Best Life Insurance Providers for Your Family’s Future

Life insurance is one of the most important financial decisions you’ll make for your family. At Archibald Insurance Agency, we help Utah families find the best life insurance providers that match their specific needs and budget.

Whether you’re just starting to explore your options or comparing coverage types, this guide walks you through everything you need to know. We’ll cover the different policy types, how to choose the right provider, and what happens during the application process.

Which Life Insurance Type Fits Your Family’s Situation

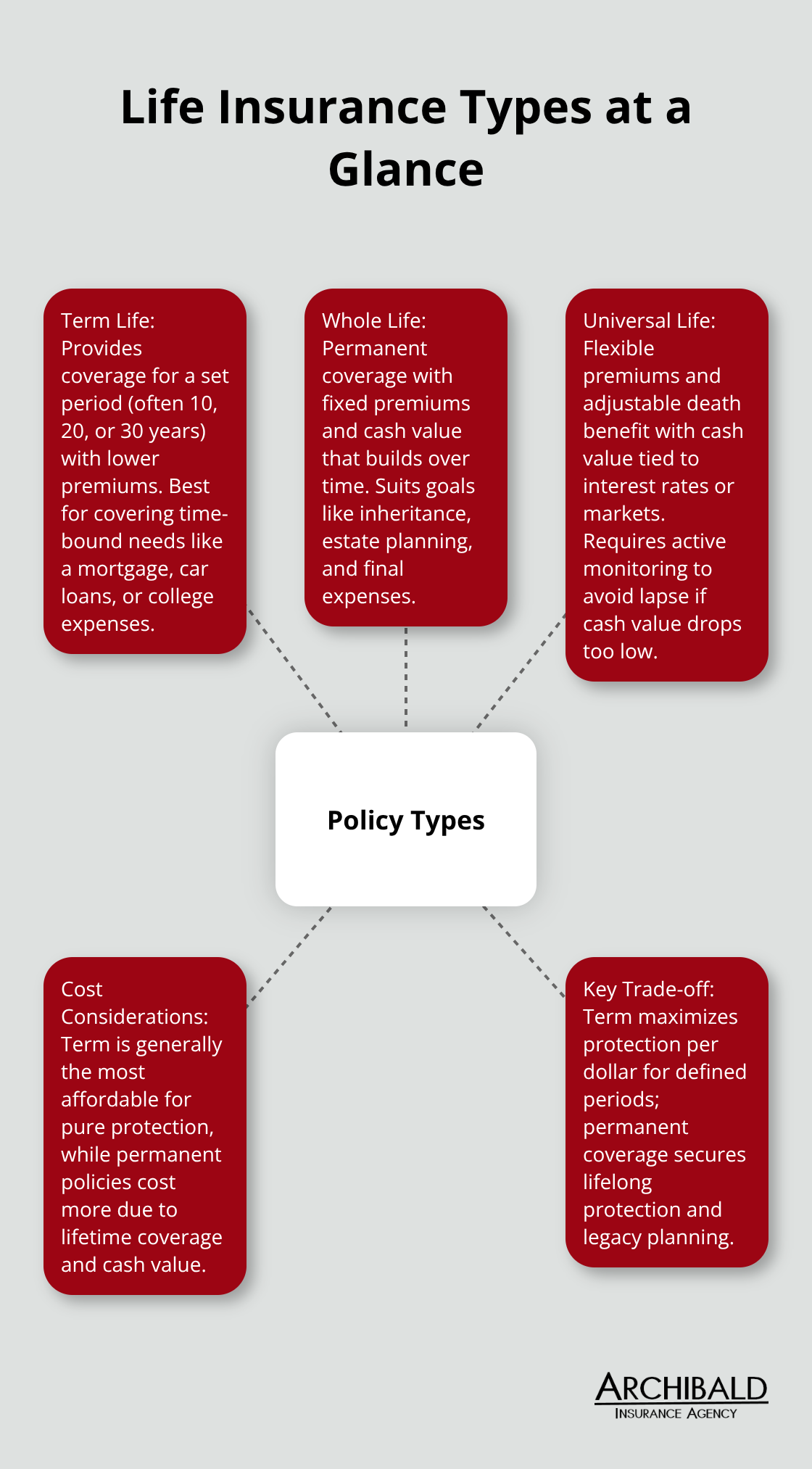

The three main life insurance types serve fundamentally different purposes, and picking the wrong one wastes money or leaves your family exposed. Term life insurance is the most straightforward option and typically costs 5 to 15 times less than whole life for the same coverage amount. Term policies lock in a fixed premium for a set period-commonly 10, 20, or 30 years-then expire. This structure makes term ideal if you have specific obligations ending at a known date, such as a mortgage, car loans, or college expenses. Once those debts are paid off or your children finish school, the coverage stops and you stop paying. The downside is straightforward: if you’re still alive when the term ends, you have no death benefit and no cash value to show for your premiums.

Permanent Coverage When You Need Lifelong Protection

Whole life insurance and universal life insurance both provide lifetime or extended coverage with a cash value component that grows over time. Whole life premiums stay fixed forever, and a portion of each payment accumulates as cash value that you can borrow against or withdraw. Whole life insurance and estate taxes appeal to people who plan for estate taxes, want to leave an inheritance, or seek permanent coverage for final expenses. Universal life offers more flexibility-you can adjust your premiums and death benefit within limits, and your cash value grows based on interest rates or market performance. However, permanent policies cost significantly more upfront. Universal life sits between term and whole life in cost but requires active monitoring because if cash value dips too low, your policy lapses and you lose coverage entirely.

Why Most Families Choose Term Life

Most families with straightforward needs should lean toward term life because the affordability lets you purchase sufficient coverage without financial strain. Term policies align well with major financial obligations that have defined endpoints. Your mortgage typically lasts 15 to 30 years, your children need support through their early twenties, and your working years have a natural conclusion around retirement age. Term life matches these timelines perfectly. You protect your family during the years when they depend on your income, then the policy expires when that need ends. This approach maximizes your protection dollars and prevents you from overpaying for coverage you no longer need.

When Permanent Life Makes Sense

Permanent life insurance becomes attractive in specific situations. If you have substantial assets and face potential estate taxes, permanent coverage provides a tax-free death benefit that your heirs can use to pay those taxes without selling family property or business interests. If you want to leave a guaranteed inheritance or fund a charitable legacy, permanent coverage delivers that promise. If you have dependents with special needs who will require lifelong support, permanent life ensures money is available regardless of when you pass away. These scenarios justify the higher cost because the coverage serves a purpose that extends beyond a fixed time period.

Evaluating Your Coverage Needs and Timeline

Start by listing your family’s financial obligations and when they end. Your mortgage payoff date, your youngest child’s college graduation, and your planned retirement age all matter. If most obligations end within 30 years, term life handles your needs efficiently. If you have ongoing obligations or estate planning goals that extend indefinitely, permanent life warrants consideration. The right choice depends on your specific situation, not on what sounds impressive or what a neighbor purchased. Once you understand which policy type aligns with your family’s timeline and goals, you can evaluate which providers offer the best rates, features, and service for that specific type of coverage.

Choosing the Right Life Insurance Provider

Calculate Your Coverage Need First

Selecting a life insurance provider requires matching three concrete factors: your actual coverage need in dollars, the rates that carrier charges for your age and health, and how quickly they approve applications. Start with coverage amount by calculating what your family would need if you died today. Add your outstanding debts (mortgage, car loans, credit cards), multiply your annual income by how many years you want to provide financial support for your survivors, and factor in final expenses. A 35-year-old with a $300,000 mortgage, two children, and $60,000 annual income typically needs $500,000 to $750,000 in coverage.

Compare Rates Across Multiple Carriers

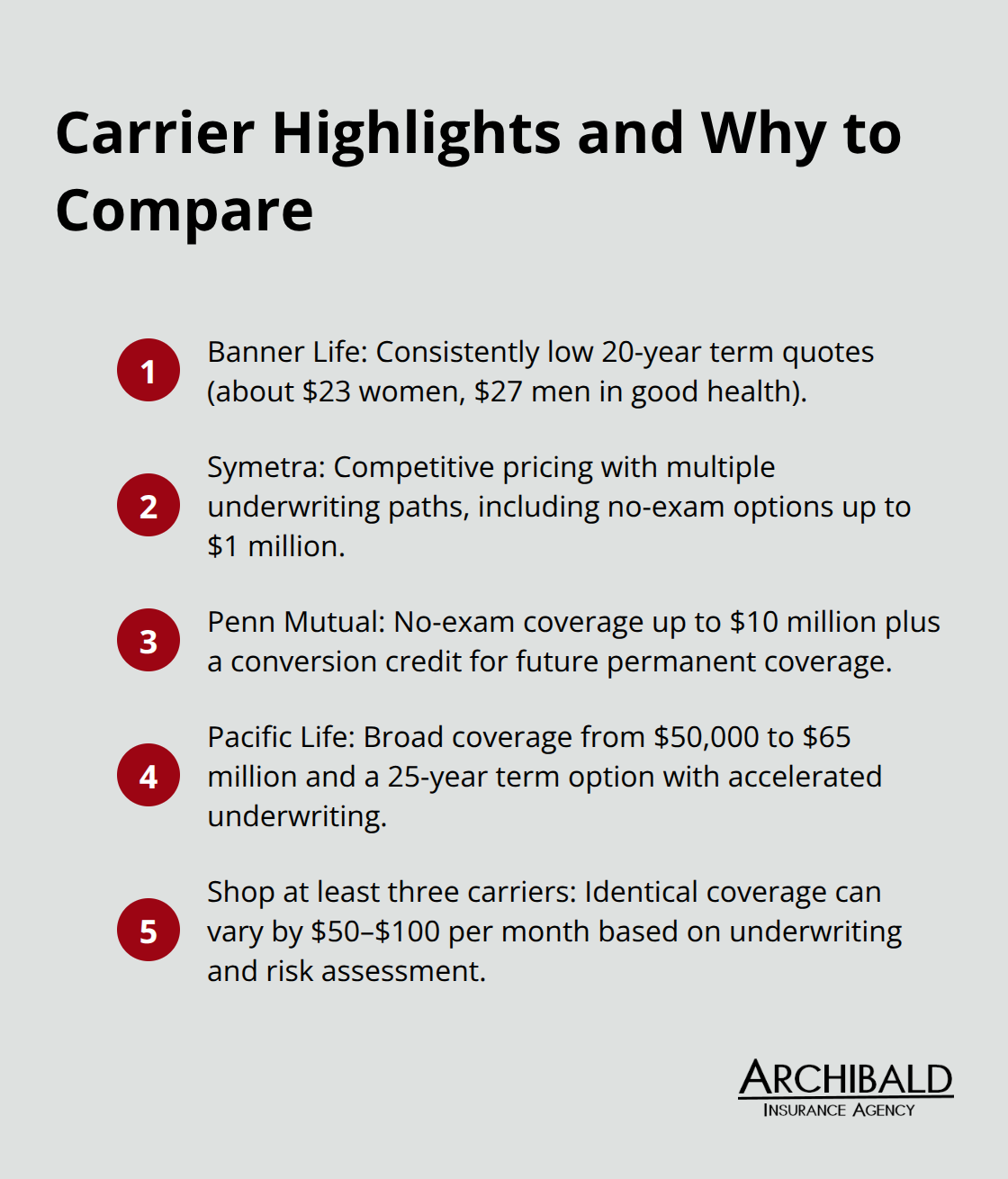

Once you know your target amount, pricing becomes the primary differentiator. Comparing rates across multiple carriers reveals significant differences in pricing. These rates vary significantly by carrier. Banner Life, which operates as Legal & General America, consistently ranks among the lowest-cost options in Utah with 20-year term quotes around $23 monthly for women and $27 for men in good health. Symetra offers similarly competitive pricing with multiple underwriting paths including no-exam options up to $1 million.

Penn Mutual extends coverage up to $10 million with no-exam underwriting and a conversion credit feature that helps applicants transition to permanent coverage later. Pacific Life covers an unusually broad range from $50,000 to $65 million and offers a 25-year term option alongside accelerated underwriting. Request illustrations from at least three carriers because rates for identical coverage can differ by $50 to $100 monthly depending on the company’s underwriting standards and risk assessment.

Evaluate Speed and Application Process

Beyond price, evaluate how each carrier handles the application process and claims. Banner Life and Symetra excel at speed, offering instant decisions for qualified applicants through streamlined underwriting that bypasses traditional medical exams. Pacific Life allows conversion to permanent coverage until age 70, giving you flexibility if your circumstances change. Nationwide distinguishes itself by including chronic, critical, and terminal illness riders on term policies, meaning you can access part of your death benefit while living if you face a serious diagnosis (providing liquidity without tapping other assets).

Assess Financial Strength and Claims Performance

Lincoln Financial stands apart for applicants with pre-existing conditions like heart disease or depression, offering favorable underwriting where other carriers impose heavy ratings or decline coverage. All major carriers carry A+ ratings from AM Best, indicating financial strength, but complaint frequency matters too. Lower NAIC complaint indices signal better customer experiences during claims. Utah law requires insurers to settle death claims within approximately 15 days after receiving proof of death, so verify each carrier’s actual track record on this timeline.

Get Side-by-Side Comparisons

Requesting quotes from multiple carriers simultaneously saves hours of individual applications and lets you see side-by-side comparisons of rates, features, and underwriting speed before committing to any provider. This approach reveals which carriers align with your timeline and budget. Once you’ve narrowed your choice to a specific provider and policy type, understanding what happens during the application process removes uncertainty from the next steps.

What Happens During the Application Process

The application process moves faster than most people expect, especially if you qualify for accelerated underwriting or no-exam options. When you submit an application, the carrier immediately reviews your age, gender, occupation, and stated health history. If you fall within their standard risk parameters, approval can happen within days rather than weeks. Banner Life and Symetra process qualified applications in as little as 48 hours, while carriers using traditional medical underwriting typically take 2 to 4 weeks.

No-Exam and Accelerated Underwriting Paths

The timeline depends entirely on whether you need a medical exam. No-exam policies up to $1 million through carriers like Symetra and Pacific Life skip the doctor visit entirely, relying instead on your medical records and prescription history. Accelerated underwriting uses data and technology to assess risk and may allow eligible applicants to skip a medical exam, though you may still need to answer detailed health questions or provide lab results if anything unusual is flagged.

Traditional Medical Underwriting

Traditional underwriting requires a paramedic to visit your home or workplace for blood pressure, blood samples, and urine tests. This adds 1 to 2 weeks to the timeline. Medical exams are thorough but straightforward: expect 30 to 45 minutes with basic vital signs, bloodwork, and a brief conversation about your health history. The exam itself costs nothing; the carrier pays the paramedic’s fee.

Health Questions and Honest Disclosure

Health questions during the application cut deeper than casual conversation. Carriers request a comprehensive health history detailing any pre-existing medical conditions, current prescription medications, past medical events, family history of early death or serious illness, smoking status, alcohol consumption, and occupational hazards. Complete honesty matters because misrepresenting your health voids the policy later. If you claim you don’t smoke but your medical records show otherwise, the insurer can deny death claims years into the policy. Lincoln Financial’s more lenient underwriting for pre-existing conditions like heart disease or depression doesn’t mean they ignore these facts; it means they’re willing to approve coverage at a standard or slightly higher rate rather than declining you outright.

Marijuana use receives different treatment across carriers. Lincoln Financial does not automatically classify daily marijuana use the same as tobacco, potentially saving you hundreds monthly in premiums compared to carriers treating it as a tobacco product. Document your medications, dosages, and the conditions they treat before your application. This speeds up the underwriting process significantly.

Timeline from Submission to Coverage

From application submission to policy approval and the first premium payment, expect 3 to 6 weeks for accelerated underwriting or 4 to 8 weeks for traditional medical underwriting. Utah law requires a 10-day free-look period after your policy arrives, giving you time to review the documents and cancel without penalty if something doesn’t match your expectations. Once approved, your policy becomes effective on the date you pay your first premium, and your family’s protection begins immediately.

Final Thoughts

Selecting the best life insurance providers for your family requires three concrete decisions: matching your coverage need to your family’s financial obligations, comparing rates across multiple carriers, and choosing a company that processes applications quickly. If you need affordable coverage for a defined period, Banner Life and Symetra offer competitive rates with streamlined underwriting, while Lincoln Financial’s favorable approach to pre-existing conditions makes them worth requesting a quote from if your health history includes complications. Pacific Life and Penn Mutual provide broader choices in coverage amounts and conversion options than many competitors.

Start by calculating your actual coverage need in dollars rather than guessing based on what sounds reasonable-add your debts, factor in income replacement for your family, and include final expenses. Request illustrations from at least three carriers simultaneously so you can compare rates side by side without spending weeks on individual applications. Utah law protects you with a 10-day free-look period after your policy arrives, so you have time to review everything before your coverage becomes final.

The application process moves faster than you might expect, especially with accelerated underwriting or no-exam options available through most major carriers (from submission to approval typically takes 3 to 8 weeks depending on whether you need a medical exam). Be honest about your health history and medications because misrepresenting facts voids your policy later. We at Archibald Insurance Agency help Utah families navigate these decisions and find coverage that protects their financial future without overpaying-contact us today to request quotes and speak with someone who understands your family’s specific needs.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation