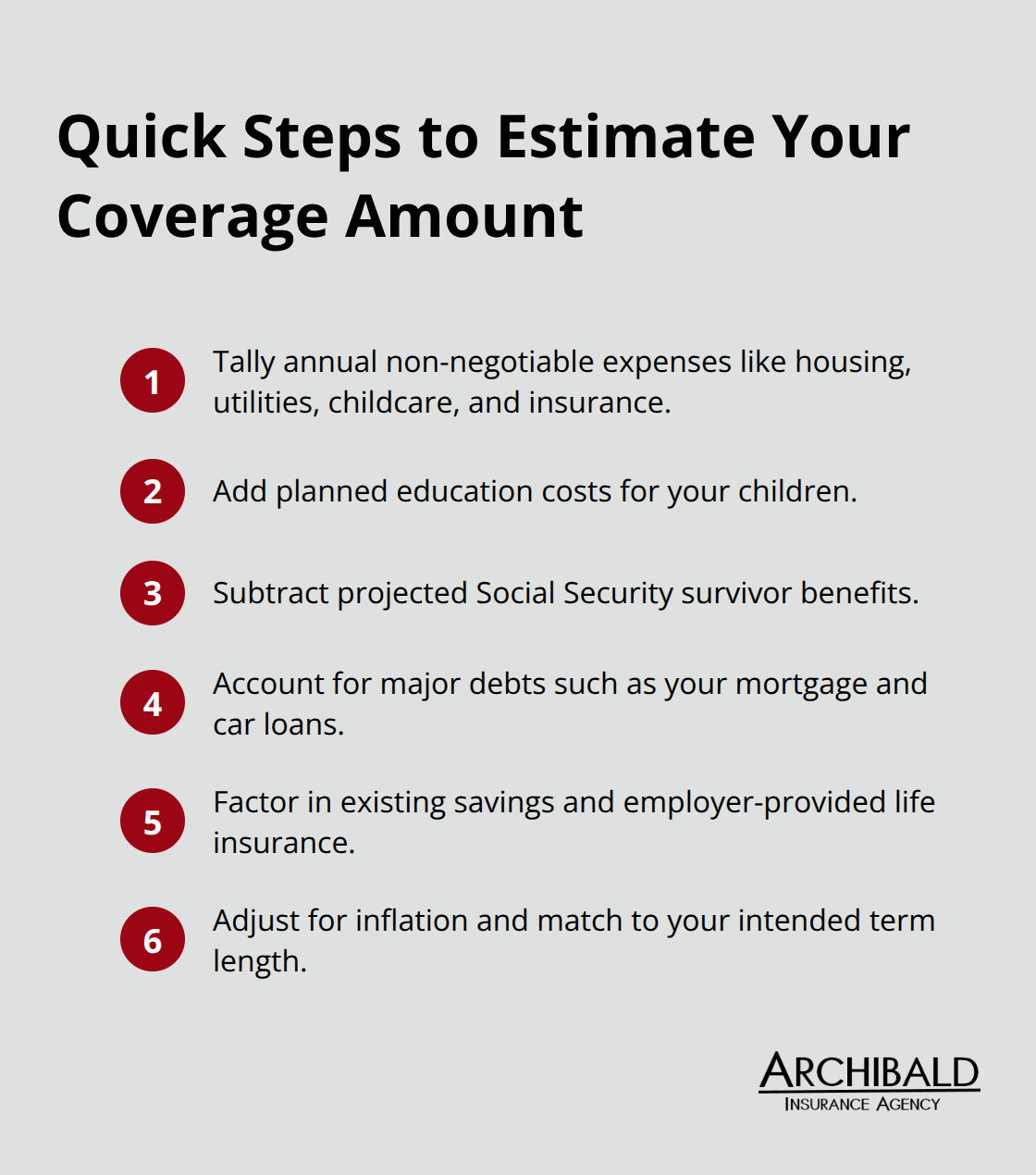

Start with what your family spends annually on non-negotiable expenses: mortgage or rent, property taxes, utilities, groceries, insurance premiums, childcare, and transportation. Add education costs if you want to fund college for your children. Then subtract what your family would receive from Social Security survivor benefits, which provide meaningful income replacement.

A $500,000 home mortgage, $40,000 annual living expenses, and $100,000 in existing savings might suggest you need $450,000 to $600,000 in coverage to bridge the gap. A family with a $200,000 mortgage and higher savings could secure adequate protection with $300,000 to $400,000. The critical mistake most Utah families make is either underestimating expenses or failing to account for inflation, which erodes purchasing power over time and means your coverage needs increase if you’re planning for a 20 or 30-year term.

Factor in Existing Savings and Other Insurance

Your existing assets and income sources substantially affect how much new coverage you actually need. If your spouse has stable employment earning $50,000 annually, your death benefit doesn’t need to replace your entire $75,000 income since household earnings continue. However, if your spouse stays home managing childcare or running a household, you need substantially more protection because that unpaid labor suddenly requires outside services.

Many Utah families overlook this reality and underinsure non-working spouses, creating dangerous gaps. Factor in any employer-provided life insurance you already carry and savings your spouse could access during the transition period. These assets reduce the death benefit you must purchase separately, lowering your monthly premium costs while still protecting your family’s standard of living.

Work With an Agent to Find Your Ideal Amount

An independent agent can map your specific situation, identify where employer coverage falls short, and calculate a death benefit that actually protects your family’s standard of living rather than leaving them scrambling. An independent agent compares term lengths and permanent options side-by-side to show you exactly how different coverage amounts impact monthly premiums, making it clear whether $300,000 or $600,000 fits your budget while delivering genuine protection.

Final Thoughts

You now understand the three core policy types available for family life insurance in Utah and how to calculate coverage that actually protects your household. Term life delivers maximum affordability during your peak earning years, while whole life provides permanent protection with cash value accumulation. The right choice depends entirely on your timeline, budget, and whether you prioritize simplicity or long-term planning features.

Selecting the correct coverage amount matters far more than picking the cheapest policy. A $500,000 death benefit protects your family’s $500,000 home and replaces income during your children’s most dependent years, while a $300,000 benefit leaves gaps if your mortgage is larger or your family expenses are higher. Working through these numbers alone leads most families to either overinsure or underinsure, wasting money or leaving dangerous protection gaps.

Contact Archibald Insurance Agency to discuss your family’s protection needs with an agent who listens and compares real options. We’ll calculate the coverage amount that protects your household, show you term and permanent options side-by-side, and explain exactly what you’re paying for. Your family’s financial security is too important to leave to guesswork or outdated employer coverage.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation