Life Insurance Quotes Utah: Quick Comparisons for Smart Buyers

Getting life insurance quotes in Utah doesn’t have to be complicated. At Archibald Insurance Agency, we help Utah residents compare quotes quickly and find coverage that fits their budget and needs.

The right policy protects your family’s financial future. Let’s show you how to navigate quotes like a smart buyer.

Why Life Insurance Quotes Matter in Utah

Shopping around for life insurance in Utah isn’t optional if you want the best rate. The difference between the lowest and highest quote for identical coverage can exceed $100 per month. A 40-year-old male non-smoker seeking $500,000 in whole life coverage might pay anywhere from $400 to $600 monthly depending on the carrier. That’s a potential $2,400 annual difference that compounds over decades.

Compare Multiple Carriers to Find Your Best Price

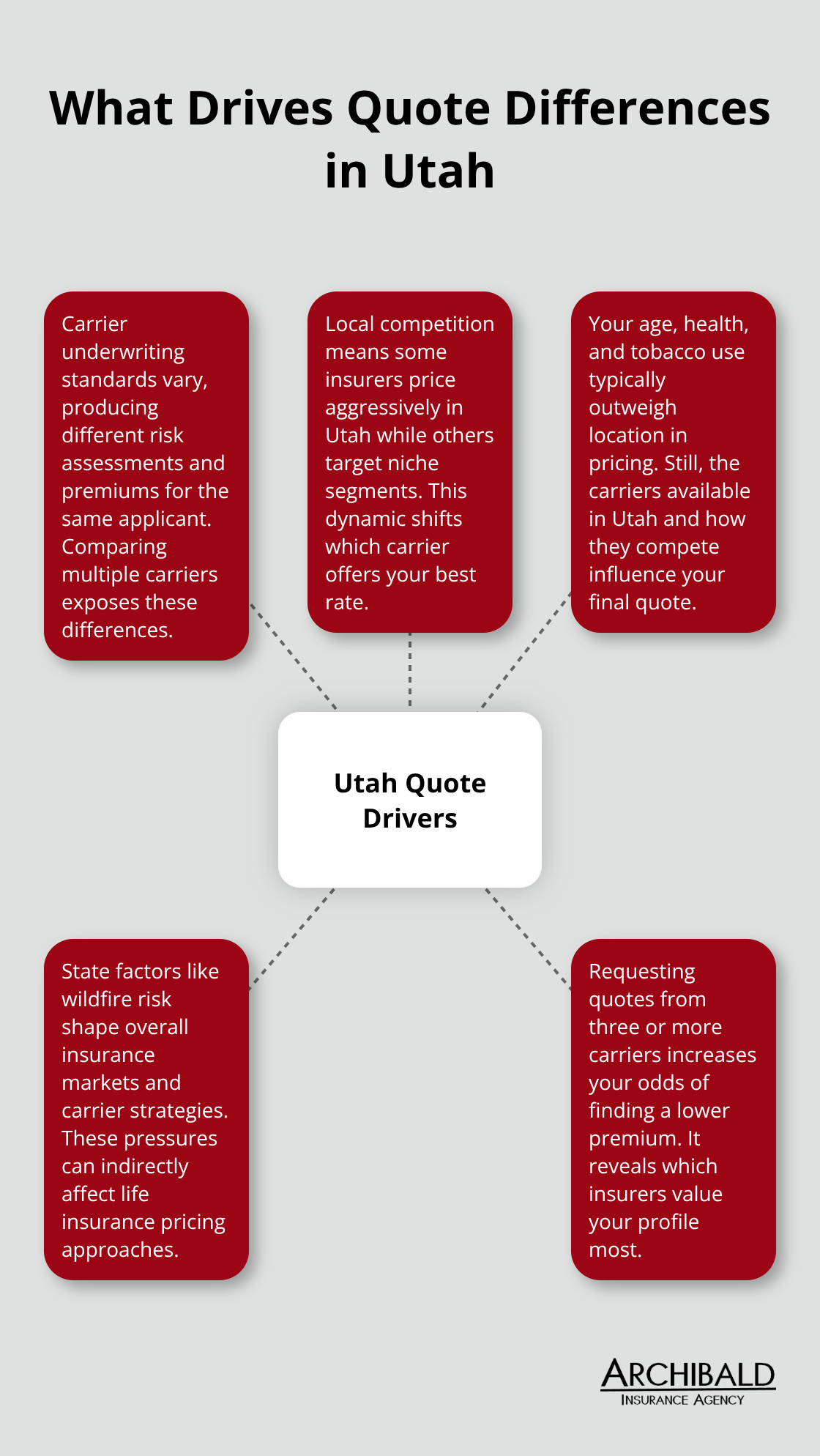

Utah’s insurance market includes major national players like Banner Life, USAA, and Pacific Life alongside regional options, each pricing policies differently based on their underwriting standards and risk models. Clients who request quotes from three or more carriers consistently identify better rates than those who accept the first offer. The variation exists because each insurer evaluates risk differently and competes for different customer segments. You’ll uncover which carriers value your specific profile most competitively in the Utah market rather than assuming national rates apply equally everywhere.

Calculate Your True Coverage Needs

Most people underestimate how much coverage they actually need. The common rule suggests 10 to 15 times your annual salary, but that’s a starting point, not a finish line. You’ll want to account for your mortgage balance, outstanding debts, your children’s college expenses, and final costs. A 35-year-old with a $300,000 mortgage, two kids, and $50,000 in other debt needs substantially more than someone with no dependents and a paid-off home. Consider using the DIME formula, which accounts for Debt, Income, Mortgage, and future expenses to determine your actual coverage needs. Once you know your target coverage amount, you can request accurate quotes that reflect what you truly require.

Understand How Utah’s Market Affects Your Quotes

Utah residents benefit from below-average homeowners insurance costs compared to the national market, but life insurance pricing varies based on local health demographics and carrier competition. Utah ranks number 9 nationally for homes at risk from wildfires, which influences overall insurance costs in the state. Some carriers price aggressively in Utah to gain market share, while others focus on specific segments like military families through USAA. Your age, health status, and smoking history matter far more than location, but the carriers available in Utah and their competitive positioning do affect your final quote.

With your coverage needs identified and an understanding of Utah’s market dynamics, you’re ready to explore the different types of life insurance available and how each one produces different quotes.

Types of Life Insurance and Quote Variations

Term Life Insurance Quotes and Affordability

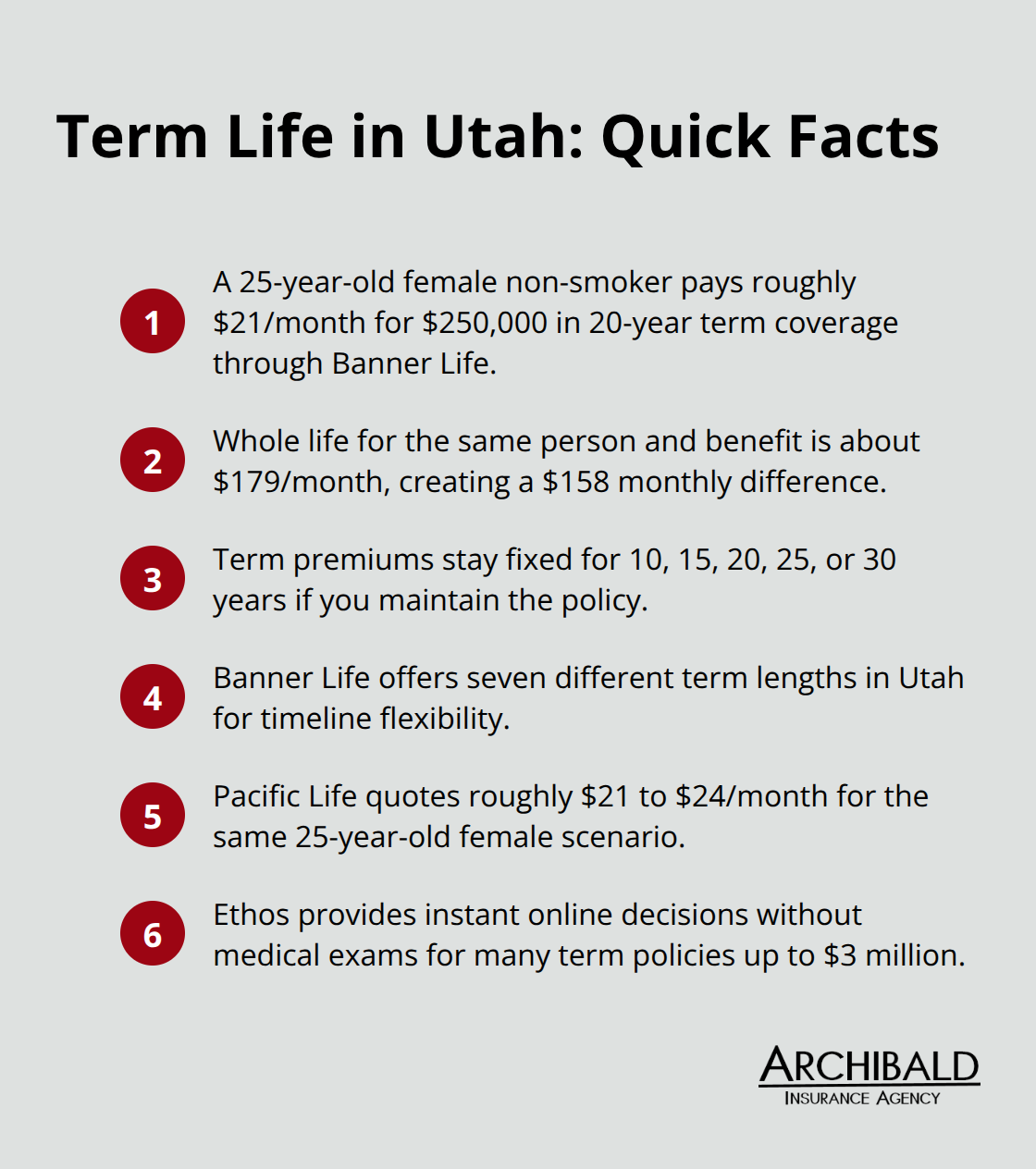

Term life insurance dominates Utah’s affordable quote landscape for good reason. A 25-year-old female non-smoker in Utah pays roughly $21 per month for $250,000 in 20-year term coverage through Banner Life, while the same person looking at whole life coverage costs approximately $179 per month for identical death benefit protection. That $158 monthly difference reveals why term life attracts younger families with temporary needs. Term quotes remain fixed for your chosen period-10, 15, 20, 25, or 30 years-meaning your premium never increases if you maintain the policy. Banner Life offers seven different term lengths in Utah, providing flexibility to match your coverage timeline to specific obligations like mortgage payoff dates or when your children finish college.

Pacific Life delivers comparable rates, quoting roughly $21 to $24 monthly for the same 25-year-old female scenario, while Ethos provides instant online decisions without medical exams for many term policies up to $3 million in coverage. The trade-off is straightforward: term life insurance expires after your selected period, offering no lifetime protection or cash value accumulation.

Whole Life Insurance and Long-Term Value

Whole life policies shift your quote equation entirely because they deliver permanent coverage and build cash reserves you can access during your lifetime. USAA’s whole life quotes in Utah show approximately $179 monthly for a 25-year-old woman with $250,000 coverage, compared to their universal life option at roughly $106 monthly for the same protection. At age 40, USAA whole life for $500,000 climbs to around $504 for women and $521 for men, demonstrating how permanent policies accelerate in cost as you age. Whole life policies accumulate cash value that grows tax-deferred and can be borrowed against, whereas term policies provide pure death benefit protection with zero cash component. To explore life insurance types and find the right coverage for your family’s financial security, consider consulting with a specialist who understands Utah’s unique market.

Universal Life Insurance Flexibility Options

Universal life provides the flexibility you need if your situation changes-you can adjust your death benefit and premium payments within policy limits without reapplying for coverage. Pacific Life offers universal life up to $10 million in coverage with no-exam options up to $3 million, appealing to those wanting substantial protection without medical underwriting. For Utah residents seeking permanent coverage, USAA dominates the market with an A++ financial strength rating from AM Best, while Pacific Life holds an A+ rating with one of the lowest complaint indices in the industry at 0.05 per the National Association of Insurance Commissioners.

Your quote comparison must weigh whether you need lifetime coverage with cash accumulation or temporary protection at the lowest possible monthly cost. Once you’ve identified which type aligns with your goals, comparing quotes and coverage options with a local specialist ensures you secure the right protection for your Utah family’s needs.

How to Get Accurate Life Insurance Quotes in Utah

Provide Complete Information for Honest Quotes

Requesting quotes without clear information produces estimates that won’t reflect your actual situation. You need to supply specific details: your exact age, current health status, whether you use tobacco products, your occupation, any pre-existing conditions, and your desired coverage amount and term length. Insurers underwrite based on these factors, and incomplete information produces quotes that may be substantially lower than your actual offer once underwriting begins. When you request quotes from multiple carriers without standardizing this information, you’re comparing apples to oranges. A 40-year-old male non-smoker in excellent health receives vastly different quotes than someone with high blood pressure or previous health issues, yet both might request identical $500,000 coverage. The solution is simple: provide the same information to each carrier and note exactly what you disclosed. This discipline reveals genuine price differences rather than quote variations from incomplete applications.

Understand Different Underwriting Paths

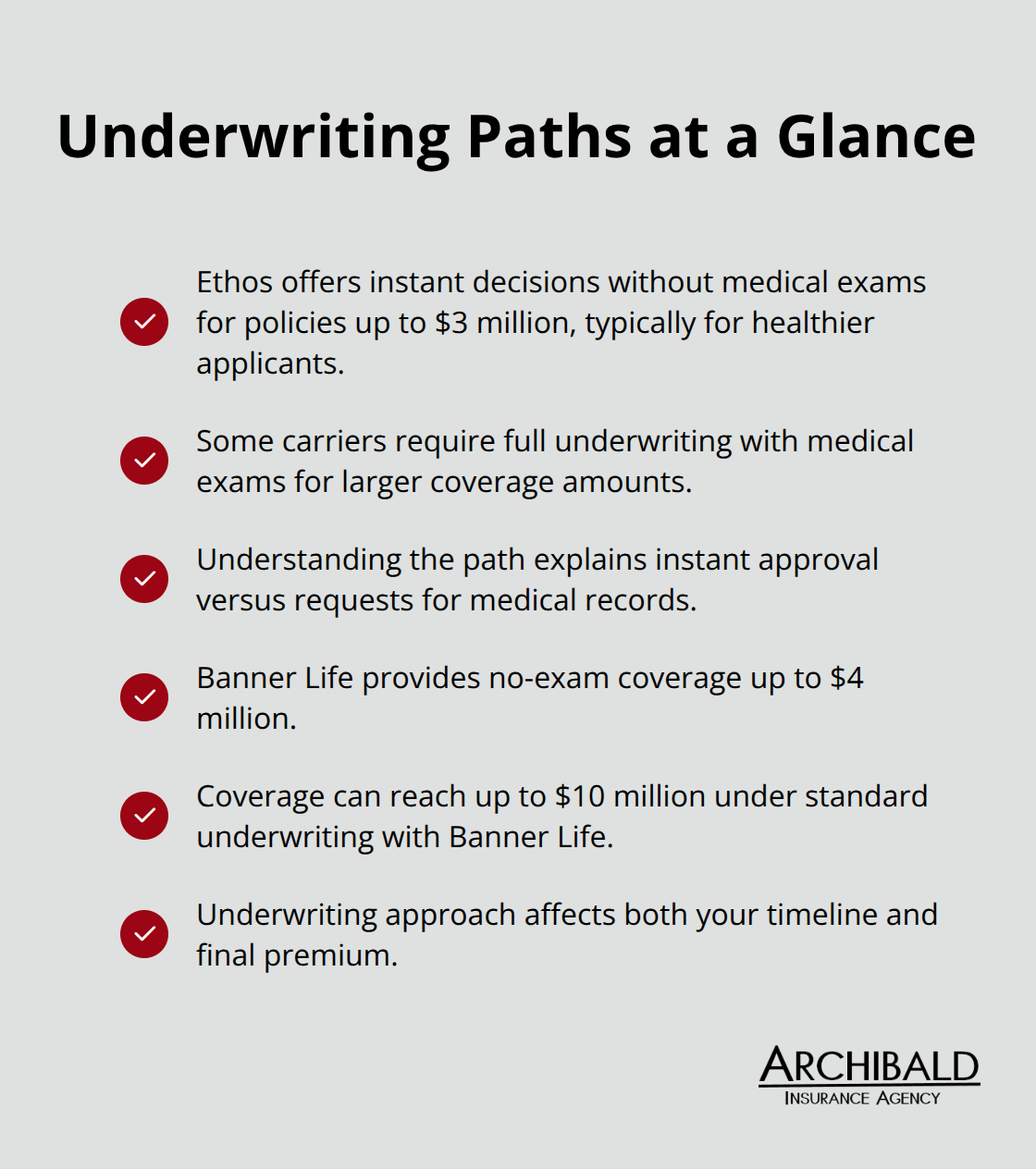

Some carriers like Ethos offer instant decisions without medical exams for policies up to $3 million, which accelerates the quote process but typically applies only to healthier applicants. Others require full underwriting with medical exams for larger coverage amounts. Understanding these underwriting paths before requesting quotes helps you interpret why one carrier provides instant approval while another requests medical records. Banner Life offers no-exam coverage up to $4 million, with the option to reach up to $10 million under standard underwriting.

These different approaches affect both your timeline and your final premium, so knowing which carriers match your health profile and urgency matters significantly.

Spot Red Flags in Quote Comparisons

Red flags appear when quotes seem too good to be true or when carriers avoid discussing policy exclusions and limitations. If a quote appears 30 percent lower than competitors for identical coverage, investigate whether the death benefit is truly equivalent or if the carrier applied different underwriting standards. Quotes significantly below typical benchmarks warrant scrutiny about what’s actually being offered. Another warning sign is when an agent pushes you toward permanent life coverage without understanding your actual needs or financial timeline. A 30-year-old with young children and a mortgage typically benefits more from 20-year term coverage than whole life, yet some agents prioritize higher commissions over appropriate recommendations.

Work with Agents Who Ask the Right Questions

Independent agents ask detailed questions about your goals, debts, dependents, and timeline before recommending specific products. Local Utah agents understand state-specific factors like wildfire risk affecting overall insurance costs and the competitive landscape among carriers operating here. They can explain why USAA dominates permanent life quotes for military families or why American Family offers competitive rates that sometimes create bundling opportunities affecting your overall insurance costs. An independent insurance agent representing multiple carriers provides genuine comparison ability rather than pushing one company’s products exclusively. Our approach means we represent numerous carriers and focus on matching your specific needs rather than promoting a single company’s offerings.

Evaluate Carrier Strength and Reliability

Financial strength ratings matter because they indicate whether a carrier will pay claims decades from now. USAA carries an A++ rating from AM Best, the highest designation available. These ratings reflect how well insurers manage claims and customer service over time. When you compare quotes, check the financial strength of each carrier alongside the premium cost. A slightly higher premium from a financially stronger carrier often provides better long-term value than saving $10 monthly with a weaker competitor.

Final Thoughts

Comparing life insurance quotes in Utah requires you to calculate your actual coverage needs before requesting quotes from multiple carriers. The 10 to 15 times annual salary rule provides a starting point, but your specific situation-mortgage balance, dependent ages, outstanding debts-determines your true need. Once you’ve identified that number, request quotes for identical coverage amounts across multiple carriers to reveal genuine price differences rather than variations from different coverage levels.

Term life insurance remains the most affordable option for younger families with temporary needs, while whole life and universal life serve those seeking permanent protection with cash value accumulation. Understanding which type matches your timeline and financial goals shapes your entire quote comparison process. Life insurance quotes in Utah reflect both national pricing trends and local market dynamics, with wildfire risk and carrier competition influencing what you’ll pay.

Work with an agent who asks detailed questions about your situation rather than pushing a single product. We at Archibald Insurance Agency represent multiple carriers and focus on matching your specific needs to the right coverage, and our team understands Utah’s insurance landscape well enough to explain why certain carriers compete aggressively in our state. Contact us to compare life insurance quotes and find protection that actually fits your family’s financial security.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation